Navigating Bad Credit Car Loans in NYC: Your Ultimate Guide to Driving Away with Confidence

Navigating Bad Credit Car Loans in NYC: Your Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

New York City is a vibrant metropolis, famous for its bustling public transportation system. While many residents rely on subways and buses, there are countless situations where having your own vehicle becomes essential. Perhaps your job requires travel outside the subway lines, you have family commitments that demand flexibility, or you simply crave the freedom of the open road.

However, for many New Yorkers, the dream of car ownership hits a snag when faced with a less-than-perfect credit score. The term "bad credit" can feel like a heavy label, leading to frustration and the belief that securing a car loan in a competitive market like NYC is impossible. We’re here to tell you that this isn’t necessarily true.

Navigating Bad Credit Car Loans in NYC: Your Ultimate Guide to Driving Away with Confidence

As an expert in auto financing, particularly for challenging credit situations, I’ve seen countless individuals navigate these waters successfully. This comprehensive guide will demystify the process of obtaining bad credit car loans in NYC, offering practical strategies, expert insights, and actionable advice to help you secure the financing you need and drive away with confidence. Our ultimate goal is to equip you with the knowledge to make informed decisions and transform your car ownership aspirations into reality, even with bad credit.

Understanding "Bad Credit" in the NYC Auto Loan Landscape

Before diving into solutions, it’s crucial to understand what "bad credit" truly means in the eyes of auto lenders. Generally, credit scores fall within a range, and lenders categorize borrowers based on these scores. A FICO score below 600-620 is typically considered "subprime" or "bad credit."

This lower score indicates to lenders a higher risk of default, often stemming from past financial missteps like missed payments, bankruptcies, or high credit utilization. In the context of car loans, this doesn’t automatically disqualify you, but it does mean you’ll likely face different terms and a more rigorous application process.

New York City presents a unique environment for car ownership. While public transport is extensive, a car offers unparalleled convenience for specific needs, especially in the outer boroughs or for weekend escapes. Lenders understand this demand, which is why specialized bad credit car loan options exist, even in this densely populated urban center.

However, the sheer volume of lenders and dealerships in NYC can be overwhelming. It’s essential to approach the market with knowledge and a clear strategy to avoid pitfalls and secure the best possible deal for your situation.

The Reality Check: Can You Really Get a Car Loan with Bad Credit in NYC?

The short answer is a resounding yes, it is absolutely possible to get a car loan with bad credit in NYC. Many lenders specialize in working with borrowers who have less-than-perfect credit histories. They understand that life happens, and a past financial setback shouldn’t permanently bar you from essential purchases.

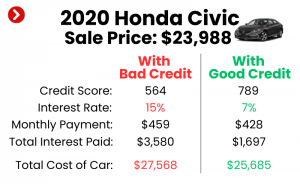

However, it’s crucial to set realistic expectations. You will likely encounter higher interest rates compared to someone with excellent credit. This is because lenders perceive a greater risk when extending credit to individuals with a history of payment challenges. Your loan terms might also be less flexible, and you may need to demonstrate additional stability.

The key to success lies not in finding a magic bullet, but in strategic preparation and understanding the various avenues available to you. With the right approach, you can navigate the NYC auto loan market effectively and secure financing that works for your budget and lifestyle. Don’t let your credit score be the sole determinant of your car ownership dreams.

Key Strategies for Securing a Bad Credit Car Loan in NYC

Securing a car loan with bad credit requires a proactive and informed approach. Based on my experience in the auto finance industry, these strategies are fundamental for improving your chances of approval and getting a fair deal.

1. Know Your Credit Score and Report Inside Out

This is your first and most critical step. Before even thinking about a car, you must understand your current credit standing. You can obtain a free copy of your credit report from each of the three major credit bureaus—Experian, Equifax, and TransUnion—once every 12 months through AnnualCreditReport.com.

Thoroughly review each report for any inaccuracies or errors. Mistakes on your credit report are surprisingly common and can negatively impact your score. If you find any discrepancies, dispute them immediately with the credit bureau; correcting these errors can often lead to a significant boost in your score. Knowing your score also helps you understand where you stand and manage your expectations when talking to lenders.

2. Save for a Significant Down Payment

A down payment is perhaps the most powerful tool you have when seeking a bad credit car loan. Lenders see a substantial down payment as a sign of your commitment and financial stability. It reduces the amount you need to borrow, which in turn lowers the lender’s risk.

Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price, if possible. A larger down payment can not only increase your chances of approval but also lead to lower monthly payments and potentially a better interest rate. It also provides you with immediate equity in the vehicle, which is a great starting point.

3. Find the Right Lender or Dealership

Not all lenders are created equal, especially when it comes to bad credit car loans. In NYC, you’ll find various options, each with its own advantages and disadvantages.

- Specialized Bad Credit Lenders: Many financial institutions focus specifically on subprime auto loans. These lenders are more accustomed to working with lower credit scores and often have more flexible criteria. You might find these through online searches or by inquiring with dealerships that advertise "special financing" or "credit rebuilder" programs.

- "Buy Here Pay Here" (BHPH) Dealerships: These dealerships act as both the seller and the lender. They can be a viable option for those with very poor credit, as they often have less stringent approval requirements. However, common mistakes to avoid are not scrutinizing the terms carefully. BHPH loans often come with significantly higher interest rates and less consumer protection. Always compare their offers with other lenders before committing.

- Traditional Banks and Credit Unions: While generally harder to secure with bad credit, don’t rule them out entirely, especially if you have an existing relationship. If you have a long history with a particular bank or credit union, they might be more willing to work with you. Credit unions, in particular, are known for offering more competitive rates to their members.

- Online Lenders/Marketplaces: Many online platforms specialize in connecting bad credit borrowers with lenders across the country, including those serving NYC. These can be a great way to get pre-qualified and compare offers from multiple lenders without multiple hard inquiries on your credit report.

Based on my experience, dealerships with dedicated "Special Finance" departments in NYC are often excellent starting points. These departments are staffed by finance managers who specialize in navigating challenging credit situations and have relationships with multiple subprime lenders.

4. Consider a Co-signer

If your credit score is particularly low, a co-signer with good credit can significantly improve your chances of approval and potentially secure a better interest rate. A co-signer essentially guarantees the loan, promising to make payments if you default.

However, this is a serious commitment for the co-signer. Their credit will be affected if you miss payments, and they will be legally responsible for the debt. Only ask someone you trust deeply and who fully understands the implications. Ensure you are absolutely confident in your ability to make every payment on time to protect their credit and your relationship.

5. Choose the Right Vehicle for Your Budget

When you have bad credit, affordability and practicality should be your top priorities, not luxury. Focus on purchasing a reliable used car that fits comfortably within your budget, rather than stretching for a brand-new vehicle.

A used car will have a lower purchase price, meaning a smaller loan amount and thus lower monthly payments. This makes it easier to manage your budget and consistently make on-time payments, which is crucial for rebuilding your credit. Research vehicle reliability to avoid unexpected repair costs, which can quickly derail your budget.

6. Prepare All Necessary Documentation

Lenders will want to see proof of your ability to repay the loan. Being organized and having all your documents ready can streamline the approval process.

Typically, you’ll need:

- Proof of identity (driver’s license, state ID)

- Proof of residency in NYC (utility bill, lease agreement)

- Proof of income (pay stubs, tax returns, bank statements)

- Proof of employment (employer contact information, recent pay stubs)

- References (sometimes required)

Demonstrating stable employment and consistent income is paramount for bad credit borrowers. It reassures lenders that you have the financial capacity to meet your monthly obligations.

7. Understand Interest Rates and Loan Terms

With bad credit, you should expect higher interest rates than someone with excellent credit. This is simply the cost of the increased risk for the lender. However, it doesn’t mean you should accept an exorbitant rate without question.

Focus on the total cost of the loan over its entire term, not just the monthly payment. A longer loan term (e.g., 72 or 84 months) might offer lower monthly payments, but you’ll pay significantly more in interest over time. Pro tips from us: Aim for the shortest loan term you can comfortably afford to minimize the total interest paid. Always ask for the Annual Percentage Rate (APR) to compare offers accurately.

8. Negotiate Wisely and Don’t Be Pressured

Many people make the common mistake of negotiating the monthly payment before negotiating the car’s price. Always negotiate the vehicle’s purchase price first, as if you were paying cash. Once you have an agreed-upon price, then discuss the financing terms.

Don’t feel pressured to make a decision on the spot. Take your time to review the loan agreement, understand all the clauses, and ensure there are no hidden fees. If something feels off, or you don’t fully understand a term, ask for clarification or walk away. There are many dealerships and lenders in NYC, and finding the right fit is worth the effort.

Common Mistakes to Avoid When Seeking a Bad Credit Car Loan in NYC

Navigating the world of bad credit auto loans can be tricky, and making the wrong moves can set you back significantly. Here are some common pitfalls to avoid:

- Applying Everywhere: Each time you apply for credit, a "hard inquiry" is placed on your credit report. Too many hard inquiries in a short period can further lower your score, making it even harder to get approved. Instead, use pre-qualification tools from online lenders or work with one or two trusted dealerships that can shop your application to multiple lenders.

- Hiding Financial Issues: Be transparent with lenders about your financial situation, including any past credit challenges. Trying to conceal information can lead to distrust and rejection. Explain any extenuating circumstances that led to your bad credit; sometimes, a compelling story can make a difference.

- Ignoring the Fine Print: Auto loan contracts can be lengthy and filled with jargon. Common mistakes to avoid are signing without fully understanding every clause, especially regarding interest rates, fees, prepayment penalties, and late payment charges. Always read the entire agreement before putting your signature on it.

- Falling for "Guaranteed Approval" Scams: Be extremely wary of any lender or dealership promising "guaranteed approval" regardless of your credit score. These are often predatory lenders who charge exorbitant interest rates, hide fees, or have unfavorable terms designed to trap borrowers in a cycle of debt. Legitimate lenders always conduct a credit check.

- Buying More Car Than You Can Afford: It’s tempting to get the flashiest car, but with bad credit, financial stability is your priority. Overextending yourself on a car payment is a recipe for disaster, leading to missed payments, potential repossession, and further damage to your credit score. Stick to a budget that leaves plenty of room for other expenses and emergencies.

The Road Ahead: Rebuilding Your Credit with Your New Car Loan

Getting approved for a bad credit car loan isn’t just about securing transportation; it’s a golden opportunity to rebuild your credit score. Your new auto loan can become a powerful tool for demonstrating responsible financial behavior.

Every single on-time payment you make is reported to the credit bureaus. This consistent positive activity will gradually improve your payment history, which is the most significant factor in your credit score. As your score improves, you’ll gain access to better financial products and lower interest rates in the future.

Pro tips from us: Set up automatic payments to ensure you never miss a due date. Consider making bi-weekly payments if your budget allows, as this can reduce the total interest paid and help you pay off the loan faster. Regularly monitor your credit score to see the positive impact of your efforts.

Expert Insights and Pro Tips from Us

Based on my extensive experience helping individuals navigate the complexities of auto financing, particularly in the unique NYC market, here are some final pro tips:

- Start Small, Aim for Improvement: Your first bad credit car loan might not be ideal, but it’s a stepping stone. Focus on making timely payments for 12-18 months. This can significantly improve your credit, potentially allowing you to refinance your loan at a lower interest rate later.

- Budgeting Before Buying: Before you even look at cars, create a detailed budget. Factor in not just the monthly loan payment, but also insurance (which can be higher in NYC), gas, parking, maintenance, and potential tolls. Understanding your total cost of ownership is vital for sustainable car ownership. For more detailed budgeting advice, you might find our article on Budgeting for a Car: What You Need to Know helpful. (Internal Link Placeholder 1)

- Research, Research, Research: Don’t just go to the first dealership you see. Use online resources, read reviews, and compare offers from multiple lenders and dealerships. Knowledge is power, especially when dealing with bad credit.

- Don’t Be Afraid to Walk Away: If a deal doesn’t feel right, if the terms are unfavorable, or if you feel pressured, simply walk away. There will always be other options. Your financial well-being is more important than a quick sale.

- Consider Pre-qualification: Many lenders offer pre-qualification that allows you to see potential loan terms without impacting your credit score. This gives you a clear idea of what you can afford before you start shopping for a car.

Conclusion: Your Journey to Car Ownership in NYC is Achievable

Securing a car loan with bad credit in NYC might seem like an uphill battle, but with the right knowledge, preparation, and perseverance, it is an entirely achievable goal. By understanding your credit, saving for a down payment, choosing the right lender, and being strategic in your approach, you can navigate the complexities of the auto finance world.

Remember, this isn’t just about getting a car; it’s about taking control of your financial future and rebuilding your credit along the way. Your new car loan can be a powerful tool to demonstrate financial responsibility, paving the way for better opportunities down the road. Stay informed, stay persistent, and soon you’ll be enjoying the freedom and convenience of driving your own vehicle through the vibrant streets of New York City.

If you’re looking for more ways to improve your financial standing, our guide on Understanding Your Credit Score: A Beginner’s Guide can provide further valuable insights. (Internal Link Placeholder 2)