Navigating Bad Credit Car Loans in Pensacola, FL: Your Comprehensive Guide to Driving Away with Confidence

Navigating Bad Credit Car Loans in Pensacola, FL: Your Comprehensive Guide to Driving Away with Confidence Carloan.Guidemechanic.com

For many in Pensacola, Florida, owning a reliable vehicle isn’t a luxury – it’s a necessity. From commuting to work along the beautiful Gulf Coast to handling daily errands and enjoying weekend adventures, a car provides essential freedom and convenience. However, if you’ve encountered financial setbacks and your credit score has taken a hit, the idea of securing a car loan can feel like an uphill battle.

The good news is that bad credit doesn’t have to put the brakes on your car ownership dreams. In Pensacola, FL, there are viable options available for individuals seeking bad credit car loans. This comprehensive guide will equip you with the knowledge, strategies, and confidence needed to navigate the auto financing landscape, secure a suitable loan, and ultimately drive away in a vehicle that meets your needs. We’ll delve deep into the specifics, offering practical advice and insider tips to help you make informed decisions.

Navigating Bad Credit Car Loans in Pensacola, FL: Your Comprehensive Guide to Driving Away with Confidence

Understanding Bad Credit and Its Impact on Car Loans

Before we explore the solutions, it’s crucial to understand what "bad credit" typically means in the context of auto financing and why it presents challenges. Your credit score is a numerical representation of your creditworthiness, largely based on your payment history, amounts owed, length of credit history, new credit, and credit mix.

What Defines "Bad Credit" for Lenders?

While there’s no single universally agreed-upon cutoff, credit scores generally fall into these categories:

- Excellent: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor/Bad: 300-579

If your FICO score falls below 600, or even into the low 600s, many traditional lenders will classify you as a "subprime" borrower. This designation indicates a higher perceived risk of default. Based on my experience in the auto financing industry, lenders become significantly more cautious when a borrower’s score dips into the "Fair" or "Poor" ranges.

Why Bad Credit Makes Auto Loans More Challenging

Lenders assess risk when approving loans. A low credit score signals to them that you might have a history of missed payments, defaults, or high debt, making them less confident in your ability to repay a new loan.

This increased risk translates into specific challenges:

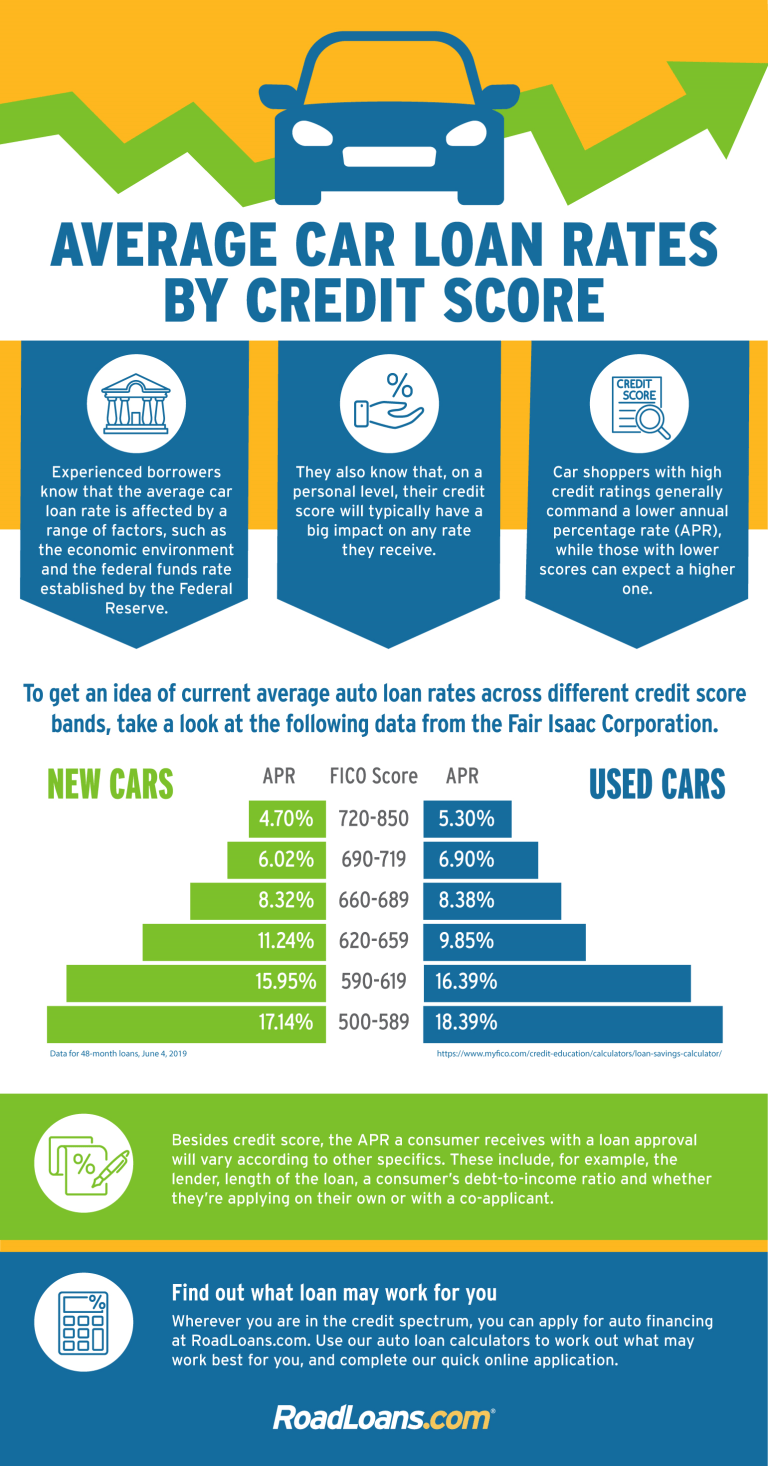

- Higher Interest Rates: To compensate for the elevated risk, lenders typically charge higher interest rates on bad credit car loans in Pensacola. This means you’ll pay more over the life of the loan.

- Stricter Approval Criteria: You might face more stringent requirements, such as a larger down payment or a shorter loan term.

- Limited Loan Options: Traditional banks might be less willing to lend, pushing you towards specialized bad credit lenders or in-house financing dealerships.

- Smaller Loan Amounts: Lenders may be hesitant to approve loans for very expensive vehicles, limiting your choices to more affordable options.

It’s important not to be discouraged by these factors. While the process requires more diligence, securing a reliable vehicle with bad credit is absolutely achievable in Pensacola, FL.

The Pensacola Landscape: Where to Find Bad Credit Car Loans

Pensacola, FL, being a vibrant community, offers a variety of lending avenues for individuals seeking auto financing, even with less-than-perfect credit. Knowing your options is the first step toward making an informed decision.

Types of Lenders in Pensacola for Bad Credit Auto Loans

Different types of institutions cater to different credit profiles. Understanding each can help you target your search effectively.

-

Traditional Banks and Credit Unions:

- Description: These are established financial institutions that often offer competitive rates for borrowers with good credit.

- For Bad Credit: While they primarily serve prime borrowers, some may have specific programs or departments that work with individuals who have fair credit or can offer secured loans. However, approval can be challenging for very low credit scores.

- Pro Tip: If you have an existing banking relationship with a local Pensacola bank or credit union, start there. They might be more willing to work with a long-term customer, even with a lower score.

- Example Local Credit Union: Pen Air Federal Credit Union, Navy Federal Credit Union (if eligible).

-

Specialized Subprime Lenders:

- Description: These lenders specifically focus on providing car loans to individuals with bad credit. They understand the challenges and structure their loans accordingly.

- For Bad Credit: This is often the most direct route for bad credit car loans in Pensacola. They have more flexible underwriting criteria compared to traditional banks.

- Considerations: Expect higher interest rates, but these lenders are more likely to approve your application. They often partner with dealerships.

-

Dealerships Offering In-House Financing (Buy Here, Pay Here – BHPH):

- Description: These dealerships not only sell cars but also act as the lender themselves. You make your payments directly to the dealership.

- For Bad Credit: BHPH dealerships are renowned for working with customers who have very poor credit or no credit history at all. They often focus more on your income and ability to pay than your credit score.

- Common Mistakes to Avoid: While convenient, BHPH loans often come with the highest interest rates and sometimes older, higher-mileage vehicles. Carefully scrutinize the vehicle’s condition and the loan terms. Ensure the dealership reports payments to credit bureaus to help you rebuild credit.

-

Online Auto Loan Marketplaces:

- Description: Websites that connect you with multiple lenders, often including subprime specialists, based on a single application.

- For Bad Credit: These platforms can be a great starting point for finding bad credit car loans in Pensacola because they allow you to compare offers from various lenders without multiple hard inquiries on your credit report (initially, at least).

- Benefit: Efficiency and convenience in finding potential lenders who are willing to work with your credit situation.

Based on my experience, for those specifically seeking bad credit car loans in Pensacola, FL, your most promising avenues will likely be specialized subprime lenders (often accessed through dealerships) and reputable buy here, pay here establishments. Online marketplaces can help you find these lenders more efficiently.

Preparing for Your Bad Credit Car Loan Application

Preparation is key to securing the best possible terms for your bad credit car loan. A well-prepared applicant demonstrates responsibility and seriousness, which can positively influence a lender’s decision.

1. Check Your Credit Score and Report

This is your starting point. You can’t improve what you don’t know.

- Why it’s Crucial: Knowing your credit score gives you a realistic expectation of what kind of loan terms you might qualify for. Reviewing your credit report allows you to identify any errors that could be unfairly dragging down your score.

- How to Do It: You are entitled to a free copy of your credit report from each of the three major bureaus (Experian, Equifax, TransUnion) once every 12 months via AnnualCreditReport.com. Many credit card companies and banks also offer free credit score monitoring.

- Pro Tip: Dispute any inaccuracies you find on your credit report immediately. Correcting errors can sometimes boost your score surprisingly quickly.

2. Create a Realistic Budget

Before even looking at cars, determine how much you can truly afford. This goes beyond just the monthly payment.

- Total Cost of Ownership: Factor in fuel, insurance (which can be higher with bad credit and certain vehicles), maintenance, and potential repair costs.

- Affordability: Your monthly car payment should comfortably fit within your budget without stretching your finances thin. Lenders will look at your debt-to-income ratio, so be realistic.

- Common Mistakes to Avoid: Overlooking insurance costs. For individuals with bad credit, insurance premiums can be significantly higher, especially for newer or more expensive vehicles. Get insurance quotes before you finalize your car choice.

3. Save for a Down Payment

A down payment is one of the most effective tools you have to improve your chances of approval and secure better loan terms with bad credit.

- Why it’s Crucial: A larger down payment reduces the amount you need to borrow, which lowers the lender’s risk. It also shows your commitment and ability to save.

- Benefits:

- Increases approval chances.

- Potentially lowers your interest rate.

- Reduces your monthly payments.

- Helps you build equity in the car faster.

- Pro Tip: Aim for at least 10-20% of the vehicle’s price, if possible. Even a few hundred dollars can make a difference.

4. Gather Necessary Documents

Being organized makes the application process smoother and faster.

- Typical Documents:

- Proof of identity (driver’s license, state ID)

- Proof of residency (utility bill, lease agreement)

- Proof of income (pay stubs, bank statements, tax returns if self-employed)

- Proof of insurance (you’ll need this before driving off the lot)

- References (sometimes required by subprime lenders)

5. Consider a Co-signer (If Applicable)

A co-signer with good credit can significantly improve your loan prospects.

- How it Helps: A co-signer essentially guarantees the loan. Their good credit history offsets your bad credit, making the loan less risky for the lender.

- Responsibilities: Both you and the co-signer are legally responsible for the loan. If you miss payments, it impacts both your credit scores. This is a serious commitment for the co-signer.

- Pro Tip: Only consider a co-signer if you are absolutely confident in your ability to make all payments on time. A missed payment could damage a personal relationship.

By taking these preparatory steps, you position yourself as a responsible borrower, even with a less-than-perfect credit history, making the search for bad credit car loans in Pensacola, FL, much more manageable.

Navigating the Bad Credit Car Loan Application Process

Once you’ve prepared, it’s time to start the actual application. This phase requires strategic thinking and a clear understanding of what lenders are looking for.

Where to Start Your Search in Pensacola

- Online Pre-Approval: Many lenders, including specialized subprime lenders and online marketplaces, offer online pre-approval forms. This allows you to see potential loan terms without committing to a specific vehicle or dealership. It also results in a "soft inquiry" on your credit, which doesn’t harm your score.

- Pro Tip: Get pre-approved by a few different lenders. This gives you leverage when negotiating at a dealership.

- Local Dealerships in Pensacola: Visit dealerships that advertise "bad credit car loans," "second-chance financing," or "we finance everyone." Many dealerships have finance managers who work with a network of lenders, including those specializing in bad credit.

- Common Mistakes to Avoid: Don’t let a dealership push you into a car you can’t afford or don’t truly need. Stick to your budget and research the vehicle’s reliability.

What Lenders Look For Beyond Your Credit Score

While your credit score is important, bad credit lenders consider other factors to assess your ability to repay:

- Stable Income: Lenders want to see consistent employment and sufficient income to cover the monthly payments.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to put towards a car payment.

- Down Payment Amount: As discussed, a larger down payment reduces the lender’s risk.

- Payment History on Other Bills: While your credit report might show some misses, a current history of on-time payments for rent, utilities, or other non-reported bills can be reassuring.

- Residency Stability: Lenders prefer borrowers who have lived at the same address for a significant period, as it suggests stability.

Common Mistakes to Avoid During Application

- Applying Everywhere: Too many hard inquiries in a short period can further damage your credit score. Focus on a few reputable lenders or use online pre-approval services.

- Hiding Information: Be honest about your financial situation. Lenders will uncover discrepancies, and honesty builds trust.

- Not Reading the Fine Print: Always read your loan agreement carefully before signing. Understand all terms, fees, and conditions.

- Falling for "Guaranteed Approval" Scams: While some dealerships are very lenient, no legitimate lender can guarantee approval without reviewing your financial situation. Be wary of promises that sound too good to be true.

Key Terms and Considerations for Bad Credit Car Loans

When dealing with bad credit car loans in Pensacola, FL, you’ll encounter specific terms and conditions that are vital to understand. These directly impact the total cost and manageability of your loan.

1. Interest Rates

This is arguably the most significant factor for bad credit borrowers.

- Expect Higher Rates: With bad credit, you will almost certainly face higher interest rates than someone with excellent credit. This is how lenders offset the increased risk.

- Comparing Rates: Don’t just accept the first offer. Compare interest rates from different lenders. Even a percentage point or two difference can save you hundreds, if not thousands, of dollars over the loan term.

- APR vs. Interest Rate: Understand the difference. The interest rate is the cost of borrowing money. The Annual Percentage Rate (APR) includes the interest rate plus any additional fees (like origination fees) associated with the loan, giving you the true annual cost of borrowing. Always compare APRs when evaluating offers.

2. Loan Terms (Loan Duration)

The loan term is the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months).

- Shorter Terms:

- Pros: Lower total interest paid, quicker path to ownership.

- Cons: Higher monthly payments, which can be challenging with a bad credit budget.

- Longer Terms:

- Pros: Lower monthly payments, making the loan more affordable in the short term.

- Cons: Significantly higher total interest paid over the life of the loan, increased risk of being "upside down" (owing more than the car is worth) for longer.

- Pro Tip: While a longer term might make monthly payments more manageable, aim for the shortest term you can comfortably afford to minimize the total cost of the loan.

3. Additional Fees

Be aware of any extra charges that might be added to your loan.

- Origination Fees: A fee charged by the lender for processing the loan.

- Documentation Fees: Charged by the dealership for preparing paperwork.

- Other Fees: Look out for charges related to credit checks, state taxes, registration, and title fees.

- Common Mistakes to Avoid: Not asking for a full breakdown of all fees. Some fees are legitimate, but others might be negotiable or questionable.

4. Prepayment Penalties

Some loans, particularly those for bad credit, may include clauses that charge you a fee if you pay off your loan early.

- Why it Matters: If you plan to refinance or pay off your loan ahead of schedule once your credit improves, a prepayment penalty could negate some of your savings.

- Always Ask: Specifically ask lenders if their loans have prepayment penalties. Based on my experience, reputable lenders are often transparent about this.

Understanding these key financial components will empower you to negotiate effectively and choose a bad credit car loan in Pensacola, FL, that aligns with your financial goals and capabilities.

Pro Tips for Securing the Best Deal on Your Bad Credit Car Loan

Even with bad credit, you have strategies to improve your position and get a more favorable deal. These pro tips are derived from years of observing successful borrowers.

1. Negotiate Everything

Don’t be afraid to negotiate, not just on the car’s price, but also on the loan terms.

- Car Price: Research the fair market value of the car you’re interested in using resources like Kelley Blue Book (KBB.com) or Edmunds. Negotiate the price of the vehicle before discussing financing.

- Interest Rate & Fees: If you have multiple pre-approvals, use them as leverage. Ask the dealership’s finance department if they can beat or match another lender’s offer. In my experience, showing a pre-approval from another lender signals that you’re a serious and informed buyer.

- Pro Tip from Us: Walk away if the deal doesn’t feel right. There are many dealerships and lenders in Pensacola, FL, and patience can pay off.

2. Improve Your Credit Score Before Applying (If Possible)

Even small improvements to your credit score can make a difference.

- Pay Down Existing Debts: Reducing your credit card balances can lower your credit utilization ratio, which positively impacts your score.

- Make On-Time Payments: Consistency is key. Ensure all your bills (credit cards, utilities, rent) are paid on time for several months leading up to your application.

- Check for Errors: As mentioned earlier, fixing errors on your credit report can quickly boost your score.

- Internal Link: For more in-depth strategies, consider reading our article on "Quick Ways to Boost Your Credit Score Before a Major Purchase" (placeholder).

3. Consider a Less Expensive, Reliable Used Car

While a brand-new car might be tempting, a reliable used vehicle is often a smarter choice for bad credit borrowers.

- Lower Loan Amount: A cheaper car means you borrow less, which translates to lower monthly payments and less interest paid over time.

- Reduced Risk: Lower initial investment and depreciation.

- Focus on Reliability: Prioritize vehicles known for their dependability and lower maintenance costs. A breakdown can quickly derail your budget.

4. Explore Refinancing Options Later

Your bad credit car loan isn’t necessarily a life sentence.

- Improve Your Credit: After 12-18 months of consistent, on-time payments on your car loan, your credit score should improve significantly.

- Seek Refinancing: Once your score is better, you can apply to refinance your loan with a traditional bank or credit union.

- Benefits of Refinancing: Potentially lower interest rates, which can drastically reduce your monthly payment or the total cost of the loan. This is a powerful strategy to save money in the long run.

- Internal Link: Learn more about the mechanics of interest rates in our article: "Demystifying Car Loan Interest Rates: What Every Borrower Needs to Know" (placeholder).

Life After the Loan: Rebuilding Your Credit

Securing a bad credit car loan in Pensacola, FL, isn’t just about getting a car; it’s also a powerful opportunity to rebuild your financial standing. This loan can be a stepping stone to a healthier credit future.

The Power of Consistent, On-Time Payments

Your car loan can be a significant positive entry on your credit report.

- Reporting to Credit Bureaus: Ensure your lender reports your payments to all three major credit bureaus (Experian, Equifax, TransUnion). Most legitimate auto lenders do, but it’s worth confirming, especially with smaller BHPH dealerships.

- Building a Positive History: Each on-time payment demonstrates your reliability and commitment to your financial obligations. This positive history gradually replaces negative entries and strengthens your credit profile.

- Pro Tip from Us: Set up automatic payments from your bank account to ensure you never miss a due date. Even a single late payment can set back your credit rebuilding efforts.

How Your Credit Score Improves

Over time, with diligent payments, you’ll see a noticeable improvement in your credit score.

- Payment History: This is the most heavily weighted factor in credit score calculations (around 35%). Perfect payment history on your car loan will significantly boost this component.

- Credit Mix: Adding an installment loan (like a car loan) to your credit profile, especially if you primarily had revolving credit (like credit cards), can diversify your credit mix and positively impact your score.

- Length of Credit History: As your loan matures, it contributes to a longer average age of your credit accounts, which is another positive factor.

Future Financial Opportunities

A higher credit score opens doors to many financial advantages:

- Lower Interest Rates: Not just for future car loans, but also for mortgages, personal loans, and credit cards.

- Easier Loan Approvals: You’ll find it much simpler to qualify for other forms of credit.

- Better Insurance Rates: Many insurance companies use credit scores as a factor in determining premiums.

- Improved Rental Opportunities: Landlords often check credit reports.

- Greater Financial Freedom: A strong credit score gives you more options and flexibility in managing your finances.

Using your bad credit car loan responsibly is an investment in your financial future. It’s a tangible way to prove your creditworthiness and regain control over your financial destiny.

Conclusion: Drive Towards a Brighter Financial Future in Pensacola, FL

Securing a car loan with bad credit in Pensacola, FL, might seem daunting, but it is an entirely achievable goal. By understanding the challenges, exploring your lending options, diligently preparing your application, and making informed decisions about loan terms, you can confidently navigate the process.

Remember, this isn’t just about getting a car; it’s an opportunity to take a significant step towards financial recovery. Use your car loan as a tool to rebuild your credit, demonstrating responsibility with every on-time payment. The road ahead might have a few bumps, but with the right knowledge and a proactive approach, you can drive away with a reliable vehicle and a clearer path to a healthier financial future.

Don’t let past financial difficulties define your present or future transportation needs. Start your journey today, armed with the insights from this guide, and find the bad credit car loan in Pensacola, FL, that works for you. Your independence on the roads of Pensacola awaits!

External Resource: For more comprehensive information on understanding and managing your credit, we recommend visiting the Consumer Financial Protection Bureau (CFPB) website at www.consumerfinance.gov. They offer valuable, unbiased resources for consumers.