Navigating Car Loan Rates in Canada: Your Ultimate Guide to Driving a Better Deal

Navigating Car Loan Rates in Canada: Your Ultimate Guide to Driving a Better Deal Carloan.Guidemechanic.com

Embarking on the journey to purchase a vehicle in Canada is an exciting prospect. Whether it’s your first car, a family upgrade, or a reliable workhorse, the dream of new wheels often comes with a significant financial decision: securing a car loan. Understanding car loan rates in Canada isn’t just about knowing a number; it’s about unlocking significant savings, making informed choices, and ultimately, driving away with peace of mind.

Based on my extensive experience in the automotive financing landscape, many Canadians overlook the crucial details of their loan, focusing only on the monthly payment. This oversight can cost thousands of dollars over the loan’s lifetime. This comprehensive guide is designed to empower you with in-depth knowledge, practical strategies, and expert insights to navigate the complexities of Canadian car loan rates, ensuring you secure the best possible deal. Let’s dive deep into making your car ownership dream a financially savvy reality.

Navigating Car Loan Rates in Canada: Your Ultimate Guide to Driving a Better Deal

What Exactly Are Car Loan Rates and Why Are They So Important in Canada?

At its core, a car loan rate, often referred to as an interest rate, is the cost you pay to borrow money from a lender to purchase a vehicle. It’s expressed as a percentage of the principal loan amount. This percentage dictates how much extra money you’ll pay back on top of the car’s actual price.

In the Canadian context, these rates are profoundly influenced by our unique financial market, including the Bank of Canada’s benchmark rates and the competitive landscape of our financial institutions. A seemingly small difference in interest rate can translate into hundreds, or even thousands, of dollars saved or spent over the term of your loan. This is why understanding and optimizing your rate is paramount.

Consider two identical $30,000 car loans over a five-year term. One has an interest rate of 4.99%, while the other is 7.99%. The lower rate could save you over $2,500 in total interest paid. This illustrates precisely why focusing on car loan rates Canada is more than just a trivial detail; it’s a critical financial lever.

The Key Factors That Shape Your Car Loan Rates in Canada

Several dynamic elements come together to determine the interest rate you’ll be offered on a car loan. Understanding these factors is the first step towards taking control and influencing a more favorable outcome. Based on my experience, neglecting any of these can significantly impact your final rate.

1. Your Credit Score: The Ultimate Financial Report Card

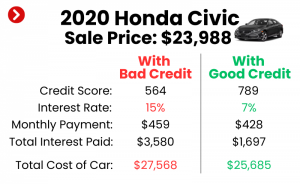

Your credit score is arguably the most influential factor in securing a competitive car loan rate. In Canada, credit bureaus like Equifax and TransUnion compile your financial history into a three-digit number, typically ranging from 300 to 900. A higher score signifies a lower risk to lenders.

Lenders use your credit score to assess your likelihood of repaying the loan. Individuals with excellent credit scores (generally 720+) are perceived as highly reliable, qualifying them for the lowest available interest rates. Conversely, a lower score suggests a higher risk, leading to higher interest rates to compensate the lender for that perceived risk.

Pro tips from us: Before you even start car shopping, check your credit score and report. This allows you to identify any errors and gives you a clear picture of where you stand. You can often get a free credit report from Canadian credit bureaus annually.

2. The Loan Term: How Long Will You Be Paying?

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 60 months, 72 months, 84 months). While a longer loan term might offer lower monthly payments, making the car seem more affordable upfront, it almost always results in paying significantly more interest over the life of the loan.

Conversely, a shorter loan term means higher monthly payments but substantially less total interest paid. Lenders also perceive shorter terms as less risky, as there’s less time for economic conditions or your financial situation to change. This often translates to a slightly better interest rate.

Common mistakes to avoid are extending your loan term simply to reduce monthly payments without considering the total cost. Always weigh the short-term affordability against the long-term financial implications.

3. Your Down Payment: Reducing Risk, Reducing Rates

A down payment is the initial sum of money you pay upfront towards the purchase price of the vehicle. Making a substantial down payment reduces the amount you need to borrow, which directly lowers the total interest you’ll pay. More importantly, it signals to lenders that you are financially responsible and committed to the purchase.

From a lender’s perspective, a larger down payment reduces their risk. If you were to default on the loan, they would have a smaller amount to recover. This reduced risk often motivates lenders to offer more attractive car loan rates Canada. A good rule of thumb is to aim for at least 10-20% of the vehicle’s purchase price as a down payment.

4. Vehicle Type: New vs. Used and Depreciation

The type of vehicle you’re buying also plays a role. New cars generally command slightly lower interest rates than used cars. This is because new cars hold their value better initially and are less prone to immediate mechanical issues, making them a more secure asset for the lender.

Used cars, while often more budget-friendly in purchase price, come with a higher perceived risk for lenders due to their age, mileage, and potential for maintenance issues. Their value also depreciates faster in the initial years. Consequently, used car loan rates can sometimes be marginally higher.

However, a well-maintained, newer used car can still qualify for excellent rates. It’s about the balance of risk and value.

5. Interest Rate Type: Fixed vs. Variable

When securing a car loan, you’ll typically encounter two types of interest rates:

- Fixed-Rate Loans: The interest rate remains constant throughout the entire loan term. Your monthly payments will never change, providing predictable budgeting. This stability is often preferred by borrowers who value certainty in their financial planning.

- Variable-Rate Loans: The interest rate can fluctuate over the loan term, usually tied to a benchmark rate like the Bank of Canada’s prime rate. If the benchmark rate increases, your interest rate and potentially your monthly payments will also rise. Conversely, if rates drop, your payments could decrease.

Based on my experience, most Canadian consumers opt for fixed-rate car loans due to the peace of mind they offer. Variable rates can be appealing when interest rates are expected to fall, but they carry inherent risk if rates unexpectedly climb.

6. Lender Type: Where You Get Your Loan Matters

The source of your car loan can significantly impact the rate you receive. In Canada, you have several options:

- Banks and Credit Unions: Traditional financial institutions often offer competitive rates, especially to their existing customers with good credit. They are generally transparent and offer a range of products.

- Dealership Financing: Dealerships frequently offer financing directly through partnerships with various banks and captive finance companies (e.g., Ford Credit, Toyota Financial Services). They can sometimes offer promotional rates, especially on new vehicles, but it’s crucial to compare these against other offers.

- Online Lenders: A growing number of online platforms specialize in car loans. They often offer quick approvals and can be competitive, especially for those with less-than-perfect credit who might find traditional banks more stringent.

Pro tips from us: Never rely solely on the dealership’s financing offer. Always shop around and get pre-approved elsewhere first. This gives you a strong negotiating position.

7. Current Economic Climate: The Bank of Canada’s Influence

The broader economic environment, particularly the Bank of Canada’s overnight lending rate, plays a pivotal role in setting prime rates across the country. When the Bank of Canada raises its rates to control inflation, borrowing costs, including car loan rates, tend to increase. Conversely, a decrease in the benchmark rate can lead to lower loan rates.

This external factor is beyond your control, but being aware of the economic trends can help you decide the best time to apply for a loan. You can track current rates and economic outlooks by checking trusted sources like the Bank of Canada’s official website for current rates.

How to Get the Best Car Loan Rates in Canada: An Expert’s Playbook

Now that you understand the factors influencing your rate, let’s turn to actionable strategies to ensure you secure the most favourable car loan rates Canada has to offer. These steps are tried and true, leading countless borrowers to significant savings.

1. Meticulously Check and Improve Your Credit Score

As discussed, your credit score is your golden ticket. Request a copy of your credit report from both Equifax and TransUnion. Review it carefully for any inaccuracies or errors that could be negatively impacting your score. Dispute any discrepancies immediately.

If your score isn’t ideal, focus on improving it before applying for a loan. This means paying all bills on time, reducing outstanding debt, and avoiding opening too many new credit accounts simultaneously. Even a small improvement can lead to a better rate.

2. Prioritize a Substantial Down Payment

Saving for a larger down payment is one of the most effective ways to lower your interest rate and reduce your total loan cost. Beyond reducing the principal borrowed, it signals strong financial health to lenders. It also helps you avoid being "upside down" on your loan (owing more than the car is worth) early in the ownership period.

Consider waiting a few extra months to save more if it means reaching a 15-20% down payment target. The long-term savings often far outweigh the short-term delay.

3. Get Pre-Approved Before Stepping into a Dealership

This is a game-changer. Obtaining pre-approval from your bank, credit union, or an online lender gives you a concrete offer and a maximum loan amount before you start shopping. This empowers you in several ways:

- You know your budget precisely.

- You walk into the dealership as a cash buyer, focusing on the car price, not just the monthly payment.

- You have a benchmark interest rate to compare against any offers from the dealership.

Based on my experience, customers with pre-approvals often secure better overall deals on the vehicle itself because they are negotiating from a position of strength.

4. Shop Around and Compare Multiple Offers

Never settle for the first loan offer you receive. Contact at least three to five different lenders – including your bank, local credit unions, and reputable online lenders. Request quotes for the same loan amount and term.

Comparing these offers side-by-side will highlight the best available rates and terms. Remember, even a half-percentage point difference can save you hundreds over the loan’s life. This comparison shopping is a non-negotiable step for savvy Canadian car buyers.

5. Understand the Fine Print and All Associated Fees

An attractive interest rate can sometimes mask hidden fees or unfavourable terms. Carefully read the entire loan agreement before signing. Look for administrative fees, early repayment penalties, or any other charges that might increase the total cost of your loan.

Pro tips from us: If anything in the contract is unclear, ask for clarification. Do not hesitate to walk away if you feel pressured or if the terms seem unfair.

6. Negotiate Your Rate

Even after getting pre-approved and comparing offers, there might still be room for negotiation, especially at the dealership. If a dealership offers you a rate higher than your pre-approval, use that pre-approval as leverage. They might be willing to match or even beat it to earn your business.

Negotiation isn’t just for the car’s price; it extends to the financing as well. Be confident and informed.

7. Consider a Shorter Loan Term (If Affordable)

While lower monthly payments from a longer term can be tempting, if your budget allows, opt for the shortest loan term possible. This significantly reduces the total interest paid and helps you build equity in your vehicle faster.

This strategy is particularly effective when interest rates are higher, as it minimizes your exposure to those elevated costs.

Understanding Different Car Loan Scenarios in Canada

The ideal car loan scenario varies significantly depending on your specific circumstances. Let’s explore a few common situations in the Canadian market.

New Car Loan Rates

New car loan rates in Canada are generally the most competitive. Lenders view new vehicles as less risky because they come with manufacturer warranties, have no prior history of accidents or maintenance issues, and typically hold their value better in the initial years. Dealerships often offer special promotional rates (e.g., 0% or 0.99%) on new vehicles through their captive finance companies, though these usually require excellent credit.

Used Car Loan Rates

Used car loan rates can be slightly higher than new car rates due to the increased perceived risk. However, the exact rate depends heavily on the age and mileage of the used vehicle, its make and model, and your creditworthiness. A certified pre-owned (CPO) vehicle from a reputable dealership might qualify for better rates than a private sale or an older, high-mileage car.

Bad Credit Car Loan Rates

Having bad credit doesn’t automatically disqualify you from getting a car loan in Canada, but it will almost certainly mean a higher interest rate. Lenders offering bad credit car loans take on greater risk, and they price that risk into the interest rate.

Strategies for bad credit include:

- Larger Down Payment: This reduces the loan amount and signals commitment.

- Co-Signer: A co-signer with good credit can significantly improve your chances and lower your rate.

- Demonstrate Stability: Show proof of stable income and employment.

- Specialized Lenders: Some lenders specialize in subprime auto loans. While rates will be higher, these loans can be a stepping stone to rebuilding credit.

Pro tips from us: If you have bad credit, focus on a reliable, affordable vehicle that you can comfortably repay. Making timely payments on this loan is an excellent way to rebuild your credit score for future, better rates.

No Credit Car Loan Rates

If you’re new to Canada or have never taken out a loan, you might have no credit history. This can be challenging but not impossible. Lenders can’t assess your risk, so they rely on other factors.

Options for no credit:

- Co-Signer: A trusted individual with good credit can co-sign.

- Secured Loan: Some lenders might offer a secured loan where the car itself acts as collateral.

- Demonstrate Income and Stability: Provide extensive documentation of stable income, employment, and residency.

- Smaller Loan Amount: Start with a less expensive vehicle to minimize the risk for the lender.

Common Mistakes to Avoid When Applying for a Car Loan in Canada

Based on my experience, many individuals make preventable errors that cost them money. Being aware of these pitfalls can save you from unnecessary financial strain.

- Not Checking Your Credit Score: As highlighted, this is foundational. Don’t go into a negotiation blind.

- Only Considering Dealership Financing: While convenient, dealerships might not always offer the best rate. Always get external quotes.

- Focusing Solely on Monthly Payments: This is perhaps the biggest mistake. A low monthly payment might seem attractive but could be achieved by extending the loan term to an excessive length, leading to significantly more interest paid overall. Always ask for the total cost of the loan.

- Extending Loan Term Too Long: While it lowers monthly payments, a very long term (e.g., 84 or 96 months) means you’ll pay more interest and might find yourself upside down on the loan.

- Ignoring Additional Fees: Be vigilant for processing fees, administrative charges, or unnecessary add-ons that can inflate the total cost.

- Applying to Too Many Lenders at Once: Each hard inquiry on your credit report can slightly ding your score. While comparison shopping within a short window (14-45 days, depending on the credit bureau) is often grouped as a single inquiry for auto loans, be mindful of excessive applications.

- Not Budgeting Beyond the Car Payment: Remember to factor in insurance, fuel, maintenance, and potential parking costs. A "cheap" monthly payment might not be so cheap when you consider all associated costs.

The Indispensable Role of a Car Loan Calculator

Before you even begin serious car shopping, a car loan calculator is your best friend. These online tools allow you to input different variables – loan amount, interest rate, and term – to instantly see how they impact your estimated monthly payment and total interest paid.

Using a calculator helps you:

- Determine Affordability: Understand what monthly payment you can realistically manage.

- Compare Scenarios: See how different interest rates or loan terms change your total cost.

- Set Expectations: Gain a realistic understanding of your financial commitment.

Pro tips from us: Experiment with various scenarios. See how increasing your down payment or shortening your loan term impacts the overall cost. This practical exercise will solidify your understanding of car loan rates Canada.

Navigating the Application Process: A Step-by-Step Guide

Once you’ve done your research and are ready to apply, follow these steps for a smooth process:

- Gather Necessary Documents: This typically includes proof of income (pay stubs, employment letter), proof of residency (utility bills), identification (driver’s license), and details of the vehicle you intend to purchase.

- Submit Applications: Apply to your chosen lenders, whether it’s your bank, a credit union, or an online platform.

- Review Offers: Carefully compare the offers you receive. Look at the interest rate, loan term, total interest paid, and any associated fees.

- Ask Questions: Don’t hesitate to ask lenders to explain any terms you don’t understand.

- Finalize the Deal: Once you’ve selected the best offer, sign the loan agreement. Ensure all the terms and conditions discussed are accurately reflected in the final document.

Pro Tips for Canadian Car Buyers: Beyond the Loan Rate

Securing a great car loan rate is a significant achievement, but a truly savvy car buyer thinks beyond just the interest.

- Consider Refinancing: If interest rates drop significantly after you’ve secured your loan, or if your credit score has improved substantially, explore refinancing your car loan. This could lead to a lower interest rate and substantial savings over the remaining term.

- Understand Your Total Budget: Beyond the car payment, factor in insurance, fuel, maintenance, and potential repairs. Use an all-encompassing budget to avoid buyer’s remorse.

- Don’t Rush the Decision: Car buying, and especially car loan decisions, should never be rushed. Take your time to research, compare, and ensure you’re comfortable with every aspect of the deal.

- Explore Certified Pre-Owned (CPO) Options: For those considering used cars, CPO programs often come with extended warranties and rigorous inspections, which can sometimes lead to slightly better financing terms than non-CPO used vehicles. This adds a layer of confidence similar to a new car purchase.

- Read Reviews of Lenders: Just as you’d research a car, research the lender. Look for reviews regarding their customer service, transparency, and overall reputation. A good rate from a problematic lender isn’t a good deal.

Conclusion: Driving Towards a Smarter Financial Future

Navigating the world of car loan rates in Canada can seem daunting, but armed with knowledge and a strategic approach, it becomes a manageable and ultimately rewarding experience. By understanding the factors that influence your rate, meticulously preparing your finances, and diligently comparing offers, you position yourself for success.

Remember, the goal isn’t just to get a car; it’s to get a car on terms that are financially sound and sustainable for you. By following the expert advice and practical strategies outlined in this comprehensive guide, you’re well on your way to securing an excellent car loan rate, saving money, and enjoying your new vehicle with complete confidence. Drive smart, Canada!

For more insights into managing your personal finances and making smart borrowing decisions, explore our other articles such as or .