Navigating Arkansas Car Loans: Your Ultimate Guide to Driving Away Happy

Navigating Arkansas Car Loans: Your Ultimate Guide to Driving Away Happy Carloan.Guidemechanic.com

Securing a car loan can feel like a complex journey, especially when you’re navigating the specific landscape of a state like Arkansas. Whether you’re dreaming of a brand-new pickup for the Ozarks or a reliable sedan for city commutes in Little Rock, understanding the intricacies of Arkansas car loans is your first step towards making a smart financial decision. This isn’t just about finding a lender; it’s about empowering yourself with knowledge to secure the best possible terms, ensuring you drive away not just with a new car, but with financial peace of mind.

Based on my years of experience in the automotive financing sector, I’ve seen firsthand how a lack of information can lead to costly mistakes. My mission with this comprehensive guide is to demystify the process, offering you an in-depth look at everything you need to know about auto financing in the Natural State. From understanding different loan types to mastering the application process and avoiding common pitfalls, we’ll cover it all. Let’s embark on this journey together to make your next car purchase a seamless and rewarding experience.

Navigating Arkansas Car Loans: Your Ultimate Guide to Driving Away Happy

Understanding the Arkansas Car Loan Landscape

Arkansas presents a unique environment for car buyers and loan seekers. The state’s diverse economy, ranging from agricultural heartlands to growing urban centers, influences everything from vehicle availability to lending practices. Consequently, understanding these local nuances is crucial for anyone seeking car loans in Arkansas.

The local market dynamics can affect interest rates, lender availability, and even the types of vehicles that are most popular. For instance, in more rural areas, trucks and SUVs might be in higher demand, potentially influencing their resale value and loan terms. Conversely, in cities like Fayetteville or Fort Smith, smaller, more fuel-efficient cars might dominate.

Why is getting the right loan so crucial? A car loan isn’t just a monthly payment; it’s a significant financial commitment that impacts your budget for several years. An ill-suited loan can lead to higher overall costs, financial strain, and even difficulty maintaining your vehicle. Conversely, a well-structured loan tailored to your financial situation can save you thousands over its lifetime and contribute positively to your credit health.

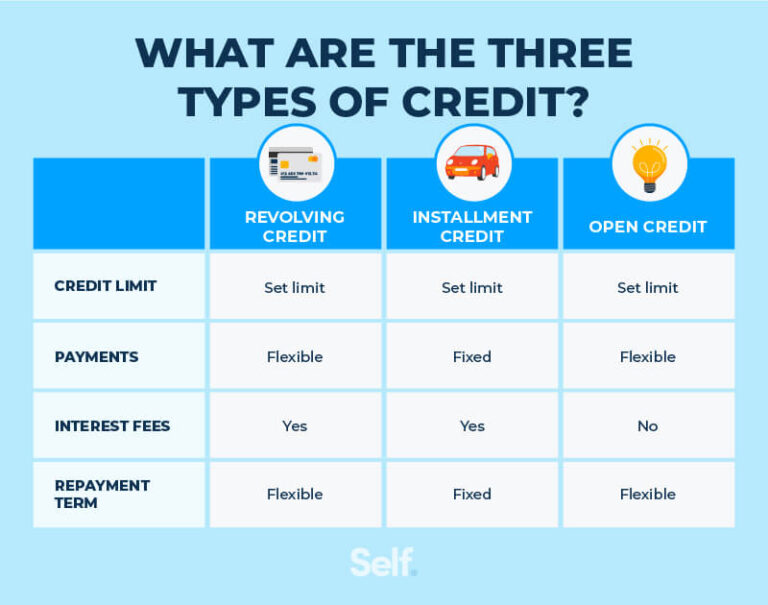

Types of Car Loans Available in Arkansas

When you’re looking for auto financing in Arkansas, you’ll encounter several different types of loans, each designed for specific situations. Understanding these options is key to choosing the one that best fits your needs. Don’t assume all car loans are the same; they vary significantly in their terms, rates, and suitability.

New Car Loans

These loans are specifically for brand-new vehicles straight from the dealership. Typically, new car loans in Arkansas offer some of the most competitive interest rates. This is because new cars hold their value better initially and pose less risk to lenders.

Lenders also often see new car buyers as more financially stable, which can translate into better terms. Expect a variety of offers from dealerships, banks, and credit unions, often with promotional rates directly from manufacturers.

Used Car Loans

Used car loans are, as the name suggests, for pre-owned vehicles. While rates for used car loans in Arkansas might be slightly higher than for new cars, they are still very accessible. The interest rate often depends on the age, mileage, and condition of the vehicle, as older cars are generally considered higher risk.

It’s vital to get a pre-purchase inspection for any used vehicle you consider. Lenders will also factor in the vehicle’s market value, often using guides like Kelley Blue Book or NADA to determine how much they are willing to lend.

Refinance Car Loans

If you already have a car loan but want to improve its terms, a refinance car loan in Arkansas might be your answer. This involves taking out a new loan to pay off your existing one. People often refinance to secure a lower interest rate, reduce their monthly payments, or change their loan term.

Based on my experience, refinancing is particularly beneficial if your credit score has improved since you first took out the loan. It can significantly reduce your total interest paid over the life of the loan.

Private Party Loans

Buying a car from a private seller in Arkansas often requires a specific type of loan. Many traditional lenders offer private party loans, though the process might involve a bit more paperwork and due diligence. The lender will typically want to verify the vehicle’s title, condition, and market value.

While private party sales can offer better prices, securing financing can sometimes be a bit more complex than buying from a dealership. It’s crucial to have all vehicle information ready for your lender.

Lease-to-Own Options (Alternative)

While not strictly a loan, lease-to-own options are another way to acquire a vehicle. This arrangement allows you to lease a car for a set period with the option to purchase it at the end of the term. These can be attractive for those who aren’t ready for full ownership or have specific credit challenges.

However, it’s important to thoroughly understand the terms, including the residual value and any fees, before committing. Always compare the total cost of a lease-to-own agreement with a traditional loan.

Key Factors Affecting Your Arkansas Car Loan Approval and Rates

Several critical factors weigh heavily on whether your Arkansas auto loan application is approved and what interest rate you’ll receive. Understanding these elements beforehand allows you to proactively strengthen your application and secure more favorable terms. Lenders evaluate your financial profile comprehensively, not just one isolated number.

Credit Score

Your credit score is arguably the most influential factor. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. A higher score signals to lenders that you are a reliable borrower, leading to lower interest rates on Arkansas car loans.

Scores typically range from 300 to 850, with anything above 700 generally considered excellent. If your score is lower, don’t despair; there are still options, but your rates might be higher. Checking your credit report for errors is a crucial first step.

Income and Employment Stability

Lenders want to be confident you can consistently make your monthly payments. Your income and employment history provide this assurance. A stable job with a consistent income for at least a year or two is often preferred.

They’ll look at your gross monthly income and may ask for pay stubs or tax returns as proof. Steady employment demonstrates reliability and capacity to repay the loan.

Down Payment Amount

A significant down payment reduces the amount you need to borrow, which lowers the lender’s risk. It also means you’ll pay less interest over the life of the loan. Many lenders prefer a down payment of at least 10-20% for new cars.

From our perspective as financial advisors, a larger down payment is always a smart move. It can even help you secure approval if your credit isn’t perfect.

Debt-to-Income (DTI) Ratio

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to assess your ability to take on additional debt. A lower DTI (typically below 43%) indicates that you have more disposable income to cover new loan payments.

If your DTI is too high, it might signal that you’re overextended, making lenders hesitant to approve another loan. Managing your existing debt is crucial before applying for new credit.

Loan Term

The loan term refers to the length of time you have to repay the loan, usually expressed in months (e.g., 36, 60, 72 months). A shorter loan term generally means higher monthly payments but less interest paid overall. Conversely, a longer term reduces monthly payments but increases the total interest.

Pro tips from us: While a longer term might seem attractive for lower monthly payments, always consider the total cost. Sometimes, a slightly higher monthly payment for a shorter term is more financially prudent.

Vehicle Age and Type

The vehicle itself plays a role. Newer cars with lower mileage typically qualify for better rates because they depreciate less rapidly and are less likely to require expensive repairs. Older, high-mileage vehicles are considered higher risk.

Lenders also consider the make and model. Some vehicles hold their value better than others, which can influence loan terms.

The Application Process: Step-by-Step Guide for Arkansas Residents

Navigating the application process for Arkansas car loans can seem daunting, but breaking it down into manageable steps makes it much simpler. Following this guide will not only streamline your experience but also put you in a stronger negotiating position. Preparation is your best ally in this process.

Step 1: Budgeting and Research

Before you even think about visiting a dealership, determine what you can realistically afford. Look at your monthly income, expenses, and existing debts. Use online car loan calculators to estimate potential monthly payments based on different interest rates and loan terms.

This step also involves researching vehicles that fit your budget and lifestyle. Don’t just focus on the car’s price; factor in insurance, maintenance, and fuel costs.

Step 2: Credit Check & Pre-Approval

Pull your credit report from all three major bureaus (Experian, Equifax, TransUnion) and review it for accuracy. Dispute any errors immediately. Knowing your score empowers you to anticipate what rates you might qualify for.

Next, seek pre-approval from a few different lenders—banks, credit unions, and online lenders. Pre-approval gives you a firm offer of how much you can borrow and at what interest rate, before you even step onto a car lot. This is invaluable negotiating power.

Step 3: Gathering Required Documents

Lenders will need several documents to verify your identity and financial standing. Having these ready in advance will significantly speed up the approval process.

Common documents include:

- Government-issued photo ID (driver’s license or state ID)

- Proof of residence (utility bill, lease agreement)

- Proof of income (pay stubs, tax returns, bank statements)

- Social Security Number

- Trade-in vehicle information (if applicable, title and registration)

Step 4: Shopping for Lenders

Don’t just take the first offer you receive. Shop around! Compare interest rates, fees, and terms from various sources.

- Banks: Offer competitive rates, especially for those with good credit.

- Credit Unions: Often have lower rates and more flexible terms for members.

- Dealerships: Provide convenience and sometimes special manufacturer incentives, but always compare their offer to your pre-approval.

- Online Lenders: Offer quick approvals and a wide range of options.

Step 5: Vehicle Selection & Negotiation

With your pre-approval in hand, you know your maximum budget. Now you can focus on finding the perfect car without worrying about financing. Negotiate the price of the car as a separate transaction from the financing.

Common mistakes to avoid are discussing your monthly payment desires before the car’s price is finalized. Always negotiate the total purchase price first.

Step 6: Finalizing the Loan

Once you’ve chosen your vehicle and agreed on a price, review the final loan documents meticulously. Ensure the interest rate, loan term, and all fees match what you were offered. Ask questions about anything you don’t understand.

Sign the paperwork only when you are completely satisfied and clear on all terms. This is a legally binding contract, so take your time.

Navigating Bad Credit Car Loans in Arkansas

Having a less-than-perfect credit score doesn’t mean you can’t get an auto loan in Arkansas. It simply means the process might require a different approach and a bit more strategy. While challenging, securing a car loan with bad credit is absolutely possible.

Lenders who specialize in bad credit car loans in Arkansas understand that financial setbacks happen. They focus more on your current ability to pay rather than solely on past credit issues. However, be prepared for potentially higher interest rates, as lenders perceive a greater risk.

Strategies for approval with bad credit include:

- Larger Down Payment: This significantly reduces the amount you need to borrow and signals to lenders that you’re serious and committed.

- Co-signer: A co-signer with good credit can dramatically improve your chances of approval and help secure a better rate. They share responsibility for the loan, so choose someone trustworthy.

- Secured Loans: Some lenders might offer secured loans, where the car itself acts as collateral. This can sometimes provide better terms than an unsecured personal loan.

- Demonstrate Stability: Show proof of stable employment and income. Lenders want to see that you have the consistent means to make payments.

It’s crucial to be wary of predatory lenders who offer "guaranteed" approval without checking your credit. These often come with exorbitant interest rates and hidden fees. Always research a lender’s reputation and read reviews. Our advice is to stick with reputable banks, credit unions, or well-established online lenders who offer transparent terms. Getting a bad credit loan and making consistent, on-time payments can actually be a great way to start rebuilding your credit score.

Understanding Interest Rates and Fees in Arkansas

When securing Arkansas car loans, understanding the true cost involves more than just the advertised interest rate. You need to grasp the difference between various financial terms and be aware of all potential fees. This knowledge empowers you to compare loan offers accurately and avoid unexpected expenses.

APR vs. Interest Rate

The interest rate is the percentage charged by the lender for borrowing the principal amount. It’s the cost of borrowing money. However, the Annual Percentage Rate (APR) provides a more comprehensive picture of the loan’s total cost.

The APR includes the interest rate plus any additional fees associated with the loan, expressed as a single annual percentage. Therefore, when comparing loan offers, always look at the APR, as it reflects the true yearly cost of your financing. A lower APR always means a cheaper loan.

Common Fees Associated with Car Loans

Beyond interest, several fees can add to the total cost of your auto financing in Arkansas:

- Origination Fees: A fee charged by the lender for processing your loan application. Not all lenders charge this, so inquire upfront.

- Documentation Fees (Doc Fees): Charged by dealerships for preparing paperwork. These can vary widely, and in Arkansas, while they are legal, they must be disclosed.

- Late Payment Fees: Incurred if you miss a payment deadline. These can be substantial and negatively impact your credit score.

- Prepayment Penalties: Some loans might charge a fee if you pay off your loan early. This is less common with auto loans but always worth checking.

- Title and Registration Fees: These are state-mandated fees for transferring ownership and registering the vehicle.

While Arkansas does not have specific state-wide interest rate caps for motor vehicle installment loans that significantly differ from general usury laws (which can be complex), it’s important to remember that rates must be "reasonable" and disclosed transparently. Always scrutinize the loan agreement for any hidden charges or clauses.

Choosing the Right Lender in Arkansas

The lender you choose for your Arkansas car loan can significantly impact your overall experience and the terms of your financing. With various options available, it’s essential to understand the advantages and disadvantages of each. From our perspective, finding the right fit is about balancing rates, customer service, and convenience.

Banks

Traditional banks are a popular choice for car loans. They often offer competitive interest rates, especially for borrowers with excellent credit scores. Banks provide a sense of stability and often have extensive resources.

However, their approval processes can sometimes be more rigid, and their customer service might feel less personal than smaller institutions. They are generally a good option if you have a strong financial history.

Credit Unions

Credit unions are member-owned financial cooperatives, which often translates to more favorable loan terms and lower interest rates. They are known for their personalized customer service and community focus. If you’re eligible to join one (often based on residency, employer, or association), a credit union can be an excellent choice for affordable car loans in Arkansas.

Their approval criteria can sometimes be more flexible than large banks, especially for those with average credit.

Dealership Financing

Most car dealerships offer in-house financing or work with a network of lenders. This option provides immense convenience, as you can handle the car purchase and financing all in one place. Dealerships can sometimes offer special manufacturer incentives or promotional rates.

However, it’s crucial to compare their offer with your pre-approved loans. While convenient, the dealership’s financing might not always be the absolute best rate available. Always compare to ensure you’re getting a competitive deal. For more in-depth advice on comparing lenders, you might find our article on Tips for Choosing the Best Auto Loan Lender helpful. (Internal Link)

Online Lenders

Online lenders have grown in popularity due to their speed and convenience. You can apply from anywhere, often receive quick decisions, and compare multiple offers with ease. They often cater to a wider range of credit scores, including those with less-than-perfect credit.

While fast, online lenders might lack the personal touch of a local bank or credit union. Ensure the online lender is reputable and secure before sharing your personal information.

Refinancing Your Car Loan in Arkansas

Refinancing your Arkansas car loan can be a smart financial move under certain circumstances. It involves replacing your current auto loan with a new one, often with different terms. This strategy can significantly impact your monthly budget and overall financial health.

When does it make sense to refinance?

- Lower Interest Rates: If interest rates have dropped since you took out your original loan, or if your credit score has significantly improved, you might qualify for a lower rate. This can reduce your monthly payments and the total interest paid.

- Improved Credit Score: As mentioned, a better credit score makes you a more attractive borrower, potentially unlocking better rates.

- Change in Financial Situation: If you’re struggling with high monthly payments, refinancing to a longer term can lower them, providing some breathing room. Conversely, if you have extra cash, refinancing to a shorter term can save you interest.

- Removing a Co-signer: If you had a co-signer to get approved initially, and your credit has since improved, refinancing can allow you to remove them from the loan.

The process of refinancing is similar to applying for an initial loan. You’ll gather your financial documents, shop for new lenders (banks, credit unions, online lenders), and compare their offers. Once approved, the new lender pays off your old loan, and you begin making payments to the new lender under the new terms. Always ensure the savings from a lower interest rate outweigh any new fees associated with the refinancing process.

Important Arkansas-Specific Considerations

Beyond the general aspects of car loans, there are specific regulations and costs unique to Arkansas that you need to be aware of. These factors can influence your total cost of ownership and the overall process of acquiring a vehicle in the Natural State.

Sales Tax

When purchasing a vehicle in Arkansas, you will be subject to state sales tax. As of my last update, the statewide sales tax rate is 6.5%. Additionally, many local jurisdictions (cities and counties) impose their own sales taxes, which are added on top of the state rate. This means the actual sales tax percentage you pay can vary depending on where you purchase the vehicle within Arkansas. Always factor this into your budget, as it can add a significant amount to the purchase price.

Title and Registration Fees

After buying a car, you’ll need to title and register it with the Arkansas Department of Finance and Administration (DFA) Motor Vehicle Division. There are various fees associated with this process:

- Title Fee: A flat fee for transferring the vehicle title into your name.

- Registration Fee: An annual fee based on the vehicle’s weight and type.

- License Plate Fee: The cost for your license plates.

- Vehicle Property Tax: Arkansas also requires you to pay personal property taxes on your vehicle. This is usually paid to your county assessor and must be current before you can renew your registration.

You can find detailed information on these fees and requirements directly on the official Arkansas Department of Finance and Administration website: Arkansas DFA Motor Vehicle Division. (External Link)

Insurance Requirements

Arkansas law mandates that all registered vehicles must carry minimum liability insurance coverage. Before you can register your vehicle, you’ll need to provide proof of insurance.

The minimum coverage requirements are:

- $25,000 for bodily injury to one person

- $50,000 for bodily injury to two or more people

- $25,000 for property damage

If you’re financing your vehicle, your lender will almost certainly require you to carry comprehensive and collision insurance in addition to the state-mandated liability coverage. This protects their investment in case of damage or theft.

Lemon Laws (Brief Mention)

Arkansas has "lemon laws" designed to protect consumers who purchase new vehicles that turn out to have significant defects that impair their use, value, or safety. While this doesn’t directly relate to the loan itself, it’s an important consumer protection to be aware of when purchasing a new car, especially when taking on a long-term loan commitment.

Pro Tips for a Smooth Arkansas Car Loan Experience

To ensure your journey to securing an Arkansas car loan is as smooth and stress-free as possible, here are some invaluable pro tips from us. These insights, gathered from years of experience in the financing world, can help you navigate common hurdles and make informed decisions.

Read the Fine Print

This cannot be stressed enough. Before signing any document, thoroughly read and understand every clause of your loan agreement. Don’t rush. Pay close attention to:

- Interest rate and APR: Ensure they match what you were quoted.

- Loan term: Understand the total number of payments.

- Total cost of the loan: This includes the principal, interest, and fees.

- Prepayment penalties: Confirm whether you can pay off the loan early without extra charges.

- Late payment fees: Know the consequences of missed payments.

If something is unclear, ask for clarification. A reputable lender will be happy to explain everything.

Don’t Be Afraid to Negotiate

Everything is negotiable, from the price of the car to the interest rate on your loan. With your pre-approval in hand, you have a strong bargaining chip. Don’t feel pressured to accept the first offer.

Negotiate the car’s price separately from the financing terms. This prevents the dealer from shifting costs around to make one aspect seem better while increasing another.

Understand Your Total Cost

Focusing solely on the monthly payment can be misleading. A lower monthly payment often comes with a longer loan term, meaning you’ll pay significantly more in total interest over the life of the loan.

Always calculate the total cost of the car, including the purchase price, interest, fees, and taxes. This holistic view allows you to make a truly financially sound decision.

Consider GAP Insurance

Guaranteed Asset Protection (GAP) insurance is often recommended, especially if you’re making a small down payment or financing a rapidly depreciating vehicle. In the event your car is totaled or stolen, GAP insurance covers the difference between what your comprehensive insurance pays out (the car’s depreciated value) and the remaining balance on your loan.

This prevents you from being upside down on your loan – owing more than the car is worth – after an unfortunate incident.

Common Mistakes to Avoid When Getting an Arkansas Car Loan

While the path to securing Arkansas car loans can be straightforward with the right information, certain missteps are frequently made by borrowers. Being aware of these common mistakes can save you money, stress, and potential long-term financial headaches. Avoid these pitfalls to ensure a smooth and successful auto financing experience.

Not Getting Pre-Approved

One of the biggest mistakes is walking into a dealership without a pre-approval from an independent lender. Without it, you lack a benchmark. The dealership knows you’re reliant on their financing, which reduces your negotiating power on both the car’s price and the loan terms.

Pre-approval provides you with a clear maximum loan amount and interest rate, allowing you to focus on negotiating the best price for the vehicle.

Focusing Only on Monthly Payments

As discussed earlier, fixating solely on the monthly payment can lead you astray. Dealerships might try to extend the loan term to lower the monthly payment, making the car seem more affordable. However, a longer term often means paying significantly more interest over the life of the loan.

Always consider the total cost of the loan and aim for a balance between an affordable monthly payment and a reasonable loan term.

Ignoring the Total Cost

Beyond monthly payments, failing to calculate the overall cost of the loan (principal + interest + fees) is a critical error. A loan that seems attractive on a monthly basis might be costing you thousands more in the long run.

Take the time to do the math or use online calculators to see the full financial picture before committing.

Not Checking Your Credit Report

Many people skip this crucial step, only to be surprised by their loan offers or even outright rejections. Your credit report might contain errors that negatively impact your score. These errors can be disputed and corrected, potentially improving your eligibility and interest rates.

Regularly checking your credit report is a good financial habit, not just for car loans. For more details on this, our article Understanding Your Credit Score for Auto Loans can provide valuable insights. (Internal Link)

Impulse Buying

Buying a car on impulse, without adequate research and planning, is a recipe for buyer’s remorse and financial strain. This includes not researching different car models, their reliability, insurance costs, or not taking the time to shop for the best loan.

Give yourself time to make a well-informed decision. The right car and the right loan are worth the effort of careful planning.

Conclusion

Navigating the world of Arkansas car loans doesn’t have to be a bewildering experience. By understanding the types of loans available, knowing the factors that influence your approval and rates, and meticulously following the application process, you empower yourself to make intelligent financial decisions. Remember, knowledge is your most valuable asset in the car-buying journey.

From securing a competitive interest rate to understanding state-specific fees, being well-informed ensures you avoid common pitfalls and drive away with a vehicle that brings you joy, not financial stress. Take the time to prepare, compare, and negotiate, and you’ll set yourself up for success. We hope this comprehensive guide has provided you with the confidence and clarity needed to secure the best possible auto financing in Arkansas and embark on your next adventure on the open road. Happy driving!