Navigating a 520 Credit Score Car Loan: Your Expert Guide to Approval

Navigating a 520 Credit Score Car Loan: Your Expert Guide to Approval Carloan.Guidemechanic.com

Getting a car loan with a less-than-perfect credit score can feel like trying to climb a mountain in flip-flops. Especially when your credit score hovers around 520, the thought of securing financing for a vehicle might seem daunting, if not impossible. But here’s the good news: while challenging, it is absolutely not impossible.

As an expert in auto financing and credit, I’m here to tell you that a 520 credit score car loan is within reach, provided you approach it with the right knowledge, strategy, and realistic expectations. This comprehensive guide will equip you with everything you need to know, from understanding what your 520 score means to actionable steps for securing a loan and even improving your financial standing in the long run. We’ll dive deep into the nuances, reveal expert tips, and help you navigate the often-tricky world of subprime auto lending.

Navigating a 520 Credit Score Car Loan: Your Expert Guide to Approval

Understanding Your 520 Credit Score: What It Really Means

Before we talk about securing a car loan, let’s address the elephant in the room: your 520 credit score. In the world of credit, a score of 520 falls squarely into the "poor" or "subprime" category. FICO scores, which most lenders use, range from 300 to 850. Generally, anything below 580 is considered poor.

This classification signals to lenders that you represent a higher risk. Based on my experience, a low credit score often indicates a history of missed payments, high credit utilization, or even past bankruptcies. Lenders, naturally, are cautious when evaluating such profiles because they want assurance that their loan will be repaid.

The immediate impact of a 520 credit score on a car loan is significant. You’ll likely face higher interest rates, stricter loan terms, and potentially a more limited selection of vehicles. Lenders offering loans in this range are taking on more risk, and they compensate for that risk by charging more for the money they lend.

Is Getting a Car Loan with a 520 Credit Score Possible? The Definitive Answer

Yes, securing a car loan with a 520 credit score is indeed possible. However, it’s crucial to manage your expectations from the outset. You won’t walk into a dealership and get the same terms as someone with excellent credit. The process will require more preparation, potentially more legwork, and a willingness to accept different conditions.

Lenders who specialize in bad credit car loans understand that financial setbacks happen. They are in the business of lending to individuals with subprime credit, but they also have safeguards in place. Your job is to present yourself as the most reliable borrower you can be, despite your credit history. This involves demonstrating financial stability and taking proactive steps to mitigate their perceived risk.

Expert Strategies to Boost Your Chances of Approval

Securing a 520 credit score car loan isn’t about magic; it’s about strategy. Here are several proven methods that, based on my extensive experience, significantly increase your approval odds and can even lead to more favorable terms.

1. Increase Your Down Payment

This is arguably one of the most impactful strategies you can employ. A larger down payment directly reduces the amount you need to borrow, which in turn lowers the lender’s risk. If you have a substantial amount of your own money invested in the car, the lender sees you as more committed and less likely to default.

Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price as a down payment. If you can manage more, even better. Not only does it make you a more attractive borrower, but it also reduces your monthly payments and the total interest paid over the life of the loan. Saving up for a down payment, even if it delays your car purchase by a few months, is often a wise financial move.

2. Find a Reliable Co-Signer

A co-signer can be a game-changer when you’re seeking a 520 credit score car loan. A co-signer, typically a friend or family member with good or excellent credit, essentially guarantees the loan. Their credit history and financial stability act as a safety net for the lender.

When you have a co-signer, the lender considers both your credit profiles. This can lead to approval for a loan you might not get on your own, and potentially even a lower interest rate. However, it’s vital to understand the implications: if you miss payments, your co-signer is equally responsible, and their credit will suffer. Choose a co-signer wisely and ensure both parties fully understand the commitment.

3. Improve Your Credit Score (Even Slightly)

While a significant credit score overhaul takes time, even minor improvements can make a difference. Before applying for a loan, get copies of your credit reports from all three major bureaus (Experian, Equifax, and TransUnion). You can do this for free annually at AnnualCreditReport.com.

Scrutinize these reports for any errors or inaccuracies. Disputing and correcting errors can sometimes provide a quick, albeit small, bump to your score. Additionally, try to pay down any small outstanding debts, like credit card balances. Lowering your credit utilization ratio (the amount of credit you’re using versus the amount available) can positively impact your score relatively quickly. Avoid opening any new credit accounts in the months leading up to your car loan application, as new inquiries can temporarily lower your score. For more in-depth strategies on rapid improvement, read our guide on .

4. Opt for a Less Expensive Vehicle

When your credit score is 520, affordability should be your primary concern, not luxury. A lower-priced vehicle translates to a smaller loan amount, which means less risk for the lender. This can significantly increase your chances of approval.

Focus on reliable, used cars that meet your transportation needs without breaking the bank. A $10,000 car loan is much easier for a subprime lender to approve than a $30,000 loan. This approach also keeps your monthly payments manageable, making it easier to pay on time and rebuild your credit.

5. Gather All Necessary Documentation

Being prepared demonstrates responsibility and financial stability. Before you even speak to a lender, gather all required documents. This typically includes:

- Proof of income (pay stubs, bank statements, tax returns)

- Proof of residency (utility bill, lease agreement)

- Valid driver’s license

- Proof of insurance (or willingness to obtain it)

- List of references (sometimes requested)

Having these documents ready streamlines the application process and shows the lender you are serious and organized. Lenders want to see a clear picture of your current financial situation, especially your ability to consistently make payments.

6. Consider a "Buy Here, Pay Here" Dealership (with Caution)

"Buy Here, Pay Here" (BHPH) dealerships are known for their willingness to approve car loans for individuals with very low credit scores, including those with a 520 credit score. They act as both the seller and the lender, cutting out traditional banks or credit unions.

The primary advantage is their high approval rate, as they focus more on your income stability than your credit history. However, common mistakes to avoid are not fully understanding the terms. BHPH loans often come with significantly higher interest rates, shorter repayment terms, and may not report your payments to all three credit bureaus. This means while you get a car, it might not help you rebuild your credit as effectively as a traditional loan. Always read the fine print and compare their offers thoroughly.

Where to Apply for a Car Loan with a 520 Credit Score

Knowing where to apply is just as important as knowing how to prepare. Not all lenders are equipped or willing to work with subprime credit.

1. Online Lenders Specializing in Bad Credit

Many online lenders have emerged specifically to cater to individuals with low credit scores. They often have streamlined application processes and can provide pre-approvals quickly. These lenders typically have a network of financial institutions that are more flexible with their lending criteria.

Pros of online lenders include convenience, the ability to compare multiple offers from various lenders without affecting your credit score too much (initial soft inquiries), and often a faster decision-making process. They are a great starting point for understanding your options without commitment.

2. Credit Unions

Don’t overlook local credit unions. Unlike large commercial banks, credit unions are member-owned and often more willing to work with members who have a challenging credit history. They may offer more flexible terms or slightly lower interest rates than traditional banks for subprime borrowers.

To apply at a credit union, you’ll need to become a member, which usually involves meeting certain eligibility criteria (e.g., living in a specific area, working for a particular employer). Their personalized approach can be a significant advantage when seeking a 520 credit score car loan.

3. Dealerships (Finance Department)

Many dealerships have finance departments that work with a variety of lenders, including those who specialize in subprime auto loans. This can be a convenient "one-stop shop" solution, as they can help you find a car and arrange financing simultaneously.

However, be prepared for potential markups on interest rates. Dealerships often add their own fees to the lender’s offered rate. It’s always a good idea to get a pre-approval from an external lender (like an online lender or credit union) before stepping onto the lot. This way, you have a benchmark to compare against and can negotiate more effectively. For more insights on securing auto loans, check out this external resource on Understanding Auto Loan Basics.

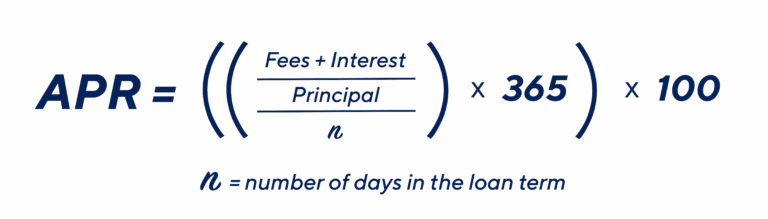

What to Expect: Interest Rates and Loan Terms

With a 520 credit score, you should anticipate higher interest rates. This is the reality of subprime lending. While excellent credit scores might see APRs in the single digits, a subprime car loan could have an APR anywhere from 15% to 25% or even higher, depending on market conditions, the lender, and your specific financial profile.

You might also be offered longer loan terms, such as 60, 72, or even 84 months. While longer terms result in lower monthly payments, they also mean you’ll pay significantly more in interest over the life of the loan. It’s a trade-off: manageable monthly payments versus higher total cost. Always do the math to understand the total amount you will repay.

The Application Process: Step-by-Step

Here’s a simplified breakdown of how to navigate the car loan application process with a 520 credit score:

- Get Pre-Approved: Start by getting pre-approved from one or two online lenders or your credit union. This gives you a realistic idea of what you qualify for and the interest rates you might face. It also provides leverage when negotiating with dealerships.

- Compare Offers: Don’t jump at the first offer. Compare interest rates, loan terms, and any associated fees from multiple lenders. This comparison is critical to finding the best possible deal.

- Choose Your Vehicle Wisely: Based on your pre-approval amount and your budget, select a vehicle that is reliable and affordable. Remember, a less expensive car is easier to finance.

- Negotiate: If you’re at a dealership, negotiate not just the car price, but also the financing terms. Having a pre-approval in hand gives you a stronger position.

- Read the Fine Print: Before signing anything, thoroughly read the entire loan agreement. Understand all terms, conditions, penalties for late payments, and any additional fees. Ask questions until everything is crystal clear.

Post-Approval: Building a Better Financial Future

Getting a car loan with a 520 credit score isn’t just about getting a car; it’s an opportunity to rebuild your credit. Once approved, your mission shifts to demonstrating responsible financial behavior.

Make Timely Payments: This is the single most important action you can take. Every on-time payment reported to the credit bureaus will gradually improve your credit score. Set up automatic payments or calendar reminders to ensure you never miss a due date.

Refinancing Opportunities: After 12-18 months of consistent, on-time payments, your credit score will likely have improved. At this point, you may qualify to refinance your car loan at a lower interest rate. Refinancing can significantly reduce your monthly payments and the total interest paid over the remaining term of the loan.

This car loan, if managed properly, can be a powerful tool for your financial recovery. For more details on how car loans can influence your financial standing, explore our article on .

Common Mistakes to Avoid When Seeking a Bad Credit Car Loan

Navigating the subprime lending landscape requires vigilance. Avoid these common pitfalls:

- Applying Everywhere: Each loan application results in a "hard inquiry" on your credit report, which can temporarily lower your score. Limit your applications to a few trusted lenders within a short timeframe (usually 14-45 days), as multiple auto loan inquiries within this period are often treated as a single inquiry by credit scoring models.

- Not Reading the Fine Print: As mentioned, high interest rates and unfavorable terms can be hidden in complex language. Always understand what you’re signing.

- Ignoring the Total Cost: Focus on the total amount you will repay, not just the monthly payment. A lower monthly payment over a longer term often means a much higher total cost.

- Buying More Car Than You Can Afford: This is a recipe for financial stress and potential default. Stick to your budget and prioritize reliability over luxury.

- Settling for the First Offer: Always compare offers. Competition among lenders can work in your favor.

Conclusion

Obtaining a 520 credit score car loan is a journey that requires patience, research, and a strategic approach. While the path might be more challenging due to higher interest rates and stricter terms, it is certainly navigable. By focusing on a substantial down payment, considering a reliable co-signer, diligently preparing your documentation, and choosing the right lenders, you significantly increase your chances of approval.

More importantly, this loan isn’t just about getting a vehicle; it’s an opportunity. It’s your chance to demonstrate financial responsibility, make consistent on-time payments, and begin the crucial process of rebuilding your credit score. Use this experience as a stepping stone to a stronger financial future, where better credit means better opportunities. Start planning today, gather your resources, and drive confidently toward your next car and improved credit.