Navigating Air Force Car Loans: Your Ultimate Guide to Smart Military Auto Financing

Navigating Air Force Car Loans: Your Ultimate Guide to Smart Military Auto Financing Carloan.Guidemechanic.com

For many Air Force service members, the dream of owning a reliable vehicle is a significant milestone. Whether you’re looking for a brand-new car to cruise around your base town or a dependable used vehicle to handle PCS moves, securing the right auto loan is crucial. However, the path to car ownership for Air Force personnel comes with its own unique set of considerations, opportunities, and potential pitfalls.

This comprehensive guide is designed to equip you with all the knowledge you need to navigate the world of Air Force car loans. We’ll delve deep into everything from understanding your financial landscape as a service member to securing the best rates and avoiding common mistakes. Our ultimate goal is to empower you to make informed decisions and drive away with confidence, knowing you’ve secured a car loan that truly serves your military life.

Navigating Air Force Car Loans: Your Ultimate Guide to Smart Military Auto Financing

The Unique Financial World of Air Force Personnel

Air Force service members operate within a distinct financial environment that sets them apart from the civilian population. While the stability of military pay is a significant advantage, factors like frequent Permanent Change of Station (PCS) moves, deployments, and the unique structure of military benefits can influence how lenders view your creditworthiness and overall financial profile.

Understanding these nuances is the first step toward securing favorable Air Force car loan terms. Your income, though steady, can be supplemented by various allowances that lenders might need help fully appreciating. Moreover, younger service members might have a limited credit history, which can sometimes present challenges when seeking financing.

Based on my experience advising military families, lenders who specialize in military loans often have a better grasp of these complexities. They understand the value of your service and the reliability of your income, often translating into more competitive rates and flexible terms tailored to your unique circumstances. This specialized understanding can make a significant difference in your car buying journey.

Exploring Your Air Force Car Loan Options

When it comes to financing a vehicle, Air Force personnel have several avenues to explore. Each option comes with its own set of advantages and disadvantages. Knowing where to look and what to expect can significantly impact your overall loan experience and the amount you’ll pay over time.

Choosing the right lender is arguably the most critical decision in this process. Don’t simply opt for the first offer you receive; thorough research and comparison shopping are essential for securing the best possible terms for your Air Force car loan.

1. Military Credit Unions: Your Best Ally

For Air Force service members, military-focused credit unions often represent the absolute best option for car financing. Institutions like USAA, Navy Federal Credit Union, and local credit unions near Air Force bases are specifically designed to serve the military community. They deeply understand the unique aspects of military life, including pay structures, deployments, and PCS cycles.

Pro tips from us recommend prioritizing these lenders because they typically offer lower interest rates, more flexible repayment terms, and a more streamlined application process for service members. They are member-owned, meaning their profits are returned to their members in the form of better rates and fewer fees. Their commitment to the military community makes them invaluable partners in your financial journey.

Many of these credit unions also provide financial education and counseling services, further assisting you in making informed decisions about your auto loan. Their staff are often veterans or military spouses themselves, creating a more empathetic and understanding lending environment. This personal connection can be incredibly reassuring when dealing with a significant financial commitment.

2. Traditional Dealership Financing

Dealership financing is a convenient option, as you can arrange your loan directly at the point of sale. Many dealerships have relationships with multiple banks and can offer various financing packages. However, this convenience sometimes comes at a cost, as dealership rates may not always be the most competitive available to Air Force members.

It’s crucial to approach dealership financing with a clear understanding of the market. Having a pre-approved loan offer from a military credit union in hand gives you significant leverage. This allows you to compare their offer directly with the dealership’s and negotiate for the best possible rate. Without external offers, you might miss out on better terms.

While some dealerships might have special programs for military members, always scrutinize the terms and conditions. Ensure that any "military discount" on financing truly translates into a better deal than what you could get elsewhere. Remember, the dealership’s primary goal is to sell you a car and make a profit, so your vigilance is key.

3. Online Lenders

The digital age has brought forth a plethora of online lenders that offer car loans with varying rates and terms. These platforms can be incredibly convenient, allowing you to compare offers from multiple lenders from the comfort of your home, often with quick approval processes. They can be a good option for comparison shopping, especially if you’re not near a military credit union.

However, the ease of access comes with a need for increased due diligence. Not all online lenders are created equal, and some may not fully understand the unique circumstances of Air Force personnel. Always check their reputation, read customer reviews, and ensure they are legitimate and transparent with their terms.

When considering an online lender, carefully review the interest rates, fees, and repayment schedules. Make sure there are no hidden charges and that the terms are clearly laid out. While they offer convenience, ensure the rates are competitive with what military credit unions provide.

4. Personal Loans (A Cautious Alternative)

In certain, very specific scenarios, some Air Force members might consider a personal loan as an alternative to a traditional auto loan. Personal loans are typically unsecured, meaning they don’t require collateral like the car itself. This can offer more flexibility, but it usually comes with significantly higher interest rates compared to a secured car loan.

As an expert in military financial planning, I strongly advise caution when considering this route for car purchases. The higher interest rates can make your car significantly more expensive over the long run. Personal loans are generally better suited for other financial needs, such as debt consolidation or unexpected emergencies, rather than financing a depreciating asset like a car.

If you find yourself in a situation where a personal loan seems like the only option, it’s a strong indicator that you might be buying more car than you can truly afford. In such cases, it’s wiser to reassess your budget, consider a less expensive vehicle, or take steps to improve your credit before committing to a high-interest personal loan for a car.

Mastering the Application Process for Air Force Members

Applying for an Air Force car loan can feel daunting, but being prepared makes the process much smoother. Understanding what lenders look for and having your documents in order can significantly improve your chances of approval and help you secure the best possible rates. Your military status often works in your favor, but you still need to present a strong financial case.

The key is to demonstrate stability, reliability, and a clear ability to repay the loan. Lenders want assurance that you are a responsible borrower. Therefore, presenting a comprehensive and organized application package is crucial for a successful outcome.

1. Essential Documents for Your Application

When applying for an Air Force car loan, lenders will typically require several key documents to verify your identity, income, and residency. Having these prepared in advance will expedite your application. These documents help the lender assess your financial stability and eligibility.

You will almost certainly need your military ID, a valid driver’s license, and proof of residence (utility bill or lease agreement). Crucially, you’ll also need your most recent Leave and Earnings Statement (LES) as proof of income. The LES clearly outlines your base pay, allowances, and deductions, providing a comprehensive picture of your financial standing. Lenders who specialize in military loans are very familiar with interpreting an LES.

Other documents might include your Social Security card and possibly proof of insurance once the loan is approved. Gathering these documents beforehand not only saves time but also presents you as an organized and serious applicant.

2. Understanding Your Credit Score

Your credit score is a numerical representation of your creditworthiness, and it plays a significant role in determining your interest rate for an Air Force car loan. Lenders use it to assess the risk of lending to you. A higher credit score generally translates to lower interest rates, saving you hundreds or even thousands of dollars over the life of the loan.

Common mistakes to avoid often include overlooking the importance of a strong credit profile. Before applying, obtain a copy of your credit report from all three major bureaus (Equifax, Experian, TransUnion) and review it for accuracy. Dispute any errors immediately, as these can negatively impact your score. Websites like AnnualCreditReport.com allow you to access your reports for free annually.

If your credit score is lower than you’d like, take steps to improve it before applying for a loan. This could involve paying down existing debts, making all payments on time, and avoiding new credit applications. Even a few points increase can make a difference in your interest rate. For young service members with limited credit history, securing a secured credit card or a small installment loan can help build a positive credit history over time.

3. The Power of a Down Payment

Making a down payment on your Air Force car loan offers several significant advantages. Firstly, it reduces the total amount you need to borrow, which in turn lowers your monthly payments. Secondly, a substantial down payment often leads to more favorable interest rates because it reduces the lender’s risk.

Based on my experience, even a modest down payment can signal to lenders that you are financially responsible and committed to the purchase. It demonstrates your ability to save and invest in your vehicle. For service members with a less-than-perfect credit history, a larger down payment can sometimes help offset the risk and make loan approval easier.

Aim for at least 10-20% of the car’s purchase price as a down payment if possible. This not only makes your monthly payments more manageable but also helps prevent you from being "upside down" on your loan (owing more than the car is worth) early in the ownership period, which is a common concern with rapidly depreciating assets like new cars.

4. Navigating Interest Rates and Loan Terms

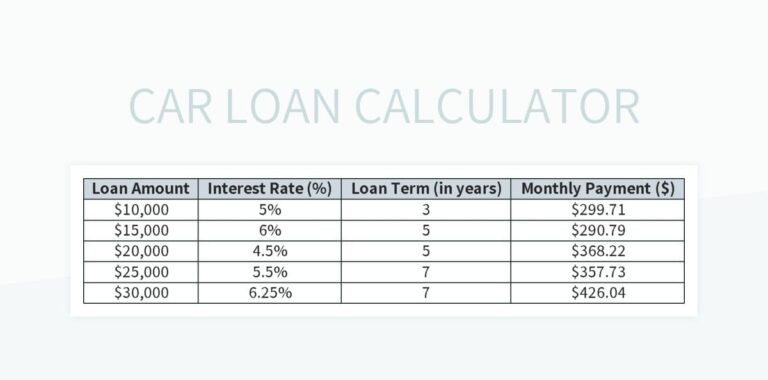

Interest rates, expressed as an Annual Percentage Rate (APR), are the cost of borrowing money. They are influenced by your credit score, the loan term, the down payment amount, and the current economic environment. Understanding how these factors interact is crucial for securing the best Air Force car loan.

Loan terms refer to the length of time you have to repay the loan, typically ranging from 36 to 72 months or even longer. While a longer loan term might offer lower monthly payments, it usually means you’ll pay more in total interest over the life of the loan. Conversely, shorter terms have higher monthly payments but save you money on interest.

Our recommendation is to strike a balance between an affordable monthly payment and the total cost of the loan. Avoid stretching out a loan simply to achieve the lowest possible monthly payment if it means paying significantly more in interest. Always consider the total amount you will pay back, not just the monthly installment.

Special Protections and Considerations for Air Force Personnel

Air Force service members are afforded certain protections and face unique circumstances that civilian borrowers do not. Being aware of these can save you money, provide peace of mind during deployments, and protect you from predatory practices. These considerations are vital for a secure and stable car ownership experience.

It’s not just about getting the loan; it’s about managing it effectively throughout your military career. Understanding your rights and responsibilities is paramount.

1. The Servicemembers Civil Relief Act (SCRA)

The Servicemembers Civil Relief Act (SCRA) is a federal law designed to provide financial and legal protections for military members as they enter active duty. While its most direct application is to debts incurred before entering active duty, understanding the SCRA is still vital for Air Force personnel navigating car loans. For pre-service debts, the SCRA can cap interest rates at 6% during periods of active duty.

As an expert in military financial planning, I’ve seen firsthand how crucial SCRA knowledge is for protecting service members. While the SCRA generally doesn’t apply to new loans taken out during active duty, its spirit of protection for military families against financial hardship is something reputable military lenders embody. Always be aware of your rights under SCRA for any pre-existing financial obligations you may have.

For detailed information on the SCRA, including eligibility and how to invoke its protections, you can refer to trusted external resources like the Consumer Financial Protection Bureau (CFPB) or the U.S. Department of Justice’s SCRA website. Knowledge of this act is a powerful tool for military financial readiness.

2. Managing Your Loan During Deployment

Deployment is a significant part of Air Force life, and it brings unique challenges for managing personal finances, including car payments. It’s crucial to have a plan in place before you deploy to ensure your Air Force car loan payments continue uninterrupted. This proactive approach prevents missed payments, which can negatively impact your credit score.

One of the most effective strategies is to set up automatic payments directly from your bank account. This ensures consistency and reduces the risk of oversight while you’re focused on your mission. Additionally, consider granting a trusted family member or spouse Power of Attorney (POA) to handle financial matters on your behalf, especially for unexpected issues that might arise.

Before deploying, communicate with your lender to inform them of your upcoming absence. While they may not offer special deferments for new loans, maintaining open communication is always beneficial. Ensure all necessary insurance coverage is in place and that someone trustworthy can check on your vehicle if it remains stateside.

3. Permanent Change of Station (PCS) and Your Vehicle

PCS moves are a regular occurrence for Air Force personnel, and they can complicate vehicle ownership and loan management. Transporting your car, updating registration, and adjusting insurance policies across state lines or even internationally requires careful planning. These logistical challenges can add stress if not properly addressed.

Before your PCS, research the vehicle registration and insurance requirements of your new duty station. Different states have different regulations, and some international assignments might have very specific rules regarding vehicle importation. Ensure your car loan lender is aware of your new address for billing and communication purposes.

If you are shipping your vehicle, understand the costs and logistics involved. Sometimes, selling your current car and purchasing a new one at your new location might be more cost-effective than shipping, especially for international moves. Always factor in the total cost of ownership, including transportation, when planning a PCS with your financed vehicle.

4. Guarding Against Predatory Lenders

Unfortunately, some unscrupulous lenders target military members, taking advantage of their unique circumstances or perceived financial naivety. These predatory lenders often offer "guaranteed approval" or "no credit check" loans with excessively high interest rates, hidden fees, and unfavorable terms. They typically operate near military bases, preying on unsuspecting service members.

Red flags to watch out for include high-pressure sales tactics, demands for upfront fees, refusal to provide terms in writing, or pushing you into a loan that feels too good to be true. Always be wary of lenders who promise a loan without reviewing your credit history or income. These are often signs of exploitative practices.

Our recommendation is to stick with reputable military credit unions or well-established national banks. If you encounter a lender you suspect is predatory, report them to your base’s legal assistance office or the Consumer Financial Protection Bureau (CFPB). Education and vigilance are your best defenses against falling victim to these schemes.

Pro Tips for Securing the Best Air Force Car Loan

Getting an Air Force car loan isn’t just about getting approved; it’s about securing the most advantageous terms possible. With a strategic approach, you can significantly reduce the overall cost of your vehicle and ensure your loan fits comfortably within your budget. These pro tips are designed to empower you throughout the entire car buying and financing process.

The key is to be proactive, informed, and confident in your negotiations. Don’t let the excitement of a new vehicle overshadow the importance of smart financial planning.

1. Get Pre-Approved Before You Shop

This is perhaps the most powerful tip for any car buyer, especially for Air Force members. Getting pre-approved for an Air Force car loan from a military credit union or another trusted lender before you even step foot in a dealership transforms your position. You walk in as a cash buyer, not just a customer seeking financing.

Pre-approval provides you with a clear budget and a firm understanding of the interest rate you qualify for. This knowledge empowers you to negotiate the car’s price separately from the financing. Dealers cannot mislead you about rates or use financing as a leverage point if you already have your own funding secured.

Our recommendation, based on years of observing successful outcomes for military members, is to always secure pre-approval. It streamlines the buying process, eliminates stress, and ensures you’re getting the best deal on both the vehicle and the loan.

2. Shop Around, Don’t Settle

Never accept the first loan offer you receive. Even if it seems reasonable, there might be a better deal waiting for you elsewhere. Comparing offers from at least three different lenders – ideally including military credit unions, national banks, and potentially online lenders – is a non-negotiable step in securing the best Air Force car loan.

Look beyond just the interest rate. Consider all fees, repayment terms, and any penalties for early repayment. A slightly higher interest rate with no fees might be better than a lower rate with substantial hidden charges. A comprehensive comparison will reveal the true cost of each loan.

This diligent approach ensures that you are getting the most competitive rates and terms available for your unique financial situation. It also forces lenders to compete for your business, which ultimately benefits you, the borrower.

3. Understand the Total Cost, Not Just Monthly Payments

It’s easy to get fixated on the monthly payment, but focusing solely on this figure can be a costly mistake. The true measure of a loan’s expense is its total cost over the entire loan term, which includes the principal, all interest paid, and any associated fees. A lower monthly payment often means a longer loan term and more interest paid overall.

Pro tips from us emphasize looking at the Annual Percentage Rate (APR), which provides a more accurate representation of the total cost of borrowing, including interest and some fees. Always ask for the total amount you will pay over the life of the loan. This comprehensive view helps you make a financially sound decision.

Factor in other costs of car ownership as well, such as insurance, maintenance, and fuel. A car that fits your monthly loan payment might still be unaffordable if the ancillary costs are too high. Consider your entire budget before committing to a vehicle.

4. Negotiate Wisely at the Dealership

Armed with your pre-approval and a clear understanding of your budget, you’re in a strong position to negotiate the car’s price. Always negotiate the vehicle’s price first, separate from any financing discussions the dealership might try to initiate. This prevents confusion and ensures you’re getting a fair price for the car itself.

Be prepared to walk away if you don’t feel the deal is right. There are always other dealerships and other cars. Your patience and willingness to decline an unfavorable offer are powerful negotiation tools. Don’t let high-pressure sales tactics rush you into a decision you might regret.

Remember, the dealership might still try to beat your pre-approved rate. If they can offer a lower APR, great! But make sure they aren’t adding any hidden fees or extending the loan term to achieve that lower monthly payment. Always compare apples to apples.

5. Read Every Line of the Contract

Before signing any documents, read the entire Air Force car loan contract carefully and thoroughly. Do not let anyone rush you through this process. Verify that all the terms you agreed upon – the interest rate, loan term, monthly payment, and total loan amount – are accurately reflected in the final paperwork.

Pay close attention to any additional products or services that might be added to the contract, such as extended warranties, paint protection, or gap insurance. While some of these might be beneficial, they are often marked up significantly and increase your loan amount. You have the right to decline most of these add-ons.

Common mistakes to avoid include signing without fully understanding every clause. If you have any questions or find discrepancies, ask for clarification before signing. If necessary, take the contract to your base’s legal assistance office for review. Once you sign, you are legally bound by the terms, so ensure everything is exactly as you expect.

Conclusion

Securing an Air Force car loan doesn’t have to be a complicated or stressful endeavor. By understanding your unique financial standing as a service member, exploring the various lending options, mastering the application process, and leveraging the special protections available to you, you can make an informed and confident decision. Your military service provides a foundation of stability that many lenders recognize and value.

Our goal in providing this in-depth guide is to empower you with the knowledge needed to navigate this important financial journey successfully. Remember, an informed borrower is a powerful borrower. By getting pre-approved, shopping around, and understanding all the terms, you’re not just getting a car; you’re making a smart investment in your financial future.

So, take the time to plan wisely, seek out the best resources, and don’t hesitate to ask questions. With the right approach, you can drive away with confidence, knowing you’ve secured the best possible Air Force car loan that aligns perfectly with your service and your lifestyle. Start your journey today and make your military auto financing experience a success!