Navigating Auto Financing: A Deep Dive into Citifinancial Car Loans and Modern Alternatives

Navigating Auto Financing: A Deep Dive into Citifinancial Car Loans and Modern Alternatives Carloan.Guidemechanic.com

Securing a car loan is a significant financial decision, often shaping your budget for years to come. For many, the journey to finding suitable auto financing can be complex, especially if their credit history isn’t pristine. You might have heard the name "Citifinancial Car Loans" in your search, a name historically associated with offering financial solutions to a broad spectrum of borrowers.

In this comprehensive guide, we’ll embark on an in-depth exploration of what "Citifinancial Car Loans" represented, their evolution in the financial landscape, and crucially, what modern alternatives exist today for individuals seeking flexible auto financing. Our goal is to equip you with the knowledge to make informed decisions, understand the nuances of auto loans, and ultimately, drive away with the best possible deal. Let’s get started.

Navigating Auto Financing: A Deep Dive into Citifinancial Car Loans and Modern Alternatives

The Legacy of Citifinancial: Understanding Its Role in Auto Lending

For a significant period, Citifinancial was a prominent player in the consumer finance market, known for providing a range of personal loans, including those often used for vehicle purchases. Their approach was distinct, often catering to individuals who might not qualify for traditional bank loans due to less-than-perfect credit scores. This made them a go-to option for many seeking accessible financing.

However, the financial landscape is constantly evolving. The entity known as Citifinancial underwent significant transformations, eventually rebranding its core personal lending business to OneMain Financial. This evolution means that while you might be searching for "Citifinancial Car Loans," the direct offering under that specific brand name for auto financing, as it once existed, is no longer available.

Based on my experience in the financial sector, understanding this historical context is crucial. When people search for "Citifinancial Car Loans" today, they are typically looking for lenders who share similar characteristics: those willing to work with varied credit profiles, offer quick approvals, and provide solutions when traditional avenues seem closed. Our discussion will therefore focus on the types of loans and lending approaches that Citifinancial historically embodied, and how these needs are met by current lenders.

Who Was Citifinancial For, and Who Do Similar Lenders Serve Today?

Historically, Citifinancial carved a niche by serving a demographic often overlooked by prime lenders. These were individuals with average, fair, or even poor credit scores, who still needed access to credit for significant purchases like vehicles. They understood that life happens, and a credit score doesn’t always tell the whole story of someone’s ability to repay.

Today, the spirit of this lending philosophy lives on through various subprime auto lenders, finance companies, and personal loan providers. These institutions understand that factors beyond a FICO score – such as stable employment, a reasonable debt-to-income ratio, and a down payment – can be strong indicators of a borrower’s reliability. They aim to provide opportunities for individuals to secure necessary transportation, often helping them rebuild their credit in the process.

Pro tips from us: If you find yourself in this category, don’t be discouraged. While your options might differ from someone with excellent credit, there are still reputable lenders willing to work with you. The key is to know what to look for and how to prepare.

Key Characteristics of "Citifinancial-Style" Auto Loans

When we talk about "Citifinancial-style" auto loans, we’re referring to financing options designed for borrowers who may not fit the strict criteria of prime lenders. These loans typically share several common characteristics that set them apart. Understanding these features is vital for anyone exploring such financing today.

Firstly, accessibility for varied credit profiles is a hallmark. These lenders are more flexible in their credit assessment, often looking beyond just the credit score to consider other aspects of your financial situation. They understand that a low credit score might be due to past challenges rather than current irresponsibility.

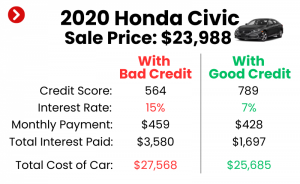

Secondly, interest rates are generally higher compared to prime loans. This is a direct reflection of the increased risk perceived by the lender when extending credit to individuals with less-than-perfect credit histories. The higher interest rate compensates the lender for this elevated risk. It’s crucial to factor this into your budget and understand the total cost of the loan over its lifetime.

Thirdly, these loans often feature flexible or extended loan terms. While longer terms can lead to lower monthly payments, making the car more affordable in the short term, they also mean you’ll pay more in interest over the life of the loan. It’s a trade-off that borrowers must carefully consider.

Finally, these loans frequently focus on collateral-based lending. Since auto loans are typically secured loans, the vehicle itself serves as collateral. This means if you default on the loan, the lender has the right to repossess the car to recoup their losses. This provides a level of security for the lender, which can make them more willing to approve loans for higher-risk borrowers.

The Application Process: What to Expect and How to Prepare

Applying for an auto loan, especially one from a non-traditional lender, requires thorough preparation. While the specific steps might vary slightly between institutions, the core elements remain consistent. Knowing what to expect can significantly streamline your journey to approval.

The process often begins with a pre-qualification step. This usually involves a soft credit check, which doesn’t impact your credit score, and provides you with an estimate of what you might be approved for. It’s a great way to gauge your options without commitment. Based on my experience, leveraging pre-qualification is a smart first step, as it helps set realistic expectations for your budget.

Following pre-qualification, you’ll move to the full application. This requires a more comprehensive submission of personal and financial information. Expect to provide details about your employment history, income, existing debts, and housing situation. Lenders use this information to assess your overall financial stability and your ability to comfortably repay the loan.

You’ll also need to gather required documents. Common documents include proof of income (pay stubs, tax returns), proof of residence (utility bills), identification (driver’s license), and sometimes bank statements. Having these ready beforehand can expedite the process significantly.

Finally, the lender will conduct a hard credit inquiry. This involves a detailed look at your credit report and score, and it will temporarily affect your credit score. This is a standard part of the lending process for full applications.

Pro tips from us: Before you even apply, pull your own credit report. Review it for inaccuracies and dispute any errors. Knowing your credit standing empowers you to address potential issues and negotiate more effectively. Common mistakes to avoid are applying to too many lenders at once (which can negatively impact your score with multiple hard inquiries) and not having all your documentation organized.

Understanding Interest Rates and Loan Terms

Interest rates and loan terms are the twin pillars determining the true cost of your auto loan. Grasping how they work and how they interact is fundamental to making a financially sound decision.

The interest rate is the cost of borrowing money, expressed as a percentage of the loan amount. Several factors influence the rate you’re offered. Your credit score is paramount; a higher score generally translates to a lower rate. Other considerations include your debt-to-income (DTI) ratio, the loan amount, and the chosen loan term. A lower DTI indicates you have more disposable income to put towards debt repayment, making you a less risky borrower.

It’s important to differentiate between the interest rate and the Annual Percentage Rate (APR). The APR includes not only the interest rate but also any additional fees associated with the loan, such as origination fees. This provides a more accurate representation of the total annual cost of borrowing. Always compare APRs when evaluating loan offers for an apples-to-apples comparison.

Loan terms refer to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, or 72 months). Shorter terms generally mean higher monthly payments but less interest paid overall. Conversely, longer terms result in lower monthly payments, which can make a car more affordable on a monthly basis, but you’ll end up paying significantly more in total interest over the life of the loan.

Pro tips from us: Don’t just focus on the lowest monthly payment. Calculate the total amount you’ll pay over the entire loan term, including all interest. Sometimes, a slightly higher monthly payment for a shorter term can save you thousands in the long run. Negotiating the interest rate is often possible, especially if you have multiple offers. Common mistakes to avoid include accepting the first offer without shopping around and extending the loan term purely to reduce monthly payments without considering the increased overall cost.

Pros and Cons of Opting for Non-Traditional Car Loans

Choosing a non-traditional auto loan, similar to what Citifinancial historically offered, comes with its own set of advantages and disadvantages. Weighing these carefully is crucial for making the right financial decision for your circumstances.

One of the most significant pros is accessibility for those with bad or limited credit. These lenders are often the only viable option for individuals who have faced financial setbacks or are just starting to build their credit history. They provide a crucial pathway to vehicle ownership, which can be essential for work, family, and daily life.

Another advantage is often quicker approval times. Non-traditional lenders sometimes have more streamlined processes, allowing for faster decisions and disbursement of funds. This can be a major benefit if you need a car quickly. Furthermore, successfully managing and repaying these loans can be an excellent way to rebuild your credit score, opening doors to better financial products in the future.

However, there are notable cons to consider. The most prominent is the higher cost. As discussed, these loans typically come with higher interest rates, which means you’ll pay more over the life of the loan compared to prime options. There’s also a potential for less favorable terms, such as longer repayment periods that increase total interest, or stricter clauses in the loan agreement.

Finally, there’s the collateral risk. Since the car secures the loan, failure to make payments can result in repossession, leading to loss of the vehicle and further damage to your credit. Common mistakes to avoid are failing to read the fine print of the loan agreement, not understanding all fees and charges, and overextending yourself financially with payments you can barely afford. Always ensure your monthly payment is comfortably within your budget, even with unexpected expenses.

Exploring Alternatives to "Citifinancial-Style" Car Loans

While "Citifinancial-style" loans serve a vital purpose, it’s always wise to explore all available alternatives before committing. The market offers a diverse range of options, each with its own advantages, particularly for those looking to secure better terms.

Credit Unions are often an excellent starting point. As member-owned non-profit organizations, they typically offer more competitive interest rates and more flexible terms than traditional banks, especially for members with good relationships. They also tend to be more understanding and willing to work with individuals facing credit challenges.

Dealership Financing is another common route. Many dealerships work with a network of lenders, including both prime and subprime institutions. While convenient, it’s essential to shop around and not just accept the first offer. Some dealerships might mark up interest rates, so comparing their offer with pre-approvals from other lenders is crucial.

Online Lenders have become increasingly popular. Companies like Capital One Auto Finance, LightStream, and others offer pre-qualification and application processes entirely online, often providing competitive rates and a wide range of loan products. They can be a great way to compare offers quickly from the comfort of your home.

For those with excellent credit, traditional banks like Chase, Bank of America, or Wells Fargo offer some of the lowest interest rates. Even if your credit isn’t perfect, it’s worth checking with your existing bank, as they might offer better terms to their established customers.

Finally, consider secured personal loans or even saving up. If you have an asset to use as collateral, a secured personal loan might offer better terms than an unsecured auto loan. And while not always feasible, saving for a significant down payment, or even buying a less expensive used car outright, can significantly reduce your borrowing needs and costs. For more on optimizing your loan options, you might find our guide on Understanding Auto Loan Refinancing helpful.

Tips for Securing the Best Possible Auto Loan

Navigating the auto loan market can feel daunting, but armed with the right strategies, you can significantly improve your chances of securing favorable terms. Here are some actionable tips:

First and foremost, improve your credit score. Even small improvements can lead to better interest rates. Pay bills on time, reduce existing debt, and avoid opening new credit accounts just before applying for a car loan. These actions demonstrate financial responsibility to lenders.

Secondly, save for a down payment. A substantial down payment reduces the amount you need to borrow, which lowers your monthly payments and the total interest paid. It also signals to lenders that you’re a lower risk, potentially leading to better loan terms. Aim for at least 10-20% of the car’s value.

Thirdly, shop around for quotes. Don’t settle for the first offer you receive. Contact multiple lenders—banks, credit unions, and online lenders—and compare their APRs, not just monthly payments. This competitive shopping can save you hundreds, if not thousands, over the life of the loan.

Get pre-approved before you even step foot in a dealership. A pre-approval gives you a clear understanding of how much you can afford and at what interest rate. This financial clarity transforms you into a cash buyer at the dealership, giving you significant leverage in negotiating the car’s price without the pressure of simultaneously arranging financing.

Finally, understand your budget. Beyond the car payment, factor in insurance, fuel, maintenance, and registration fees. A common mistake is focusing solely on the monthly car payment and neglecting these other significant ownership costs. A good rule of thumb is that your total vehicle expenses should not exceed 10-15% of your take-home pay. For further reading on managing your finances and credit, Investopedia offers excellent resources on Understanding Your Credit Score.

Refinancing Your Auto Loan: A Path to Better Terms?

Even after you’ve secured an auto loan, your financial journey doesn’t have to be static. Refinancing your auto loan can be a powerful strategy to improve your financial situation, especially if circumstances have changed since you first financed your vehicle.

You should consider refinancing if your credit score has significantly improved since you took out the original loan. A better credit score often qualifies you for lower interest rates. Another key reason is if market interest rates have dropped. If current rates are lower than what you’re paying, refinancing could save you money.

The benefits of refinancing can be substantial. The primary advantage is a lower interest rate, which directly translates to less money paid over the loan’s term. This can also lead to lower monthly payments, freeing up cash flow in your budget. Alternatively, you might choose to keep your monthly payment similar but opt for a shorter loan term, paying off the car faster and reducing total interest.

The process of refinancing is similar to applying for a new loan. You’ll shop around for new lenders, submit an application, and provide documentation. If approved, the new lender pays off your old loan, and you begin making payments to the new lender under the new terms. It’s a straightforward process that can yield significant financial relief. For a deeper dive into this topic, our article, Optimizing Your Auto Loan: A Guide to Refinancing, offers comprehensive insights.

The Impact of Your Car Loan on Your Financial Future

A car loan is more than just a means to acquire a vehicle; it’s a significant financial commitment that can profoundly impact your long-term financial health. Understanding these implications is crucial for responsible borrowing.

Firstly, your car loan directly influences your credit score. Making timely payments consistently will positively build your credit history, demonstrating reliability to future lenders. Conversely, missed or late payments can severely damage your score, making it harder and more expensive to obtain credit in the future. This is why maintaining payment discipline is paramount.

Secondly, it affects your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. Lenders use DTI to assess your ability to manage additional debt. A high DTI, potentially exacerbated by a large car loan, can hinder your ability to qualify for other loans, such as mortgages, or even reduce the amount you can borrow.

Finally, managing a car loan helps in building financial discipline. Successfully handling this responsibility teaches you budgeting, consistency, and the importance of meeting financial obligations. This experience is invaluable for developing a robust financial foundation and preparing for even larger financial commitments down the line. It’s a stepping stone to greater financial stability and confidence.

Conclusion: Driving Towards Smart Auto Financing Decisions

The journey to securing auto financing, particularly for those exploring options akin to what "Citifinancial Car Loans" once offered, requires careful consideration and an informed approach. While the Citifinancial brand has evolved, the need for accessible, flexible auto loans persists. Today, a variety of lenders, from credit unions to online platforms, stand ready to assist borrowers with diverse credit profiles.

Our deep dive has highlighted the importance of understanding loan characteristics, preparing for the application process, and meticulously comparing interest rates and terms. We’ve emphasized the critical role of a strong credit score, the benefits of a down payment, and the power of shopping around. Remember, your auto loan isn’t just about getting a car; it’s about building a foundation for your financial future.

By applying the pro tips and avoiding common mistakes discussed, you can navigate the complexities of auto financing with confidence. Make informed decisions, prioritize your financial well-being, and drive away not just with a new vehicle, but with a loan that truly works for you. Your path to responsible and rewarding car ownership begins with knowledge and careful planning.