Navigating Car Loans: A Comprehensive Guide Beyond GE Finance’s Legacy

Navigating Car Loans: A Comprehensive Guide Beyond GE Finance’s Legacy Carloan.Guidemechanic.com

The journey to owning a car often involves securing a loan, a financial agreement that can feel complex and daunting. Many consumers, recalling a prominent name from the past, still search for "GE Finance Car Loan" hoping to find a reliable partner for their auto financing needs. While GE Capital was once a significant player in the financial services landscape, including auto lending, the market has evolved considerably.

This comprehensive guide aims to demystify the world of car loans. We’ll explore the historical context of GE Finance’s role, explain what car loans entail today, walk you through the application process, help you understand interest rates and fees, and equip you with the knowledge to make informed decisions. Our ultimate goal is to provide you with a roadmap to securing the best possible auto loan, ensuring you drive away with confidence, not confusion.

Navigating Car Loans: A Comprehensive Guide Beyond GE Finance’s Legacy

The Legacy of GE Capital in Auto Finance: A Historical Context

For many years, General Electric, through its financial services arm, GE Capital, was a colossal force in the global financial sector. Their extensive portfolio included commercial loans, leases, and yes, consumer financing, which encompassed auto loans. The brand name "GE" carried immense weight, synonymous with stability, reliability, and widespread accessibility.

This strong brand recognition meant that countless individuals and businesses turned to GE Capital for their financing needs, including car purchases. They offered competitive rates and a broad range of products, making them a go-to option for many seeking to finance a new or used vehicle. The sheer scale of their operations meant they were a familiar presence in dealerships and finance offices across the nation.

However, the financial landscape is constantly shifting. Over the past decade, General Electric embarked on a strategic pivot, divesting most of its GE Capital assets to streamline operations and refocus on its industrial core. This massive restructuring saw GE Capital exit many of its retail finance operations, including the direct provision of consumer auto loans. Therefore, while the search term "GE Finance Car Loan" remains prevalent due to past recognition, GE Capital no longer offers these types of loans directly to consumers.

Based on my experience, many people recall a positive interaction with GE Capital in the past, leading them to search for this familiar name. It’s important to understand that while the name carries a strong legacy, the actual service is no longer available from GE itself. This doesn’t mean you’re out of options; it simply means you’ll be looking at other reputable lenders who have stepped up to fill that space.

Understanding Car Loans in Today’s Market

Even without GE Finance in the picture, the fundamental concept of a car loan remains the same. A car loan is essentially an agreement where a lender provides you with a lump sum of money to purchase a vehicle, and you agree to repay that amount, plus interest, over a predetermined period. It’s a structured way to acquire a significant asset without having to pay the full price upfront.

At its core, a car loan has three main components: the principal, which is the amount of money you borrow; the interest rate, which is the cost of borrowing that money expressed as a percentage; and the loan term, which is the length of time you have to repay the loan, typically measured in months. Each of these elements plays a crucial role in determining your monthly payment and the total cost of the loan.

There are several types of car loans available, each tailored to different needs. A new car loan is specifically for financing a brand-new vehicle from a dealership. These often come with lower interest rates due to the vehicle’s higher value and lower risk of mechanical issues. Used car loans, on the other hand, are for pre-owned vehicles and may have slightly higher rates depending on the car’s age and mileage, reflecting a slightly increased risk for the lender. Finally, car loan refinancing allows you to replace your existing car loan with a new one, often to secure a lower interest rate, reduce your monthly payment, or change the loan term. This can be a smart move if your credit score has improved or if market rates have dropped since you initially financed your vehicle.

Navigating the Modern Auto Loan Landscape: Where GE Capital Used to Be

Since GE Capital is no longer a direct provider of consumer auto loans, understanding where to look for financing is paramount. The modern auto loan landscape is vibrant and competitive, populated by a diverse array of lenders, each with its own strengths and offerings. This competition ultimately benefits you, the consumer, by providing more choices and potentially better rates.

Your primary options today include traditional banks, local credit unions, captive finance companies, and a growing number of online lenders. Each category has distinct advantages. Traditional banks, for instance, offer the convenience of established relationships and a wide range of financial products. Credit unions are known for their member-focused approach, often providing competitive rates and personalized service due to their non-profit structure.

Captive finance companies are another significant player; these are financial arms directly owned by car manufacturers, such as Toyota Financial Services or Ford Credit. They often offer special promotional rates and incentives for purchasing their brand’s vehicles, which can be very attractive. Lastly, online lenders have emerged as a powerful force, providing quick approvals, streamlined digital application processes, and competitive rates, often catering to a wider range of credit profiles.

Pro tips from us: Don’t limit yourself to just one type of lender. Shop around and compare offers from at least three different sources. This approach dramatically increases your chances of finding the most favorable terms for your specific situation. Remember, the best deal isn’t always the first one you encounter.

Key Factors Lenders Consider for Car Loan Approval

When you apply for a car loan, lenders evaluate several key factors to assess your creditworthiness and the risk involved in lending you money. Understanding these elements can help you prepare your application and potentially secure better terms. It’s a comprehensive review designed to ensure you can realistically meet your repayment obligations.

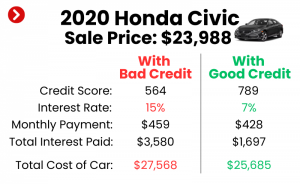

Your credit score is arguably the most critical factor. This three-digit number, generated by credit bureaus, is a snapshot of your financial reliability. A higher score indicates a lower risk to lenders, often translating into lower interest rates and more favorable loan terms. Lenders typically look for scores in the "good" to "excellent" range, but options exist for those with fair or even poor credit, albeit usually with higher interest rates.

Another crucial metric is your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. Lenders use it to determine if you have enough disposable income to comfortably take on additional debt, like a car loan. A lower DTI ratio suggests you manage your existing debt well and have more financial capacity, making you a more attractive borrower.

Lenders also want to see income stability. This typically means consistent employment and a verifiable income stream. You’ll likely need to provide proof of employment, such as pay stubs or tax returns, to demonstrate your ability to make regular payments. A steady job history reassures lenders that your income is reliable and ongoing.

While not always mandatory, a down payment can significantly improve your loan application. Putting money down upfront reduces the amount you need to borrow, which lowers your monthly payments and the total interest paid over the life of the loan. It also signals to lenders your commitment to the purchase and reduces their risk. A substantial down payment can sometimes help you qualify for better rates, especially if your credit score isn’t perfect.

Finally, the vehicle’s age and condition can impact the loan terms. Lenders view newer, lower-mileage vehicles as less risky because they are more liquid assets and typically hold their value better. Older vehicles, while still financeable, might come with shorter loan terms or higher interest rates due to increased depreciation and potential maintenance costs.

The Car Loan Application Process: A Step-by-Step Guide

Securing a car loan doesn’t have to be an intimidating ordeal. By understanding the typical application process, you can approach it with confidence and efficiency. The journey usually begins even before you set foot in a dealership, highlighting the importance of preparation.

The first, and often most overlooked, step is getting pre-approved. Pre-approval means a lender has reviewed your financial information and provisionally agreed to lend you a certain amount at a specific interest rate, subject to final verification. This step is incredibly powerful; it gives you a clear budget, transforms you into a cash buyer at the dealership, and provides leverage for negotiation. It separates your car purchase from the financing discussion, making the overall experience smoother.

Next, you’ll need to gather your documents. Lenders typically require proof of identity (driver’s license), proof of income (pay stubs, tax returns, bank statements), proof of residence (utility bill), and information about the vehicle you intend to purchase (if you’ve already chosen one). Having these readily available will expedite the application process.

Once you have your pre-approval or have chosen a lender, you’ll formally submit the application. This involves filling out a form, either online or in person, providing all the requested financial and personal details. The lender will then perform a hard inquiry on your credit report, which will temporarily lower your score by a few points.

After submission, the lender will review your application and provide an offer. This offer will detail the loan amount, interest rate, loan term, and monthly payment. It’s crucial to meticulously review all aspects of this offer, understanding every clause and condition. Don’t hesitate to ask questions if anything is unclear.

Common mistakes to avoid are rushing this review process or feeling pressured to accept the first offer you receive. Take your time, compare it with any other pre-approvals you have, and ensure it aligns with your financial goals.

Demystifying Interest Rates and Fees

Understanding the true cost of your car loan goes beyond just the monthly payment. It involves grasping the nuances of interest rates and various fees that can add up over time. Transparency in these areas is key to making a financially sound decision.

The Annual Percentage Rate (APR) is the most important figure to focus on. While the interest rate reflects the cost of borrowing money, the APR encompasses the interest rate plus any additional fees associated with the loan, expressed as a single annual percentage. This gives you a more accurate picture of the total cost of borrowing. A lower APR means a cheaper loan.

Car loans can come with either fixed or variable interest rates. A fixed-rate loan means your interest rate, and consequently your monthly payment (excluding any principal prepayments), will remain the same for the entire loan term. This provides predictability and stability. A variable-rate loan, conversely, has an interest rate that can fluctuate based on market conditions. While it might start lower, it carries the risk of increasing over time, making your payments unpredictable. For car loans, fixed rates are overwhelmingly more common and generally recommended for peace of mind.

Beyond the interest, you might encounter several common fees. An origination fee is charged by the lender for processing your loan application. Late payment fees are incurred if you miss a payment deadline. Some loans might also have an early payoff penalty, which is a fee charged if you repay your loan before the scheduled term ends. While less common in consumer auto loans today, it’s always worth checking your loan agreement.

Pro tips from us: Always ask for the full breakdown of all fees and ensure they are included in the APR calculation. Don’t be afraid to negotiate the interest rate or ask if certain fees can be waived, especially if you have excellent credit or multiple competitive offers. A slight reduction in APR can save you hundreds, even thousands, over the life of the loan.

Smart Repayment Strategies

Once your car loan is approved and you’re driving your new vehicle, the next phase is responsible repayment. Strategic repayment can not only ensure you meet your obligations but can also save you money and potentially shorten the loan term. It’s about taking control of your financial commitment.

The most fundamental aspect is understanding your monthly payments. Ensure you know the exact amount due, the due date, and how to make payments (online, mail, automatic deduction). Setting up automatic payments is highly recommended to avoid late fees and maintain a good payment history, which positively impacts your credit score.

Consider accelerated payments as a powerful strategy to save on interest and pay off your loan faster. Even making a small extra payment each month, or adding a 13th payment annually, can significantly reduce the total interest paid over the loan’s life. For example, if your monthly payment is $300, sending an extra $50 each month could shave months off your loan term and hundreds off the total cost. Every dollar of extra principal paid directly reduces the amount on which interest is calculated.

Another excellent option to consider is refinancing an existing loan. If your credit score has improved significantly since you first took out the loan, or if prevailing interest rates have dropped, you might qualify for a new loan with a lower interest rate or more favorable terms. Refinancing can lead to lower monthly payments, substantial savings on interest, or a more manageable loan term. However, always calculate the total cost of refinancing, including any new fees, to ensure it truly benefits you. Our guide on offers valuable insights into when and how to refinance effectively.

Common Mistakes to Avoid When Getting a Car Loan

Navigating the car loan process can be complex, and it’s easy to fall into common traps that can cost you time and money. Being aware of these pitfalls can help you steer clear of them and secure a more favorable deal.

One of the most frequent errors is not checking your credit score and report beforehand. Your creditworthiness is a primary determinant of your interest rate. Going into a loan application blind means you don’t know what kind of rates you realistically qualify for, putting you at a disadvantage during negotiations. Always get a free copy of your credit report and address any inaccuracies before applying. For more tips on improving your credit score, check out our article on .

Another significant mistake is focusing solely on the monthly payment. While a low monthly payment might seem attractive, it often comes at the expense of a longer loan term and a higher total interest paid. Lenders might offer extended terms (e.g., 72 or 84 months) to make the payment seem affordable, but this significantly increases the overall cost of the vehicle. Always consider the total cost of the loan, not just the monthly installment.

Ignoring the total cost of the loan is closely related to the previous point. This includes the principal, all interest, and any associated fees. A seemingly small difference in APR can translate into thousands of dollars over several years. Use online calculators to compare the total cost of different loan offers before making a decision.

Many buyers skip the pre-approval step, heading directly to the dealership to discuss financing. This puts you at a distinct disadvantage. Without a pre-approved loan in hand, you lack leverage and may feel pressured to accept the dealership’s financing offer, which might not be the most competitive. As we discussed, pre-approval empowers you as a buyer.

Finally, falling for unnecessary add-ons can inflate your loan amount. Dealerships often offer extended warranties, GAP insurance, paint protection, and other services. While some might be beneficial, many are overpriced or unnecessary. Carefully evaluate each add-on and only agree to those that genuinely provide value and fit your budget. Remember, these additions increase the principal amount you borrow and, consequently, the interest you pay.

Choosing the Right Lender: Alternatives to the GE Legacy

With GE Capital no longer in the direct consumer auto loan market, identifying the right alternative lender is crucial. The key is to understand the landscape and leverage the competition to your advantage. Each type of lender offers a unique value proposition.

Banks remain a popular choice. Large national banks offer convenience, often having existing relationships with customers, which can streamline the application process. They typically have competitive rates for borrowers with strong credit. However, their processes can sometimes be less flexible than smaller institutions.

Credit Unions are highly recommended for their customer-centric approach. As non-profit organizations, they often offer lower interest rates and more flexible terms compared to traditional banks because their profits are returned to members in the form of better rates and lower fees. Membership is usually required but is often easy to obtain.

Captive Finance Companies (e.g., Honda Financial Services, BMW Financial Services) are excellent options if you’re buying a new car of a specific brand. They frequently provide attractive promotional offers, such as 0% APR for a limited term or cash rebates, to encourage sales of their vehicles. It’s always worth checking their offers when buying a new car.

Online Lenders have revolutionized the auto finance market. Companies like LightStream, Capital One Auto Finance (online division), and others offer quick, convenient application processes, often with rapid approval times. They can be particularly competitive for a wide range of credit scores and often provide tailored solutions. Their digital-first approach means less paperwork and faster results.

Pro tips from us: Don’t settle for the first offer. Apply with at least three different lenders – a bank, a credit union, and an online lender. Compare their APRs, loan terms, and any associated fees. Read reviews and look for lenders with excellent customer service. This diligent comparison shopping is your best defense against overpaying.

The Future of Auto Finance

The auto finance industry is dynamic, constantly evolving with technological advancements and shifting consumer preferences. Understanding these trends can give you an edge in future car-buying decisions. The sector is moving towards greater efficiency, personalization, and integration.

The rise of digital lending is perhaps the most significant trend. Online platforms are making the loan application and approval process faster, more transparent, and accessible from anywhere. This trend is only expected to accelerate, with AI and machine learning playing a larger role in credit assessment and personalized loan offers. The convenience of applying for a loan from your couch is becoming the new standard.

The increasing popularity of electric vehicles (EVs) is also impacting auto finance. As more consumers opt for EVs, lenders are beginning to develop specialized loan products that consider factors like battery life, government incentives, and the unique depreciation curves of these vehicles. We may see more "green" auto loan options emerge.

Finally, expect to see more personalized finance solutions. Lenders are leveraging data analytics to offer highly customized loan products based on individual credit profiles, driving habits (telematics), and even lifestyle. This could mean more flexible payment schedules or interest rates that adjust based on how you drive your vehicle.

The landscape may look different from the days of GE Finance Car Loans, but the core principles of smart borrowing remain. The future promises even more innovative and tailored approaches to getting you behind the wheel.

Conclusion: Driving Forward with Confidence

While the familiar name of GE Finance may no longer be a direct option for your car loan needs, the world of auto financing is richer and more competitive than ever. From understanding the historical context to navigating today’s diverse lending landscape, this guide has aimed to equip you with the knowledge needed to make informed decisions.

Remember, securing the best car loan is about preparation, understanding your credit, comparing offers, and being aware of the true cost of borrowing. By taking the time to research, compare, and ask the right questions, you empower yourself to drive away with not just a new car, but also a smart financial agreement. Take control of your car buying journey, and you’ll find that navigating the complexities of auto finance can be a rewarding experience.

We encourage you to explore different lenders, leverage pre-approval, and always prioritize the total cost of the loan over just the monthly payment. Your financial future, and your new car, deserve that diligence. Share your experiences and tips in the comments below – your insights can help other readers on their car loan journey!

External Link: For more information on responsible borrowing and consumer financial protection, you can visit the Consumer Financial Protection Bureau (CFPB) website: https://www.consumerfinance.gov/