Navigating a 523 Credit Score Car Loan: Your Comprehensive Guide to Getting Approved

Navigating a 523 Credit Score Car Loan: Your Comprehensive Guide to Getting Approved Carloan.Guidemechanic.com

Securing a car loan when your credit score hovers around 523 can feel like an uphill battle. Many people find themselves in this challenging situation, perhaps due to past financial setbacks, limited credit history, or unforeseen circumstances. The good news is that while it presents significant hurdles, obtaining a 523 credit score car loan is not impossible.

This comprehensive guide is designed to empower you with the knowledge and strategies needed to navigate the complexities of financing a vehicle with less-than-perfect credit. We’ll delve deep into what a 523 score means for car loans, the obstacles you’ll encounter, and most importantly, the actionable steps you can take to increase your chances of approval. Our goal is to provide you with a clear roadmap, ensuring you understand every aspect of this journey.

Navigating a 523 Credit Score Car Loan: Your Comprehensive Guide to Getting Approved

Understanding Your 523 Credit Score

A credit score of 523 falls squarely into the "Poor" or "Very Poor" category, according to major credit bureaus like FICO and VantageScore. This numerical representation of your creditworthiness signals to lenders that you may carry a higher risk of defaulting on a loan. It’s a snapshot of your past financial behavior, including payment history, amounts owed, length of credit history, new credit, and credit mix.

Lenders rely heavily on this score to assess the likelihood of you repaying your debts. A lower score suggests a history of missed payments, high credit utilization, or possibly bankruptcies, making them more hesitant to lend. Consequently, securing a 523 credit score car loan will present unique challenges compared to someone with excellent credit.

Based on my experience, lenders view scores in this range as indicative of significant financial risk. This means they will likely scrutinize your application much more closely, looking for any mitigating factors. They are essentially trying to balance their desire to lend with the need to protect their investment.

Is Getting a Car Loan with a 523 Credit Score Possible?

Yes, getting a car loan with a 523 credit score is indeed possible, but it requires a strategic approach and realistic expectations. While traditional lenders like major banks might be reluctant, a segment of the auto finance industry specializes in what are known as "subprime" loans. These loans are specifically designed for individuals with lower credit scores.

Subprime lenders are willing to take on higher risks, but they offset this risk by imposing stricter terms and conditions. This typically translates into higher interest rates, larger down payment requirements, and sometimes shorter loan terms. It’s crucial to understand that while approval is within reach, the cost of borrowing will be significantly higher than for someone with a good credit score.

The key is to thoroughly research your options and prepare your financial profile as much as possible before approaching lenders. Don’t let the low score discourage you entirely; instead, view it as a signal to be extra diligent in your search. With the right strategy, you can find a lender willing to work with your situation.

The Challenges You’ll Face with a Low Credit Score

Navigating the auto loan market with a 523 credit score means you’ll encounter several common challenges. Being aware of these obstacles upfront will help you prepare and avoid potential pitfalls. Understanding these points is crucial for anyone seeking a 523 credit score car loan.

Higher Interest Rates (APR)

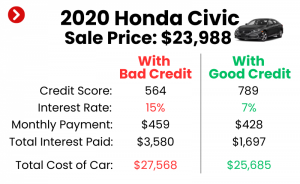

This is perhaps the most significant challenge. Lenders compensate for the increased risk associated with a low credit score by charging much higher Annual Percentage Rates (APRs). While someone with excellent credit might secure an APR of 3-5%, you could be looking at rates upwards of 15%, 20%, or even 25% or more.

A higher APR dramatically increases the total cost of your car over the life of the loan. Even a small difference in the interest rate can add thousands of dollars to your overall repayment. It’s essential to calculate the total cost, not just the monthly payment, when comparing offers.

Larger Down Payments

Lenders often require a more substantial down payment from borrowers with poor credit. A significant down payment reduces the loan amount, thereby lowering the lender’s risk. It also demonstrates your commitment and ability to save.

Expect to put down anywhere from 10% to 20% or even more of the vehicle’s purchase price. While this might seem like a barrier, it’s also a powerful tool to improve your chances of approval and secure better terms. The more you can put down, the better your position.

Stricter Loan Terms

Loan terms for subprime borrowers can also be more rigid. You might find fewer options for long repayment periods, or conversely, be pushed towards longer terms to lower monthly payments, which ultimately means paying more interest over time. Lenders might also impose specific requirements regarding vehicle age or mileage.

Additionally, the lender might require additional documentation or more frequent reporting on your part. Understanding these terms completely before signing any agreement is paramount. Don’t hesitate to ask questions about anything unclear.

Limited Vehicle Options

With a 523 credit score, your options for vehicles might be more restricted. Lenders are typically more comfortable financing a reliable, affordable used car rather than a brand-new, expensive model. This is because the depreciation of new cars adds another layer of risk.

Focusing on a more economical vehicle that meets your needs, rather than your desires, is a practical strategy. This approach makes you a less risky borrower and opens up more possibilities for approval. Prioritize reliability and affordability above all else.

Potential for Predatory Lenders

Unfortunately, the subprime market can attract less scrupulous lenders who prey on desperate borrowers. These lenders might offer seemingly easy approvals but with excessively high interest rates, hidden fees, or unfavorable terms. Common mistakes to avoid are accepting the first offer without comparison or signing documents you don’t fully understand.

Always be wary of deals that sound too good to be true, or lenders who pressure you into making quick decisions. Thorough research and a critical eye are your best defenses against predatory practices. Always ensure the lender is reputable and transparent.

Strategies for Securing a Car Loan with a 523 Credit Score

Despite the challenges, several effective strategies can significantly improve your chances of obtaining a 523 credit score car loan. Implementing these approaches will not only help you get approved but also potentially secure more favorable terms. Each strategy aims to mitigate the risk in the eyes of the lender.

1. Save for a Significant Down Payment

As mentioned, a substantial down payment is one of your most powerful tools. It directly reduces the amount you need to borrow, which in turn reduces the lender’s risk exposure. The more cash you can put down, the more attractive you become as a borrower.

Aim for at least 10-20% of the car’s purchase price, if possible. Not only does this improve your approval odds, but it also lowers your monthly payments and the total interest paid over the life of the loan. Start saving diligently as soon as you consider buying a car.

2. Consider a Co-signer

Enlisting a co-signer with good credit can dramatically improve your chances of approval and help you secure a better interest rate. A co-signer essentially guarantees the loan, promising to make payments if you default. Their good credit score offsets your lower score.

Pro tips from us: Ensure your co-signer understands the full responsibility they are undertaking. If you fail to make payments, their credit score will also be negatively impacted. Choose someone you trust implicitly, and who trusts you, like a family member or close friend, and have an open conversation about the risks and responsibilities involved.

3. Opt for a Used, Affordable Vehicle

Resist the temptation to buy a new, expensive car. Lenders are much more willing to finance a less expensive, reliable used vehicle. A lower purchase price means a smaller loan amount, which translates to lower risk for the lender and easier approval for you.

Focus on practical, fuel-efficient models known for their reliability and lower maintenance costs. This approach demonstrates financial prudence and makes your overall loan more manageable. Look for vehicles that hold their value well and have a solid service history.

4. Explore Dealerships Specializing in Bad Credit Loans

Some dealerships, often referred to as "Buy Here, Pay Here" lots, specialize in working with borrowers with poor credit. These dealerships typically offer in-house financing, meaning they are both the seller and the lender. This can make approval easier, as they are more focused on your ability to pay rather than solely on your credit score.

However, "Buy Here, Pay Here" loans often come with higher interest rates and less flexible terms. Always compare their offers with those from other subprime lenders or credit unions before committing. Carefully read all contracts and understand the full cost.

5. Get Pre-approved (with caution)

Getting pre-approved for a loan can give you a clear idea of what you can afford and demonstrates to dealerships that you’re a serious buyer. However, be mindful of the difference between "soft" and "hard" credit inquiries. A soft inquiry won’t impact your score, but a hard inquiry (which usually happens during a pre-approval or application) can temporarily lower it.

Limit your applications to a few lenders within a short timeframe (typically 14-45 days, depending on the scoring model). This allows multiple hard inquiries for the same type of loan to be counted as a single inquiry, minimizing the impact on your credit score. Shop around for the best rates and terms.

6. Provide Proof of Stable Income and Employment

Lenders want assurance that you have the financial capacity to repay the loan. Strong proof of stable income and consistent employment can significantly bolster your application, even with a low credit score. This is where your current financial stability can override past credit issues.

Be prepared to provide recent pay stubs, bank statements, tax returns, and employer contact information. Demonstrate a consistent work history and sufficient income to cover the monthly payments, along with your other living expenses. The more evidence you can offer of financial responsibility, the better.

7. Offer Collateral (if applicable and wise)

While less common for standard car loans, offering additional collateral (such as another paid-off vehicle or property) could potentially secure better terms. This reduces the lender’s risk even further. However, this is a significant step and should be considered very carefully.

Understand that if you default on the car loan, you could lose the additional collateral. This option is typically only considered in very specific circumstances and after exhausting other strategies. Always weigh the risks against the potential benefits.

The Application Process: What to Expect

Once you’ve implemented these strategies, it’s time to face the application process for your 523 credit score car loan. Knowing what to expect can help reduce stress and ensure you’re prepared. This stage is where all your preparation comes to fruition.

Required Documents

Lenders will typically ask for a range of documents to verify your identity, income, and residency. Be ready with:

- Government-issued ID: Driver’s license or state ID.

- Proof of income: Recent pay stubs, W-2s, or tax returns (if self-employed).

- Proof of residency: Utility bill or lease agreement.

- Proof of insurance: You’ll need to show you have adequate coverage before driving off the lot.

- Bank statements: To show financial stability and available funds for a down payment.

- References: Sometimes required, especially for "Buy Here, Pay Here" dealerships.

Having these documents organized and readily available will streamline the application process. Any delays in providing documentation can slow down your approval.

Credit Checks (Multiple Inquiries)

When you apply for a loan, lenders will perform a hard inquiry on your credit report. As discussed, multiple hard inquiries for the same type of loan within a specific window (usually 14-45 days) are often grouped together by credit scoring models to minimize impact. However, too many disparate applications can still lower your score.

Focus your applications on a few well-researched lenders or dealerships. This strategic approach helps protect your credit score from excessive dips. Be transparent about your credit history; honesty can build trust with potential lenders.

Negotiating Terms

Even with a 523 credit score, there might be some room for negotiation, especially if you’ve prepared well with a substantial down payment or a co-signer. Focus on negotiating:

- The total price of the vehicle: Don’t just focus on the monthly payment.

- The down payment amount: See if they’ll accept slightly less than initially asked.

- The interest rate (APR): Even a quarter of a percentage point can save you money.

- The loan term: A shorter term means higher monthly payments but less interest paid overall.

Pro tips from us: Always negotiate the car price first, before discussing financing. This ensures you’re getting a fair deal on the vehicle itself. Don’t be afraid to walk away if the terms are unfavorable. For more information on understanding auto loan terms, you can consult trusted external resources like the Consumer Financial Protection Bureau (Link to CFPB on auto loans).

Reading the Fine Print

This is arguably the most critical step. Before signing any loan agreement, read every single word of the contract. Pay close attention to:

- The total loan amount and total repayment amount.

- The APR: Ensure it matches what was quoted.

- Any hidden fees: Origination fees, processing fees, documentation fees.

- Prepayment penalties: Can you pay off the loan early without extra charges?

- Late payment penalties: Understand the consequences of missing a payment.

- Any clauses about repossession or default.

If you don’t understand something, ask for clarification. Don’t let anyone pressure you into signing before you’re fully comfortable. This contract is a significant financial commitment.

Improving Your Credit Score Before Applying

While it might delay your car purchase, taking steps to improve your credit score before applying for a 523 credit score car loan is the best long-term strategy. Even a small increase can open doors to better loan terms and significantly reduce your total cost of ownership. This proactive approach shows lenders you are serious about managing your finances.

Pay Bills On Time

Your payment history is the most crucial factor in your credit score. Make every effort to pay all your bills—credit cards, utilities, rent, and any existing loan payments—on time, every time. Set up automatic payments or reminders to avoid missing due dates.

Consistent on-time payments demonstrate reliability and responsibility, which lenders value highly. Even a few months of perfect payment history can start to nudge your score upwards. This habit is the cornerstone of good financial health.

Reduce Existing Debt

High credit utilization (the amount of credit you’re using compared to your total available credit) can significantly drag down your score. Focus on paying down credit card balances to reduce your utilization ratio. Aim to keep it below 30%, but ideally even lower.

Reducing your debt not only improves your credit score but also frees up more of your income, making your car loan payments more manageable. This shows lenders you have capacity for new debt.

Check Your Credit Report for Errors

Errors on your credit report are surprisingly common and can negatively impact your score without you even knowing. Obtain free copies of your credit report from all three major bureaus (Experian, Equifax, and TransUnion) annually via AnnualCreditReport.com.

Review each report meticulously for inaccuracies, such as accounts that aren’t yours, incorrect payment statuses, or outdated negative information. If you find errors, dispute them immediately with the credit bureau. Correcting these errors can sometimes boost your score quickly. For a more in-depth guide on how to improve your credit score, check out our dedicated article: .

Alternatives to a Traditional Car Loan

Sometimes, a traditional 523 credit score car loan simply isn’t the best option, or perhaps it’s not immediately available. Exploring alternatives can provide temporary solutions or even lead to better long-term financial outcomes. Consider these options if you’re struggling to secure favorable terms.

Saving Up to Buy Cash

The most financially sound option, if feasible, is to save up enough money to purchase a used car with cash. This eliminates the need for a loan, meaning no interest payments, no credit checks, and no monthly obligations. It offers complete financial freedom regarding your vehicle.

While it might take longer to save, it prevents you from entering into a high-interest loan that could exacerbate your financial situation. Even saving a substantial portion for a larger down payment and a smaller loan is a step in the right direction.

Public Transportation/Ridesharing

If immediate vehicle ownership isn’t critical, relying on public transportation, carpooling, or ridesharing services can be a viable interim solution. This allows you to avoid the costs and commitments of car ownership while you work on improving your financial standing.

Use the money you would have spent on car payments, insurance, and maintenance to save for a down payment or pay down existing debt. This strategic pause can set you up for a much better deal in the future.

Borrowing from Family/Friends (with formal agreement)

If you have supportive family members or friends, they might be willing to lend you money for a car. This can be a much more affordable option, often with little to no interest. However, it’s crucial to approach this arrangement with the utmost professionalism.

Draw up a formal loan agreement outlining the loan amount, repayment schedule, and any interest agreed upon. Treat it like a professional loan to protect the relationship and ensure clear expectations. Defaulting on a loan from a loved one can have severe personal consequences.

After Approval: Managing Your 523 Credit Score Car Loan

Congratulations on securing your 523 credit score car loan! This isn’t just about getting a car; it’s also a significant opportunity to rebuild your credit and improve your financial future. How you manage this loan will have a lasting impact.

Make Payments On Time, Every Time

This cannot be stressed enough. Consistent, on-time payments are paramount. Every payment you make on time will be reported to the credit bureaus and will positively contribute to your payment history, the most impactful factor in your credit score.

Set up automatic payments from your bank account to ensure you never miss a due date. Even if you have to adjust your budget, prioritize your car loan payment. This is your chance to demonstrate financial reliability.

Potential for Refinancing Later

As you consistently make on-time payments and your credit score improves, you might become eligible for refinancing your car loan at a lower interest rate. After 6-12 months of perfect payments, check your credit score and explore refinancing options.

Refinancing can significantly reduce your monthly payments and the total interest paid over the life of the loan. It’s a reward for responsible financial behavior and a smart move to save money in the long run.

How This Loan Can Rebuild Credit

A subprime car loan, managed responsibly, can be a powerful tool for credit rebuilding. By demonstrating that you can handle a significant installment loan, you show lenders that you are a more reliable borrower. This positive payment history will slowly but surely pull your credit score upwards.

As your score improves, you’ll gain access to better financial products, including lower interest rates on future loans and credit cards. View this loan as an investment in your financial future, not just a means to get a car. For more details on how various loans, including subprime auto loans, can impact your credit, check out our article: .

Conclusion: Your Roadmap to a 523 Credit Score Car Loan

Obtaining a 523 credit score car loan is undeniably challenging, but it is far from impossible. This comprehensive guide has laid out the realities of borrowing with a low credit score, from the higher interest rates and larger down payments to the limited vehicle options. More importantly, we’ve equipped you with a robust set of strategies to overcome these obstacles.

By focusing on a significant down payment, considering a co-signer, opting for an affordable used vehicle, and diligently preparing your financial documentation, you can significantly enhance your approval odds. Remember to research thoroughly, compare offers, and always read the fine print before committing to any agreement. Your journey to car ownership, even with a 523 credit score, is a testament to perseverance and smart financial planning.

Most importantly, view this opportunity as a chance to rebuild your financial standing. Consistent, on-time payments will not only secure your transportation but also pave the way for a healthier credit score and a brighter financial future. Don’t be discouraged by past setbacks; instead, empower yourself with knowledge and take proactive steps. Start your journey today, armed with the insights from this guide, and drive towards better credit and reliable transportation.