Navigating a 581 Credit Score Car Loan: Your Ultimate Guide to Approval

Navigating a 581 Credit Score Car Loan: Your Ultimate Guide to Approval Carloan.Guidemechanic.com

Getting a car is often a necessity, not just a luxury, for many people. It opens doors to new job opportunities, ensures reliable transportation for family needs, and provides a sense of independence. However, the path to vehicle ownership can seem daunting, especially when your credit score isn’t in the "excellent" range. If you’re looking for a 581 credit score car loan, you’re likely navigating the challenging waters of subprime lending.

A 581 credit score falls into what lenders typically categorize as "Fair" or "Poor." This often translates to higher hurdles when seeking financing. But don’t despair! While it requires a strategic approach and a clear understanding of the lending landscape, securing a car loan with a 581 credit score is absolutely possible. This comprehensive guide will equip you with the knowledge, strategies, and expert tips to drive away with the car you need, even with less-than-perfect credit.

Navigating a 581 Credit Score Car Loan: Your Ultimate Guide to Approval

Understanding Your 581 Credit Score: What It Means for Car Loans

Your credit score is a three-digit number that tells lenders how risky you are as a borrower. A 581 FICO score, for instance, falls squarely within the "Fair" category (300-579 is "Poor," 580-669 is "Fair"). While not the lowest possible score, it signals to auto lenders that you might have a history of missed payments, high credit utilization, or other financial challenges.

This score suggests a higher likelihood of default compared to borrowers with excellent credit. As a result, lenders will approach your application with more caution. They might offer less favorable terms, require more documentation, or even ask for additional security.

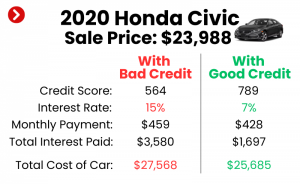

The impact of a 581 credit score on an auto loan is primarily seen in the interest rates you’ll be offered. Lenders use a tiered system, and those with lower scores are placed in a higher-risk tier, leading to significantly higher Annual Percentage Rates (APRs). This means you’ll pay substantially more over the life of the loan than someone with a prime credit score.

Understanding this reality is the first step toward effective planning. It allows you to set realistic expectations and focus on strategies that mitigate the perceived risk in the eyes of potential lenders. Knowing where you stand financially empowers you to make informed decisions.

Is Getting a Car Loan with a 581 Credit Score Possible? The Good News & The Reality

The short answer is yes, getting a car loan with a 581 credit score is indeed possible. Many lenders specialize in what are known as "subprime auto loans," which are designed specifically for individuals with credit scores below the prime threshold. These lenders understand that life happens and that a past financial misstep shouldn’t permanently sideline your ability to secure reliable transportation.

However, the reality is that the terms of such a loan will likely differ significantly from what someone with excellent credit would receive. You should anticipate higher interest rates, which directly translate to higher monthly payments and a greater total cost of the vehicle over the loan term. It’s crucial to be prepared for this financial reality.

Moreover, lenders might impose stricter conditions. This could include requirements for a larger down payment, a shorter loan term to reduce risk, or even the need for a co-signer. While these conditions might seem challenging, they are often the keys to unlocking approval when your credit score is 581.

Don’t let the prospect of higher rates or stricter terms discourage you. Instead, view them as factors to be managed through careful planning and strategic negotiation. Your goal isn’t just to get approved, but to get approved on the best possible terms available for your credit situation.

Strategies for Securing a Car Loan with a 581 Credit Score

Securing a 581 credit score car loan requires more than just filling out an application. It demands a proactive, informed, and strategic approach. By taking specific steps before and during the application process, you can significantly improve your chances of approval and potentially secure better terms.

A. Boosting Your Chances Before You Apply

Preparation is paramount when you have a 581 credit score. A little effort upfront can make a significant difference in the offers you receive.

1. Check Your Credit Report Thoroughly

Before you even think about applying for a car loan, pull your full credit reports from all three major bureaus: Experian, Equifax, and TransUnion. This is a critical first step. You’re looking for inaccuracies or errors that could be dragging your score down unnecessarily.

Based on my experience, it’s surprising how often consumers find mistakes on their reports, ranging from incorrect late payments to accounts that don’t belong to them. Disputing and removing these errors can provide an instant, albeit sometimes small, boost to your credit score. This simple act can sometimes push you into a slightly better credit tier.

2. Improve Your Credit Score (Even Slightly)

While a significant credit score jump might take time, there are short-term actions you can take to make a positive impact. Focus on reducing small outstanding debts, especially those with high interest rates or nearing their credit limit. Paying down credit card balances, even by a small amount, can improve your credit utilization ratio, which is a major factor in your score.

Pro tips from us: Even a 10-20 point increase can sometimes move you from one lending tier to another, potentially saving you hundreds or even thousands of dollars in interest over the life of a car loan. Showing recent responsible financial behavior, even if small, can also be a positive signal to lenders.

3. Save for a Larger Down Payment

This is perhaps one of the most impactful strategies when dealing with a 581 credit score car loan. A substantial down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. Lenders are more comfortable financing a smaller portion of the vehicle’s value.

Based on my experience, a larger down payment is often the single most impactful factor in improving your chances of approval and securing a better interest rate when your credit is subprime. It demonstrates your financial commitment and lowers your loan-to-value (LTV) ratio, making the loan more attractive to lenders. Aim for at least 10-20% of the car’s purchase price if possible.

B. Navigating the Application Process

Once you’ve prepared your finances, it’s time to strategically approach lenders. This phase requires careful consideration of where and how you apply.

1. Get Pre-Approved First

Don’t walk into a dealership without knowing what you can afford. Seek pre-approval from multiple lenders – banks, credit unions, and online auto loan providers. Pre-approval gives you a clear understanding of the loan amount, interest rate, and terms you qualify for before you start shopping.

This process allows you to separate the financing from the car buying experience, reducing pressure at the dealership. Pro tips from us: Having a pre-approval in hand gives you leverage during negotiations, as you’re effectively walking in with your own financing, allowing you to focus purely on the vehicle price.

2. Consider a Co-signer

If you’re struggling to get favorable terms on your own, a co-signer with good credit can significantly improve your chances. A co-signer essentially guarantees the loan, promising to make payments if you default. This greatly reduces the risk for the lender.

Common mistakes to avoid are not fully discussing the responsibilities with your co-signer. Both parties are legally responsible for the debt, and a missed payment affects both credit scores. Choose someone you trust implicitly and who understands the commitment.

3. Explore Different Lender Types

Not all lenders are created equal, especially for subprime borrowers.

- Banks: Traditional banks might be hesitant with a 581 score, but if you have an existing relationship, they might be more flexible.

- Credit Unions: Often more community-focused, credit unions can be more willing to work with members with lower scores and may offer slightly better rates.

- Online Lenders: Many online platforms specialize in bad credit auto loans and can offer quick pre-approvals and competitive rates.

- Buy-Here-Pay-Here Dealerships: These dealerships finance loans in-house, making approval almost guaranteed. However, they often come with very high interest rates and limited vehicle choices. While an option, it should generally be a last resort.

4. Choose the Right Vehicle

When your credit score is 581, practicality should outweigh luxury. Opt for a reliable, affordable used car rather than a brand-new model with all the bells and whistles. A less expensive car means you’ll need to borrow less, which in turn means lower monthly payments and less overall interest paid.

Focus on a vehicle that meets your needs without stretching your budget too thin. Remember, this car loan can be a stepping stone to rebuilding your credit, allowing you to qualify for better terms on your next vehicle purchase.

C. Understanding Loan Terms and Conditions

Getting approved is one thing; understanding the terms is another. For a 581 credit score car loan, scrutinizing the details is non-negotiable.

1. Interest Rates

With a 581 credit score, expect interest rates to be significantly higher than prime rates, often ranging from 10% to 20% or even higher. It’s crucial to compare offers from multiple lenders to find the most competitive rate available to you. Even a small difference in the APR can save you hundreds or thousands of dollars over the loan’s life.

Don’t just accept the first offer you receive. Use your pre-approvals as negotiation tools.

2. Loan Term (Length)

Lenders might offer longer loan terms (e.g., 72 or 84 months) to make monthly payments seem more affordable. While this reduces the immediate financial burden, it dramatically increases the total amount of interest you’ll pay over the life of the loan. You also risk owing more on the car than it’s worth (being "upside down") as depreciation outpaces your payments.

Based on my experience, aim for the shortest loan term you can comfortably afford. A 48 or 60-month term is often preferable to minimize total interest paid.

3. Hidden Fees & Add-ons

Be vigilant for additional fees and unnecessary add-ons that can inflate the total cost of your loan. This includes extended warranties, GAP insurance (while sometimes useful, ensure it’s not overpriced), and various administrative fees. While some fees are legitimate, others are negotiable or entirely optional.

Always read the fine print of your loan agreement. Ask for a breakdown of every charge and question anything you don’t understand or agree with.

4. The Importance of the APR

When comparing loan offers, always focus on the Annual Percentage Rate (APR), not just the stated interest rate. The APR includes the interest rate plus any additional fees, giving you a truer picture of the total cost of borrowing. This is the most accurate way to compare different loan proposals side-by-side.

A lower interest rate might look appealing, but if it comes with high origination fees, the overall APR could be higher than an offer with a slightly higher interest rate but no additional fees.

What to Expect When Applying for a 581 Credit Score Car Loan

When you have a 581 credit score, the application process might feel a bit different. Lenders will perform a more thorough review of your financial history. They might request additional documentation, such as proof of income, residence, and employment stability, beyond what a prime borrower would need.

Expect fewer options when it comes to vehicle choice. Lenders are more likely to approve loans for vehicles that hold their value well or are less expensive, as this reduces their risk in case of repossession. Your desired make and model might need to be adjusted to fit what lenders are willing to finance.

Your monthly payments will likely be higher, or the loan term will be longer, compared to someone with excellent credit. This is the direct consequence of a higher interest rate and the need to mitigate lender risk. Be prepared for this and ensure your budget can comfortably accommodate these payments.

Finally, be prepared to negotiate, even with bad credit. While your leverage might be limited, there’s always room to discuss vehicle price, trade-in value, and potentially some fees. Don’t be afraid to walk away if an offer feels exploitative or doesn’t align with your budget.

Common Mistakes to Avoid When Seeking a 581 Credit Score Car Loan

Navigating the world of subprime auto loans can be tricky. Avoiding these common pitfalls can save you money, stress, and protect your credit score.

- Applying Everywhere: Each time you apply for credit, a "hard inquiry" is placed on your credit report. Too many hard inquiries in a short period can further depress your score. It’s better to get pre-approved or apply with 2-3 lenders within a 14-45 day window (depending on the scoring model), as these are typically grouped as a single inquiry for auto loans.

- Not Checking Your Credit Report: As discussed, errors are common. Skipping this step means potentially missing an opportunity to improve your score and terms.

- Ignoring the Down Payment: A small or no down payment makes you a much riskier borrower in the eyes of a lender. This often results in higher interest rates or outright denial.

- Focusing Only on Monthly Payments: While important, fixating solely on the monthly payment can lead to longer loan terms and significantly higher total interest paid. Always consider the total cost of the loan.

- Settling for the First Offer: Competition exists even in subprime lending. Always compare offers from multiple lenders to ensure you’re getting the best possible terms for your situation.

- Buying More Car Than You Can Afford: It’s tempting to get the flashiest car, but overextending yourself financially can lead to missed payments, repossession, and further damage to your credit. Be realistic about your budget, including insurance, fuel, and maintenance costs.

Rebuilding Your Credit Through a Car Loan

One of the significant benefits of successfully securing and managing a 581 credit score car loan is the opportunity it presents to rebuild your credit history. An auto loan is an installment loan, and making consistent, on-time payments demonstrates responsible financial behavior.

Every on-time payment reported to the credit bureaus contributes positively to your payment history, which is the most influential factor in your credit score. Over time, as you consistently meet your obligations, your credit score will gradually improve. This improved score will then open doors to better financial products, lower interest rates on future loans, and greater financial flexibility.

Consider this car loan as an investment in your financial future. It’s not just about getting from point A to point B; it’s about establishing a positive credit trajectory that can benefit you for years to come.

Pro Tips from Our Experts

As experienced professionals in the lending and credit space, we’ve seen countless individuals navigate the challenges of subprime auto loans. Here are some invaluable insights to help you succeed:

- Negotiate Everything: From the vehicle’s price to the interest rate and any added fees, always be prepared to negotiate. Every dollar saved can make a difference in your total cost.

- Don’t Rush the Process: Car buying can be an emotional experience, but with a 581 credit score, patience is your greatest asset. Take your time to research, compare, and make informed decisions.

- Read All Documents Carefully: Before signing anything, thoroughly read every line of the loan agreement. If you don’t understand a clause, ask for clarification. Don’t be pressured into signing before you’re completely comfortable.

- Understand Your Full Budget: Beyond the car payment, factor in insurance costs (which can be higher for newer cars or those financed with bad credit), fuel, maintenance, and potential repair costs. A car loan is just one piece of the ownership puzzle.

- Consider Refinancing Later: Once you’ve made 6-12 months of on-time payments, and your credit score has improved, you might be able to refinance your car loan at a lower interest rate. This can significantly reduce your monthly payments and total interest paid over the remaining term.

- Boost Your Credit Score Quickly: For more detailed strategies on improving your financial standing before or after your car loan, check out our guide on .

- Deciphering Loan Terms: To gain a deeper understanding of how interest rates and other factors impact your loan, read our comprehensive article on .

- Reliable Credit Information: For a foundational understanding of credit scores and reports, refer to trusted sources like MyFICO: .

Conclusion

Securing a 581 credit score car loan might present a few more obstacles than a prime loan, but it is by no means an impossible feat. With the right preparation, a strategic approach to lenders, and a clear understanding of loan terms, you can successfully navigate the process. Remember, a higher down payment, a co-signer, and shopping around for the best interest rates are powerful tools in your arsenal.

This car loan isn’t just about getting a vehicle; it’s a significant opportunity to demonstrate financial responsibility and actively work towards improving your credit score. By making consistent, on-time payments, you’ll be paving the way for a stronger financial future. Arm yourself with knowledge, act with diligence, and you’ll soon be driving away with confidence, knowing you’ve made a smart and informed decision.