Navigating BB&T Bank Car Loans: Your Ultimate Guide to Truist Auto Financing Success

Navigating BB&T Bank Car Loans: Your Ultimate Guide to Truist Auto Financing Success Carloan.Guidemechanic.com

The dream of a new car often begins long before you set foot on a dealership lot. It starts with imagining the open road, the comfort of a reliable vehicle, and the freedom it offers. For many, turning that dream into a reality involves securing the right financing. Historically, BB&T Bank was a trusted name for countless individuals seeking auto loans, known for its customer-centric approach and competitive offerings.

However, the financial landscape is always evolving. BB&T Bank, a prominent player in the banking sector, merged with SunTrust Bank in 2019 to form Truist Financial Corporation, one of the largest banks in the United States. This significant transition means that while you might be searching for "BB&T Bank Car Loan," the services you’re looking for are now offered under the Truist brand. This comprehensive guide will walk you through everything you need to know about securing a Truist auto loan, leveraging the legacy of BB&T’s commitment to its customers.

Navigating BB&T Bank Car Loans: Your Ultimate Guide to Truist Auto Financing Success

Our goal is to equip you with the knowledge and confidence to navigate the world of car financing effectively. We’ll delve deep into Truist’s vehicle financing options, the application process, key factors that influence your loan, and expert tips to ensure you secure the best possible terms. Whether you’re eyeing a brand-new model, a reliable used car, or looking to refinance an existing loan, this article is your definitive resource.

Understanding Truist Auto Loans: The Evolution from BB&T

The merger of BB&T and SunTrust was a monumental event, creating a new banking powerhouse: Truist. This consolidation brought together two strong institutions, combining their strengths, resources, and customer bases. For those seeking auto loans, this transition means accessing a broader range of financial products and services backed by an even larger, more robust institution.

While the name has changed, the commitment to helping individuals finance their vehicles remains a core part of Truist’s offering. They continue to provide flexible and competitive car financing solutions designed to meet diverse needs. This evolution signifies an enhanced capability to serve customers, integrating best practices from both legacy banks.

Why Consider Truist for Your Car Financing Needs?

Based on my experience in the financial industry, choosing the right lender is paramount. Truist, as the successor to BB&T, offers several compelling reasons to consider them for your vehicle financing options:

- Established Reputation: Truist carries the combined legacy of BB&T and SunTrust, both long-standing banks known for their reliability and customer service. This provides a level of trust and stability that newer lenders might not offer.

- Comprehensive Offerings: They provide a variety of auto loan products, catering to different vehicle types and financial situations. This flexibility allows you to find a loan that truly fits your specific requirements.

- Competitive Rates: Truist aims to offer competitive auto loan rates, helping you manage your monthly payments and overall loan cost. Their scale allows them to be a strong contender in the market.

- Customer Support: With a vast network and substantial resources, Truist emphasizes customer support, offering assistance throughout the application and repayment process. This can be invaluable when you have questions or need guidance.

Choosing a reputable financial institution for your auto loan is a decision that impacts your financial health for years. Truist’s background and current offerings position them as a strong choice for many car buyers.

Decoding Truist’s Vehicle Financing Options

Truist provides a range of auto loan products designed to suit various car purchasing scenarios. Understanding these options is the first step toward making an informed decision about your car loan. Each type serves a specific purpose, tailored to the condition and age of the vehicle you intend to purchase, or your existing loan situation.

1. New Car Loans

If you’re in the market for a brand-new vehicle, a new car loan from Truist is specifically designed for this purpose. These loans typically come with certain advantages. Lenders often view new cars as less risky due to their pristine condition and manufacturer’s warranty.

This can translate into more favorable interest rates and longer loan terms compared to financing a used vehicle. New car loans are ideal for those who want the latest features, minimal maintenance worries in the initial years, and the opportunity to customize their ride directly from the dealership. The process is generally straightforward when purchasing from an authorized dealer.

2. Used Car Loans

For many drivers, a pre-owned vehicle offers excellent value and affordability. Truist also provides used car loan options, allowing you to finance a pre-owned vehicle with confidence. While the terms might differ slightly from new car loans, they are still highly competitive.

Key factors for used car loans include the vehicle’s age, mileage, and condition. Lenders typically have specific criteria for the maximum age and mileage they will finance. Opting for a used car loan is a smart financial move if you’re looking to save money on depreciation and overall purchase price while still getting a reliable vehicle.

3. Auto Loan Refinancing

Perhaps you already have a car loan but are looking for better terms. Refinancing a car loan with Truist could be an excellent strategy. Refinancing involves taking out a new loan to pay off your existing auto loan, ideally at a lower interest rate or with more favorable terms.

This can be particularly beneficial if your credit score has improved significantly since you first took out the loan, or if market interest rates have dropped. Refinancing can lead to lower monthly payments, reduced total interest paid over the life of the loan, or even a shorter repayment period. It’s a proactive step towards optimizing your existing auto financing.

4. Lease Buyout Loans

For those currently leasing a vehicle, Truist may offer lease buyout loans. When your lease term ends, you often have the option to purchase the car at a predetermined price. A lease buyout loan provides the necessary funds to complete this purchase.

This option is particularly appealing if you love your leased car, have kept it in excellent condition, and the buyout price is favorable. It allows you to transition from leasing to ownership, avoiding penalties for excess mileage or wear and tear, and continuing to drive a vehicle you’re already familiar with and enjoy.

The Truist Auto Loan Application Process: A Step-by-Step Guide

Securing a Truist auto loan doesn’t have to be a daunting task. Understanding the application process beforehand can significantly streamline your experience and increase your chances of approval. Based on my insights, preparation is key.

Key Requirements for Car Loan Eligibility

Before you even begin the application, it’s crucial to understand the fundamental criteria lenders like Truist consider. These requirements help them assess your ability to repay the loan.

- Credit Score: Your credit score is perhaps the most significant factor. It’s a numerical representation of your creditworthiness. A higher credit score indicates a lower risk to lenders, often leading to better auto loan rates. While there’s no official minimum, aiming for a score in the "good" to "excellent" range (typically 670 and above) is advisable for the best terms. Truist does offer options for various credit profiles, but your score will dictate your rate.

- Income and Employment: Lenders need to confirm you have a stable source of income to make your monthly payments. This usually involves providing proof of employment, such as pay stubs, W-2 forms, or tax returns if you’re self-employed.

- Debt-to-Income (DTI) Ratio: Your DTI ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates you have more disposable income to manage new debt, making you a more attractive borrower. Lenders typically prefer a DTI ratio below 43%.

- Down Payment: While not always mandatory, making a down payment for a car loan significantly reduces the amount you need to borrow, thereby lowering your monthly payments and total interest paid. It also shows the lender your commitment and reduces their risk.

- Vehicle Information: For a secured auto loan, the vehicle itself serves as collateral. You’ll need details like the make, model, year, mileage, and Vehicle Identification Number (VIN) for the car you intend to purchase.

Step-by-Step Application Guide

Once you’ve gathered your financial documents and understood the requirements, the application process for a Truist auto loan generally follows these steps:

- Gather Your Documents: Collect necessary identification (driver’s license), proof of income, residence, and any other financial statements Truist may request. Having these ready accelerates the process.

- Get Pre-Approved: This is a pro tip from us! Applying for Truist pre-approval is highly recommended. Pre-approval gives you a clear understanding of how much you can borrow, your estimated interest rate, and your potential monthly payment before you even step into a dealership. It allows you to shop like a cash buyer, strengthening your negotiation position. You can typically apply for pre-approval online.

- Complete the Application: Whether online, over the phone, or in person at a Truist branch, you’ll fill out a detailed application form. Be accurate and honest with all information provided.

- Underwriting and Review: Truist’s loan officers will review your application, credit history, income, and other financial details. They may contact you for additional information or clarification.

- Receive a Decision: You’ll be notified of Truist’s decision. If approved, you’ll receive a loan offer outlining the terms, including the loan amount, interest rates, and repayment schedule.

- Finalize the Loan: Once you accept the terms, you’ll sign the necessary paperwork. The funds will then be disbursed to the dealership (for a new purchase) or to you (for refinancing or a lease buyout).

Factors Influencing Your Auto Loan: What You Need to Know

Several key elements come into play when Truist determines your loan eligibility and the specific terms of your car financing. Understanding these factors empowers you to improve your position as a borrower and secure a more favorable deal.

1. Your Credit Score: The Game Changer

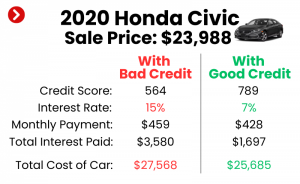

As mentioned, your credit score for a car loan is paramount. It’s not just a number; it’s a summary of your financial responsibility. A higher score signifies a history of timely payments and responsible credit management, which translates to lower perceived risk for the lender.

- Excellent Credit (780-850): You’ll likely qualify for the lowest auto loan rates available, often advertised as promotional rates.

- Good Credit (670-779): You’ll still receive very competitive rates, although they might be slightly higher than those with excellent credit.

- Fair Credit (580-669): Approval is still possible, but your rates will be higher to compensate for the increased risk. You might need to make a larger down payment.

- Poor Credit (300-579): Securing a standard loan can be challenging, and if approved, the interest rates will be significantly higher. For those with bad credit car loan Truist options might still exist, but they require careful consideration of the terms. You might need a co-signer or a secured loan with a substantial down payment.

Based on my experience, consistently paying bills on time, keeping credit utilization low, and checking your credit report for errors are crucial steps to maintaining a healthy credit score.

2. Interest Rates: What to Expect

The interest rate is the cost of borrowing money, expressed as a percentage of the loan amount. It directly impacts your monthly payments and the total cost of the loan over its lifetime. Truist, like other lenders, sets interest rates based on several factors:

- Market Conditions: General economic conditions and the Federal Reserve’s policies influence overall interest rates.

- Your Creditworthiness: This is the most significant individual factor.

- Loan Term: Shorter loan terms often have slightly lower interest rates, as the lender’s risk exposure is reduced.

- Vehicle Type: New cars often qualify for lower rates than used cars.

It’s vital to compare rates from different lenders, and even within Truist’s offerings, to ensure you’re getting the best possible deal. Don’t just accept the first rate you’re offered.

3. Loan Terms: Balancing Payments and Total Cost

The loan terms refer to the length of time you have to repay the loan. Common terms for auto loans range from 24 months (2 years) to 84 months (7 years).

- Shorter Terms (e.g., 36 or 48 months): These typically come with higher monthly payments but result in less interest paid over the life of the loan. You’ll own your car outright sooner.

- Longer Terms (e.g., 60, 72, or 84 months): These offer lower monthly payments, making the car more "affordable" on a month-to-month basis. However, you’ll pay significantly more in total interest over the longer repayment period, and your car will depreciate more before you pay it off.

A common mistake to avoid is focusing solely on the lowest monthly payment. Always consider the total cost of the loan over its entire term.

4. Down Payment: Its Impact

Making a down payment for a car loan is a powerful financial move. It directly reduces the principal amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay.

- Reduces Risk: A larger down payment signals to the lender that you’re a serious and responsible borrower, potentially leading to better loan terms.

- Builds Equity Faster: You start with more equity in your car, reducing the risk of being "upside down" (owing more than the car is worth).

- Lower Monthly Payments: A smaller loan amount means smaller installments.

While 10-20% is often recommended for new cars, any amount you can put down will be beneficial.

5. Vehicle Type and Age

The type of vehicle you’re financing also plays a role. New cars typically get better rates and longer terms because they have a predictable value and are less likely to require immediate major repairs. Used cars, especially older ones, are considered higher risk due to potential mechanical issues and faster depreciation, which can lead to higher rates or shorter maximum loan terms.

Pro Tips for Securing the Best Truist Auto Loan

Beyond understanding the basics, there are strategies you can employ to significantly improve your chances of getting a fantastic deal on your Truist auto loan. These insights come from years of observing successful financial planning.

1. Improve Your Credit Before You Apply

This is the single most impactful step. If you know you’ll be needing a car loan in the near future, start working on your credit score now. Pay down existing debts, especially credit card balances, and ensure all your payments are on time. A few months of diligent effort can make a substantial difference in your interest rate.

2. Shop Around, Even Within Truist’s Offerings

While this article focuses on Truist, it’s always wise to compare offers from at least three different lenders. This gives you leverage and ensures you’re getting a competitive rate. Even within Truist, different loan products might have slightly varied terms, so discuss all available options with your loan officer.

3. Negotiate the Car Price Separately

Pro tip from us: Always negotiate the vehicle’s purchase price before discussing financing options. Dealers often try to bundle these discussions, which can obscure the true cost of each. Knowing your pre-approved loan amount from Truist allows you to focus solely on getting the best price for the car itself.

4. Understand All Fees and Charges

Read the loan agreement carefully. Ensure you understand all fees, including origination fees, application fees, and late payment charges. Don’t hesitate to ask your Truist representative for clarification on any term or fee you don’t understand. Transparency is key in any financial agreement.

5. Consider a Co-Signer (If Applicable)

If you have a lower credit score, adding a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate. Remember, a co-signer is equally responsible for the loan, so it should only be considered with someone you trust implicitly and who understands the commitment.

Common Mistakes to Avoid When Applying for an Auto Loan

Even experienced car buyers can fall prey to common pitfalls. Being aware of these common mistakes to avoid can save you money and stress in the long run.

- Not Getting Pre-Approved: This is perhaps the biggest mistake. Without pre-approval, you’re walking into the dealership blind, susceptible to whatever financing terms they offer. Having a Truist pre-approval in hand gives you power.

- Focusing Only on Monthly Payments: While important, solely looking at the lowest monthly payment can lead you into a longer loan term with significantly more interest paid over time. Always consider the total cost of the loan.

- Ignoring Total Loan Cost: Calculate the total amount you’ll pay over the life of the loan (principal + interest). A seemingly low monthly payment over 72 or 84 months can add up to thousands more in interest.

- Skipping the Vehicle Inspection: Especially for used cars, always get an independent mechanic to inspect the vehicle before finalizing the purchase. This can save you from buying a lemon and needing unexpected repairs shortly after purchase.

- Applying for Too Many Loans Simultaneously: Each loan application results in a "hard inquiry" on your credit report, which can temporarily ding your score. Group your loan applications within a short timeframe (e.g., 14-45 days) so credit bureaus count them as a single inquiry for rate shopping purposes.

Managing Your Truist Auto Loan: Post-Approval Best Practices

Once your Truist auto loan is approved and you’re driving your new vehicle, the journey isn’t over. Effective loan management is crucial for maintaining good financial health.

Payment Options

Truist offers various convenient ways to make your monthly payments:

- Online Banking: Set up automatic payments through your Truist online account to ensure you never miss a due date.

- Mobile App: Manage your loan and make payments on the go using the Truist mobile banking app.

- Phone Payments: Make payments over the phone with a customer service representative.

- Mail: Send checks or money orders via postal service.

- In-Branch: Visit a Truist branch to make your payment in person.

Automating your payments is a pro tip from us to avoid late fees and maintain a positive payment history, which further strengthens your credit score.

Early Payoff Benefits

If your financial situation improves, consider paying off your loan earlier than scheduled. Most auto loans, including those from Truist, do not have prepayment penalties. Paying extra each month or making lump-sum payments can:

- Save on Interest: The sooner you pay off the principal, the less interest accrues over time.

- Free Up Cash Flow: Once the loan is paid off, that monthly payment amount becomes disposable income or can be directed towards other financial goals.

- Improve Debt-to-Income Ratio: Reducing your debt load positively impacts your DTI, which can be beneficial for future lending needs.

Is a Truist Car Loan Right for You? Making an Informed Decision

Deciding whether a Truist auto loan is the best fit for your needs involves a careful evaluation of your personal financial situation and the specific terms offered. As an expert, I always advise a thorough self-assessment.

Consider your credit score, current income, existing debts, and how comfortable you are with the proposed monthly payments and loan terms. If you value a large, established bank with a wide range of services and competitive rates, Truist, carrying on the legacy of BB&T, presents a strong option. Their commitment to customer service and diverse loan products makes them a contender for many borrowers.

Before committing, ensure you:

- Understand All Terms: Leave no stone unturned in understanding the APR, total interest, and any potential fees.

- Compare Offers: Always compare your Truist offer with at least one or two other lenders to ensure competitiveness.

- Assess Your Budget: Can you comfortably afford the monthly payments without straining your budget? Build in a buffer for unexpected expenses.

- Read the Fine Print: Never sign a loan agreement without fully reading and understanding every clause.

For additional financial planning insights, you might find resources on responsible borrowing helpful. External Link: Consumer Financial Protection Bureau – Auto Loans

Conclusion: Driving Forward with Confidence

Securing the right car loan is a significant step towards car ownership. While the name "BB&T Bank Car Loan" has evolved into Truist auto loan, the commitment to providing accessible and competitive vehicle financing remains steadfast. By understanding the different loan types, navigating the application process with diligence, and implementing smart financial strategies, you can secure favorable terms that align with your budget and goals.

Remember, knowledge is your most powerful tool in the car buying journey. Armed with the insights from this comprehensive guide, you are now well-equipped to make informed decisions about your car financing with Truist. Drive forward with confidence, knowing you’ve chosen a path that’s both financially sound and aligned with your automotive dreams. Happy driving!