Navigating a Car Loan with a 460 Credit Score: Your Comprehensive Guide to Approval

Navigating a Car Loan with a 460 Credit Score: Your Comprehensive Guide to Approval Carloan.Guidemechanic.com

Securing a car loan can feel like an insurmountable challenge when your credit score hovers around 460. Many people believe it’s impossible, leading to frustration and the feeling of being stuck without reliable transportation. However, while a 460 credit score presents significant hurdles, it doesn’t mean the road to car ownership is completely closed.

This comprehensive guide is designed to empower you with the knowledge and strategies needed to navigate the complexities of getting a car loan with very poor credit. We’ll explore realistic expectations, uncover practical steps, and provide expert insights to increase your chances of approval. Our ultimate goal is to help you drive away in a reliable vehicle while simultaneously building a stronger financial future.

Navigating a Car Loan with a 460 Credit Score: Your Comprehensive Guide to Approval

Understanding Your 460 Credit Score

Before diving into loan strategies, it’s crucial to understand what a 460 credit score signifies in the lending world. Credit scores, like FICO and VantageScore, typically range from 300 to 850. A score of 460 falls squarely into the "Very Poor" category.

This classification indicates to lenders that you pose a high credit risk. Historically, individuals with scores in this range have a higher likelihood of defaulting on loans. This perception impacts everything from loan approval to the interest rates you’ll be offered.

Common reasons for such a low score include missed payments, collection accounts, bankruptcies, foreclosures, or a limited credit history. Lenders view these factors as red flags, making them hesitant to extend credit. It’s not a personal judgment, but rather a statistical assessment of risk.

Is a Car Loan with a 460 Credit Score Truly Possible?

The short answer is yes, getting a car loan with a 460 credit score is possible, but it comes with specific conditions and expectations. This isn’t a straightforward process, and it requires a strategic approach. Based on my experience working with numerous clients in similar situations, securing a conventional loan from a prime lender is highly unlikely.

Instead, you’ll be looking at what’s known as the "subprime" lending market. These lenders specialize in working with borrowers who have lower credit scores. They are willing to take on more risk, but in exchange, they typically charge significantly higher interest rates and may require additional safeguards.

It’s important to set realistic expectations from the outset. You likely won’t qualify for the best deals, the lowest interest rates, or the newest luxury vehicles. The goal here is to secure a reliable, affordable car that meets your immediate transportation needs and, more importantly, provides an opportunity to rebuild your credit.

Strategies to Increase Your Chances of Approval

Successfully obtaining a car loan with a 460 credit score requires more than just filling out an application. It demands preparation, strategic decision-making, and a clear understanding of what lenders look for. Here are the key strategies to boost your approval odds.

1. Save a Significant Down Payment

One of the most powerful tools you have when seeking a car loan with bad credit is a substantial down payment. This isn’t just a suggestion; it’s often a critical requirement for subprime lenders. A significant down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk.

Think of it this way: the more money you put down upfront, the less money the lender stands to lose if you default. This immediately makes your application more attractive. It also demonstrates your commitment to the purchase and your ability to save, which are positive indicators for lenders.

Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price, or even more if possible. A larger down payment not only increases your approval chances but also reduces your monthly payments and the total interest paid over the life of the loan. It creates immediate equity in the vehicle, which can be beneficial if you need to sell it later.

2. Find a Reliable Cosigner

A cosigner with good credit can dramatically improve your chances of loan approval. A cosigner is someone who legally agrees to take full responsibility for the loan if you fail to make payments. Their strong credit history and income essentially act as a guarantee for the lender.

For lenders, a cosigner mitigates the risk associated with your low credit score. They see that there’s another financially responsible party to fall back on if you encounter difficulties. This can lead to better loan terms, including a lower interest rate than you’d receive on your own.

Choosing a cosigner is a significant decision. It should be someone with excellent credit, stable income, and a strong trust relationship with you, such as a family member or a very close friend. Common mistakes to avoid include asking someone who isn’t fully aware of the responsibility or someone whose own credit might be negatively impacted. Remember, if you miss payments, it will affect both your credit and theirs.

3. Choose the Right Vehicle (Affordable & Practical)

When you have a 460 credit score, your focus should be on practicality and affordability, not luxury. Lenders for subprime loans prefer to finance vehicles that hold their value reasonably well and are not excessively expensive. This reduces their risk in case of repossession.

Avoid brand-new cars, as they depreciate rapidly and typically come with higher price tags, increasing the loan amount. Instead, focus on reliable, used vehicles that fit comfortably within your budget. A car that costs $10,000-$15,000 is often a more realistic target than one costing $30,000+.

Beyond the sticker price, consider the total cost of ownership. Factor in insurance premiums (which can be higher for bad credit borrowers), maintenance, and fuel costs. Overbuying is a common mistake that can lead to financial strain and, ultimately, loan default.

4. Explore Specific Lenders for Bad Credit

Not all lenders are created equal, especially when dealing with very poor credit. You’ll need to target lenders who specialize in subprime auto loans. These include certain dealerships, credit unions, and online lenders.

Many dealerships have "Special Finance" departments specifically designed to work with buyers who have challenged credit. They often have relationships with a network of subprime lenders. Starting your search here can be effective, as they are accustomed to these situations.

Credit unions can also be a good option. They are member-owned and sometimes offer more flexible lending criteria and slightly better rates than traditional banks, even for bad credit borrowers. Online subprime lenders are another avenue, offering convenience and potentially quicker pre-approvals. You can often get pre-qualified with a soft credit inquiry, which won’t hurt your score. For more details on finding the right lenders, you might find our article on "Finding the Best Bad Credit Car Loan Lenders" helpful.

5. Gather All Necessary Documentation

Being prepared with all required documents can significantly streamline the application process and show lenders you are serious and organized. Lenders, especially those working with bad credit, will want a comprehensive picture of your financial situation beyond just your credit score.

You’ll typically need proof of income, such as recent pay stubs (at least two or three months’ worth), bank statements, or tax returns if you’re self-employed. Proof of residence, like a utility bill or lease agreement, is also standard. Valid identification (driver’s license, state ID) is a must.

Additionally, some lenders may ask for a list of personal references. Having everything ready when you apply demonstrates reliability and can speed up the approval process, preventing delays that might lead to frustration.

6. Be Prepared for Higher Interest Rates

One of the undeniable realities of getting a car loan with a 460 credit score is facing significantly higher interest rates. Lenders charge more interest to compensate for the increased risk they are taking on. While it might seem unfair, it’s a standard practice in subprime lending.

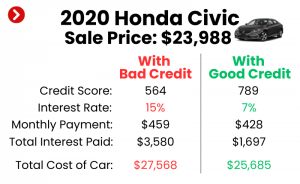

For comparison, a borrower with excellent credit might get an interest rate of 3-5%, while someone with a 460 score could face rates of 15-25% or even higher. It’s crucial to factor this into your budget and understand its impact on your total loan cost and monthly payments. Don’t be surprised or deterred by these rates; they are part of the process.

The key is to focus on making consistent, on-time payments. This allows you to potentially refinance the loan at a lower rate in 12-18 months once your credit score improves. This initial high-interest loan can be a stepping stone, not a permanent burden.

7. Improve Your Credit Score BEFORE Applying (If Time Allows)

While this article focuses on getting a loan with a 460 score, if you have any flexibility with your timeline, even a modest improvement in your credit score can make a big difference. Every point counts, and moving up even 20-30 points can open doors to slightly better terms.

Start by obtaining your free credit report from AnnualCreditReport.com and review it thoroughly for errors. Dispute any inaccuracies immediately. Focus on paying down high-interest debt, especially on credit cards, as this can quickly improve your credit utilization ratio. Make sure all your current bills are paid on time.

Even small, consistent positive actions can begin to chip away at a low score. If you can wait a few months and implement these strategies, you might find yourself in a slightly stronger negotiating position. For a detailed roadmap, refer to our "Ultimate Guide to Improving Your Credit Score."

The Application Process with a Low Credit Score

The application process for a car loan with a 460 credit score will often involve a bit more scrutiny than for someone with prime credit. Lenders will look beyond just the number. They want to see stability.

Pre-qualification is a great first step. Many subprime lenders and dealerships offer pre-qualification with a soft credit pull, which doesn’t affect your credit score. This gives you an idea of what you might qualify for before committing to a hard inquiry.

Once you proceed with a full application, lenders will meticulously examine your income stability and debt-to-income (DTI) ratio. They want to ensure you have a steady income stream that can comfortably cover your proposed car payments in addition to your existing financial obligations. A low DTI ratio is always favorable.

Based on my experience, transparency is key. Be honest about your financial situation. Trying to hide information or misrepresent your income will only lead to rejection. Lenders appreciate honesty and a clear picture of your ability to repay. Once approved, be prepared to negotiate terms, focusing on the total cost of the loan and ensuring the monthly payment is genuinely affordable.

Pro Tips for Success and Rebuilding Your Credit

Getting the loan is just the first step. The ultimate goal is to use this opportunity to rebuild your credit and improve your financial standing.

- Don’t Apply Everywhere: Resist the urge to apply for loans at every dealership or lender. Multiple hard inquiries in a short period can further damage your credit score. Use pre-qualification tools first.

- Read the Fine Print: Subprime loans can sometimes come with additional fees or less favorable terms. Understand every clause, including early payoff penalties or specific requirements. Ask questions until you’re completely clear.

- Make Payments ON TIME, EVERY TIME: This cannot be stressed enough. Consistent, on-time payments are the single most effective way to improve your credit score. Set up automatic payments or reminders to ensure you never miss a due date. This loan is your chance to prove you are a responsible borrower.

- Consider Refinancing Later: After 12-18 months of consistent payments, your credit score should improve significantly. At that point, you may qualify to refinance your car loan at a much lower interest rate, saving you a substantial amount of money over the remaining loan term.

- A Car Loan as a Credit-Building Tool: View this loan not just as a means to get a car, but as a powerful credit-building instrument. Successfully managing this loan will demonstrate responsible financial behavior to future lenders, opening doors to better rates and opportunities down the line. To monitor your progress, regularly check your credit reports from trusted sources like Experian, Equifax, or TransUnion via AnnualCreditReport.com.

Common Mistakes to Avoid When Seeking a 460 Credit Score Car Loan

Navigating the subprime auto loan market can be tricky, and several common pitfalls can derail your efforts or leave you in a worse financial situation.

- Applying Blindly to Multiple Lenders: As mentioned, this leads to numerous hard inquiries that negatively impact your credit. Do your research and target appropriate lenders.

- Not Having a Down Payment: While not always mandatory, a lack of a down payment makes approval significantly harder and will result in higher monthly payments and interest.

- Overlooking Hidden Fees and Add-ons: Be vigilant for extended warranties, GAP insurance, or other add-ons that inflate the loan amount. While some might be beneficial, ensure you understand and agree to all additional costs.

- Buying More Car Than You Can Afford: It’s tempting to get a nicer car, but an overly expensive vehicle can lead to financial strain, missed payments, and ultimately, repossession. Stick to your budget.

- Ignoring the Importance of a Cosigner (If Applicable): If you have access to a willing and qualified cosigner, not utilizing that resource is a missed opportunity for better terms.

Conclusion

Securing a car loan with a 460 credit score is undoubtedly a challenging endeavor, but it is far from impossible. By understanding the landscape of subprime lending, preparing diligently, and adopting a strategic approach, you can significantly increase your chances of approval. Remember, this journey is not just about getting a car; it’s about taking a crucial step towards financial recovery and establishing a positive credit history.

Focus on saving a substantial down payment, exploring reliable cosigner options, choosing an affordable vehicle, and targeting lenders who specialize in bad credit. Most importantly, once you secure the loan, commit to making every payment on time. This proactive approach will not only get you the transportation you need but will also lay a solid foundation for rebuilding your credit score and opening up better financial opportunities in the future. Start planning today, and drive towards a brighter financial tomorrow.