Navigating Bad Credit Car Loans in Maine: Your Ultimate Guide to Driving Away with Confidence

Navigating Bad Credit Car Loans in Maine: Your Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

The rugged beauty of Maine, with its sprawling coastlines, dense forests, and charming towns, often necessitates reliable transportation. Whether you’re commuting to work in Portland, exploring Acadia National Park, or simply running errands in Bangor, a dependable vehicle isn’t just a luxury; it’s often a vital link to daily life. However, for many Mainers, the challenge of securing a car loan can be daunting, especially when faced with a less-than-perfect credit history.

This is where the journey to understanding Bad Credit Car Loans Maine begins. If your credit score has taken a hit due to past financial hurdles, it can feel like a closed door. But let me assure you, it’s not. Based on my extensive experience in the auto financing world, there are viable pathways and dedicated lenders ready to help you get behind the wheel. This comprehensive guide will illuminate every step of the process, empowering you to make informed decisions and drive off with confidence.

Navigating Bad Credit Car Loans in Maine: Your Ultimate Guide to Driving Away with Confidence

Understanding Bad Credit and Its Impact on Your Car Loan Journey

Before diving into solutions, it’s crucial to grasp what "bad credit" truly means in the eyes of a lender. Your credit score, typically a FICO or VantageScore, is a three-digit number that summarizes your creditworthiness. Scores generally range from 300 to 850, with anything below 620 often categorized as "subprime" or "bad credit." This score is a snapshot of your financial past, including payment history, amounts owed, length of credit history, new credit, and credit mix.

When you apply for car loans Maine with a low credit score, lenders perceive a higher risk. This risk assessment directly influences the terms they offer. You might face higher interest rates, require a larger down payment, or have fewer options regarding vehicle choice. It’s important to understand that while a bad credit score presents challenges, it doesn’t automatically disqualify you from obtaining a loan. Many lenders specialize in poor credit auto loans and understand that life happens.

Why a Car is More Than Just a Convenience in Maine

In many parts of Maine, public transportation options are limited, making a personal vehicle indispensable. Winters can be harsh, and distances between towns can be significant. Relying on rideshares or asking for favors can quickly become unsustainable, impacting everything from your job stability to your ability to access healthcare and groceries.

Therefore, securing a car loan isn’t just about personal freedom; it’s about maintaining your livelihood and quality of life. For those seeking financing with bad credit in the Pine Tree State, the stakes are often higher, making a clear understanding of the lending landscape even more critical.

Preparing for Your Bad Credit Car Loan Journey: Laying the Groundwork

Success in securing a car loan with bad credit heavily relies on preparation. Approaching the process with knowledge and a clear strategy can significantly improve your chances of approval and help you secure more favorable terms.

1. Check Your Credit Score and Report

This is your starting point. You can obtain a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) annually through AnnualCreditReport.com. Review it meticulously for any errors or inaccuracies. Disputing errors can potentially boost your score, even if only by a few points, which can make a difference.

Understanding what’s on your report also helps you anticipate what lenders will see. It allows you to address any red flags proactively or explain past issues confidently.

2. Set a Realistic Budget

Before you even look at cars, determine what you can genuinely afford each month. This isn’t just about the car payment. Factor in insurance, fuel, maintenance, registration, and potential repair costs. A common mistake is to focus solely on the monthly payment without considering the total cost of ownership.

Pro tips from us: Aim for a car payment that, along with all other car-related expenses, doesn’t exceed 10-15% of your net monthly income. Being realistic here prevents future financial strain and potential loan default, which would further damage your credit.

3. Gather Essential Documents

Lenders specializing in bad credit auto loans will want to verify your identity, income, and residency. Having these documents ready can streamline the application process:

- Proof of Income: Recent pay stubs (usually 2-3 months), bank statements, or tax returns if self-employed.

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Proof of Identity: Driver’s license or state ID.

- Proof of Insurance: You’ll need this before driving off the lot.

- References: Sometimes required, especially for subprime loans.

Having these prepared demonstrates your seriousness and reliability, which can be a huge plus when your credit score isn’t doing all the talking.

4. Understand Your Rights as a Consumer

As you navigate the world of auto financing Maine, remember you have rights under consumer protection laws. The Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB) offer resources on fair lending practices. Don’t feel pressured into a loan you don’t understand or that feels exploitative. Always ask questions until you’re completely clear on all terms and conditions.

Finding the Right Lender for Bad Credit Car Loans in Maine

The type of lender you approach can significantly impact your success when seeking bad credit car loans Maine. Not all lenders are created equal, especially when it comes to accommodating less-than-perfect credit.

1. Specialized Subprime Lenders

These lenders specifically cater to individuals with low credit scores. They have different underwriting criteria than traditional banks, often focusing more on your current income stability and ability to repay rather than solely on your past credit history. Many online platforms specialize in connecting borrowers with subprime lenders across the country, including those serving Maine.

These lenders understand the nuances of financing with bad credit and often have more flexible terms, though interest rates will generally be higher to offset the perceived risk.

2. Dealership Financing (Including "Buy Here Pay Here")

Many Maine car dealerships bad credit friendly options exist, offering in-house financing. This can be convenient as you can apply for a loan and purchase a vehicle all in one place. Dealerships often work with a network of various lenders, including subprime ones, to find an option for you.

"Buy Here Pay Here" (BHPH) dealerships are another option. These dealerships lend you the money directly, rather than through a third-party bank. They are often a last resort for those with very poor credit or no credit history. While they offer high approval rates, common mistakes to avoid are not thoroughly understanding their terms, which often include higher interest rates and more frequent payment schedules (e.g., weekly or bi-weekly). Always compare their offers with other lenders.

3. Credit Unions

Credit unions are member-owned financial institutions known for their community focus. They often have more flexible lending standards and may be more willing to work with members who have bad credit, especially if you have a long-standing relationship with them. Their interest rates can sometimes be more competitive than those offered by subprime lenders or BHPH dealerships.

If you’re already a member of a credit union in Maine, it’s definitely worth checking their Maine auto loan options.

4. Traditional Banks

While traditional banks typically have stricter lending criteria, it doesn’t hurt to inquire, especially if you have a banking relationship with them. They might be more amenable if you have a significant down payment or a co-signer with good credit. However, for most individuals seeking bad credit car loans Maine, other options will likely yield more positive results.

The Application Process for Bad Credit Car Loans in Maine: What to Expect

Once you’ve identified potential lenders, the application process for secure car loan Maine with bad credit usually follows a similar pattern. Transparency and honesty are your best assets here.

- Pre-qualification (Optional but Recommended): Many lenders offer a pre-qualification process that involves a "soft" credit pull, which doesn’t affect your credit score. This gives you an idea of what loan amount and interest rate you might qualify for without commitment.

- Formal Application: You’ll fill out a detailed application providing personal, financial, and employment information. This will involve a "hard" credit inquiry, which might temporarily lower your score by a few points.

- Documentation Submission: As mentioned earlier, submit all required documents promptly and accurately.

- Lender Review: The lender will assess your application, looking beyond just your credit score. They’ll consider your debt-to-income ratio, employment history, stability of residence, and the amount of your down payment.

- Offer and Negotiation: If approved, you’ll receive a loan offer detailing the principal amount, interest rate, term length, and monthly payment. This is your opportunity to ask questions and, if possible, negotiate terms.

Based on my experience, lenders are looking for signs of stability and your ability to repay. A steady job history, a low debt-to-income ratio (even with bad credit), and a significant down payment can speak volumes about your reliability.

Strategies to Improve Your Chances of Approval

Even with bad credit, there are proactive steps you can take to strengthen your loan application for buying a car with bad credit.

1. Make a Substantial Down Payment

This is perhaps the single most impactful strategy. A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It also often translates to a lower monthly payment and less interest paid over the life of the loan.

Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price. This demonstrates your commitment and financial discipline, making you a more attractive borrower.

2. Consider a Co-signer

If you have a trusted friend or family member with good credit, asking them to co-sign your loan can significantly improve your chances of approval and potentially secure a lower interest rate. A co-signer agrees to be legally responsible for the loan if you default.

Common mistakes to avoid are not fully understanding the co-signer’s responsibility. This is a serious commitment for them, so ensure both parties are fully aware of the implications. It’s crucial to make timely payments to protect your co-signer’s credit.

3. Set Realistic Expectations for Your Vehicle

When you’re seeking bad credit car loans Maine, it’s wise to prioritize needs over wants. Focus on reliable, affordable used cars rather than brand-new, high-end models. A less expensive car means a smaller loan amount, which is easier to get approved for and more manageable to repay.

Many Maine car dealerships bad credit programs will have a selection of reliable used vehicles that fit within various budget constraints.

4. Demonstrate Stability

Lenders favor stability. A consistent employment history (e.g., at the same job for several years), a stable residence, and a history of paying bills on time (even if other credit issues exist) can positively influence their decision. Highlight these aspects during your application.

Understanding Loan Terms and Avoiding Predatory Practices

Once you receive an offer for poor credit auto loans, it’s critical to meticulously review the terms. Not all loan offers are created equal, and some can be more advantageous than others, even with bad credit.

1. Interest Rates

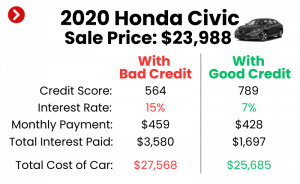

Expect higher interest rates with bad credit. This is the cost of borrowing money. While you might not qualify for the lowest rates, compare offers from different lenders. Even a percentage point difference can save you hundreds, if not thousands, over the life of the loan.

Pro tips from us: Don’t be afraid to walk away if an interest rate feels excessively high or if you suspect it’s predatory. Knowledge is power, and comparing offers empowers you to make a better decision.

2. Loan Duration (Term Length)

Loan terms typically range from 36 to 72 months, or even longer. A longer loan term means lower monthly payments, but you’ll pay significantly more in interest over time. Conversely, a shorter term means higher monthly payments but less overall interest.

For financing with bad credit, it’s often a balancing act between affordability and total cost. Choose a term that makes your monthly payments manageable without extending the loan unnecessarily.

3. Fees and Additional Costs

Be aware of any origination fees, application fees, or prepayment penalties. Some lenders might try to roll additional products, like extended warranties or GAP insurance, into your loan without fully explaining them. While some of these products can be valuable, ensure you understand what you’re paying for and if it’s truly necessary.

4. Read the Fine Print

This cannot be stressed enough. Before signing anything, read the entire loan agreement carefully. If there’s anything you don’t understand, ask for clarification. Don’t rush this process. Ensure all verbal agreements are reflected in the written contract.

After Approval: Rebuilding Your Credit with Your New Car Loan

Getting approved for bad credit car loans Maine is a significant step, but it’s also an opportunity to improve your financial standing. This loan can serve as a powerful tool for credit rebuilding.

Making consistent, on-time payments each month is paramount. Every payment reported positively to the credit bureaus will gradually contribute to an improved credit score. Over time, this will open doors to better financial products, lower interest rates on future loans, and greater financial freedom.

Pro tips from us: Set up automatic payments if possible to avoid missing due dates. Consider making slightly more than the minimum payment when you can, as this will help you pay off the loan faster and reduce the total interest paid.

Specific Considerations for Maine Residents

Beyond the general advice, there are a few Maine-specific points to keep in mind for auto financing Maine.

- Weather Conditions: Maine’s harsh winters mean that four-wheel drive or all-wheel drive vehicles are often preferred. Factor this into your vehicle choice and budget, as these models can sometimes be more expensive. Ensure your loan allows you to secure a safe and reliable vehicle for Maine’s climate.

- Local Dealerships: Explore local dealerships that advertise as "bad credit friendly" or specialize in subprime lending. These establishments often have established relationships with lenders who understand the unique financial situations of Maine residents. Many Maine car dealerships bad credit options are available throughout the state, from Augusta to Presque Isle.

- State Regulations: While federal laws govern much of consumer lending, it’s always good to be aware of any state-specific regulations in Maine that might apply to car loans or interest rate caps. The Maine Bureau of Financial Institutions can be a valuable resource.

Frequently Asked Questions About Bad Credit Car Loans in Maine

Here are answers to some common questions we encounter regarding bad credit auto loans:

- Can I get a car loan with no money down and bad credit in Maine?

While possible, it’s significantly more challenging. Lenders prefer a down payment to reduce their risk. If you have very bad credit, a no-money-down loan will likely come with very high interest rates and stricter terms. It’s always best to save for a down payment if you can. - How much interest will I pay with bad credit?

Interest rates for bad credit car loans vary widely based on your credit score, income, the lender, and the loan term. While someone with excellent credit might get rates below 5%, those with bad credit could see rates anywhere from 10% to 25% or even higher. It’s crucial to compare offers. - What documents do I absolutely need?

At a minimum, expect to provide proof of identity (driver’s license), proof of income (recent pay stubs), and proof of residency (utility bill). The more prepared you are, the smoother the process will be. - How long does it take to get approved?

Pre-qualification can be instantaneous online. A formal application can take anywhere from a few hours to a few days, depending on the lender and the complexity of your financial situation. Many dealerships can get you approved on the same day.

Driving Forward with Confidence in Maine

Securing Bad Credit Car Loans Maine might seem like an uphill battle, but with the right approach and a clear understanding of your options, it’s an entirely achievable goal. This comprehensive guide has provided you with the knowledge and strategies to navigate the process effectively. Remember to prepare thoroughly, explore all your lending options, understand your loan terms, and use this opportunity to rebuild your credit.

Don’t let a past financial setback prevent you from accessing the reliable transportation you need in Maine. By being informed and proactive, you can confidently drive away in a vehicle that meets your needs, paving the way for a more stable and mobile future. Start your journey today by assessing your credit and exploring the reputable lenders ready to assist Mainers just like you.