Navigating Bad Credit Car Loans in Springfield, IL: Your Comprehensive Guide to Driving Forward

Navigating Bad Credit Car Loans in Springfield, IL: Your Comprehensive Guide to Driving Forward Carloan.Guidemechanic.com

Securing a car loan can feel like a daunting challenge, especially when past financial hurdles have impacted your credit score. If you’re in Springfield, Illinois, and find yourself in this situation, you’re not alone. Many residents face the same concerns, wondering if owning a reliable vehicle is an achievable dream.

The good news is that bad credit car loans in Springfield, IL, are not only possible but also a pathway to rebuilding your financial standing. This comprehensive guide is designed to empower you with the knowledge, strategies, and confidence needed to navigate the process successfully. We’ll delve deep into every aspect, ensuring you have all the tools to make an informed decision and drive away in the car you need.

Navigating Bad Credit Car Loans in Springfield, IL: Your Comprehensive Guide to Driving Forward

Understanding the Landscape: What Exactly Are Bad Credit Car Loans?

Before we dive into the specifics of Springfield, IL, it’s crucial to understand what "bad credit" means in the context of auto financing. Generally, a credit score below 600-620 is considered "subprime" or "bad credit" by most lenders. This doesn’t mean you’re uncreditworthy; it simply indicates a higher perceived risk for financial institutions.

Lenders assess your credit history to gauge your reliability in repaying debts. A lower score might reflect late payments, defaults, or even a lack of credit history. These factors can make traditional lenders hesitant, often leading to higher interest rates or stricter loan terms.

However, the market for auto loans bad credit has evolved significantly. Many lenders and dealerships now specialize in assisting individuals with less-than-perfect credit. They understand that life happens, and a credit score doesn’t always tell the whole story.

Based on my experience working with countless individuals in similar situations, securing a car loan with bad credit isn’t about finding a magic bullet. It’s about preparation, understanding your options, and knowing how to present yourself as a responsible borrower, even with past blemishes on your credit report. It’s a journey, and every step taken correctly improves your outcome.

The Springfield, IL Auto Finance Scene: Your Local Options

Springfield, IL, offers a variety of avenues for individuals seeking car financing Springfield IL options, even with poor credit. Knowing where to look and what to expect from each type of lender is your first strategic advantage. Each has its own benefits and drawbacks, particularly for those with a challenging credit history.

Traditional Banks and Credit Unions

While often the first choice for prime borrowers, traditional banks and credit unions can be more stringent with their lending criteria. They typically offer the lowest interest rates to applicants with excellent credit. For those with bad credit, securing a loan directly from these institutions might be challenging, or the terms offered may not be competitive.

However, if you have an existing relationship with a local credit union in Springfield, it’s always worth inquiring. Credit unions are member-focused and might be more flexible or willing to work with members who have a long-standing history with them, even with a lower credit score. Their decisions can sometimes be more personalized than those of larger banks.

Dealerships Specializing in Bad Credit

Many car dealerships in and around Springfield, IL, have dedicated finance departments that work with a network of lenders specializing in poor credit car financing. These dealerships often have relationships with "subprime" lenders who are more willing to approve loans for individuals with lower credit scores. They understand the nuances of the market and can often match you with a suitable lender.

When exploring dealerships for bad credit Springfield IL, look for those advertising "second-chance financing" or "credit re-establishment programs." These phrases often indicate a willingness and capability to help. Our pro tip is to focus on dealerships that clearly communicate their process and offer transparency in their financing options, rather than those that seem to rush you into a decision.

Online Lenders and Lending Marketplaces

The digital age has brought a wealth of online lending options. Numerous online platforms specialize in connecting individuals with bad credit to lenders who can approve their loan applications. These platforms often provide quick pre-approval decisions and can offer competitive rates.

The advantage of online lenders is convenience and speed. You can apply from the comfort of your home, and often receive multiple offers, allowing you to compare terms easily. However, always ensure the online lender is reputable and transparent about all fees and interest rates. From our vantage point in the auto finance industry, verifying legitimacy is paramount when dealing with online entities.

Buy-Here-Pay-Here (BHPH) Dealerships

These are dealerships that also act as the lender. They finance the vehicle directly through their own company, often without extensive credit checks. For individuals with very severe credit issues or no credit history, BHPH dealerships can be a viable option to buy a car with bad credit Springfield.

While they offer a high approval rate, it’s crucial to approach BHPH options with caution. Interest rates can be significantly higher, and the vehicle selection might be limited to older, higher-mileage cars. Furthermore, not all BHPH dealerships report payments to credit bureaus, which negates one of the key benefits of getting a loan with bad credit – the opportunity to rebuild your credit score.

Preparing for Success: Your Pre-Application Checklist

Success in securing bad credit car loans Springfield IL heavily relies on thorough preparation. Walking into the process informed and organized significantly increases your chances of approval and helps you secure more favorable terms. This isn’t just about getting a loan; it’s about getting the right loan.

1. Know Your Credit Score and Report

Your credit score is the first thing lenders will look at. Obtain a copy of your credit report from all three major bureaus (Experian, Equifax, and TransUnion) at AnnualCreditReport.com. Review it carefully for any inaccuracies, which you can dispute to potentially boost your score.

Understanding what’s on your report allows you to anticipate lender concerns. It also gives you leverage. If you can explain past issues (e.g., medical emergency, temporary job loss), it can humanize your application.

2. Establish a Realistic Budget

Before you even look at cars, determine how much you can realistically afford each month for a car payment, insurance, and maintenance. Use a budget calculator to factor in all your monthly expenses and income. Overextending yourself on a car payment is a common mistake that can lead to financial strain and even repossession.

Pro tips from us: Aim for a payment that is comfortable, not just manageable. Remember that interest rates for bad credit loans will be higher, meaning more of your payment goes towards interest initially.

3. Save for a Down Payment

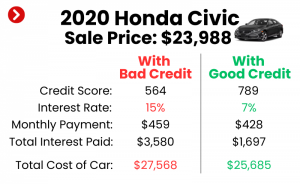

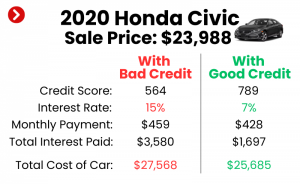

A significant down payment is one of the most powerful tools you have when seeking bad credit car loans. It reduces the amount you need to borrow, thereby lowering your monthly payments and the total interest paid. More importantly, it signals to lenders that you are serious and have some financial discipline.

Lenders view a substantial down payment as a sign of commitment and reduced risk. It shows you have "skin in the game." Aim for at least 10-20% of the car’s purchase price if possible. Even a smaller down payment is better than none.

4. Gather Necessary Documents

Lenders will require documentation to verify your identity, income, and residency. Having these ready will streamline the application process. Common documents include:

- Government-issued photo ID (driver’s license)

- Proof of residence (utility bill, lease agreement)

- Proof of income (recent pay stubs, bank statements, tax returns if self-employed)

- Proof of insurance (you’ll need this before driving off the lot)

- List of references (sometimes requested)

Common mistakes to avoid are showing up without proper documentation or with outdated information. This can delay your application or even lead to denial. Being organized demonstrates responsibility.

The Application Process: A Step-by-Step Guide

Once you’ve done your homework, it’s time to engage with lenders. The process for get a car loan with bad credit might differ slightly from traditional loans, but the core steps remain similar. Understanding them will help you navigate with confidence.

Step 1: Get Pre-Approved (If Possible)

Many lenders, especially online ones, offer a pre-approval process. This involves a soft credit inquiry (which doesn’t harm your score) and gives you an idea of the loan amount and interest rate you might qualify for. A pre-approval acts like a conditional offer, giving you significant leverage when you visit dealerships in Springfield, IL.

Having a pre-approval in hand means you walk onto the lot as a cash buyer, knowing your budget before falling in love with a car outside your price range. It shifts the focus from "Can I get a loan?" to "Which car can I buy with this loan?"

Step 2: Choose Your Vehicle Wisely

With bad credit, it’s often wise to opt for a reliable, affordable used car rather than a brand-new, expensive model. A lower purchase price means a smaller loan amount, lower payments, and less overall interest. Focus on reliability and fuel efficiency.

Remember, this first loan is often a stepping stone. Your goal is to secure a car you need, make timely payments, and begin rebuilding your credit score. You can always upgrade later once your financial standing improves.

Step 3: Complete the Full Application

Whether you’re working with a dealership’s finance department or an online lender, you’ll complete a full loan application. This will involve a hard credit inquiry, which might temporarily dip your score by a few points. However, multiple hard inquiries for the same type of loan within a short period (usually 14-45 days) are often grouped as one for scoring purposes, so don’t be afraid to shop around.

Be honest and accurate with all information provided. Any discrepancies can lead to delays or even outright denial. Lenders appreciate transparency, especially when dealing with bad credit scenarios.

Step 4: Review and Negotiate Loan Terms

Once approved, you’ll receive a loan offer detailing the interest rate, loan term (length), and monthly payment. Don’t be afraid to ask questions. Understand every line of the contract.

Pro tips from us: Focus on the total cost of the loan over its lifetime, not just the monthly payment. A longer loan term might offer lower monthly payments but will result in paying significantly more in interest. Try to negotiate for the shortest term you can comfortably afford.

Finding the Right Dealership in Springfield, IL for Bad Credit

Your choice of dealership is paramount when seeking bad credit car loans in Springfield, IL. Not all dealerships are equally equipped or willing to assist buyers with credit challenges. You need a partner, not just a seller.

Look for dealerships that openly advertise their ability to help customers with varying credit scores. Websites that feature phrases like "credit challenges welcome," "fresh start financing," or "we work with all credit types" are good indicators. These dealerships typically have dedicated finance managers experienced in working with subprime lenders.

When you visit a dealership, pay attention to their customer service. Do they listen to your needs? Are they transparent about the financing options available? A reputable dealership will take the time to explain everything clearly and not pressure you into a decision. Ask about their network of lenders; a wider network means more options for you.

Based on our years of experience, a truly helpful dealership will focus on finding a solution that fits your budget and helps you move forward, rather than just pushing the most expensive car or loan. They understand that a satisfied customer, even with bad credit, can become a loyal customer and refer others.

Strategies to Improve Your Chances (and Future Credit)

Beyond the immediate loan application, several strategies can significantly improve your chances of approval for Springfield IL auto loans and, crucially, set you on a path to a better financial future.

Consider a Co-signer

If you have a trusted family member or friend with good credit who is willing to co-sign your loan, it can dramatically improve your chances of approval and secure a lower interest rate. A co-signer essentially guarantees the loan, taking on equal responsibility for repayment.

While this can be a huge help, it’s a significant commitment for your co-signer. Ensure you are absolutely confident in your ability to make timely payments, as any missed payments will negatively impact both your credit scores.

Opt for a Smaller Loan Amount and a Modest Car

As mentioned earlier, aiming for a less expensive car reduces the risk for lenders and the overall cost for you. A smaller loan amount means lower monthly payments, making it easier to manage and reducing the chance of default. This is a strategic move to build positive credit history.

Focus on cars that are reliable and meet your essential needs, rather than focusing on luxury features. This practical approach will pay dividends in the long run.

The Power of Timely Payments

This is perhaps the most critical strategy. Once you secure your bad credit car loan, making every payment on time, every month, is paramount. Payment history is the most significant factor in your credit score. Consistent, on-time payments will gradually build a positive credit history, showing future lenders that you are a responsible borrower.

Over time, this positive payment history will increase your credit score, opening doors to better financial products, lower interest rates, and more opportunities down the line. It’s the ultimate goal of getting a bad credit loan – to use it as a tool for credit repair. Further reading:

Explore Refinancing Options Later

Once you’ve made 6-12 months of on-time payments, your credit score will likely have improved. At this point, you might be eligible to refinance your car loan at a lower interest rate. Refinancing can significantly reduce your monthly payment and the total interest you pay over the life of the loan. This is a smart financial move that many with bad credit leverage to save money.

Common Pitfalls and How to Avoid Them

Even with the best intentions, the world of auto finance can have its traps. Being aware of common pitfalls will help you avoid costly mistakes when pursuing auto loans bad credit in Springfield, IL.

High-Pressure Sales Tactics

Some dealerships might use aggressive sales tactics to push you into a deal that isn’t in your best interest. They might rush you through paperwork or try to upsell you on unnecessary add-ons. Don’t be afraid to walk away if you feel pressured or uncomfortable. Take your time, ask questions, and never sign anything you don’t fully understand.

Unrealistic Loan Terms

Be wary of loan offers with extremely long terms (e.g., 72 or 84 months) or excessively high interest rates. While a longer term means lower monthly payments, it also means you’ll pay significantly more in interest over the life of the loan. This can also lead to being "upside down" on your loan, where you owe more than the car is worth.

The "Too Good to Be True" Trap

If a deal seems too good to be true, it probably is. Be skeptical of promises of "guaranteed approval" regardless of credit, especially without a down payment. Always read the fine print and ensure all verbal agreements are documented in writing.

Hidden Fees and Add-Ons

Review the purchase agreement carefully for any hidden fees or unnecessary add-ons like extended warranties or protection packages that you didn’t agree to or don’t need. While some add-ons can be valuable, others are simply profit generators for the dealership. Understand what you are paying for and why.

Beyond the Loan: Building a Better Financial Future

Securing bad credit car loans in Springfield, IL, is not just about getting a vehicle; it’s a pivotal step towards financial improvement. Your journey doesn’t end when you drive off the lot; it truly begins.

The Importance of Responsible Repayment

Every on-time payment you make is a brick in the foundation of your improved credit score. Prioritize your car payment, even above other discretionary spending. Set up automatic payments to ensure you never miss a due date. This consistency will be recognized by credit bureaus and future lenders.

Regularly Monitor Your Credit Score

Keep an eye on your credit score and report regularly. Seeing your score improve can be incredibly motivating. It also allows you to catch any new errors or fraudulent activity promptly. Many credit card companies and banks now offer free credit score monitoring services.

The Benefits of a Good Credit Score

As your credit score improves, a world of financial opportunities opens up. You’ll qualify for lower interest rates on future loans (mortgages, personal loans), better credit card offers, and even lower insurance premiums. A good credit score signifies financial responsibility and can save you thousands of dollars over your lifetime. Explore more:

Conclusion: Your Path to Driving Forward in Springfield, IL

Navigating bad credit car loans in Springfield, IL, requires diligence, preparation, and a clear understanding of your options. While it might seem challenging, it’s an entirely achievable goal that can significantly impact your mobility and financial future. By understanding your credit, budgeting wisely, saving for a down payment, and choosing the right lending partner, you can overcome past credit challenges.

Remember, this isn’t just about buying a car; it’s about making a smart financial decision that serves as a stepping stone to better credit. Take control of your financial narrative, make responsible choices, and soon you’ll be enjoying the freedom of the open road in Springfield, IL, with a vehicle you earned and a credit score you’re actively rebuilding. Start your journey today – the right car, and a brighter financial future, await.