Navigating Bad Credit Car Loans in Augusta, GA: Your Ultimate Guide to Driving Away with Confidence

Navigating Bad Credit Car Loans in Augusta, GA: Your Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

For many residents in Augusta, Georgia, owning a reliable vehicle isn’t just a convenience – it’s often a necessity. Whether it’s for commuting to work, taking children to school, or simply enjoying the beautiful Peach State, a car provides essential freedom and opportunity. However, the path to car ownership can feel daunting when you’re dealing with a less-than-perfect credit score. The good news? Bad credit car loans in Augusta, GA are a very real possibility, and with the right approach, you can secure the financing you need.

This comprehensive guide is designed to be your go-to resource, demystifying the process and empowering you to make informed decisions. We’ll dive deep into everything you need to know, from understanding your credit situation to finding the best lenders and driving away in your new car. Our goal is to provide real value, helping you navigate the unique landscape of auto financing in Augusta, GA, even with challenging credit.

Navigating Bad Credit Car Loans in Augusta, GA: Your Ultimate Guide to Driving Away with Confidence

Understanding Bad Credit and Its Impact on Car Loans

Before we explore solutions, it’s crucial to understand what "bad credit" means in the context of auto financing and why it presents a challenge. Your credit score is a three-digit number that lenders use to assess your financial reliability. It’s generated from your credit report, which details your borrowing and repayment history.

What Constitutes "Bad Credit"?

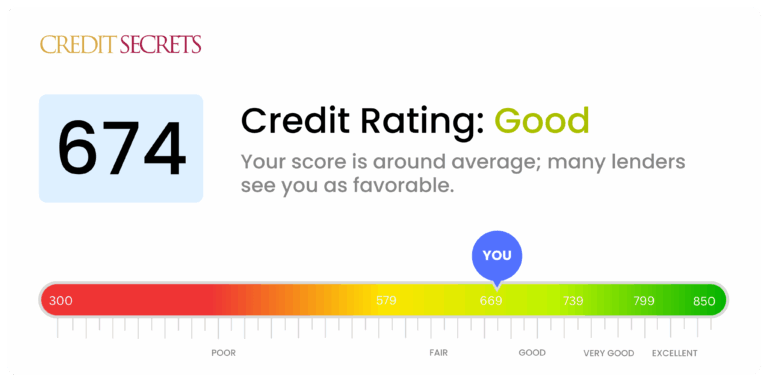

Generally, FICO scores range from 300 to 850. While definitions can vary slightly among lenders, credit scores typically fall into these categories:

- Excellent: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor/Bad: 300-579

If your score falls into the "Fair" or "Poor" categories, you’re likely considered a "subprime" borrower. This doesn’t mean you’re uncreditworthy, but it does signal a higher risk to lenders. Common factors leading to bad credit include missed payments, high credit card balances, collections, bankruptcies, or a limited credit history.

Why Bad Credit Makes Car Loans Challenging

Lending money always involves risk. When you have bad credit, lenders perceive a higher chance that you might default on your payments. To offset this increased risk, they typically:

- Charge Higher Interest Rates: This is the most common consequence. A higher interest rate means you’ll pay more over the life of the loan.

- Require Larger Down Payments: A substantial down payment reduces the loan amount and signals your commitment to the purchase.

- Offer Shorter Loan Terms: While a shorter term means higher monthly payments, it also reduces the overall interest paid and the lender’s risk exposure.

- Limit Vehicle Options: Some lenders might restrict the age or mileage of the vehicle you can finance to minimize their risk.

Based on my experience in the auto finance world, many individuals with bad credit feel discouraged before they even start. However, it’s important to remember that bad credit is a common situation, and there are many lenders specializing in helping people like you. The key is to be prepared and persistent.

The Challenges of Securing a Car Loan with Bad Credit in Augusta, GA

While it’s entirely possible to get a car loan with bad credit in Augusta, GA, it’s wise to be aware of the specific hurdles you might encounter. Understanding these challenges upfront can help you prepare and navigate the process more effectively.

Higher Costs Over the Long Run

As mentioned, a primary challenge is the higher interest rate. While a prime borrower might qualify for an interest rate in the low single digits, someone with bad credit might see rates anywhere from 10% to 20% or even higher, depending on the lender and their credit profile. This significantly increases the total cost of the vehicle over the loan term.

Let’s put this into perspective: A $20,000 loan over 60 months at 5% interest would cost you approximately $2,645 in interest. The same loan at 15% interest would cost you over $8,500 in interest. The difference is substantial.

Fewer Lender Options and Stricter Criteria

Mainstream banks and credit unions often have stringent credit score requirements, making it harder for subprime borrowers to qualify. This narrows your pool of potential lenders, meaning you might not have as many offers to compare.

Furthermore, the lenders who do specialize in bad credit car loans might have stricter requirements regarding income, employment history, and debt-to-income ratios. They want to ensure you have a stable financial situation that can support the new loan.

The Need for a Solid Down Payment

Common mistakes to avoid are underestimating the power of a down payment. While a down payment is always beneficial, it becomes almost essential when you have bad credit. Lenders view a significant down payment as a sign of your commitment and an immediate reduction in their risk.

A larger down payment can also lower your monthly payments, reduce the total interest you pay, and even potentially help you qualify for a slightly better interest rate. Aiming for at least 10-20% of the car’s purchase price is a strong strategy.

Navigating the Emotional Rollercoaster

The process can be emotionally taxing. You might face rejections, feel judged, or worry about being taken advantage of. It’s crucial to remain patient and informed. Remember, many people have successfully navigated this path, and you can too.

Pro tips from us: Stay calm and focused. Every "no" brings you closer to a "yes" if you learn from it and adjust your strategy. Don’t let initial rejections deter you from your goal of securing reliable transportation in Augusta, GA.

Your Strategy: Preparing for a Bad Credit Car Loan in Augusta, GA

Preparation is your most powerful tool when seeking Augusta GA auto loans bad credit. The more organized and informed you are, the better your chances of securing favorable terms.

1. Know Your Credit Score and Report

This is your starting point. You can get a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, TransUnion) once every 12 months at AnnualCreditReport.com. Many credit card companies also offer free credit score monitoring.

- Review for Accuracy: Dispute any errors you find. Even a small correction can positively impact your score.

- Understand the Factors: Identify what’s negatively affecting your score. Is it late payments? High credit utilization? This knowledge empowers you.

- What Lenders See: Knowing your score helps you anticipate what lenders will see and allows you to set realistic expectations.

2. Create a Realistic Budget

Before you even look at cars, determine what you can genuinely afford each month. Consider not just the car payment, but also insurance, fuel, maintenance, and potential repair costs.

- Income vs. Expenses: List all your monthly income and outgoings. Be honest with yourself.

- The 20/4/10 Rule: While not a strict rule for bad credit loans, it’s a good guideline: a 20% down payment, a loan term no longer than four years, and car expenses (payment + insurance) not exceeding 10% of your gross monthly income. Adjust this based on your specific situation.

- Emergency Fund: Ensure you have some savings for unexpected car repairs or other emergencies.

3. Save for a Significant Down Payment

We’ve emphasized this already, but it bears repeating. A substantial down payment is one of the best ways to improve your chances and reduce your overall loan cost.

- Show Commitment: It signals to lenders that you are serious and have some financial discipline.

- Lower Loan Amount: Less money borrowed means less interest accrues over time.

- Offset Risk: For lenders, a higher down payment directly reduces their exposure if you default.

4. Gather All Necessary Documents

Lenders will require documentation to verify your identity, income, and residence. Having these ready will streamline the application process. Typical documents include:

- Proof of Identity: Driver’s license or state ID.

- Proof of Residence: Utility bill, lease agreement.

- Proof of Income: Recent pay stubs (last 2-3 months), bank statements, tax returns (if self-employed).

- References: Sometimes required, non-family members are usually preferred.

- Proof of Insurance: You’ll need this before driving off the lot.

Pro tips from us: Organize these documents in a folder or digitally. It shows you are serious and prepared, which can leave a good impression on lenders in Augusta, GA.

Finding the Right Lender for Bad Credit Car Loans in Augusta, GA

Once you’re prepared, the next step is finding a lender willing to work with your credit situation. Augusta, GA, offers several avenues for bad credit auto loans. It’s crucial to explore each option to find the best fit for your needs.

1. Specialty Bad Credit Dealerships

Many dealerships in and around Augusta, GA, specialize in working with buyers who have challenged credit. These dealerships often have relationships with multiple subprime lenders or offer in-house financing.

- How They Work: They understand the nuances of bad credit and are often more flexible with their lending criteria.

- Pros: Higher approval rates, streamlined process, and they can sometimes help you find a vehicle that fits your budget.

- Cons: Interest rates might be higher than traditional lenders, and vehicle selection might be limited to what they can finance.

- E-E-A-T: Based on my experience, these dealerships can be a lifeline for many, but always scrutinize the loan terms carefully. Don’t rush into a decision.

2. Local Credit Unions

Credit unions are member-owned financial institutions known for their community focus and often more flexible lending practices compared to large banks.

- How They Work: They might be more willing to look beyond just your credit score and consider your overall financial picture, especially if you have an existing relationship with them.

- Pros: Potentially lower interest rates than specialty lenders, personalized service, and a focus on member well-being.

- Cons: You usually need to be a member to apply, and their approval criteria, while more flexible, can still be challenging for very low credit scores.

- Check out local credit unions in Augusta, such as SRP Federal Credit Union or Georgia’s Own Credit Union, to see their auto loan offerings.

3. Online Lenders Specializing in Bad Credit

The digital age has brought a wealth of online lenders who specialize in subprime auto loans. These platforms can offer convenience and a wide range of options.

- How They Work: You typically fill out a single online application, and they connect you with multiple lenders who are likely to approve you.

- Pros: Quick pre-approval processes, ability to compare multiple offers from the comfort of your home, and often a broader network of lenders.

- Cons: Less personalized service, and it’s essential to research the reputation of the online platform and its lending partners.

- Common mistakes to avoid are applying to too many online lenders at once, as each application can result in a hard inquiry on your credit report, which can temporarily lower your score.

4. "Buy Here, Pay Here" (BHPH) Dealerships

These dealerships offer in-house financing, meaning they are both the seller and the lender. They are often a last resort for those who can’t secure financing elsewhere.

- How They Work: They typically approve anyone with a stable income, as they prioritize your ability to make payments directly to them.

- Pros: Very high approval rates, regardless of credit history.

- Cons: Significantly higher interest rates, often shorter loan terms leading to higher monthly payments, and sometimes less desirable vehicle selection. They may also not report payments to credit bureaus, which means it won’t help rebuild your credit.

- Pro tips from us: If considering a BHPH option, thoroughly understand every aspect of the contract. The total cost can be very high, and some terms can be predatory. Ensure they report to credit bureaus if you want to rebuild your credit.

The Application Process: What to Expect When Seeking Augusta GA Auto Loans Bad Credit

Once you’ve identified potential lenders, it’s time to navigate the application process. Knowing what to expect can help you remain calm and confident.

The Initial Application and Pre-Approval

Most lenders will have an initial application, which can often be completed online or in person. This typically involves providing personal information, employment details, and income figures.

- Soft vs. Hard Inquiries: Many lenders offer a "pre-qualification" process that uses a soft credit inquiry, which doesn’t affect your credit score. Once you proceed to a full application, a hard inquiry will be made.

- Be Honest: Provide accurate information. Misrepresenting your financial situation can lead to rejection or even legal issues.

Understanding the Loan Offer

If approved, you’ll receive a loan offer outlining the terms. This is where your preparation pays off. Key elements to scrutinize include:

- Interest Rate (APR): This is the most crucial number, representing the true annual cost of borrowing. Compare this across different offers.

- Loan Term: How many months you have to repay the loan. Longer terms mean lower monthly payments but more interest paid overall.

- Monthly Payment: Ensure this fits comfortably within your budget.

- Total Amount Repayable: This includes the principal and all interest.

- Any Fees: Look for origination fees, processing fees, or prepayment penalties.

E-E-A-T: Based on my experience, many people get fixated on the monthly payment. While important, always consider the total cost of the loan. A lower monthly payment over a longer term often means paying significantly more in interest.

Negotiating Terms

Even with bad credit, there might be some room for negotiation, especially if you have multiple offers.

- Down Payment: A larger down payment can often lead to a lower interest rate.

- Trade-in: If you have a trade-in vehicle, ensure you get a fair value for it, as this also acts as a form of down payment.

- Be Prepared to Walk Away: If the terms aren’t favorable or don’t feel right, be ready to explore other options. Don’t feel pressured into a deal.

For more detailed steps on credit repair and how it can impact your ability to negotiate better loan terms, check out our comprehensive guide on .

Beyond the Loan: Rebuilding Your Credit in Augusta, GA

Securing a bad credit car loan is not just about getting a car; it’s also a powerful opportunity to rebuild your credit score. This can open doors to better financial opportunities in the future.

Making Timely Payments

This is the single most important action you can take. Your payment history accounts for 35% of your FICO score.

- Consistency is Key: Pay on time, every time. Set up automatic payments or calendar reminders to ensure you never miss a due date.

- Full Payments: Always pay the full amount due, not just the minimum.

- Positive Impact: Each on-time payment demonstrates financial responsibility and will gradually improve your credit score.

The Power of Refinancing

As your credit score improves over time (typically 6-12 months of on-time payments), you might become eligible to refinance your car loan at a lower interest rate.

- Lower Your Payments: A lower interest rate can significantly reduce your monthly payments.

- Save Money: You’ll pay less interest over the remaining life of the loan.

- Check Eligibility: Many lenders offer refinancing, and it’s worth exploring once your credit has shown improvement.

Maintaining Financial Health

Beyond your car loan, continue practicing good financial habits:

- Keep Credit Utilization Low: Aim to use less than 30% of your available credit on credit cards.

- Diversify Credit: A mix of credit types (e.g., installment loan like a car loan, revolving credit like a credit card) can be beneficial.

- Regularly Monitor Your Credit: Keep an eye on your credit report for any discrepancies or fraudulent activity.

Local Considerations for Augusta, GA Residents

Augusta, GA, has a vibrant community and a diverse range of dealerships and financial institutions. When seeking bad credit car loans in Augusta, GA, consider these local insights:

- Dealership Clusters: Areas like Washington Road or Gordon Highway often have multiple dealerships close together, making it easier to compare options without traveling far.

- Community Resources: Local financial literacy programs or non-profits in Augusta might offer free advice or workshops on budgeting and credit improvement.

- Driving Needs: Consider Augusta’s specific driving conditions. A reliable vehicle is essential, especially if you commute across the Savannah River or need to navigate the city’s various neighborhoods.

For general advice on consumer financial products, including auto loans, you can consult trusted external resources like the Consumer Financial Protection Bureau (CFPB) at ConsumerFinance.gov. They offer unbiased information and tools to help you make informed decisions.

Conclusion: Your Journey to Car Ownership in Augusta, GA

Securing bad credit car loans in Augusta, GA, is an achievable goal, not an insurmountable obstacle. While it requires diligent preparation, informed decision-making, and a bit of persistence, the reward of reliable transportation and the opportunity to rebuild your credit is well worth the effort.

By understanding your credit, preparing your finances, exploring the right lenders, and carefully reviewing loan terms, you can confidently navigate the process. Remember, this journey isn’t just about getting a car; it’s about taking control of your financial future and demonstrating your commitment to responsible borrowing. Don’t let past credit challenges hold you back. Start your journey today, and drive away with confidence on the streets of Augusta, GA!

Disclaimer: This article provides general information and is not financial advice. It is recommended to consult with a qualified financial advisor or credit professional for personalized guidance based on your specific situation. Loan approvals and terms are subject to lender discretion and individual credit profiles.