Navigating Auto Loan Rates CT Used Car: Your Ultimate Guide to Smart Financing in Connecticut

Navigating Auto Loan Rates CT Used Car: Your Ultimate Guide to Smart Financing in Connecticut Carloan.Guidemechanic.com

Embarking on the journey to purchase a used car in Connecticut can be an exciting prospect, offering a blend of value, variety, and often, a more budget-friendly entry into vehicle ownership. However, the path to driving away in your chosen pre-owned vehicle often involves navigating the complex world of auto financing. Understanding Auto Loan Rates CT Used Car is not just about finding a monthly payment you can manage; it’s about making an informed financial decision that saves you money in the long run and secures your financial well-being.

This comprehensive guide is designed to be your indispensable resource, delving deep into everything you need to know about securing the best possible used car loan rates in the Nutmeg State. We’ll demystify the factors influencing your rates, explore your lending options, walk you through the application process, and share expert tips to ensure you drive away with confidence, not just a new-to-you car.

Navigating Auto Loan Rates CT Used Car: Your Ultimate Guide to Smart Financing in Connecticut

The Allure of the Used Car Market in Connecticut

The demand for used cars continues to grow, and for good reason. Opting for a pre-owned vehicle often means a lower purchase price, less depreciation over time, and potentially lower insurance costs compared to a brand-new model. In Connecticut, the vibrant used car market offers a vast array of choices, from reliable daily drivers to luxury pre-owned vehicles.

However, the perceived affordability of a used car can sometimes overshadow the critical importance of financing. For most buyers, securing an auto loan is a necessary step, and the terms of that loan—especially the interest rate—can significantly impact the total cost of your vehicle. Understanding how to find competitive CT auto financing for your used car is paramount.

Based on my experience, many first-time used car buyers in Connecticut focus heavily on the vehicle’s sticker price, sometimes overlooking the true cost implications of the loan itself. A seemingly small difference in interest rate can translate into hundreds, if not thousands, of dollars over the life of the loan. This article aims to empower you with the knowledge to avoid such pitfalls.

Key Factors Influencing Your Auto Loan Rates in CT

When lenders assess your application for a used car loan in Connecticut, they consider a multitude of factors to determine the level of risk involved. This risk assessment directly translates into the interest rate they offer you. A lower perceived risk typically results in a more favorable interest rate. Let’s explore these critical elements in detail.

Your Credit Score: The Cornerstone of Your Rate

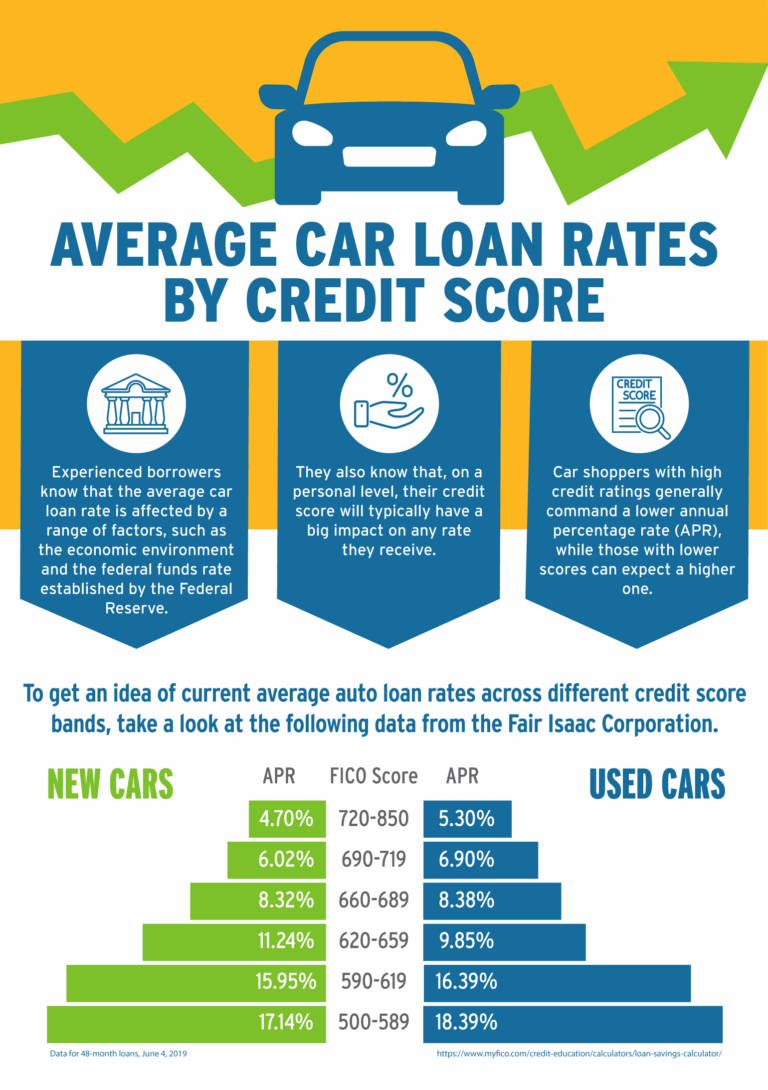

Without a doubt, your credit score is the single most influential factor in determining the Auto Loan Rates CT Used Car you’ll be offered. Lenders use this three-digit number to gauge your creditworthiness and your history of managing debt. A higher credit score signals a lower risk to lenders, making you eligible for more competitive rates.

FICO scores, the most commonly used credit scoring model, typically range from 300 to 850. Generally, scores above 700 are considered "good" or "excellent," while scores below 620 might place you in the "subprime" category, resulting in higher interest rates. Lenders often have specific tiers of rates based on these score ranges. For instance, someone with an excellent credit score (780+) might qualify for rates as low as 4-6%, while a borrower with a fair score (600-660) could see rates upwards of 10-15% or even higher for a used car.

Pro tip: Always check your credit report and score months before you plan to apply for a loan. This gives you time to identify and dispute any errors, or to take steps to improve your score, such as paying down existing debt or making timely payments. Improving your score even by a few points can sometimes move you into a better rate tier.

Loan Term: Balancing Monthly Payments and Total Cost

The loan term, or the length of time you have to repay the loan, also plays a significant role in your interest rate. Generally, shorter loan terms (e.g., 36 or 48 months) tend to come with lower interest rates because the lender’s risk exposure is reduced. However, shorter terms also mean higher monthly payments.

Conversely, longer loan terms (e.g., 60 or 72 months) typically have higher interest rates, as the lender is taking on more risk over an extended period. While a longer term can make monthly payments more affordable, you’ll end up paying significantly more in total interest over the life of the loan. For example, a $20,000 loan at 6% for 36 months might cost you $1,900 in interest, but the same loan at 7.5% for 72 months could cost over $5,000 in interest. It’s crucial to balance the affordability of your monthly payment with the total cost of the loan.

Down Payment: Reducing Risk, Reducing Rates

Making a substantial down payment on your used car is one of the smartest financial moves you can make. A larger down payment immediately reduces the amount of money you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay. From a lender’s perspective, a significant down payment also reduces their risk.

When you put more money down, you have more equity in the vehicle from day one, making you less likely to default on the loan. This reduced risk often translates into a lower interest rate offer. Aim for at least 10-20% of the vehicle’s purchase price as a down payment, if possible. This not only secures better used car loan rates CT but also helps prevent you from being "upside down" on your loan, where you owe more than the car is worth.

Vehicle Age and Mileage: Collateral Value

The characteristics of the used car itself—specifically its age and mileage—can impact the interest rate. Lenders view the vehicle as collateral for the loan. Older cars with higher mileage are generally perceived as having a higher risk of mechanical failure and faster depreciation. This higher risk can lead to higher interest rates, as the lender needs to offset the potential for the collateral to lose value quickly.

Newer used cars, perhaps those only a few years old with lower mileage, often qualify for better rates because they are seen as more reliable and hold their value better. Some lenders may even have restrictions on financing very old or high-mileage vehicles, or they might offer only very high rates for such cars. When looking for pre-owned vehicle financing Connecticut, remember that the vehicle’s condition and age are key considerations for lenders.

Debt-to-Income Ratio (DTI): Your Financial Capacity

Your debt-to-income (DTI) ratio is another crucial metric lenders use to assess your ability to take on new debt. It’s calculated by dividing your total monthly debt payments by your gross monthly income. A low DTI ratio indicates that you have plenty of income left after covering your existing debts, making you a more attractive borrower.

Lenders typically prefer a DTI ratio below 36%, though some may accept up to 43% depending on other factors. A high DTI suggests that you might be stretched thin financially, increasing the risk of default. This can lead to a denial of your loan application or, at best, a higher interest rate on your Auto Loan Rates CT Used Car. Managing your existing debt and ensuring a healthy DTI is vital before applying for a new loan.

Current Market Interest Rates: The Broader Economic Picture

Beyond your personal financial situation and the specific vehicle, the general economic climate and prevailing market interest rates play a significant role. The Federal Reserve’s monetary policy, for instance, influences the prime rate, which in turn affects the rates offered by banks and other lenders. When the Fed raises interest rates, auto loan rates tend to follow suit.

While you can’t control the broader economy, being aware of the current interest rate environment can help you set realistic expectations. If rates are generally high, securing a historically low rate might be challenging, regardless of your credit score. Staying informed about economic trends can help you decide if it’s a good time to buy or if waiting might yield better rates. You can often find current market trends and analysis on reputable financial news sites like The Wall Street Journal or Bloomberg.

Where to Find Auto Loan Rates CT Used Car

Once you understand the factors influencing your rates, the next step is to explore where you can actually secure your loan. In Connecticut, you have several options, each with its own advantages and disadvantages. Shopping around is crucial to finding the best used car rates CT.

Dealership Financing: Convenience at a Cost?

Many car dealerships offer on-site financing, acting as an intermediary between you and a network of lenders (banks, credit unions, and their own captive finance companies). This "one-stop shop" approach is incredibly convenient, allowing you to complete the car purchase and financing in one visit. Dealerships often advertise special financing rates or incentives, especially for certain models or during promotional periods.

However, common mistake: Accepting the first offer without shopping around is a significant error. While convenient, dealership financing might not always offer the most competitive rates. Dealerships often add a markup to the interest rate they receive from the lender, which is how they profit from the financing. It’s essential to compare their offer with pre-approvals you’ve secured elsewhere. Don’t be afraid to negotiate the interest rate with the dealership, as they often have some flexibility.

Banks & Credit Unions: Traditional Lenders with Competitive Offers

Traditional banks and local credit unions are excellent sources for used car loans in Connecticut. They often offer very competitive rates, especially if you have an existing relationship with them. Credit unions, in particular, are known for their member-focused approach and can sometimes provide lower rates and more flexible terms than larger banks, as they are not-for-profit institutions.

The process typically involves applying directly with the bank or credit union. If approved, they will provide you with a pre-approval letter, which states the maximum loan amount, interest rate, and terms you qualify for. This pre-approval gives you significant leverage when negotiating at the dealership, as you walk in knowing exactly how much you can spend and at what rate.

Online Lenders: Speed, Variety, and Comparison

The rise of online lenders has revolutionized auto financing, offering unparalleled convenience and the ability to compare multiple offers quickly. Websites like LightStream, Capital One Auto Finance, and others allow you to apply for pre-approval from the comfort of your home, often receiving decisions within minutes.

Online lenders typically have lower overhead costs, which can translate into competitive interest rates. They also make it easy to see various loan options side-by-side, helping you find the best terms for your Auto Loan Rates CT Used Car. For a deeper dive into comparing online lenders, check out our article on . This modern approach to lending empowers consumers with transparency and choice.

Private Party Loans: A Niche Option

If you’re purchasing a used car from a private seller (not a dealership), securing a loan can be a bit more challenging. Some banks and credit unions do offer "private party" auto loans, but they might have stricter requirements or higher interest rates due to the increased risk. The lack of dealer warranties or inspections can make lenders more hesitant.

For private party sales, you might need a larger down payment, and the lender will likely require a thorough inspection of the vehicle and a clear title. While private sales can sometimes offer a better deal on the car itself, the financing aspect requires more diligence and research to find a suitable lender.

The Application Process: Your Step-by-Step Guide for CT Used Car Loans

Securing a used car loan in Connecticut doesn’t have to be daunting. By following a structured approach, you can streamline the process and increase your chances of getting the best possible CT auto financing.

Step 1: Get Pre-Approved

This is perhaps the most crucial step. Getting pre-approved for a loan before you even step foot on a dealership lot provides immense benefits. It gives you a clear understanding of your budget, the maximum amount you can borrow, and the interest rate you qualify for. This knowledge empowers you to negotiate the car’s price more effectively, as you can focus on the vehicle’s cost rather than being swayed by monthly payment figures dictated by the dealer’s financing.

Most banks, credit unions, and online lenders offer a pre-approval process that involves a "soft" credit inquiry, which doesn’t negatively impact your credit score. Once pre-approved, you’ll receive a conditional offer, typically valid for 30-60 days.

Step 2: Gather Your Documents

Once you’re ready to apply for the actual loan, you’ll need to have several documents prepared. While specific requirements can vary slightly by lender, you’ll generally need:

- Proof of Identity: Driver’s license or state ID.

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2 forms, or tax returns (for self-employed individuals).

- Vehicle Information: Once you’ve chosen a car, you’ll need its VIN, make, model, year, and mileage.

- Insurance Information: Proof of auto insurance is required before you can drive the car off the lot.

Having these documents ready will significantly speed up the application process and help you secure used car loan rates CT without unnecessary delays.

Step 3: Compare Loan Offers Thoroughly

Do not settle for the first loan offer you receive. Apply with multiple lenders—banks, credit unions, and online providers—to compare their rates and terms. Lenders typically allow for a "rate shopping" period (usually 14-45 days) where multiple hard credit inquiries for the same type of loan are counted as a single inquiry, minimizing the impact on your credit score.

When comparing offers, focus on the Annual Percentage Rate (APR), not just the monthly payment. The APR reflects the true cost of borrowing, including interest and any fees. A lower APR means less money paid over the life of the loan. Also, examine the loan term, any prepayment penalties, and late payment fees.

Step 4: Negotiate with Confidence

With a pre-approval in hand, you are in a much stronger negotiating position. If a dealership offers you financing, compare their APR with your pre-approved rate. If the dealership’s offer is higher, you can use your pre-approval to ask them to match or beat it. If their offer is lower, you’ve found an even better deal! Remember, you’re negotiating two separate things: the price of the car and the terms of the loan. Keep them distinct for the best outcome.

Pro Tips for Securing the Best Auto Loan Rates CT Used Car

Securing an optimal used car loan in Connecticut requires strategic planning and smart execution. Here are some expert tips to help you get the most favorable terms.

- Boost Your Credit Score: As emphasized, your credit score is king. Pay bills on time, reduce credit card balances, and avoid opening new credit accounts in the months leading up to your loan application. Even a modest improvement can lead to significantly better Auto Loan Rates CT Used Car.

- Save for a Larger Down Payment: The more you can put down upfront, the less you’ll need to borrow, and the lower your risk profile will appear to lenders. This almost always translates to better interest rates.

- Shop Around Aggressively: Don’t limit yourself to one lender. Get pre-approvals from at least three to four different sources (banks, credit unions, online lenders) to ensure you’re getting the most competitive rate.

- Consider a Co-signer (If Necessary): If your credit score is less than ideal, a co-signer with excellent credit can help you qualify for a better interest rate. However, ensure both parties understand the responsibilities, as the co-signer is equally liable for the loan.

- Beware of Unnecessary Add-ons: Dealerships may try to upsell you on extended warranties, paint protection, or other add-ons that can significantly increase your loan amount and interest paid. Carefully evaluate if these are truly necessary or if you can purchase them separately at a better price.

- Know the Car’s Value: Research the market value of the specific used car you’re interested in using resources like Kelley Blue Book (KBB.com) or NADAguides. This knowledge will help you negotiate a fair purchase price, which in turn impacts your loan amount and total cost.

- Understand Your Budget Beyond the Payment: Consider not just the monthly car payment, but also insurance, maintenance, fuel, and registration costs in Connecticut. A lower interest rate helps keep your monthly loan payment down, contributing to overall affordability.

Refinancing Your CT Used Car Loan: When and Why

Even if you’ve already secured a used car loan in Connecticut, your journey for better rates doesn’t necessarily end. Refinancing your auto loan means taking out a new loan to pay off your existing one, ideally with more favorable terms.

When does refinancing make sense?

- Improved Credit Score: If your credit score has significantly improved since you first took out the loan, you might qualify for a much lower interest rate now.

- Lower Market Rates: If general interest rates have dropped since your original loan, you could save money by refinancing.

- Desire for a Lower Monthly Payment: Refinancing to a longer term (though this might increase total interest) can reduce your monthly payments, freeing up cash flow.

- Remove a Co-signer: If your credit has improved, you might be able to refinance the loan in your name only, releasing your co-signer from their obligation.

Refinancing can lead to substantial savings over the life of your loan, either by lowering your monthly payment or reducing the total amount of interest paid. If you’re considering refinancing, our guide on offers more detailed insights. It’s always worth exploring if you can get a better deal on your existing CT auto financing.

Common Mistakes to Avoid When Financing a Used Car in CT

Navigating the world of auto loans can be tricky, and several common missteps can lead to higher costs or less favorable terms. Being aware of these pitfalls can save you money and stress.

- Not Checking Your Credit Score: Many buyers go into the process blind, unaware of their credit standing. This puts them at a disadvantage when negotiating rates. Always check your score first.

- Only Focusing on the Monthly Payment: Dealerships often try to "sell" you on a monthly payment, not the total cost. A low monthly payment might hide a long loan term and a high interest rate, meaning you pay significantly more overall.

- Skipping Pre-Approval: As discussed, pre-approval is your superpower. Without it, you lack leverage and clear budget boundaries, making you susceptible to less favorable dealer financing.

- Not Shopping Around for Lenders: Assuming your primary bank or the dealership offers the best rate is a costly assumption. Always compare multiple offers.

- Ignoring the Total Cost of the Loan (APR): The APR is the most accurate reflection of the loan’s cost. Don’t let a seemingly low monthly payment distract you from a high APR.

- Buying a Car You Can’t Truly Afford: Beyond the loan payment, remember to factor in insurance, registration fees, maintenance, and fuel. Overextending yourself financially can lead to stress and potential default.

Connecticut Specific Considerations

While the core principles of auto financing apply nationwide, it’s always good to be mindful of state-specific regulations. In Connecticut, you’ll also need to factor in sales tax (currently 6.35% on motor vehicles), registration fees, and potential emissions testing requirements for used vehicles. These costs are separate from your loan but contribute to the overall expense of owning a car in CT. Be sure to budget for these additional expenses when calculating your total financial commitment.

Drive Smarter: Your Journey to Confident CT Used Car Financing

Securing the best Auto Loan Rates CT Used Car is a crucial step in smart vehicle ownership. By understanding the key factors that influence your rates, diligently exploring your lending options, and approaching the application process with an informed strategy, you empower yourself to make a financially sound decision. Remember, knowledge is power, and taking the time to research and compare can lead to significant savings over the life of your loan.

Don’t let the excitement of a new-to-you car overshadow the importance of shrewd financing. Arm yourself with information, shop around, and negotiate confidently. Your financial future, and your wallet, will thank you for it. Start your journey today and drive away with not just a great used car, but a great deal on your financing too!