Navigating Americu Car Loan Rates: Your Ultimate Guide to Driving Smarter

Navigating Americu Car Loan Rates: Your Ultimate Guide to Driving Smarter Carloan.Guidemechanic.com

The dream of a new set of wheels – whether it’s a sleek sedan, a family-friendly SUV, or a rugged pickup – often begins with a critical question: how will you finance it? For many in the communities it serves, Americu Credit Union stands out as a strong contender. They offer a member-focused approach to lending, which can translate into competitive Americu car loan rates and excellent service.

However, simply knowing a lender exists isn’t enough. To truly secure the best deal and make an informed decision, you need to understand the nuances of how car loan rates are determined and what Americu specifically offers. This comprehensive guide will equip you with all the knowledge you need, transforming you from a hopeful car buyer into a savvy loan applicant.

Navigating Americu Car Loan Rates: Your Ultimate Guide to Driving Smarter

What Makes Americu Different? The Credit Union Advantage

Before diving into the specifics of Americu car loan rates, it’s crucial to understand the unique nature of a credit union. Unlike traditional banks, which are for-profit institutions owned by shareholders, credit unions like Americu are non-profit financial cooperatives. They are owned by their members.

This fundamental difference often translates into tangible benefits for borrowers. Because their primary goal isn’t to maximize shareholder profits, credit unions can frequently offer more favorable loan rates, lower fees, and a more personalized customer service experience. Based on my experience in the financial industry, many people overlook credit unions, assuming they are just smaller banks. This is a common mistake that can cost you significant savings over the life of a loan.

Americu, as a member-centric organization, reinvests its earnings back into the credit union through improved services, better rates, and educational programs for its members. This cooperative spirit is a significant advantage when you’re seeking financing for a major purchase like a car. They are motivated to help their members succeed financially, rather than simply meeting quarterly profit targets.

Understanding Americu Car Loan Rates: The Core Factors at Play

When you apply for an auto loan with Americu, several key factors come into play that directly influence the interest rate you’ll be offered. These aren’t arbitrary figures; they’re calculated based on a careful assessment of risk and your financial profile. Understanding these elements is your first step towards securing the most competitive Americu auto loan possible.

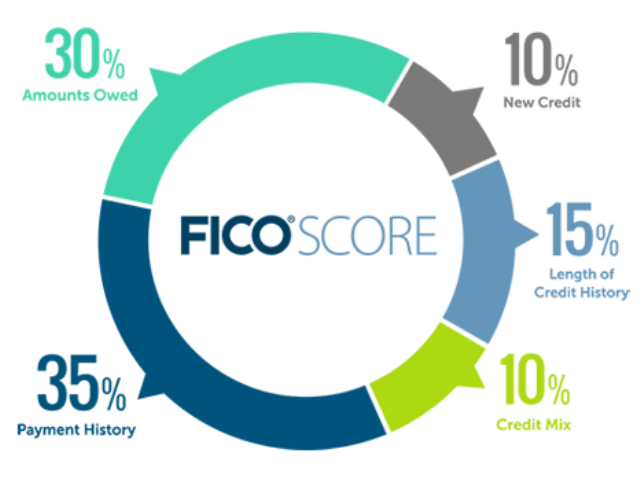

Your Credit Score: The Cornerstone of Your Rate

Without a doubt, your credit score is the single most important factor determining your car loan interest rate. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. A higher credit score signals to Americu that you are a reliable borrower, leading to lower interest rates.

Typically, scores are categorized into ranges: excellent, good, fair, and poor. Borrowers with excellent credit (generally 720+) will qualify for the lowest Americu interest rates, as they pose the least risk. Conversely, those with lower scores might still get approved, but they will likely face higher rates to compensate Americu for the increased risk involved.

Pro tips from us: Always check your credit score and credit report well before applying for any loan. This allows you time to correct any errors and understand where you stand. There are many free services available to help you monitor your credit.

Loan Term (Length): Short vs. Long

The loan term, or the length of time you have to repay the loan, also significantly impacts your Americu car loan rates and your total cost. Common terms range from 36 months to 72 or even 84 months. While a longer term means lower monthly payments, it almost always results in a higher interest rate and a greater total amount of interest paid over the life of the loan.

Americu, like most lenders, views longer terms as carrying more risk because there’s more time for things to go wrong (e.g., job loss, car depreciation). Therefore, they typically charge a slightly higher interest rate for extended repayment periods. Opting for the shortest term you can comfortably afford is often the most financially savvy decision.

Loan Amount and Vehicle Type: New vs. Used

The actual amount you need to borrow and the type of vehicle you’re purchasing also play a role. Generally, new car loans tend to have slightly lower interest rates than used car loans. This is because new cars depreciate more predictably and hold their value better initially, making them a less risky asset for Americu to finance.

For used cars, the age and mileage of the vehicle can also influence the rate. Older cars with high mileage might be subject to higher rates or specific lending criteria. Americu will assess the vehicle’s value to ensure it aligns with the loan amount, protecting both you and the credit union.

Your Down Payment: Showing Your Commitment

Making a substantial down payment can significantly improve your chances of securing a lower Americu auto loan interest rate. A larger down payment reduces the amount you need to borrow, which in turn reduces Americu’s risk. It also demonstrates your financial commitment to the purchase.

When you put down a significant portion of the car’s price, you instantly have more equity in the vehicle. This makes you a more attractive borrower. Aim for at least 10-20% of the vehicle’s purchase price as a down payment if your budget allows.

Relationship with Americu: Member Benefits

As a credit union, Americu often rewards its loyal members. If you have an established banking relationship with Americu, perhaps a checking or savings account, or other loans in good standing, you might be eligible for preferential Americu car loan rates. This is part of the credit union’s philosophy of giving back to its members.

It’s always worth discussing your existing relationship with a loan officer. They might be able to find additional discounts or benefits specifically for you. Building a strong financial history with a single institution can yield surprising advantages.

Types of Americu Car Loans: Tailored to Your Needs

Americu understands that not all car buying situations are the same. They offer a range of auto loan products designed to meet various needs, whether you’re buying brand new, pre-owned, or looking to save money on an existing loan.

New Car Loans: For That Fresh-Off-the-Lot Feeling

If you’re eyeing a brand-new vehicle, Americu’s new car loans are specifically structured for this purpose. These loans often come with the most competitive Americu interest rates, reflecting the lower risk associated with financing a vehicle with zero miles and a full manufacturer’s warranty. The terms for new car loans can extend up to 84 months, though, as mentioned, shorter terms are often more cost-effective.

When considering a new car loan, ensure you’ve done your research on the specific make and model. Having a clear idea of the vehicle you want will streamline the application process and help Americu tailor the best loan offer for you.

Used Car Loans: Smart Savings on Pre-Owned Vehicles

Buying a used car can be a fantastic way to save money and still get a reliable vehicle. Americu offers robust used car loan options, but the Americu used car loan rates and terms might vary slightly compared to new car loans. Factors like the vehicle’s age, mileage, and condition are more closely scrutinized.

Typically, Americu will have limits on the age or mileage of a used car they will finance, often around 7-10 years old and under 100,000-125,000 miles. These parameters help manage the risk of financing older vehicles. Always get a pre-purchase inspection for a used car, regardless of where you get your loan.

Auto Loan Refinancing: Optimizing Your Existing Loan

Perhaps you already have a car loan but are looking for a better deal. This is where Americu’s auto loan refinancing options come into play. Refinancing allows you to replace your current car loan with a new one, ideally with a lower interest rate or more favorable terms. This can significantly reduce your monthly payments or the total interest paid over time.

Common mistakes to avoid are not exploring refinancing options when your credit score has improved, or when market rates have dropped since you originally financed your car. Many people secure their initial loan at the dealership, often without comparing rates, and end up paying more than necessary. Refinancing with Americu could be a smart financial move if your circumstances have changed or if you found a better rate.

The Americu Car Loan Application Process: A Step-by-Step Guide

Securing an Americu car loan doesn’t have to be a daunting process. By understanding the steps involved and preparing adequately, you can navigate it smoothly and efficiently.

Step 1: Preparation is Key – Gather Your Documents

Before you even begin the application, gather all necessary documentation. This typically includes:

- Proof of Identity: Driver’s license, state ID.

- Proof of Income: Recent pay stubs, tax returns, or bank statements.

- Proof of Residence: Utility bill, lease agreement.

- Vehicle Information: If you’ve already chosen a car, have the VIN, make, model, and mileage ready.

- Credit History: While Americu will pull your credit report, it’s wise to review your own beforehand.

Having these documents organized will expedite the entire application process. Any delays in providing information can prolong your wait for approval.

Step 2: The Power of Pre-Approval

One of the smartest moves you can make is to get pre-approved for an Americu auto loan before you even set foot in a dealership. Pre-approval means Americu has reviewed your financial information and determined how much you qualify to borrow and at what interest rate, based on current Americu car loan rates.

Pro tips from us: Get pre-approved before you step onto the dealership lot. This gives you immense bargaining power, turning you into a cash buyer in the eyes of the salesperson. You’ll know exactly what you can afford, separating the car price negotiation from the financing negotiation.

Step 3: Submitting Your Application

Americu offers convenient ways to apply for a car loan. You can typically apply online through their secure portal, visit one of their local branches, or even apply over the phone. The application form will ask for personal, financial, and employment details.

Be sure to fill out the application accurately and completely. Inaccurate information can lead to delays or even rejection. If you have questions, don’t hesitate to reach out to an Americu loan officer for clarification.

Step 4: Approval and Funding

Once your application is submitted, Americu will review your information, pull your credit report, and assess your eligibility. This process can sometimes be very quick, especially if you’re pre-approved. If approved, you’ll receive a loan offer detailing your Americu car loan rates, term, and monthly payments.

After you accept the offer, Americu will guide you through the final steps, which involve signing the loan documents. The funds will then be disbursed, either directly to you (for private sales) or to the dealership. You’re now ready to drive off in your new car!

How to Get the Best Americu Car Loan Rates: Strategies for Success

Securing a car loan is more than just applying; it’s about strategizing to get the most favorable terms possible. Here are actionable steps you can take to ensure you qualify for the best Americu auto loan rates.

1. Improve Your Credit Score

This is paramount. If you have time before your car purchase, work on boosting your credit score. Pay down existing debts, especially credit card balances, and make all payments on time. A higher score directly translates to lower Americu interest rates.

2. Increase Your Down Payment

As discussed, a larger down payment reduces the loan amount and Americu’s risk. This makes you a more attractive borrower and can lead to a lower interest rate. Even an extra few hundred dollars can make a difference.

3. Choose a Shorter Loan Term

While longer terms offer lower monthly payments, they come with higher overall interest. If your budget allows, opt for a 36-month or 48-month loan over a 60-month or 72-month one. You’ll pay significantly less in interest over the life of the loan.

4. Negotiate (Even with Credit Unions)

While Americu offers competitive rates, it doesn’t hurt to inquire if there are any special promotions or member-specific discounts you might be eligible for. Sometimes, a simple conversation can uncover additional savings.

5. Consider a Co-Signer (with Caution)

If your credit score isn’t ideal, a co-signer with excellent credit can help you qualify for better Americu car loan rates. However, understand that a co-signer is equally responsible for the debt, so choose someone you trust and who understands the commitment.

6. Automate Payments for Potential Discounts

Some lenders, including credit unions, offer a small interest rate discount (e.g., 0.25%) for setting up automatic payments from your checking account. This guarantees on-time payments and reduces administrative costs for Americu. Always ask if such discounts are available.

Based on my years in the auto finance industry, these strategies consistently yield better outcomes for borrowers. Diligence and preparation are your greatest assets.

Comparing Americu Rates: What to Look For Beyond the Number

When evaluating Americu car loan rates or comparing them with other lenders, it’s vital to look beyond just the headline interest rate. Several other factors can impact the true cost of your loan.

APR vs. Interest Rate: A Crucial Distinction

The Annual Percentage Rate (APR) is the most important figure to consider. It includes not just the interest rate but also any fees associated with the loan, expressed as an annual percentage. The interest rate is simply the cost of borrowing the principal amount.

A lower interest rate might seem appealing, but if it comes with high origination fees, the APR could still be higher than a loan with a slightly higher interest rate but no fees. Always compare APRs when shopping for a loan.

Fees: The Hidden Costs

Inquire about any potential fees associated with the Americu auto loan. These could include application fees, origination fees, or documentation fees. While credit unions typically have fewer fees than banks, it’s always good to confirm. Also, ask about late payment fees or fees for changing payment dates.

Understanding these charges upfront prevents any unwelcome surprises later on. Transparency is key in any financial agreement.

Prepayment Penalties: Ensure Flexibility

Some loan agreements include prepayment penalties, meaning you’ll be charged a fee if you pay off your loan early. This is less common with credit unions like Americu, but it’s essential to confirm that your Americu car loan does not have such clauses. You want the flexibility to pay down your loan faster if your financial situation improves.

Insurance Requirements

Americu, like all auto lenders, will require you to carry full coverage insurance on your financed vehicle until the loan is paid off. This protects their interest in the asset. Ensure you budget for these insurance costs, as they are a necessary part of vehicle ownership.

Beyond the Rate: Other Americu Benefits to Consider

While competitive Americu car loan rates are a primary draw, the credit union offers additional advantages that contribute to a superior borrowing experience. These benefits often go unnoticed but add significant value.

Personalized Service

As a member-owned institution, Americu prides itself on personalized service. You’re not just a number; you’re a member of their community. This often means more attentive loan officers, a willingness to work with you through challenges, and a more human approach to lending.

Financial Education Resources

Many credit unions, including Americu, offer financial education resources to their members. This could include workshops, online tools, or one-on-one counseling to help you make smarter financial decisions, including managing your car loan and overall budget effectively.

Member Dividends and Rewards

Depending on Americu’s financial performance and specific programs, some credit unions return profits to members in the form of dividends or other rewards. While not guaranteed, this is a potential benefit unique to the credit union model.

Convenience and Accessibility

Americu typically offers modern banking conveniences, including online loan applications, mobile banking, and a network of branches. This makes managing your Americu auto loan and other accounts straightforward and accessible.

Common Mistakes to Avoid When Applying for an Americu Car Loan

Even with all the right information, it’s easy to make missteps. Being aware of common pitfalls can save you money and stress.

1. Not Checking Your Credit Score

As emphasized, your credit score is critical. Failing to check it beforehand means you go into the application process blind, unaware of your true borrowing power. Always get a free copy of your credit report from AnnualCreditReport.com.

2. Applying to Too Many Lenders

While comparing rates is crucial, applying for multiple loans within a short period can negatively impact your credit score. Each "hard inquiry" can temporarily lower your score. Aim to get pre-approved by 2-3 lenders, including Americu, within a 14-45 day window to have them count as a single inquiry.

3. Focusing Only on Monthly Payment

A common mistake is fixating solely on the monthly payment. A low monthly payment often comes with a longer loan term and a higher overall cost due to more interest paid. Always consider the total cost of the loan, not just the monthly figure.

4. Not Reading the Fine Print

Loan agreements can be lengthy and filled with jargon, but it’s essential to read and understand every clause. Don’t sign anything you don’t fully comprehend. Ask Americu loan officers to explain any confusing terms.

5. Falling for Dealership Financing Without Comparing

Dealerships often offer their own financing, which might seem convenient. However, they may not always offer the best rates. Common mistakes to avoid are letting the excitement of a new car overshadow careful financial planning. Always have your Americu pre-approval in hand to compare against any dealership offers. This ensures you get the best deal, whether it’s from Americu or elsewhere.

Conclusion: Drive Smart with Americu

Navigating the world of car loans can feel complex, but with the right knowledge, you can make a confident and financially sound decision. Americu Credit Union offers a compelling option for those seeking competitive Americu car loan rates coupled with the benefits of a member-focused institution.

By understanding the factors that influence your rate, exploring the different loan types, and employing smart strategies, you are well-positioned to secure an auto loan that fits your budget and financial goals. Remember, the lowest interest rate isn’t the only metric; consider the total cost, fees, and the quality of service.

Armed with this comprehensive guide, you’re ready to approach your car purchase with confidence and clarity. Take the time to prepare, compare, and choose wisely. Your journey to a new car and smarter financing starts here. Start your journey with Americu today and drive smarter tomorrow!