Navigating Bad Credit Car Loans in Dallas: Your Comprehensive Guide to Getting Back on the Road

Navigating Bad Credit Car Loans in Dallas: Your Comprehensive Guide to Getting Back on the Road Carloan.Guidemechanic.com

Finding yourself in need of a reliable vehicle in a sprawling city like Dallas, only to be met with the challenge of a less-than-perfect credit score, can feel incredibly daunting. The thought of applying for a car loan when your credit history has a few bumps might even seem impossible. But here’s the reassuring truth: bad credit car loans in Dallas are not only possible but are a common solution for many individuals.

This comprehensive guide is designed to empower you with the knowledge and strategies needed to secure a car loan, even with bad credit, right here in the heart of Texas. We understand the frustration and the urgent need for transportation in a city where public transit might not reach every corner of your daily life. From understanding your credit to finding the right lenders and making smart financial decisions, we’ll walk you through every step. Our goal is to demystify the process, provide actionable advice, and help you drive away in a car that fits your needs and your budget.

Navigating Bad Credit Car Loans in Dallas: Your Comprehensive Guide to Getting Back on the Road

Understanding Bad Credit and Its Impact on Car Loans

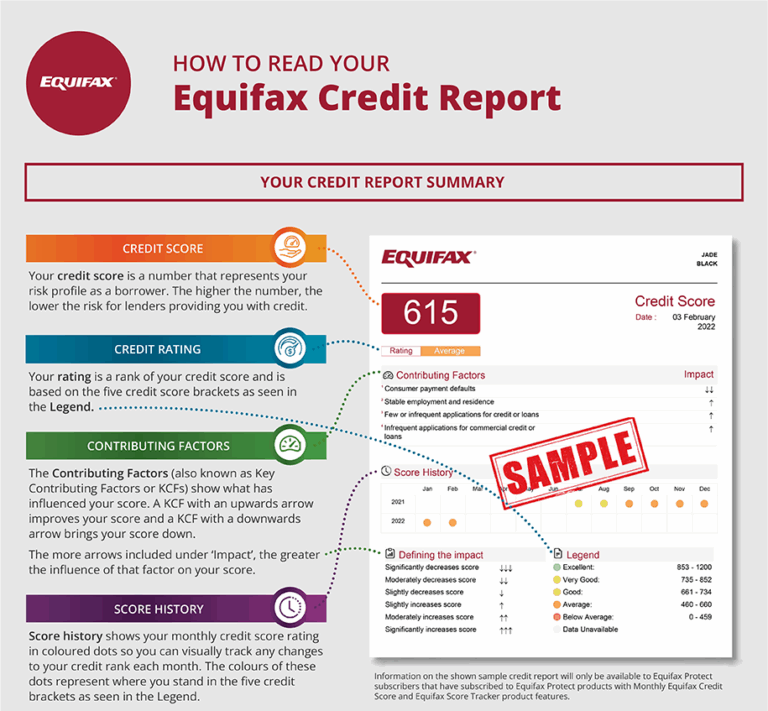

Before diving into solutions, it’s crucial to grasp what "bad credit" truly means in the eyes of a lender. Your credit score, typically a FICO or VantageScore, is a three-digit number that summarizes your creditworthiness. Scores generally range from 300 to 850. A score below 600-620 is often considered "subprime" or "bad credit."

This score is influenced by several factors: your payment history, amounts owed, length of credit history, new credit, and credit mix. When lenders see a low score, they perceive a higher risk. They worry about your ability to consistently make payments on time, which is why traditional lenders might hesitate to approve a loan.

In a dynamic market like Dallas, where the cost of living and the reliance on personal transportation are significant, a low credit score can feel like a major roadblock. Many believe it automatically disqualifies them from car ownership. However, this is a common misconception. While it presents challenges, it certainly doesn’t close all doors.

Is a Car Loan with Bad Credit in Dallas Even Possible? Absolutely!

The short answer is a resounding yes! Securing a car loan with bad credit in Dallas is entirely achievable. The key lies in understanding that the lending landscape has evolved, with many institutions specializing in what are known as "subprime auto loans." These loans are specifically designed for individuals with credit scores that fall below traditional lending thresholds.

For many Dallas residents, a car isn’t a luxury; it’s a necessity for commuting to work, taking children to school, and managing daily responsibilities across our expansive metroplex. Recognizing this vital need, a robust market of lenders, dealerships, and financial institutions has emerged, dedicated to providing options for those with less-than-perfect credit. Their business model is built around assessing risk differently and offering pathways to vehicle ownership for a broader spectrum of borrowers.

Proven Strategies for Securing a Bad Credit Car Loan in Dallas

Navigating the world of bad credit car loans requires a strategic approach. By taking proactive steps and understanding what lenders are looking for, you can significantly improve your chances of approval and secure more favorable terms.

1. Know Your Credit Score and Report Inside Out

Your credit report is your financial fingerprint, and it’s the first thing lenders will scrutinize. Before you even think about stepping onto a car lot, obtain a copy of your credit report from all three major bureaus: Experian, Equifax, and TransUnion. You are entitled to a free report from each once every 12 months via AnnualCreditReport.com.

Carefully review these reports for any inaccuracies or errors. Pro tip from us: Disputing and correcting errors can sometimes boost your score surprisingly quickly, even by a few points, which might make a difference in loan approval or interest rates. Understanding what factors are impacting your score also gives you insights into areas you might improve over time.

2. Craft a Realistic Budget and Stick to It

One of the most critical steps, especially with bad credit, is determining what you can truly afford. Don’t just think about the monthly car payment. Consider the total cost of car ownership: insurance, fuel, maintenance, registration, and potential repairs. A common mistake to avoid is stretching your budget too thin just to get a car.

Based on my experience, lenders want to see stability. They’ll look at your income, existing debts, and living expenses to calculate your debt-to-income ratio. A lower ratio indicates you have more disposable income to put towards a car payment. Create a detailed monthly budget that accounts for all your expenses and reveals a comfortable amount you can dedicate to a car loan without financial strain.

3. Save for a Substantial Down Payment

A down payment is your secret weapon when you have bad credit. Putting money down upfront significantly reduces the risk for lenders. It shows them you’re serious about the purchase and have some financial discipline. More importantly, it reduces the amount you need to borrow, which can lead to lower monthly payments and less interest paid over the life of the loan.

Aim for at least 10-20% of the vehicle’s purchase price, if possible. Even a smaller down payment is better than none. Based on my experience, a solid down payment can often be the deciding factor for approval, especially when other credit factors are less than ideal. It also instantly gives you equity in the vehicle.

4. Consider a Co-signer (with Caution)

If you have a trusted friend or family member with excellent credit who is willing to co-sign for your loan, this can significantly improve your chances of approval and potentially secure a lower interest rate. A co-signer essentially guarantees the loan, promising to make payments if you default.

While this can be a great solution, it comes with a major caveat. Your co-signer’s credit will also be impacted by the loan, and they are equally responsible for the debt. Common mistake to avoid: entering into a co-signing agreement without a clear understanding of the responsibilities and potential strain it could put on your relationship. Ensure both parties are fully aware of the commitment.

5. Explore Diverse Lender Types

Don’t limit yourself to just one type of lender. Dallas offers a variety of options for bad credit car loans:

- Dealership Financing: Many dealerships in Dallas have dedicated finance departments that work with a network of lenders, including those specializing in subprime loans. Some are "buy-here-pay-here" dealerships, which lend directly to you, often with less stringent credit requirements but potentially higher interest rates.

- Credit Unions: Often more community-focused, credit unions can sometimes be more flexible and understanding than traditional banks when it comes to borrowers with bad credit. Their interest rates can also be competitive.

- Online Lenders: A growing number of online platforms specialize in bad credit auto loans. They offer convenience and often have quick pre-approval processes. They can be a good starting point for comparing offers.

6. Get Pre-approved Before You Shop

Getting pre-approved for a loan is a powerful strategy. It means a lender has reviewed your financial situation and agreed to lend you a certain amount, up to a specific limit, at a particular interest rate. This offers several benefits:

- Clear Budget: You know exactly how much you can spend, preventing you from falling in love with a car outside your price range.

- Negotiating Power: You walk into the dealership with financing already secured, giving you leverage to negotiate the car’s price rather than being focused solely on the monthly payment.

- Credit Impact: Pre-approval usually involves a "soft inquiry" on your credit, which doesn’t harm your score. A "hard inquiry" only happens when you finalize the loan application.

7. Gather All Necessary Documentation

Being prepared can significantly speed up the loan application process. Lenders will typically require:

- Proof of identity (Driver’s License or State ID)

- Proof of residency (Utility bill, lease agreement)

- Proof of income (Recent pay stubs, bank statements, tax returns if self-employed)

- Proof of insurance (Once you’ve chosen a vehicle)

- References (Sometimes required, especially for buy-here-pay-here)

Having these documents organized and ready shows responsibility and efficiency, which can positively influence a lender’s perception.

Finding the Right Dealerships in Dallas for Bad Credit

Not all dealerships are created equal when it comes to bad credit car loans. In Dallas, look for dealerships that specifically advertise "bad credit auto financing," "second chance auto loans," or "guaranteed approval." These are often indicators that they have established relationships with subprime lenders or offer in-house financing.

Always read online reviews and check their reputation. Look for dealerships that are transparent about their financing options and prioritize customer education over high-pressure sales tactics. A reputable dealership will take the time to explain your loan terms, not just the monthly payment.

Understanding the Terms of Your Bad Credit Car Loan

When dealing with bad credit, it’s essential to understand that your loan terms might differ from those with excellent credit. This doesn’t mean you should accept any offer, but rather understand what to expect.

- Interest Rates: Expect a higher Annual Percentage Rate (APR) compared to prime loans. This is how lenders compensate for the increased risk. Focus on getting the lowest rate possible by applying the strategies above.

- Loan Term: The length of time you have to repay the loan. Longer terms mean lower monthly payments but more interest paid over the life of the loan. Shorter terms mean higher monthly payments but less total interest. Pro tips from us: Balance affordability with the total cost. Don’t extend the term unnecessarily just to lower the payment slightly.

- Fees: Be vigilant for any hidden fees, such as origination fees, documentation fees, or prepayment penalties. Always ask for a detailed breakdown of all costs.

Always focus on the total cost of the loan, not just the monthly payment. A lower monthly payment over a very long term can result in paying significantly more in interest.

Rebuilding Your Credit with a Bad Credit Car Loan

One of the most significant benefits of securing a bad credit car loan is the opportunity it presents to rebuild your credit history. Each on-time payment you make is reported to the credit bureaus. Consistent, timely payments will gradually improve your credit score.

As your credit score improves, you might even become eligible to refinance your car loan down the line. Refinancing allows you to secure a new loan with a lower interest rate, reducing your monthly payments and the total amount of interest you’ll pay. This is a common and highly effective strategy for those who start with bad credit. For more detailed insights, consider exploring our guide on How to Improve Your Credit Score After a Car Loan (Internal Link Placeholder).

Common Mistakes to Avoid When Seeking Bad Credit Car Loans in Dallas

Navigating this process can be tricky, and some common pitfalls can make it even harder. Avoid these mistakes to ensure a smoother experience:

- Not Checking Your Credit Report: As mentioned, ignorance is not bliss here. Errors can cost you.

- Applying Everywhere: Each "hard inquiry" for a loan can temporarily ding your credit score. Try to limit your applications to a few targeted lenders within a short timeframe (usually 14-45 days) so they count as a single inquiry for scoring purposes.

- Ignoring the Budget: Overextending yourself financially is a recipe for disaster, potentially leading to default and further credit damage.

- Settling for the First Offer: Always compare at least two or three loan offers to ensure you’re getting competitive terms.

- Not Reading the Fine Print: Every clause in your loan agreement matters. Understand interest rates, fees, penalties, and payment schedules.

- Getting Emotionally Attached to a Car: Keep a clear head. Focus on a reliable, affordable vehicle that meets your needs, not necessarily your dream car, especially initially.

Conclusion: Your Road to a Car Loan in Dallas is Clear

Obtaining bad credit car loans in Dallas might seem like an uphill battle, but with the right information and a strategic approach, it’s a perfectly achievable goal. Remember, a less-than-perfect credit score is a reflection of your financial past, not necessarily your financial future. This journey is not just about getting a car; it’s about taking a significant step towards rebuilding your credit and securing your financial independence.

By understanding your credit, budgeting wisely, saving for a down payment, exploring various lenders, and carefully reviewing loan terms, you can confidently navigate the Dallas auto loan market. Take the first step today: check your credit report, set a budget, and start exploring your options. You’ll be on the road in Dallas with a reliable vehicle and a stronger financial outlook sooner than you think. For more general financial guidance, consider visiting the Consumer Financial Protection Bureau’s website at consumerfinance.gov (External Link).