Navigating Car Loan Rates in Dallas, Texas: Your Ultimate Guide to Securing the Best Deal

Navigating Car Loan Rates in Dallas, Texas: Your Ultimate Guide to Securing the Best Deal Carloan.Guidemechanic.com

Buying a car in Dallas, Texas, is an exciting prospect, whether you’re cruising down Central Expressway or exploring the vibrant neighborhoods. However, the excitement can quickly turn into apprehension when faced with the complexities of car loan rates. Understanding how these rates work and how to secure the best possible deal is paramount to making a financially sound decision.

This comprehensive guide is designed to empower you with the knowledge and strategies you need to confidently navigate the Dallas car loan market. We’ll dive deep into everything from factors influencing rates to where to find the best lenders, ensuring you drive away with a fantastic vehicle and an even better financing agreement.

Navigating Car Loan Rates in Dallas, Texas: Your Ultimate Guide to Securing the Best Deal

Decoding Car Loan Rates: The Essentials You Need to Know

At its core, a car loan rate is the cost of borrowing money to purchase a vehicle, expressed as a percentage. This percentage, often referred to as the Annual Percentage Rate (APR), is more than just the interest rate; it includes certain fees and charges associated with the loan, giving you a truer picture of the total cost.

Understanding your APR is crucial because it directly impacts your monthly payments and the total amount you’ll pay over the life of the loan. A seemingly small difference in APR can translate into hundreds, even thousands, of dollars saved or spent over several years. This is why thorough research and negotiation are non-negotiable steps in your car buying journey.

Key Factors That Influence Your Car Loan Rates

Several variables play a significant role in determining the car loan rates you’ll be offered in Dallas. Being aware of these factors allows you to prepare and position yourself for the most favorable terms.

1. Your Credit Score: The Cornerstone of Lending Decisions

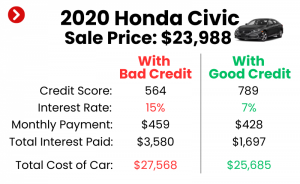

Your credit score is arguably the most influential factor in securing a competitive car loan rate. Lenders use this three-digit number to assess your creditworthiness and the likelihood of you repaying your debt. A higher credit score signals lower risk to lenders.

Individuals with excellent credit scores (typically 720+) are consistently offered the lowest interest rates, as they are perceived as highly reliable borrowers. Conversely, those with lower scores may face higher rates to compensate lenders for the increased risk. Taking steps to improve your credit score before applying for a loan can significantly impact your financial future.

2. Loan Term: Balancing Monthly Payments and Total Interest

The loan term refers to the length of time you have to repay the loan, often expressed in months (e.g., 36, 48, 60, 72 months). A longer loan term generally results in lower monthly payments, which can be attractive for budget management. However, this convenience comes at a cost.

Extending the loan term typically means paying more interest over the life of the loan. Lenders often charge a slightly higher APR for longer terms because they are taking on risk for a more extended period. It’s essential to find a balance between affordable monthly payments and minimizing the total interest paid.

3. Down Payment: Reducing Your Loan Amount and Risk

A down payment is the initial amount of money you pay upfront for the car, reducing the total amount you need to borrow. Making a substantial down payment can work wonders for your car loan rates. Lenders view a larger down payment as a sign of your commitment and financial stability.

By putting more money down, you decrease the lender’s risk exposure, as they have less capital tied up in the loan. This often translates into lower interest rates and more favorable loan terms. Based on my experience, aiming for at least a 20% down payment on a new car and 10% on a used car can significantly improve your rate offers.

4. Vehicle Type (New vs. Used): Risk and Depreciation

The type of vehicle you intend to purchase also influences your loan rate. New cars typically come with lower interest rates compared to used cars. This is primarily because new cars hold their value better initially and present less risk to the lender in case of default and repossession.

Used cars, on the other hand, have already depreciated and carry a higher perceived risk for lenders. Their value can fluctuate more, and their mechanical reliability might be less certain. Consequently, used car loan rates tend to be slightly higher to offset this increased risk.

5. Debt-to-Income (DTI) Ratio: Your Financial Capacity

Your debt-to-income (DTI) ratio is a measure of your monthly debt payments compared to your gross monthly income. Lenders use this ratio to assess your ability to take on additional debt. A lower DTI ratio indicates that you have more disposable income to cover your loan payments.

A high DTI ratio, however, suggests that you might be overextended financially, making you a riskier borrower. Lenders in Dallas and across Texas will scrutinize this ratio closely. Keeping your DTI below 36% (including your proposed car payment) is often a good benchmark for securing competitive rates.

The Dallas-Fort Worth Auto Market: What Makes it Unique

Dallas, a sprawling metropolis, boasts a robust economy and a dynamic automotive market. The sheer number of dealerships, banks, and credit unions competing for your business means that opportunities for favorable car loan rates are abundant, provided you know where to look.

The competitive landscape here can work to your advantage. Lenders are constantly vying for customers, often leading to special promotions and competitive rate offerings. This is particularly true for those with strong credit profiles.

However, the size of the market also means there’s a lot of noise. It’s easy to get overwhelmed by choices, which underscores the importance of a structured approach to your car loan search. Don’t just settle for the first offer you receive; explore the breadth of options available.

Exploring Your Car Loan Options in Dallas

The Dallas market offers a diverse array of car loan products tailored to different financial situations and vehicle preferences. Understanding these options is the first step toward making an informed decision.

New Car Loans

Designed for brand-new vehicles straight from the dealership, new car loans typically feature the lowest interest rates. Lenders often offer incentives for new car purchases, sometimes even 0% APR promotions for highly qualified buyers, though these are rare and usually come with strict conditions. The longer lifespan and higher initial value of new cars make them a less risky investment for lenders.

Used Car Loans

Used car loans are for pre-owned vehicles and generally carry slightly higher interest rates than new car loans. This is due to factors like vehicle depreciation, potential unknown maintenance history, and overall higher risk for the lender. Despite the slightly higher rates, used cars often represent significant savings over new ones, making them a popular choice for many Dallas residents.

Car Loan Refinancing

If you already have a car loan but believe you can get a better rate, refinancing might be your answer. This involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms. Many Dallas lenders specialize in refinancing, especially if your credit score has improved since your original purchase or if current market rates have dropped.

Bad Credit Car Loans in Dallas

For individuals with less-than-perfect credit, securing a car loan can be more challenging, but it’s far from impossible in Dallas. Several lenders specialize in bad credit car loans, often referred to as subprime loans. While these loans come with significantly higher interest rates to offset the increased risk, they offer an opportunity to purchase a vehicle and, more importantly, to rebuild your credit history through timely payments.

Lease vs. Buy: A Brief Consideration

While not a loan in the traditional sense, leasing is another popular way to acquire a vehicle. It involves paying to use a car for a set period (typically 2-4 years) rather than owning it. Leasing often results in lower monthly payments than buying, but you don’t build equity and have mileage restrictions. For those who enjoy driving a new car every few years, leasing can be an attractive alternative.

Where to Secure Your Car Loan in Dallas, Texas

The Dallas-Fort Worth metroplex provides a wealth of lending institutions, each with its own advantages. Shopping around among these different sources is a pro tip that cannot be overstated.

1. Banks: National Reach, Local Presence

Both national banks (like Chase, Bank of America, Wells Fargo) and regional banks have a strong presence in Dallas. They offer a wide range of auto loan products, often with competitive rates for well-qualified borrowers. Banks typically have established online application processes and numerous branch locations for in-person assistance.

Pro tip from us: If you already have an existing relationship with a bank (e.g., checking or savings account), they might offer you slightly better rates or more flexible terms as a loyal customer. It’s always worth starting your inquiry with your current financial institution.

2. Credit Unions: Member-Focused Benefits

Credit unions are non-profit financial cooperatives owned by their members, a structure that often translates into more favorable loan rates and lower fees compared to traditional banks. Dallas is home to numerous excellent credit unions, such as Dallas (Texas) Federal Credit Union, Resource One Credit Union, and Credit Union of Texas.

To qualify for a loan from a credit union, you usually need to become a member, which often involves meeting specific eligibility criteria (e.g., living or working in a certain area, belonging to an affiliated organization). Based on my experience, credit unions frequently offer some of the best car loan rates available, especially for used cars and refinancing.

3. Dealership Financing: Convenience and Captive Lenders

Dealerships often offer convenient, on-the-spot financing options through their partnerships with various banks and captive finance companies (e.g., Ford Credit, Toyota Financial Services). This can be a streamlined process, allowing you to complete the purchase and financing in one location.

While convenient, it’s crucial to approach dealership financing with caution. While they can sometimes secure competitive rates, especially for promotional offers, their primary goal is to sell cars. Always compare their offer with pre-approvals you’ve secured elsewhere. Common mistakes to avoid are accepting the first rate offered without negotiation, or feeling pressured into signing without fully understanding the terms.

4. Online Lenders: Speed and Comparison Tools

The digital age has brought forth a host of online lenders that specialize in auto loans. Companies like Capital One Auto Finance, LightStream, and Carvana (which also sells cars) offer quick online applications, instant decisions, and competitive rates.

The biggest advantage of online lenders is the ease of comparing multiple offers from the comfort of your home. This approach saves time and can help you quickly identify the most competitive rates available without visiting multiple physical locations. They are particularly useful for pre-approval processes.

Strategies for Securing the Best Car Loan Rates in Dallas

Finding the right lender is only half the battle; employing smart strategies will help you lock in the most favorable car loan rates in Dallas.

1. Boost Your Credit Score Before You Apply

As discussed, your credit score is king. Before you even start looking at cars, pull your credit report from AnnualCreditReport.com and review it for accuracy. Dispute any errors, pay down high-interest debt, and ensure all your payments are on time. Even a small bump in your score can significantly reduce your interest rate. For more insights on improving your financial standing, you might find our article on incredibly helpful.

2. Get Pre-Approved from Multiple Lenders

One of the most powerful tools in your arsenal is pre-approval. This involves applying for a loan with banks, credit unions, or online lenders before you step onto a dealership lot. Pre-approval gives you a concrete loan offer, including the interest rate and maximum loan amount, allowing you to shop for a car with confidence.

With a pre-approval in hand, you effectively become a cash buyer, shifting the negotiation power in your favor. You know what rate you qualify for, preventing dealerships from marking up the interest rate or pushing you into less favorable terms.

3. Shop Around and Compare Offers Diligently

Never settle for the first loan offer you receive. Get quotes from at least three to five different lenders – a mix of banks, credit unions, and online providers. Compare their APRs, loan terms, and any associated fees. This competitive shopping forces lenders to offer their best rates to win your business.

Remember that multiple loan inquiries within a short period (typically 14-45 days) are often grouped together by credit bureaus as a single credit pull, minimizing the impact on your score. So, shop broadly and quickly.

4. Negotiate More Than Just the Car Price

While negotiating the vehicle’s price is standard, many buyers forget they can also negotiate the loan terms. If a dealership offers financing, present them with your pre-approval offers. Ask them if they can beat or match your best rate. Often, they have access to various lenders and might be able to find a better deal to close the sale.

5. Make a Significant Down Payment

As mentioned earlier, a larger down payment directly reduces the amount you need to borrow, which can lead to lower interest rates. It also signals financial stability to lenders, making you a more attractive borrower. If possible, aim for at least 10-20% of the vehicle’s price.

6. Opt for a Shorter Loan Term if Feasible

While longer loan terms mean lower monthly payments, they also lead to more interest paid over time. If your budget allows, choose the shortest loan term you can comfortably afford. A 48-month or 60-month loan will almost always have a lower APR than a 72-month or 84-month loan.

7. Consider a Co-Signer (If Necessary)

If you have a limited credit history or a lower credit score, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate. A co-signer essentially guarantees the loan, taking on responsibility for repayment if you default. This reduces the lender’s risk.

The Car Loan Application Process: What to Expect

Once you’ve found your ideal car and a competitive loan offer, the application process is relatively straightforward. You’ll typically need to provide several documents:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Pay stubs, tax returns, or bank statements.

- Proof of Residency: Utility bills or lease agreement.

- Vehicle Information: Make, model, VIN (if applicable).

- Social Security Number.

Lenders will perform a hard credit inquiry, which might temporarily ding your credit score by a few points. However, the benefits of securing a great rate far outweigh this minor impact. Ensure you thoroughly read and understand all loan documents before signing. Pay attention to the APR, total interest paid, any fees, and the repayment schedule.

Beyond the Rate: Other Crucial Factors to Consider

While the interest rate is a major component of your car loan, it’s not the only factor that impacts the true cost of your financing. Overlooking these additional elements can lead to unexpected expenses.

1. Fees and Charges

Some lenders charge various fees, such as origination fees, documentation fees, or processing fees. While these might seem minor individually, they can add up and increase the overall cost of your loan. Always ask for a detailed breakdown of all fees included in the loan. Reputable lenders should be transparent about these charges.

2. Prepayment Penalties

A prepayment penalty is a fee charged by some lenders if you pay off your loan earlier than scheduled. While most modern auto loans do not have prepayment penalties, it’s crucial to confirm this with your lender. The ability to pay off your loan early without penalty gives you financial flexibility and can save you money on interest.

3. Lender Reputation and Customer Service

Beyond the numbers, consider the reputation of the lender and their commitment to customer service. Will they be easy to work with if issues arise? Do they have a track record of fair practices? Checking online reviews and asking for recommendations can provide valuable insights into a lender’s reliability. A positive relationship with your financial institution can make a significant difference in the long run.

4. Insurance Requirements

Lenders will typically require you to carry full coverage insurance (collision and comprehensive) on your financed vehicle until the loan is paid off. This protects their investment in case of an accident or theft. Ensure you factor the cost of this insurance into your overall budget, as it’s a mandatory ongoing expense.

Navigating Challenging Situations: Bad Credit Car Loans in Dallas

For those facing the challenge of bad credit, securing a car loan in Dallas requires a slightly different approach. While rates will undoubtedly be higher, options are available.

Based on my experience, many subprime lenders operate in the Dallas area, specializing in helping individuals with low credit scores. These lenders focus more on your current income and ability to repay rather than solely on your credit history.

Pro tips for bad credit car loans:

- Be Realistic: Expect higher interest rates and potentially a larger down payment requirement.

- Focus on Affordability: Choose a car that is truly within your budget, keeping monthly payments manageable.

- Improve Your Credit: While you’re making payments on your bad credit loan, diligently work on improving your credit score. Make all payments on time, keep credit card balances low, and avoid new debt. This will position you for refinancing at a lower rate in the future.

- Explore Buy-Here-Pay-Here Dealerships with Caution: These dealerships offer in-house financing, often for those with very poor credit. While convenient, their interest rates are typically very high, and the terms can be less favorable. Proceed with extreme caution and ensure you understand every aspect of the agreement. For more information on managing your finances, consider exploring resources like the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov.

Conclusion: Drive Smarter, Not Harder, in Dallas

Securing a car loan in Dallas, Texas, doesn’t have to be a daunting task. By understanding the factors that influence car loan rates, exploring your diverse lending options, and implementing smart shopping strategies, you can confidently navigate the market. Your credit score, down payment, and the loan term are powerful levers you can pull to significantly impact your financing terms.

Remember, the ultimate goal is to find a loan that fits comfortably into your budget, allowing you to enjoy your new vehicle without financial stress. Take your time, do your homework, and don’t be afraid to negotiate. With this comprehensive guide, you are well-equipped to secure the best car loan rates Dallas has to offer and embark on your next automotive adventure with peace of mind. Happy driving!