Navigating Bad Credit Car Loans in Rochester MN: Your Ultimate Guide to Driving Away Today

Navigating Bad Credit Car Loans in Rochester MN: Your Ultimate Guide to Driving Away Today Carloan.Guidemechanic.com

Facing the challenge of a low credit score can feel like a roadblock when you need a car, especially when you’re specifically searching for "Bad Credit Car Loans Rochester MN." The need for reliable transportation in Rochester, Minnesota, is undeniable, whether it’s for commuting to work, taking your kids to school, or simply enjoying everything our vibrant city has to offer. Many people mistakenly believe that bad credit means an immediate dead end for securing an auto loan.

This couldn’t be further from the truth. While having a less-than-perfect credit history does present unique hurdles, it certainly doesn’t make car ownership an impossible dream. This comprehensive guide is designed to empower you with the knowledge and strategies needed to successfully navigate the world of bad credit car loans right here in Rochester, MN. We’ll dive deep into everything you need to know, from understanding your credit to securing the best possible terms and even using your loan to rebuild your financial future.

Navigating Bad Credit Car Loans in Rochester MN: Your Ultimate Guide to Driving Away Today

Understanding Bad Credit and Its Impact on Car Loans

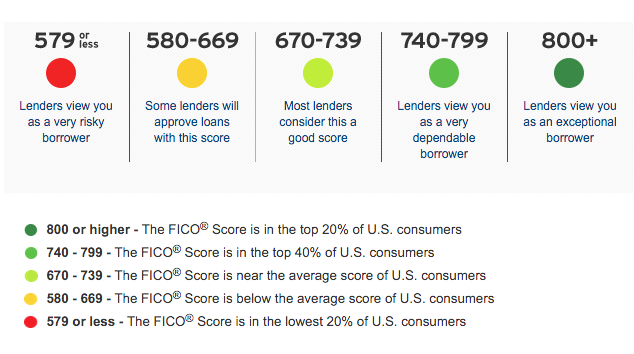

Before we delve into solutions, it’s crucial to understand what "bad credit" actually means in the eyes of a lender. Your credit score, typically a FICO score ranging from 300 to 850, is a numerical representation of your creditworthiness. Scores generally fall into categories: excellent (800+), very good (740-799), good (670-739), fair (580-669), and poor (300-579). A score in the "fair" or "poor" range is often considered bad credit.

Lenders use these scores to assess the risk of lending money. A lower score suggests a higher risk of default, meaning you might not repay the loan as agreed. This perceived risk directly influences their willingness to lend and the terms they offer. For individuals with bad credit, lenders often compensate for this higher risk by charging higher interest rates or requiring specific loan conditions.

However, the good news is that many lenders, particularly those specializing in subprime auto loans, understand that life happens. They recognize that a credit score doesn’t always tell the whole story. These lenders are often willing to work with individuals who have had financial setbacks, providing a vital pathway to car ownership for residents of Rochester, MN, who might otherwise be overlooked.

The Reality of Bad Credit Car Loans in Rochester MN

When you’re searching for "Bad Credit Car Loans Rochester MN," it’s important to set realistic expectations. While securing a loan is achievable, the terms might not be identical to someone with excellent credit. You’ll likely encounter higher Annual Percentage Rates (APRs) and potentially stricter down payment requirements. This is a standard practice in the subprime lending market to mitigate the increased risk for the lender.

Based on my experience working with countless individuals in Rochester and the surrounding areas, many local dealerships and financial institutions are equipped to handle bad credit situations. They understand the local economy and the transportation needs of our community. Their goal is often to find a workable solution that gets you into a reliable vehicle while also offering a chance to improve your credit standing.

Don’t let the initial terms discourage you. View this as an opportunity. A bad credit car loan, when managed responsibly, can be a powerful tool for credit rebuilding. Each on-time payment you make demonstrates your reliability, gradually improving your credit score over time.

Preparing for Your Bad Credit Car Loan Application

Preparation is paramount when applying for any loan, especially with bad credit. A well-prepared application can significantly increase your chances of approval and potentially secure more favorable terms. Here’s how to get ready:

1. Know Your Credit Score and Report

The very first step is to understand exactly where you stand. Obtain copies of your credit report from all three major bureaus (Experian, Equifax, and TransUnion) and check your FICO score. You can get a free report annually from each bureau at AnnualCreditReport.com. Review these reports meticulously for any errors or inaccuracies. Disputing and correcting these can sometimes give your score a quick, beneficial boost.

Knowing your score also helps you anticipate what lenders will see. It allows you to speak confidently about your credit history and explain any past issues rather than being surprised by them during the application process.

2. Budgeting is Key

Before even looking at cars, create a realistic budget that accounts for all your monthly expenses, including the potential car payment, insurance, fuel, and maintenance. Pro tips from us: Don’t underestimate the power of a solid budget. An affordable car payment is one you can consistently make without stretching your finances too thin. Lenders want to see that you have the income to support the loan, and a well-thought-out budget demonstrates your financial responsibility.

Remember, the total cost of car ownership extends far beyond just the monthly payment. Factor in everything to avoid future financial strain.

3. Gather Necessary Documents

Having all your paperwork in order beforehand streamlines the application process. Typically, you’ll need:

- Proof of identity (driver’s license or state ID)

- Proof of residency (utility bill, lease agreement)

- Proof of income (recent pay stubs, bank statements, tax returns if self-employed)

- Proof of insurance (or be ready to obtain it)

- References (sometimes required)

Having these documents ready shows lenders you are serious and organized, making the process smoother for everyone involved.

4. Consider a Down Payment

A down payment, even a small one, can significantly improve your chances of approval and potentially lower your interest rate. By putting money down, you reduce the amount you need to borrow, which decreases the lender’s risk. It also shows your commitment to the loan. Based on my experience, even 5-10% of the car’s value can make a noticeable difference in how lenders perceive your application.

If you can save up a larger down payment, you’ll likely see even better terms. It’s a clear signal to lenders that you have some financial stability.

5. Find a Co-signer (If Possible)

If you have a trusted friend or family member with good credit who is willing to co-sign for you, this can be a huge advantage. A co-signer essentially guarantees the loan, meaning they agree to make payments if you default. This significantly reduces the risk for the lender, often leading to better interest rates and more favorable terms.

However, a word of caution: a co-signer takes on significant responsibility. If you miss payments, it will negatively impact their credit as well. Ensure both parties fully understand the implications before proceeding.

Where to Find Bad Credit Car Loans in Rochester MN

Rochester, MN, offers several avenues for individuals seeking bad credit car loans. Knowing where to look can save you time and help you find the right fit. Common mistakes to avoid are jumping at the first offer without comparing options.

1. Local Dealerships Specializing in Subprime Loans

Many dealerships in and around Rochester, MN, have dedicated finance departments that specialize in working with customers who have less-than-perfect credit. These dealerships often have relationships with multiple lenders, including those that specifically cater to subprime borrowers. They understand the nuances of bad credit financing and can guide you through the process.

Look for dealerships that advertise "we finance everyone," "credit rebuilding programs," or similar slogans. These are often indicators that they are equipped to handle diverse credit situations.

2. Credit Unions & Local Banks

Don’t overlook local credit unions and community banks in Rochester. While they might have stricter lending criteria than some specialized subprime lenders, they often offer more personalized service and potentially lower interest rates if you qualify. Credit unions, in particular, are member-focused and might be more flexible, especially if you have an existing relationship with them.

It’s always worth checking with your current bank or local credit union first, as they might be more willing to work with you based on your existing account history.

3. Online Lenders

A growing number of online lenders specialize in bad credit auto loans. These platforms offer convenience, allowing you to apply from home and often receive quick pre-approval decisions. However, it’s crucial to exercise caution. Thoroughly research any online lender, read reviews, and ensure they are reputable. Compare their offers with those from local institutions to ensure you’re getting a competitive deal.

While convenient, always be wary of online lenders that promise guaranteed approval without any credit check, as these can often lead to predatory loan terms.

The Application Process for Bad Credit Auto Loans

Once you’ve done your prep work and identified potential lenders, the application process itself is the next step. Understanding each stage will help you navigate it confidently.

1. Pre-Approval: Your Strategic Advantage

Before you even step foot on a car lot, consider getting pre-approved for a loan. Pre-approval involves a soft credit inquiry (which doesn’t harm your score) and gives you a clear idea of how much you can borrow, at what interest rate, and under what terms. This allows you to shop for a car with a solid budget in mind, putting you in a stronger negotiating position.

With a pre-approval in hand, you become a cash buyer in the eyes of the dealership, shifting the focus from your credit to the car’s price. For more tips on negotiating car prices, check out our guide on .

2. Completing the Application

When filling out the loan application, be completely honest and provide accurate information. Lenders will verify your income, employment, and residency. Any discrepancies can lead to delays or even rejection. Be prepared to explain any negative items on your credit report; often, a clear, concise explanation can help the lender understand your situation better.

Transparency builds trust, and trust is crucial when dealing with bad credit.

3. Reviewing Loan Offers

If you receive multiple loan offers, don’t just look at the monthly payment. Focus on the Annual Percentage Rate (APR), which includes the interest rate plus any fees, giving you the true cost of borrowing. Also, consider the loan term (how long you have to repay) and the total amount you’ll pay over the life of the loan. A lower monthly payment often means a longer loan term and more interest paid overall.

Take your time to compare offers side-by-side. Understand all the fees, penalties, and conditions before making a decision.

4. Choosing the Right Vehicle

With bad credit, practicality should often outweigh luxury. Choose a reliable, affordable vehicle that meets your needs without overextending your budget. A more expensive car will mean a larger loan, higher payments, and potentially higher interest. Focus on getting a vehicle that will reliably get you where you need to go in Rochester, MN.

Remember, the goal is not just to get a car, but to get a car that you can afford and use as a stepping stone to improve your financial health.

Key Factors Affecting Your Bad Credit Car Loan Terms

Several elements play a critical role in shaping the terms of your bad credit auto loan. Understanding these can help you better prepare and negotiate.

1. Interest Rate (APR)

The interest rate, often expressed as an APR, is arguably the most significant factor. With bad credit, your APR will be higher than someone with excellent credit. This reflects the increased risk the lender is taking. The difference of even a few percentage points can add hundreds or thousands of dollars to the total cost of your loan over its lifetime.

Your credit score, income, debt-to-income ratio, and the loan term all influence the APR you’ll be offered.

2. Loan Term

The loan term is the duration over which you’ll repay the loan, typically ranging from 36 to 72 months. A shorter loan term means higher monthly payments but less interest paid overall. A longer loan term results in lower monthly payments but significantly more interest over the life of the loan.

While a longer term might seem appealing due to lower monthly payments, always calculate the total cost to ensure you’re not paying an exorbitant amount in interest.

3. Down Payment Amount

As discussed, a substantial down payment reduces the principal amount borrowed, directly impacting your monthly payments and the total interest accrued. It also signals financial stability to lenders. The more you put down, the better your loan terms are likely to be.

4. Vehicle Choice

The type of vehicle you choose also affects your loan terms. Newer, more expensive cars often come with higher interest rates and require larger down payments, especially for bad credit borrowers. Lenders also consider the car’s depreciation rate and resale value, as the vehicle acts as collateral for the loan.

Opting for a slightly older, reliable, and more affordable used car can often result in more favorable loan terms for those with bad credit.

Strategies for Improving Your Financial Situation While Repaying Your Loan

Securing a bad credit car loan is not just about getting a car; it’s a golden opportunity to rebuild your credit and improve your financial future.

1. Make Payments On Time, Every Time

This is the single most crucial step. Based on my experience, consistently making on-time payments is the most effective way to rebuild your credit. Payment history accounts for 35% of your FICO score. Every on-time payment you make gets reported to the credit bureaus, gradually improving your score and demonstrating your reliability as a borrower. Set up automatic payments or reminders to ensure you never miss a due date.

2. Avoid Additional Debt

While repaying your car loan, try to avoid taking on new debt. This includes opening new credit cards or taking out personal loans. Lenders prefer to see a manageable debt-to-income ratio. Focusing on paying down your existing debts, especially high-interest ones, will also free up more money for your car payments and improve your overall financial health.

3. Monitor Your Credit Report

Continue to monitor your credit report regularly. Check for any errors, fraudulent activity, or unexpected changes. As your score improves, you’ll be able to track your progress and see the positive impact of your consistent payments. This can also motivate you to continue your responsible financial habits.

4. Refinancing Options

Once you’ve made 6-12 months of on-time payments and your credit score has improved, you might be eligible to refinance your car loan. Refinancing means taking out a new loan, often with a lower interest rate, to pay off your existing loan. This can significantly reduce your monthly payments and the total amount of interest you pay over the life of the loan.

It’s a smart strategy to consider once your credit has stabilized and improved.

Common Myths About Bad Credit Car Loans

There are many misconceptions floating around about bad credit car loans that can deter people from even trying. Let’s debunk a few:

- Myth 1: "You’ll definitely get ripped off." While bad credit loans come with higher interest rates, being informed and doing your research means you won’t necessarily get "ripped off." By comparing offers and understanding terms, you can find a fair deal.

- Myth 2: "You can only get a beat-up, unreliable car." Many dealerships offer quality used vehicles that are still reliable and within your budget. Focus on a car’s condition and maintenance history, not just its price tag.

- Myth 3: "It’s impossible to improve your credit with a bad credit car loan." On the contrary, this is one of the most effective ways to rebuild credit. Consistent, on-time payments demonstrate your ability to manage debt responsibly, leading to a higher credit score.

Pro Tips for a Smooth Car Buying Experience in Rochester MN

To ensure your journey to car ownership in Rochester is as smooth as possible, keep these pro tips in mind:

- Negotiate Wisely: Even with bad credit, there’s often room for negotiation on the car’s price. However, be realistic. Focus on getting a fair deal on the vehicle first, then discuss financing.

- Read the Fine Print: Always read every line of your loan agreement before signing. Understand all fees, terms, and conditions. Don’t hesitate to ask questions if anything is unclear.

- Don’t Feel Pressured: Never feel rushed or pressured into making a decision. If a deal doesn’t feel right, walk away. There are always other options available in Rochester.

- Seek Advice: If you’re unsure, consult a trusted financial advisor or an experienced friend or family member before signing. For more resources on personal finance, visit a trusted external source like the Consumer Financial Protection Bureau (CFPB) website for unbiased information on auto loans and credit.

- Consider Insurance Costs: Get insurance quotes for the vehicles you’re considering. Insurance costs can vary wildly and significantly impact your overall monthly budget.

Building a Brighter Financial Future (Beyond the Loan)

Getting a bad credit car loan in Rochester, MN, is more than just acquiring a vehicle; it’s a strategic move towards financial recovery. It’s a tangible step you’re taking to prove your creditworthiness and open doors to better financial opportunities in the future. Once you’ve successfully managed your car loan for a period, you’ll find other financial products, like mortgages or personal loans, becoming more accessible and affordable.

Remember that this car loan is a tool. Use it wisely, and it will serve as a strong foundation for a much brighter financial future. To learn more about improving your overall financial health, explore our article on .

Conclusion

Securing "Bad Credit Car Loans Rochester MN" is an entirely achievable goal, not a pipe dream. While the path may require a bit more preparation and understanding, it’s a journey many residents of our community successfully embark on. By understanding your credit, preparing thoroughly, knowing where to look for lenders, and managing your loan responsibly, you can drive away in a reliable vehicle.

More importantly, you can use this opportunity to rebuild your credit score, opening up a world of better financial possibilities down the road. Don’t let past financial setbacks define your future. Take control, educate yourself, and start your journey towards car ownership and improved financial health in Rochester today.