Navigating Austin’s Auto Loan Landscape: Your Ultimate Guide to Securing the Best Car Loan Rates

Navigating Austin’s Auto Loan Landscape: Your Ultimate Guide to Securing the Best Car Loan Rates Carloan.Guidemechanic.com

Welcome to Austin, Texas – a vibrant, booming city known for its live music, innovative tech scene, and rapidly growing population. As more people flock to this dynamic metropolis, the need for reliable transportation becomes increasingly crucial. Whether you’re a long-time resident or a newcomer settling into the 512, finding the perfect car often goes hand-in-hand with securing the right financing.

Understanding car loan rates in Austin can feel like deciphering a complex code, especially with so many factors at play. From your credit score to the type of vehicle you choose, every detail impacts the interest rate you’ll ultimately pay. But don’t worry – as your expert guide, I’m here to demystify the process. This comprehensive article will equip you with the knowledge and strategies to confidently navigate Austin’s auto loan market, ensuring you drive away with not just a great car, but also an excellent deal on your financing.

Navigating Austin’s Auto Loan Landscape: Your Ultimate Guide to Securing the Best Car Loan Rates

Our ultimate goal is to empower you with the insights needed to make informed decisions, save money, and avoid common pitfalls. Let’s dive deep into everything you need to know about car loan rates in the heart of Texas.

The Unique Pulse of the Austin Car Market

Austin isn’t just another big city; it has a distinct economic rhythm that influences everything from housing to vehicle prices. The city’s explosive growth, fueled by a booming tech industry and a constant influx of new residents, creates a unique dynamic for car buyers and lenders alike. High demand often translates to competitive pricing for vehicles, and by extension, a highly competitive lending environment.

This rapid expansion means more dealerships, more lenders, and a wider array of options than ever before. However, it also means you need to be savvier as a consumer. Knowing the local landscape can give you a significant edge when it comes to securing favorable car loan rates right here in Austin.

Demystifying the Factors That Shape Your Car Loan Rates

Before we explore where to find the best rates in Austin, it’s essential to understand the core elements that lenders consider. These factors are universal but play out uniquely within Austin’s specific economic context.

1. Your Credit Score: The Cornerstone of Your Loan Rate

Based on my experience, your credit score is arguably the single most influential factor determining the interest rate you’ll be offered. Lenders use this three-digit number to assess your creditworthiness and the likelihood of you repaying your loan. A higher score signals less risk, leading to lower interest rates and more attractive loan terms.

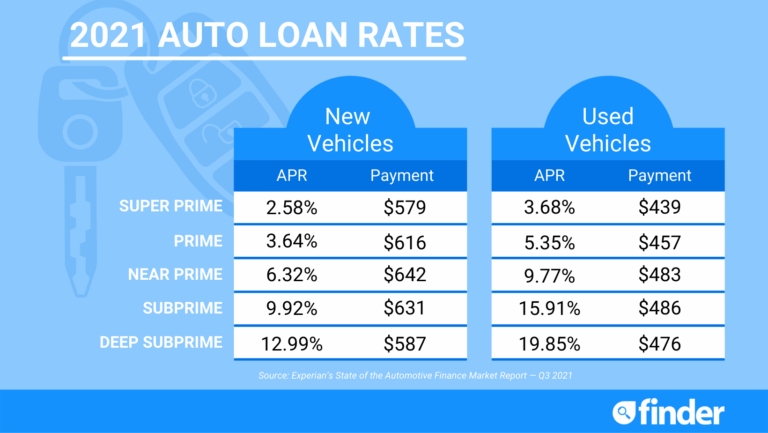

- Excellent Credit (780-850): Borrowers in this range typically qualify for the lowest advertised rates, often below 4-5% APR for new cars, depending on market conditions.

- Good Credit (670-779): Most consumers fall into this category. You’ll still get competitive rates, but they might be a percentage point or two higher than those with excellent credit.

- Fair Credit (580-669): Expect higher interest rates here, as lenders perceive a greater risk. Rates could range from 8% to 15% or more.

- Poor Credit (Below 580): Securing a loan can be challenging, and rates will be significantly higher, often 15% to 25% or even more. Subprime lenders specialize in this area, but their rates reflect the elevated risk.

Pro tip from us: Before you even start car shopping, get a free copy of your credit report from AnnualCreditReport.com and review it for accuracy. Correcting errors can significantly boost your score and save you thousands over the life of your loan. For a deeper dive into credit, consider reading our hypothetical article: .

2. The Loan Term: Short-Term Savings vs. Long-Term Payments

The loan term, or the length of time you have to repay the loan, directly impacts both your monthly payment and the total interest paid. Common terms range from 36 to 84 months.

While a longer loan term (e.g., 72 or 84 months) will result in lower monthly payments, it almost always means you’ll pay significantly more in total interest over the life of the loan. Conversely, a shorter term (e.g., 36 or 48 months) means higher monthly payments but substantially less interest paid overall. Lenders also often offer slightly lower interest rates for shorter terms because their risk is reduced.

3. Your Down Payment: A Powerful Negotiating Tool

Making a substantial down payment reduces the amount you need to borrow, which directly lowers your monthly payments. More importantly, it signals to lenders that you’re a serious borrower with skin in the game, often leading to better interest rates.

Common mistakes to avoid are opting for a "zero down" offer without fully understanding the implications. While appealing, it means you’re financing the entire vehicle cost, plus taxes and fees, immediately putting you in an upside-down position where you owe more than the car is worth due to rapid depreciation. Aim for at least 10-20% down if possible.

4. Vehicle Type: New vs. Used Car Considerations

Lenders often view new car loans as less risky than used car loans. New cars typically hold their value better in the initial years (though they still depreciate rapidly), and their maintenance costs are usually lower. This can translate to slightly lower interest rates for new vehicles.

Used cars, while generally more affordable upfront, come with a higher perceived risk due to unknown maintenance history and faster depreciation in some cases. Consequently, used car loan rates might be a bit higher. However, older used cars or those with higher mileage can still offer excellent value if financed smartly.

5. Lender Type: Exploring Your Options in Austin

The type of institution you choose for your car loan can significantly impact your rate and overall experience. Austin offers a diverse lending landscape.

- Banks (Local & National): Traditional banks like Chase, Wells Fargo, and local Austin banks offer a wide range of auto loan products. They can be a good option if you have an existing relationship with them.

- Credit Unions: Based on my experience, credit unions in Austin, such as Austin Telco Federal Credit Union, Amplify Credit Union, or RBFCU (Randolph-Brooks Federal Credit Union), are often hidden gems. They are member-owned, meaning they frequently offer more competitive interest rates and personalized service compared to larger banks.

- Online Lenders: Companies like Capital One Auto Finance, LightStream, and others provide convenient online applications and competitive rates. They’re excellent for quick comparisons and pre-approvals.

- Dealership Financing: While convenient, especially if you’re approved on the spot, dealership financing might not always offer the absolute best rate. Dealerships often work with multiple lenders and can mark up interest rates to increase their profit. Always compare their offer with pre-approvals you’ve secured elsewhere.

6. Current Economic Conditions: A Broader Impact

Broader economic factors, such as the Federal Reserve’s interest rate decisions and inflation, indirectly influence car loan rates across the board. When the Fed raises rates, borrowing costs for banks increase, which then trickles down to consumers in the form of higher loan rates. Staying aware of these trends can help you decide if it’s a good time to buy.

Where to Secure the Most Favorable Car Loan Rates in Austin

Now that we understand the influencing factors, let’s pinpoint where Austin residents can find the most competitive financing.

Leverage Local Credit Unions

As mentioned, Austin’s credit unions are a fantastic resource. Their member-centric approach often translates to better rates and more flexible terms. They typically require you to be a member (which usually involves opening a small savings account or meeting specific residency/employment criteria), but the benefits often outweigh this minor step.

- Austin Telco Federal Credit Union: Known for competitive auto loan rates and a strong community presence.

- Amplify Credit Union: Another local favorite, often lauded for great customer service and attractive loan products.

- RBFCU (Randolph-Brooks Federal Credit Union): While headquartered outside Austin, RBFCU has a significant presence and offers highly competitive rates to its members, including many Austin residents.

Explore Reputable Online Lenders

Don’t overlook the power of online lenders. Their streamlined processes and lower overhead can sometimes lead to very competitive rates. Many offer pre-qualification without impacting your credit score, allowing you to compare offers from various lenders quickly and easily. This is an excellent way to get a baseline for what you should expect.

Don’t Discount Your Existing Bank Relationship

If you have a long-standing relationship with a bank in Austin, check their auto loan offerings. Sometimes, they’ll extend preferential rates to loyal customers. It’s always worth a call or an online inquiry.

The Power of Pre-Approval: Your Secret Weapon

Pro tips from us: The single most effective strategy for securing the best car loan rates in Austin is to get pre-approved before you step foot in a dealership.

What is Pre-Approval?

Pre-approval means a lender has reviewed your financial information, determined your creditworthiness, and provisionally agreed to lend you a certain amount at a specific interest rate for your car purchase. This usually involves a "hard inquiry" on your credit report, which will have a minor, temporary impact on your score. However, multiple hard inquiries for the same type of loan within a short window (typically 14-45 days) are often treated as a single inquiry by credit bureaus, so shop around!

Benefits of Pre-Approval

- Negotiating Power: Walking into a dealership with a pre-approval letter in hand instantly transforms you into a cash buyer. You’re no longer dependent on their financing, which gives you immense leverage to negotiate the car’s price.

- Clear Budget: You know exactly how much you can afford, preventing you from falling in love with a car outside your budget.

- Focus on the Car: With financing sorted, you can focus solely on negotiating the best price for the vehicle itself, rather than juggling two complex negotiations simultaneously.

- Comparison Shopping: It provides a benchmark. If the dealership offers you a better rate, great! If not, you have a solid backup.

Navigating the Dealership: Smart Negotiation Tactics

Even with pre-approval, the dealership will likely try to offer their own financing. Here’s how to handle it.

Separate the Negotiations

Common mistakes to avoid are allowing the dealership to combine the car price and loan terms into one confusing negotiation. Always negotiate the car’s price first, as if you’re paying cash. Once you’ve agreed on a price, then you can discuss financing.

Understand the APR, Not Just the Interest Rate

Lenders will quote an Annual Percentage Rate (APR), which includes the interest rate plus any fees associated with the loan. Always compare APRs when looking at different loan offers to get the true cost of borrowing. A seemingly lower interest rate might hide higher fees, resulting in a higher APR.

Beware of Unnecessary Add-Ons

Dealerships often try to upsell you on extended warranties, paint protection, GAP insurance (if you already have a significant down payment), or other accessories. While some might be useful, these add-ons are often high-profit items for the dealership and can significantly increase your total loan amount and monthly payment. Scrutinize each one and only accept what you truly need and understand.

For more insights on navigating dealerships effectively, you might find our hypothetical article, , particularly useful.

Refinancing Your Austin Car Loan: Is It Right for You?

Perhaps you already have a car loan but are wondering if you could get a better rate. Refinancing your car loan in Austin is a viable option for many.

When Does Refinancing Make Sense?

- Improved Credit Score: If your credit score has significantly improved since you first took out the loan, you might qualify for a much lower interest rate.

- Lower Market Rates: Interest rates may have dropped since your original purchase.

- High Original Rate: If you had fair or poor credit when you first bought the car, a high initial interest rate means there’s more room to save.

- Change in Financial Situation: You might want to lower your monthly payments by extending the loan term (though this increases total interest paid) or reduce total interest by shortening the term.

The Refinancing Process

The process is similar to getting a new loan: research lenders, compare offers, and apply. Many of the same Austin-based credit unions and online lenders that offer initial car loans also provide refinancing options. Based on my experience, even a small reduction in your APR can save you hundreds, if not thousands, of dollars over the remaining life of your loan.

Special Considerations for Austin Residents

Living in Austin comes with its unique quirks, and these can subtly influence your car buying and financing journey.

- Cost of Living: Austin’s cost of living is notoriously high. Factor this into your overall budget when determining how much car payment you can comfortably afford. Don’t let a low monthly payment lure you into a loan that strains your finances.

- Traffic and Commute: Austin traffic can be brutal. This might influence your choice of vehicle (fuel efficiency, comfort features) and, by extension, the car’s price and loan amount.

- Local Sales Tax: Remember that Texas sales tax (6.25% of the vehicle’s purchase price) will be added to your total cost, usually financed into the loan. Factor this into your budget calculations.

Pro Tips from an Expert Blogger for Austin Car Buyers

Securing the best car loan rate in Austin isn’t just about finding the lowest number; it’s about making a smart, informed financial decision.

- Build and Maintain Excellent Credit: This is your most powerful asset. Pay bills on time, keep credit utilization low, and regularly check your credit report.

- Save for a Substantial Down Payment: The more you put down, the less you borrow, and the better your rates will likely be.

- Research Thoroughly: Don’t just apply to one lender. Get multiple quotes from different types of lenders (banks, credit unions, online) to ensure you’re getting the best deal.

- Don’t Rush the Decision: Take your time. A car loan is a significant financial commitment. Patience can save you a lot of money.

- Read the Fine Print: Always understand every aspect of your loan agreement, including any prepayment penalties, late fees, and what happens in case of default. If something is unclear, ask!

- Utilize External Resources: For general financial guidance and consumer protection, resources like the Consumer Financial Protection Bureau (CFPB) offer valuable, unbiased information on auto loans. You can find excellent resources on their website at www.consumerfinance.gov.

Driving Forward with Confidence in Austin

Navigating the landscape of car loan rates in Austin might seem daunting at first, but with the right knowledge and a strategic approach, you can confidently secure financing that perfectly fits your budget and needs. Remember, the goal isn’t just to get a car, but to get a car on terms that empower your financial well-being.

By understanding the key factors influencing your rate, exploring all your lending options, leveraging the power of pre-approval, and negotiating smartly, you’re well on your way to a successful car buying experience in our incredible city. So, do your homework, stay informed, and get ready to cruise the streets of Austin with peace of mind. Your ideal car and the best loan rate are out there waiting for you!