Navigating Ally Financial Car Loans: Your Ultimate Guide to Auto Financing Success

Navigating Ally Financial Car Loans: Your Ultimate Guide to Auto Financing Success Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect. However, for many, the road to car ownership often involves navigating the complexities of auto financing. Understanding your options and choosing the right lender can make all the difference in securing a deal that works for your budget and financial goals. This is where a prominent player like Ally Financial comes into the picture, offering a wide array of auto loan solutions.

As an expert blogger and professional SEO content writer, I’ve delved deep into the world of auto finance, and Ally Financial consistently stands out. This comprehensive guide will illuminate every facet of securing and managing an Ally Financial Car Loan, providing you with the in-depth knowledge needed to make informed decisions. We’ll cover everything from the application process to understanding rates, refinancing options, and how to effectively manage your loan.

Navigating Ally Financial Car Loans: Your Ultimate Guide to Auto Financing Success

Understanding Ally Financial: A Legacy in Auto Finance

Ally Financial, often simply referred to as Ally, boasts a rich history in the automotive financing sector. Originally established as General Motors Acceptance Corporation (GMAC) over a century ago, Ally has evolved into a leading digital financial services company. They are known for providing a broad spectrum of financial products, with auto financing remaining a core offering.

Their extensive experience in the industry means they understand the nuances of car buying and lending. Ally works with a vast network of dealerships across the United States, facilitating loans for millions of consumers annually. This widespread presence makes an Ally Auto Loan a readily available option for many car shoppers.

Why Consider Ally for Your Auto Loan?

Ally’s strength lies in its long-standing relationships with dealerships and its commitment to digital convenience. They offer competitive rates to qualified borrowers and have developed user-friendly platforms for loan management. For many, the familiarity and established reputation of Ally provide a sense of security in a significant financial decision.

However, it’s also important to note that Ally primarily works through dealerships. This means you won’t typically apply directly to Ally for a new car loan; instead, the dealership will submit your application to Ally and other lenders on your behalf. Understanding this indirect approach is key to navigating the process effectively.

The Ally Financial Car Loan Application Process: A Step-by-Step Breakdown

Securing an Ally Financial Car Loan begins with understanding the application journey. While the dealership often acts as the intermediary, knowing what to expect can empower you throughout the process. It’s crucial to be prepared and informed before you even step foot on the lot.

Pre-qualification vs. Full Application

Before committing to a specific vehicle, many dealerships offer a pre-qualification step. This often involves a "soft pull" on your credit, which doesn’t impact your credit score. Pre-qualification gives you an estimate of what loan terms you might qualify for, helping you set a realistic budget.

A full application, conversely, requires a "hard pull" on your credit, which can temporarily ding your score by a few points. This is the stage where Ally, or other lenders, makes a final decision on your loan approval and offers specific rates and terms. Always confirm if you’re undergoing a soft or hard inquiry.

Essential Documents You’ll Need

Based on my experience, gathering all necessary documents beforehand significantly speeds up the application process. When you’re ready to apply for an Ally Car Financing option, whether through a dealership or for refinancing, you’ll typically need:

- Proof of Identity: A valid driver’s license or state-issued ID.

- Proof of Income: Recent pay stubs, tax returns, or bank statements to demonstrate your ability to repay the loan.

- Proof of Residency: Utility bills or a lease agreement with your current address.

- Social Security Number: For credit checks.

- Vehicle Information: If you’ve already chosen a car, details like VIN, make, model, and mileage will be required.

Having these documents readily available not only streamlines the process but also demonstrates your preparedness to the lender. It shows you are serious about your application.

The Impact of Your Credit Score

Your credit score is arguably the most critical factor influencing your Ally Auto Loan rates and approval chances. Lenders use this three-digit number to assess your creditworthiness and the risk associated with lending to you. A higher credit score generally translates to lower interest rates and more favorable loan terms.

Pro tips from us: Always review your credit report before applying for any significant loan, including an Ally Car Loan. Check for any inaccuracies or errors that could be negatively impacting your score. Correcting these can significantly improve your loan prospects.

Dealership vs. Direct Application for Ally Auto Loans

For new and used car purchases, Ally Financial primarily operates as an indirect lender. This means they partner with dealerships who submit loan applications on behalf of their customers. You won’t typically walk into an Ally branch to apply for a new car loan.

However, if you’re looking to refinance an existing auto loan, you can often apply directly to Ally. This distinction is important because the initial purchase experience is heavily influenced by the dealership’s financing department. They will shop your application around to various lenders, including Ally, to find the best offer.

Ally Auto Loan Rates and Terms: What to Expect

Understanding the financial specifics of your loan is paramount. The interest rate and loan term directly impact your monthly payments and the total cost of your Ally Car Financing. Don’s just focus on the payment, but look at the entire picture.

Factors Influencing Your Rates

Several elements contribute to the interest rate you’ll be offered for an Ally Auto Loan:

- Credit Score: As mentioned, this is paramount. Borrowers with excellent credit scores (typically 720+) will qualify for the lowest rates.

- Loan Term: Shorter loan terms generally come with lower interest rates because the lender takes on less risk over a shorter period.

- Down Payment: A larger down payment reduces the loan amount, signaling less risk to the lender and potentially leading to a better rate.

- Vehicle Age and Type: New cars often have lower rates than used cars, and certain vehicle types might also influence rates.

- Current Market Conditions: Overall economic factors and prevailing interest rates set by the Federal Reserve can also play a role.

It’s vital to remember that rates are highly personalized. What one person qualifies for may be different for another, even with similar credit scores, due to these various factors.

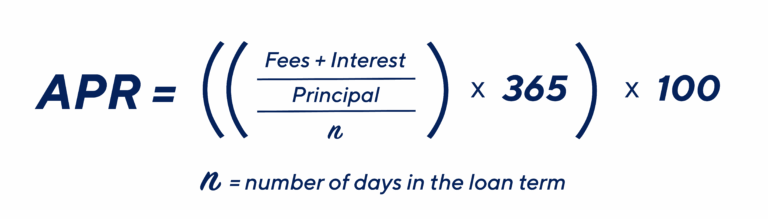

Understanding APR (Annual Percentage Rate)

When comparing loan offers, always focus on the Annual Percentage Rate (APR), not just the stated interest rate. The APR represents the true annual cost of borrowing, including not only the interest rate but also any additional fees or charges rolled into the loan. This provides a more accurate comparison between different Ally Car Loan offers or offers from other lenders.

A common mistake is focusing only on the monthly payment without considering the total interest paid over the loan term. A lower monthly payment achieved by extending the loan term often means paying significantly more in interest over the life of the loan. Always calculate the total cost.

Loan Terms: 36, 48, 60, 72, 84 Months

Ally Financial, like most auto lenders, offers a range of loan terms. Each option has its own set of pros and cons:

- Shorter Terms (e.g., 36 or 48 months): These typically come with higher monthly payments but lower overall interest paid. You own your car outright faster.

- Medium Terms (e.g., 60 or 72 months): These strike a balance, offering more manageable monthly payments while still keeping total interest relatively low. This is often a popular choice for new car buyers.

- Longer Terms (e.g., 84 months): These result in the lowest monthly payments, making expensive cars seem more affordable. However, you’ll pay significantly more in interest over the life of the loan, and you risk owing more than the car is worth (being "upside down") as it depreciates.

Carefully consider your budget and long-term financial goals when choosing an Ally Auto Loan term. A longer term might seem appealing initially, but the long-term financial implications can be substantial.

Navigating Ally Financial Used Car Loans and New Car Loans

Ally Financial provides financing solutions for both new and used vehicles, but there are distinct differences in how these loans are structured and what you might expect. Understanding these nuances can help you prepare for the specific type of financing you need.

New Car Loans with Ally

New car loans through Ally often come with the most favorable terms and interest rates. This is primarily because new vehicles typically hold their value better initially and present less risk to the lender. Dealerships frequently have incentives or special financing offers on new models that may involve Ally as a participating lender.

When purchasing a new car, you might find promotional APRs that are significantly lower than standard rates. However, these often require excellent credit. Always inquire about any special Ally Financial car loan offers when shopping for a new vehicle.

Ally Financial Used Car Loans

Used car loans, while still a strong offering from Ally, can have slightly higher interest rates compared to new car loans. This is due to factors like the vehicle’s age, mileage, and potential wear and tear, which can increase the perceived risk for the lender. Ally will have specific criteria for the age and mileage of used vehicles they are willing to finance.

It’s crucial to ensure the used vehicle you’re interested in meets Ally’s financing guidelines. Dealerships that partner with Ally will be able to guide you through this. For instance, very old or high-mileage vehicles might not qualify for standard auto loans and may require alternative financing.

Certified Pre-Owned (CPO) Vehicles

Certified Pre-Owned (CPO) vehicles occupy a unique space between new and used cars. These are used vehicles that have undergone rigorous inspections and often come with extended warranties from the manufacturer. Because of their higher quality and warranty backing, CPO vehicles might qualify for better Ally Auto Loan rates than standard used cars, sometimes even approaching new car rates.

If you’re considering a used car, exploring CPO options that qualify for favorable Ally financing can be a smart move. It offers a balance of cost savings and peace of mind.

Ally Auto Loan Refinancing: When and Why It Makes Sense

Refinancing an existing auto loan is a strategy many car owners consider to improve their financial situation. Ally Financial is a significant player in the refinancing market, offering options to help you adjust your current loan terms.

What is Auto Refinancing?

Auto refinancing involves taking out a new loan to pay off your existing car loan. The new loan will typically have different terms, such as a lower interest rate or a different loan term. This process effectively replaces your old loan with a new one, ideally one that is more advantageous to you.

It’s a common practice, and many individuals find significant savings by refinancing their car loan with Ally. The key is to understand when it’s the right move for your specific circumstances.

Reasons to Refinance Your Ally Car Loan

There are several compelling reasons why you might consider refinancing:

- Lower Interest Rate: If your credit score has improved since you initially took out your loan, or if market rates have dropped, you might qualify for a lower interest rate. This can significantly reduce the total interest you pay over the life of the loan.

- Lower Monthly Payment: By extending your loan term, you can reduce your monthly payment, freeing up cash flow. Be mindful, however, that a longer term typically means more interest paid overall.

- Change Loan Term: You might want to shorten your loan term to pay off your car faster, or extend it to lower your monthly payments if your financial situation has changed.

- Remove a Co-signer: If your financial standing has improved, refinancing can allow you to remove a co-signer from your loan, releasing them from their financial obligation.

I’ve seen many clients save thousands by refinancing their Ally car loan when their credit improved. It’s a powerful tool for financial optimization.

Ally’s Refinancing Process

The refinancing process with Ally is generally straightforward. Unlike initial purchase loans, you can often apply directly to Ally for refinancing. You’ll typically need to provide similar documentation as for an original loan, including proof of income, identity, and details of your current vehicle and loan.

Ally will review your credit history, income, and the value of your vehicle before offering new terms. Compare these new terms carefully against your current loan to ensure that refinancing truly offers a benefit. Look at the total cost of the loan, not just the monthly payment.

Managing Your Ally Financial Car Loan: Payments and Support

Once you’ve secured your Ally Financial Car Loan, effective management is key to a smooth and stress-free experience. Ally provides various tools and channels to help you stay on top of your payments and address any questions.

Convenient Payment Options

Ally offers multiple ways to make your auto loan payments, catering to different preferences:

- Online Payments: The most common and convenient method. You can set up one-time payments or schedule recurring payments through your Ally Auto online account.

- Ally Auto Mobile App: Their dedicated app provides a seamless way to manage your account, view statements, and make payments on the go.

- Auto-Pay (ACH): Setting up automatic payments directly from your bank account ensures you never miss a due date. This can also sometimes qualify you for a slight interest rate discount.

- Pay by Phone: You can call Ally’s customer service to make a payment over the phone.

- Pay by Mail: Traditional check payments are also an option, though less common now.

Choosing the method that best fits your routine helps maintain a good payment history, which is crucial for your credit score.

The Ally Auto App: Your Loan Management Hub

The Ally Auto app is a robust tool designed to put loan management at your fingertips. Through the app, you can:

- View account details: Check your current balance, payment history, and loan terms.

- Make payments: Schedule or make one-time payments easily.

- Set up alerts: Receive notifications for upcoming payments or account updates.

- Access statements: View and download your monthly statements.

Utilizing the app can significantly enhance your experience with your Ally Financial car loan, making it easier to stay organized and informed.

Ally Customer Service and Support

Should you have any questions or encounter issues with your Ally Auto Loan, their customer service channels are readily available. You can typically reach them via:

- Phone: A dedicated customer service line for auto loans.

- Online Chat: Often available through their website or the Ally Auto app.

- Secure Message: Through your online account, you can send secure messages for non-urgent inquiries.

For the most up-to-date information on Ally’s current offerings and contact methods, you can always visit their official website at Ally Financial Auto Loans. They provide comprehensive resources and FAQs to assist their customers.

Making Extra Payments and Early Payoff

Making extra payments on your Ally Financial Car Loan can be a smart financial move. Any amount paid over your minimum monthly payment typically goes directly towards the principal balance of your loan. This reduces the amount of interest you’ll pay over the loan’s life and helps you pay off the loan faster.

Before making extra payments, confirm with Ally that there are no prepayment penalties. While rare for standard auto loans, it’s always good to verify. Paying off your loan early can save you a significant amount in interest, freeing up your budget for other financial goals.

Addressing Common Concerns and FAQs about Ally Auto Loans

When considering an Ally Financial Car Loan, it’s natural to have questions, especially regarding specific situations or challenges. Let’s tackle some common concerns.

Ally Financial and Bad Credit Car Loans

Can you get an Ally Financial Car Loan with bad credit? While Ally does finance a wide range of credit profiles, securing a loan with poor credit (typically below 600) can be more challenging. If approved, you can expect significantly higher interest rates to offset the increased risk for the lender.

If you have bad credit, consider these strategies:

- Improve Your Credit Score: Prioritize paying down other debts, making all payments on time, and checking your credit report for errors. For more detailed advice on improving your credit score, check out our guide on Improving Your Credit Score for a Better Auto Loan (hypothetical internal link).

- Larger Down Payment: A substantial down payment can mitigate risk for Ally and increase your approval chances.

- Co-signer: A financially strong co-signer can significantly improve your application.

The Role of a Co-signer

A co-signer is someone who agrees to be equally responsible for your loan if you default. For individuals with limited credit history or a low credit score, adding a co-signer with good credit can make an Ally Auto Loan approval possible. It also often helps secure a better interest rate.

However, a co-signer takes on significant risk. If you miss payments, their credit score will also be negatively impacted. Ensure both parties fully understand the implications before proceeding with a co-signed loan.

Lease vs. Buy with Ally Financial

Ally Financial offers both auto loans (buying) and leasing options. The choice between leasing and buying depends heavily on your lifestyle, driving habits, and financial preferences:

- Leasing: You essentially rent the car for a set period, making lower monthly payments than buying, but you don’t own the vehicle. It’s great for those who like to drive a new car every few years.

- Buying: You own the car outright once the loan is paid off, building equity. Monthly payments are higher, but you have no mileage restrictions and can customize the car.

Ally can facilitate both options through their dealership network. Weigh the pros and cons carefully to decide which path aligns best with your needs.

Dealing with Late Payments or Defaults

Missing payments on your Ally Financial Car Loan can have serious consequences. Late payments will incur fees and negatively impact your credit score. Repeated late payments or defaulting on your loan can lead to vehicle repossession and severe, long-lasting damage to your credit.

If you anticipate difficulty making a payment, contact Ally Financial immediately. They may offer options like payment deferral or modified payment plans, depending on your situation. Open communication is always the best first step to avoid more drastic measures.

Pro Tips for a Smooth Ally Financial Car Loan Experience

To ensure you have the best possible experience with your Ally Financial Car Loan, here are some expert tips gleaned from years in the auto finance industry.

Negotiate Wisely at the Dealership

Remember that the dealership is a business, and their goal is to maximize profit. When applying for an Ally Car Loan through a dealer, don’t be afraid to negotiate. This includes not only the vehicle price but also the interest rate. Even if Ally is offering a specific rate, the dealership might have some flexibility or other lenders to consider.

Always arrive prepared with research on vehicle prices and your credit score. This knowledge is your biggest negotiation tool.

Understand All Terms and Conditions

Before signing any Ally Auto Loan agreement, read every single line of the contract. Understand the interest rate, the full loan term, all fees, and any penalties for late payments or early payoff. If something is unclear, ask questions until you fully comprehend it.

Ignorance is not bliss when it comes to financial contracts. Take your time, and don’t feel pressured to sign until you’re completely comfortable.

Monitor Your Credit Regularly

Even after securing your Ally Financial car loan, continue to monitor your credit score. Regular monitoring helps you catch any fraudulent activity or errors that could affect your financial standing. It also allows you to track improvements that might make you eligible for refinancing down the line.

Many banks and credit card companies now offer free credit score monitoring. Utilize these tools to stay informed.

Build an Emergency Fund

While not directly related to the Ally Car Loan application, having an emergency fund is crucial for managing any debt. Life is unpredictable, and unexpected expenses can arise. An emergency fund provides a buffer, ensuring you can continue to make your Ally Auto Loan payments even if you face a temporary financial setback.

This financial cushion prevents you from falling behind on payments, which could otherwise damage your credit and incur late fees. Want to understand interest rates better? Read our article on Demystifying Auto Loan Interest Rates: What You Need to Know (hypothetical internal link).

Conclusion: Your Path to Ally Financial Car Loan Success

Navigating the world of auto financing, especially with a major lender like Ally Financial, requires knowledge, preparation, and a strategic approach. From understanding the application process and deciphering interest rates to exploring refinancing options and effectively managing your payments, every step contributes to a successful car ownership journey.

Ally Financial stands as a strong contender in the auto loan market, offering a range of solutions for both new and used vehicles, as well as refinancing opportunities. By leveraging the insights provided in this comprehensive guide, you are now well-equipped to make informed decisions, secure favorable terms, and confidently manage your Ally Auto Loan. Drive away with peace of mind, knowing you’ve made a smart financial choice.