Navigating Car Loan Programs For Bad Credit: Your Comprehensive Guide to Driving Away with Confidence

Navigating Car Loan Programs For Bad Credit: Your Comprehensive Guide to Driving Away with Confidence Carloan.Guidemechanic.com

For many, a car isn’t just a luxury; it’s a necessity for work, family, and daily life. But what happens when your credit history stands in the way of securing that essential set of wheels? If you’ve faced the challenge of bad credit, you know the frustration and often, the feeling of being stuck. The good news is, a less-than-perfect credit score doesn’t mean your dream of car ownership is out of reach.

Securing a car loan with bad credit is absolutely possible, but it requires a strategic approach, thorough understanding, and a willingness to explore various options. This in-depth guide is designed to empower you with the knowledge and strategies needed to navigate the world of car loan programs for bad credit. We’ll break down the complexities, offer practical advice, and help you drive away with confidence, even when your credit score isn’t perfect.

Navigating Car Loan Programs For Bad Credit: Your Comprehensive Guide to Driving Away with Confidence

Understanding Bad Credit and Its Impact on Car Loans

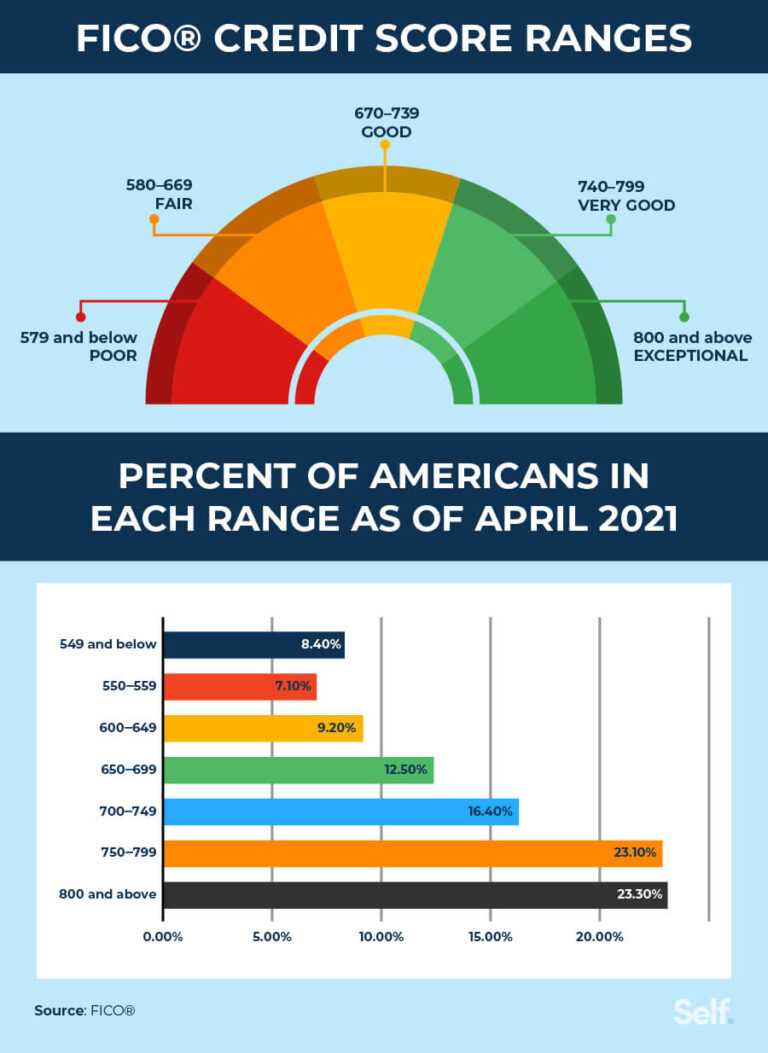

Before diving into solutions, it’s crucial to understand what "bad credit" entails and why it affects your loan application. Credit scores, like FICO or VantageScore, are numerical representations of your creditworthiness. Generally, a score below 600-620 is considered "subprime" or "bad credit" by most lenders.

This low score signals to lenders that you might be a higher risk borrower. It suggests a history of missed payments, high debt, or perhaps limited credit history altogether. Consequently, lenders become more cautious, and if they do approve your loan, it often comes with less favorable terms.

The primary impacts of bad credit on a car loan include higher interest rates and potentially larger down payment requirements. A higher interest rate means you’ll pay significantly more over the life of the loan. Furthermore, lenders might offer shorter loan terms, leading to higher monthly payments, or restrict your choices to older, less expensive vehicles.

The Reality of "Guaranteed Approval" and "No Credit Check" Loans

When searching for car loans with bad credit, you’ll inevitably encounter phrases like "guaranteed approval" or "no credit check." It’s essential to approach these with a healthy dose of skepticism. Based on my experience in the auto finance industry, truly "guaranteed approval" for a conventional loan is almost non-existent.

Lenders always assess some level of risk. While some dealerships and finance companies specialize in subprime lending and have very high approval rates, they still need to ensure you have a stable income to repay the loan. If a lender promises 100% guaranteed approval without any questions asked, it’s often a red flag indicating extremely high interest rates, hidden fees, or predatory loan terms.

Similarly, "no credit check" often points towards specific types of lenders, primarily "Buy Here, Pay Here" (BHPH) dealerships. While these dealers do offer loans without pulling your traditional credit report, they assess your ability to pay based on your income and employment history. We’ll delve deeper into BHPH options shortly, but be aware that they come with their own set of pros and cons, often including very high interest rates and limited reporting to credit bureaus.

Key Strategies for Securing a Car Loan with Bad Credit

Even with a challenging credit history, there are proactive steps you can take to significantly improve your chances of approval and secure more favorable loan terms. These strategies demonstrate to lenders that you are a responsible borrower, despite past credit issues.

1. Improve Your Credit Score (Even a Little)

While a complete credit overhaul takes time, even small improvements can make a difference. Start by obtaining a free copy of your credit report from all three major bureaus (Experian, Equifax, TransUnion) via AnnualCreditReport.com. Scrutinize these reports for any errors or inaccuracies; disputing and correcting them can sometimes boost your score.

Focus on paying down small debts, especially those with high interest rates, and try to make all your payments on time. Consistency is key here. Becoming an authorized user on a trusted family member’s credit card, provided they have excellent payment habits, can also positively impact your credit age and payment history. For more detailed steps, you might find our guide on How to Improve Your Credit Score Quickly helpful.

2. Save for a Significant Down Payment

A down payment is one of the most powerful tools in your arsenal when applying for a bad credit car loan. When you put money down, you reduce the total amount you need to borrow, which in turn lowers the risk for the lender. It also shows your commitment and financial responsibility.

Lenders are more likely to approve a loan for a lower amount, especially if they see you’ve invested your own cash. A substantial down payment can also lead to lower monthly payments and, crucially, a lower interest rate, saving you money over the life of the loan. Aim for at least 10-20% of the car’s purchase price if possible.

3. Find a Co-signer

A co-signer can be a game-changer for individuals with bad credit. A co-signer is someone with good credit who agrees to take legal responsibility for the loan if you fail to make payments. Their strong credit history essentially "backs up" your application, making you a much less risky proposition for the lender.

A good co-signer is someone with an excellent credit score, stable income, and a willingness to take on the responsibility. This is a significant ask, as any missed payments will negatively impact their credit score as well. Choose a co-signer carefully and ensure both parties fully understand the commitment involved.

4. Explore Dealerships Specializing in Bad Credit Auto Loans

Many dealerships understand the need for reliable transportation regardless of credit history. They often have "special finance" departments dedicated to helping customers with bad credit. These departments work with a network of subprime lenders who are more willing to approve loans for higher-risk borrowers.

These dealerships are experienced in structuring deals that work within the parameters set by subprime lenders. They can guide you through the process and help you find a vehicle that fits your budget and loan approval. Do your research to find reputable dealerships in your area known for their bad credit financing options.

5. Consider Credit Unions

Credit unions often offer a more personalized approach to lending compared to large banks. Because they are member-owned, they sometimes have more flexible lending criteria and may be more willing to work with individuals who have less-than-perfect credit. Their interest rates can also be more competitive.

If you are already a member of a credit union, or if you qualify for membership, it’s definitely worth inquiring about their auto loan programs. They might view your overall financial relationship and stability more favorably than just your credit score.

6. Get Pre-Approved

Seeking pre-approval is a smart move for any car buyer, but it’s particularly beneficial for those with bad credit. Pre-approval means a lender has reviewed your financial information and determined how much they are willing to lend you, along with an estimated interest rate. This process typically involves a "soft" credit inquiry, which doesn’t harm your credit score.

Having a pre-approval in hand gives you significant negotiating power at the dealership. You’ll know your budget before you even step onto the lot, allowing you to focus on the car and not just the financing. It also prevents you from getting emotionally attached to a car you can’t afford, streamlining the entire buying process.

Types of Car Loan Programs for Bad Credit

Understanding the different avenues available for bad credit auto financing is crucial. Each option has its own characteristics, benefits, and potential drawbacks.

1. Subprime Auto Loans

Subprime auto loans are specifically designed for borrowers with low credit scores (typically below 620). These loans are offered by traditional banks, credit unions, and specialized finance companies that are willing to take on higher risk. The trade-off for this accessibility is usually a higher Annual Percentage Rate (APR) compared to prime loans.

Despite the higher interest, subprime loans serve a vital purpose. They provide a pathway to car ownership for millions and, importantly, offer an opportunity to rebuild credit. By making consistent, on-time payments on a subprime auto loan, you can gradually improve your credit score, paving the way for better financial opportunities in the future.

2. Buy Here, Pay Here (BHPH) Dealerships

Buy Here, Pay Here dealerships are unique in that they act as both the car seller and the lender. Instead of arranging financing through a third-party bank, you make your payments directly to the dealership. This model often appeals to those with very poor credit or no credit history, as approvals are typically easier and quicker.

Pros of BHPH:

- Easier Approval: Often require minimal credit checks, focusing more on your income and employment stability.

- Quick Process: You can often drive away with a car the same day.

- Less Stringent Requirements: Good for those turned down by traditional lenders.

Cons of BHPH:

- Very High Interest Rates: These can be significantly higher than subprime loans, sometimes reaching the maximum allowed by state law.

- Limited Vehicle Choice: You’re restricted to the inventory available on their lot, which may be older or have higher mileage.

- Higher Prices: Vehicles often come with inflated price tags.

- May Not Report to Credit Bureaus: A common mistake to avoid is assuming all BHPH loans help rebuild credit. Many do not report your payments, meaning your on-time payments won’t improve your credit score. Always ask if they report to the major credit bureaus.

3. Online Lenders Specializing in Bad Credit

The digital age has brought forth a host of online lenders who specialize in bad credit auto financing. These platforms can be incredibly convenient, allowing you to compare offers from multiple lenders without leaving your home. Many online lenders have streamlined application processes and quick approval times.

When considering online lenders, it’s crucial to do your due diligence. Look for lenders with positive reviews, clear terms and conditions, and transparent interest rates. Ensure they are legitimate and reputable. Comparing offers from several online lenders can help you find the best possible terms for your situation.

What Lenders Look For When You Have Bad Credit

Even when dealing with bad credit, lenders are looking for specific indicators of your ability and willingness to repay the loan. Understanding these factors can help you present yourself as a more attractive borrower. Pro tips from us: prepare these documents and information in advance.

- Income Stability: Lenders want to see a steady and verifiable source of income. This demonstrates your capacity to make regular monthly payments. Be prepared to provide pay stubs, bank statements, or proof of employment.

- Debt-to-Income Ratio (DTI): Your DTI is the percentage of your gross monthly income that goes towards paying your monthly debt payments. Lenders prefer a lower DTI, as it indicates you have enough disposable income to handle a new car payment.

- Down Payment: As mentioned, a significant down payment reduces the loan amount and the lender’s risk. It shows your financial commitment and ability to save.

- Co-signer: If you have a co-signer with good credit, this significantly strengthens your application by adding an extra layer of security for the lender.

- Vehicle Choice: Lenders might be more comfortable approving a loan for a more modest, reliable vehicle rather than a high-end luxury car. Choosing a car that fits your budget and is less likely to incur expensive repairs can work in your favor.

Negotiating Your Bad Credit Car Loan

Securing a bad credit car loan doesn’t mean you should settle for the first offer. Negotiation is still a vital part of the car-buying process.

Always focus on the total price of the car, not just the monthly payment. Dealerships might try to distract you with low monthly figures that stretch over an unnecessarily long loan term, ultimately costing you more in interest. Be wary of add-ons like extended warranties, rust protection, or fabric treatments unless you’ve thoroughly researched their value and decided they are essential.

Understand the difference between the interest rate and the Annual Percentage Rate (APR). The APR includes the interest rate plus any additional fees, giving you a more accurate picture of the true cost of borrowing. If the terms offered seem too high or don’t align with your budget, don’t be afraid to walk away. There are always other options and other lenders. For further guidance on smart car buying, consider reviewing resources like the FTC’s guide on buying a car (https://www.consumer.ftc.gov/articles/0056-buying-car).

Rebuilding Your Credit Through a Car Loan

One of the most significant long-term benefits of securing a bad credit car loan is the opportunity it presents for credit rebuilding. A car loan is an installment loan, meaning you make fixed payments over a set period. By consistently making these payments on time, every single month, you establish a positive payment history.

This positive payment history is a powerful factor in improving your credit score. As your score gradually rises, you’ll gain access to better financial products, lower interest rates on future loans, and an overall healthier financial standing. View your bad credit car loan not just as a means to get a car, but as a strategic stepping stone towards financial recovery.

Common Mistakes to Avoid When Seeking a Bad Credit Car Loan

Navigating bad credit auto financing can be tricky. Being aware of common pitfalls can save you money, time, and stress.

- Applying Everywhere: Each time you apply for credit, a "hard inquiry" appears on your credit report. Too many hard inquiries in a short period can negatively impact your score. Focus on a few reputable lenders rather than applying to dozens.

- Not Knowing Your Budget: Before you even look at cars, determine how much you can truly afford for a monthly payment, insurance, fuel, and maintenance. Don’t let a salesperson push you into a vehicle beyond your means.

- Falling for "Guaranteed Approval" Scams: As discussed, be extremely cautious of promises that sound too good to be true. They often come with predatory terms.

- Ignoring the Total Cost: Focus on the total price of the vehicle and the total amount you’ll pay back over the loan term, not just the appealing monthly payment. A lower monthly payment over a longer term often means paying much more in interest.

- Not Reading the Fine Print: Always read your loan agreement thoroughly before signing. Understand all terms, conditions, fees, and penalties. If something isn’t clear, ask for clarification.

Conclusion: Your Road to Car Ownership is Clear

Securing a car loan with bad credit may seem like an uphill battle, but with the right knowledge and a proactive approach, it’s a journey you can successfully complete. Remember, your credit score is just one piece of your financial story, and it doesn’t have to define your ability to get the transportation you need.

By improving your credit, making a down payment, exploring specialized lenders, and understanding the types of programs available, you empower yourself to make informed decisions. Use this car loan as an opportunity to not only get a reliable vehicle but also to build a stronger financial future. With persistence and smart choices, you’ll soon be driving away with confidence, knowing you’ve taken control of your credit journey.