Navigating Bank of America Auto Loan Rates for Used Cars: Your Ultimate Guide

Navigating Bank of America Auto Loan Rates for Used Cars: Your Ultimate Guide Carloan.Guidemechanic.com

Embarking on the journey to purchase a used car can be exciting, but securing the right financing is often the most critical step. For many, Bank of America stands out as a prominent option, offering a wide array of financial products, including auto loans. However, understanding Bank Of America Auto Loan Rates Used Cars requires more than just a quick glance at a rate sheet. It demands a deep dive into eligibility, application processes, and the myriad factors influencing your final interest rate.

This comprehensive guide is designed to be your go-to resource. We’ll demystify the complexities of obtaining a used car loan from Bank of America, providing you with actionable insights, expert tips, and a clear roadmap to secure the best possible financing for your next pre-owned vehicle. Our goal is to empower you with the knowledge needed to make informed decisions and drive away with confidence.

Navigating Bank of America Auto Loan Rates for Used Cars: Your Ultimate Guide

Understanding Bank of America’s Role in Used Car Financing

Bank of America is one of the largest financial institutions in the United States, offering a broad spectrum of banking and lending services. When it comes to auto loans, they are a significant player, providing financing solutions for both new and used vehicles. Their extensive network and competitive offerings make them a popular choice for many car buyers.

Choosing a reputable lender like Bank of America offers several advantages. You benefit from their established processes, customer support, and the potential for competitive interest rates, especially if you’re already a Bank of America customer with an existing relationship. This familiarity can often streamline the application process.

It’s crucial to recognize the distinction between new and used car loans. While both aim to help you finance a vehicle, used car loans typically come with slightly different parameters. This can include varying interest rates, vehicle age restrictions, and mileage limitations, all of which we will explore in detail.

Decoding Bank of America Auto Loan Rates for Used Cars

The interest rate you receive on a used car loan from Bank of America is not a one-size-fits-all figure. Instead, it’s a dynamic number influenced by several interconnected factors. Understanding these elements is key to predicting and potentially improving the rate you’ll be offered.

What Influences Your Interest Rate?

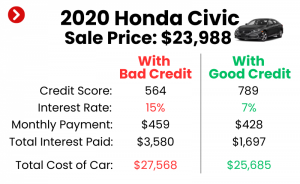

Your credit score is arguably the most significant determinant of your interest rate. Lenders, including Bank of America, use your credit score as a primary indicator of your creditworthiness and your likelihood to repay the loan. A higher credit score signals lower risk, typically resulting in lower interest rates.

The loan term, which is the length of time you have to repay the loan, also plays a crucial role. Shorter loan terms often come with lower interest rates because the lender’s risk exposure is reduced over a shorter period. However, shorter terms usually mean higher monthly payments.

The amount of your down payment also impacts your rate. A larger down payment reduces the amount you need to borrow, which can lower the lender’s risk and potentially lead to a more favorable interest rate. It also shows your commitment to the purchase.

Furthermore, the specific details of the used vehicle you intend to purchase can affect the rate. Factors like the car’s age, mileage, make, model, and overall condition are assessed. Lenders might view older, high-mileage vehicles as higher risk due to potential maintenance issues and faster depreciation, which could translate into slightly higher rates.

Typical Rate Ranges and How to Find Current Rates

While Bank of America frequently updates its advertised rates, it’s important to remember these are often "as low as" rates, usually reserved for applicants with excellent credit. Based on my experience, individuals with strong credit (720+) might see rates in the low single digits, while those with fair or good credit (620-719) could expect rates that are several percentage points higher. These are general ranges, and your specific offer will vary.

To find the most accurate and current Bank Of America Auto Loan Rates Used Cars, your best approach is to visit their official auto loan section online. They typically provide a rate checker tool where you can input basic information (credit score range, loan term, vehicle type) to get a personalized estimate. This pre-qualification step is invaluable.

Pro tips from us: Don’t just look at the advertised rates. Always take the time to pre-qualify or get a pre-approval. This gives you a concrete rate offer based on your specific financial profile, allowing you to shop for a car with a clear budget and financing in hand.

Eligibility Requirements: What Bank of America Looks For

Securing a used car loan from Bank of America involves meeting a set of specific eligibility criteria. Understanding these requirements beforehand can significantly streamline your application process and increase your chances of approval.

Credit Score: The Cornerstone of Approval

As mentioned, your credit score is paramount. Bank of America, like most lenders, utilizes credit scores to gauge your financial responsibility. While they don’t publicly state a minimum credit score for auto loans, applicants with scores in the "good" to "excellent" range (typically 670 and above) are more likely to qualify for their most competitive rates.

Even if your credit score is less than ideal, you might still qualify, albeit potentially at a higher interest rate. Bank of America considers your entire financial picture, not just one number. However, aiming for the best possible credit score before applying will always yield better results.

Income and Debt-to-Income (DTI) Ratio

Bank of America will assess your income to ensure you have the financial capacity to make regular loan payments. They will look at your employment history, stability, and overall income level. A steady and sufficient income is crucial for demonstrating repayment ability.

Your debt-to-income (DTI) ratio is another critical factor. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to cover new loan payments, which is favorable to lenders. A high DTI can signal financial strain and may affect your approval or the rate you receive.

Residency and Age

To apply for a loan with Bank of America, you typically need to be a U.S. citizen or a permanent resident, and at least 18 years of age. These are standard requirements for most financial institutions and ensure legal capacity to enter into a loan agreement.

Vehicle Requirements: Not Just Any Used Car

Bank of America also has specific requirements for the used vehicle itself. Common stipulations include limitations on the vehicle’s age and mileage. For instance, they might only finance vehicles that are no older than 10 years and have not exceeded a certain mileage threshold, such as 125,000 or 150,000 miles. These requirements help mitigate the risk associated with older, potentially less reliable vehicles.

The vehicle’s value, as determined by an independent appraisal guide like Kelley Blue Book (KBB) or NADAguides, is also important. Bank of America will typically only lend up to a certain percentage of the vehicle’s established market value. This ensures that the loan amount is commensurate with the car’s actual worth.

A common mistake applicants make is assuming any used car will qualify. Always verify the vehicle’s specifics against Bank of America’s current requirements before you get too far into the car-buying process. This can save you significant time and potential disappointment.

The Application Process: Step-by-Step with Bank of America

Applying for a used car loan with Bank of America is a structured process, designed to be straightforward for applicants. Understanding each stage can help you navigate it smoothly and efficiently.

Pre-qualification vs. Pre-approval

Before diving into a full application, it’s wise to understand the difference between pre-qualification and pre-approval. Pre-qualification gives you an estimate of what you might qualify for, often with a soft credit inquiry that doesn’t impact your score. It’s a good starting point for budgeting.

Pre-approval, on the other hand, involves a more thorough review of your financial information and a hard credit inquiry. If approved, you receive a conditional offer for a specific loan amount and interest rate, valid for a certain period. This is incredibly powerful as it essentially makes you a cash buyer at the dealership, giving you leverage in negotiations.

Gathering Your Documents

To ensure a smooth application, have all necessary documents ready. This typically includes:

- Personal Identification: Driver’s license or state ID.

- Proof of Income: Recent pay stubs, tax returns, or bank statements.

- Proof of Residency: Utility bill or lease agreement.

- Social Security Number.

- Vehicle Information (if already selected): VIN, make, model, year, mileage.

Having these items organized before you apply can significantly speed up the process. It demonstrates preparedness and professionalism, which can positively influence the lender.

The Application Itself: Online or In-Person

Bank of America offers the convenience of applying for an auto loan online through their website. This is often the quickest and most popular method, allowing you to complete the application from the comfort of your home. The online portal guides you through each step, requesting personal, financial, and employment information.

Alternatively, you can visit a Bank of America branch to apply in person. This option is beneficial if you prefer face-to-face interaction or have complex questions that you’d like to discuss directly with a loan officer. Both methods lead to the same outcome, so choose the one that suits your preference.

What Happens After Application

Once you submit your application, Bank of America will review your information, pull your credit report, and assess your eligibility. You will typically receive a decision within one to two business days, sometimes even faster for online applications. If approved, you’ll receive a loan offer outlining the interest rate, loan amount, and terms.

Pro tips from us: Always get pre-approved before you start serious car shopping. This not only gives you a firm offer but also empowers you to negotiate confidently with dealerships, knowing exactly what financing you already have secured. It puts you in the driver’s seat of the car-buying experience.

Maximizing Your Chances for the Best Used Car Loan Rates

While Bank of America’s rates are competitive, there are proactive steps you can take to ensure you secure the most favorable terms for your used car loan. These strategies focus on improving your financial profile and making smart choices during the loan process.

Improving Your Credit Score

Your credit score is a reflection of your financial health. Before applying, dedicate time to improving it. Pay down existing debts, especially credit card balances, to lower your credit utilization. Make all your payments on time, as payment history is the largest factor in your score. Avoid opening new credit accounts just before applying, as this can temporarily lower your score.

For more tips on improving your credit score, check out our guide on .

Making a Larger Down Payment

A substantial down payment signals to the lender that you are serious about the purchase and reduces their risk. The less money you need to borrow, the lower the loan-to-value (LTV) ratio, which often translates to a better interest rate. Aim for at least 10-20% of the vehicle’s purchase price if possible.

A larger down payment also reduces your monthly payments and the total interest paid over the life of the loan. This can lead to significant long-term savings and a more manageable financial commitment.

Choosing a Shorter Loan Term

While longer loan terms offer lower monthly payments, they almost always come with higher interest rates over the life of the loan. Opting for the shortest loan term you can comfortably afford can save you thousands in interest. Assess your budget carefully to find the right balance between monthly payment affordability and total cost.

Shopping Around (Even with BofA as a Preference)

Even if Bank of America is your preferred lender, it’s always wise to compare offers from a few different financial institutions. This ensures you’re getting the most competitive rate available to you. Having multiple offers can also give you leverage if you want to negotiate with Bank of America for a better rate.

Negotiating with the Dealer (If Applicable)

If you’re buying from a dealership, remember that they often have their own financing options or preferred lenders. While it’s convenient, their initial offer might not always be the best. Use your pre-approval from Bank of America as a negotiating tool to either get a better rate from the dealer or stick with your BofA offer.

Considering a Co-signer

If your credit score is fair or you have a limited credit history, adding a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate. A co-signer shares responsibility for the loan, reducing the lender’s risk. However, ensure both parties understand the implications.

Beyond the Rate: Other Factors to Consider

While the interest rate is a major component of any auto loan, it’s not the only factor that impacts your overall cost and experience. A holistic view of the loan terms will help you make the best decision.

Loan Terms (Length)

As discussed, the loan term affects both your monthly payment and the total interest paid. Longer terms mean lower monthly payments but more interest over time. Shorter terms mean higher monthly payments but less overall interest. Carefully evaluate your budget and financial goals to choose the term that’s right for you.

Fees and Charges

Always inquire about any associated fees with the loan. This might include origination fees, application fees, or prepayment penalties. Bank of America is generally transparent about their fees, but it’s always good practice to ask for a full breakdown of all costs upfront. Hidden fees can significantly increase the actual cost of your loan.

Payment Options

Bank of America typically offers various convenient payment options, including automatic deductions from your checking account, online payments, or payments by mail. Understanding these options and choosing one that fits your routine can help you avoid late payments and maintain a good payment history. Setting up auto-pay is often the easiest way to ensure timely payments.

Customer Service and Support

Consider the quality of customer service and support offered by the lender. Bank of America has a robust customer service network, but it’s worth noting their hours of operation and available channels for assistance. Having reliable support can be invaluable if you encounter questions or issues during the life of your loan.

Refinancing Options

Life circumstances change, and sometimes, so do interest rates. Bank of America may offer options to refinance your used car loan down the road. If your credit score improves significantly after you’ve taken out the initial loan, or if market rates drop, refinancing could save you money. It’s a good idea to know if this flexibility exists.

Common Pitfalls and How to Avoid Them

Even with the best intentions, car buyers can fall into common traps when seeking auto financing. Being aware of these pitfalls can help you avoid costly mistakes and secure a better deal.

Not Checking Your Credit Report

One of the most frequent errors is not reviewing your credit report before applying for a loan. Your report might contain inaccuracies or outdated information that could negatively impact your score. Always get a free copy of your credit report from AnnualCreditReport.com and dispute any errors before applying.

Accepting the First Offer

Never feel pressured to accept the first loan offer you receive, whether it’s from a dealership or a bank. As mentioned earlier, shopping around and comparing offers is crucial. This due diligence ensures you’re getting the most competitive rate available based on your credit profile.

Overlooking Total Cost vs. Monthly Payment

It’s easy to get fixated on the monthly payment, especially when budgeting. However, focusing solely on the lowest monthly payment can lead to longer loan terms and significantly more interest paid over time. Always consider the total cost of the loan, including principal and all interest, when making your decision.

Ignoring Vehicle Requirements

As we discussed, Bank of America has specific requirements for the age and mileage of used vehicles they will finance. Common mistakes to avoid are falling in love with a car that doesn’t meet these criteria and then facing rejection. Always confirm the vehicle’s eligibility before getting emotionally invested in a particular car.

Not Factoring in Additional Costs

Beyond the loan, remember to budget for other car-related expenses. These include insurance, registration fees, taxes, and potential maintenance costs for a used vehicle. A true understanding of your overall car ownership costs will prevent financial surprises down the line.

For the most up-to-date information on Bank of America’s auto loan offerings, always refer to their official website: External Link: Bank of America Auto Loans.

Conclusion: Driving Forward with Confidence

Securing a used car loan from Bank of America can be a straightforward and rewarding process when approached with the right knowledge. By understanding how Bank Of America Auto Loan Rates Used Cars are determined, diligently preparing your application, and proactively working to improve your financial standing, you significantly enhance your chances of obtaining favorable terms.

Remember, the key to a successful auto loan experience lies in preparation, comparison, and attention to detail. Don’t just settle for the first offer; empower yourself with information, ask questions, and make choices that align with your financial well-being. With the insights provided in this guide, you are now better equipped to navigate the world of used car financing and drive off in your desired vehicle with confidence and peace of mind. Start your journey today by exploring Bank of America’s offerings and taking the first step towards your next used car.