Navigating Car Loans for High-Mileage Vehicles: Your Ultimate Guide to Financing Cars Over 100k Miles

Navigating Car Loans for High-Mileage Vehicles: Your Ultimate Guide to Financing Cars Over 100k Miles Carloan.Guidemechanic.com

Buying a car can be an exciting journey, but when your budget points towards a vehicle with over 100,000 miles on the odometer, a common question arises: "Can I even get a car loan for that?" The short answer is yes, it’s absolutely possible. However, securing car loans for cars over 100k miles comes with its own unique set of challenges and considerations that prospective buyers need to understand thoroughly.

Many people assume that once a car crosses the six-figure mileage mark, it’s automatically deemed too risky for lenders. While it’s true that high mileage presents certain hurdles, it doesn’t mean the door to financing is entirely closed. This comprehensive guide is designed to demystify the process, offering you expert insights and practical strategies to help you navigate the world of high-mileage car loans, ensuring you make an informed and financially sound decision.

Navigating Car Loans for High-Mileage Vehicles: Your Ultimate Guide to Financing Cars Over 100k Miles

We’ll delve into what lenders look for, how to improve your chances of approval, and crucial tips for making a smart purchase. Our goal is to equip you with the knowledge to not just get approved, but to secure the best possible terms for your next vehicle, even if it has seen a good deal of the open road.

Understanding the Stigma: Why High Mileage Matters to Lenders

Before diving into how to get approved, it’s crucial to understand the lender’s perspective. When you apply for a car loan, lenders assess risk. A higher-mileage vehicle generally presents a higher risk profile for several reasons, which directly influence their lending decisions.

Firstly, depreciation is a major concern. Cars, especially those with significant mileage, tend to depreciate faster. If a borrower defaults on a loan, the lender needs to repossess and sell the car to recoup their losses. A rapidly depreciating asset means a greater potential loss for the lender.

Secondly, reliability is a key factor. A car with over 100,000 miles is statistically more likely to require significant repairs compared to a newer, lower-mileage vehicle. These potential repair costs could strain the borrower’s finances, making it harder for them to keep up with loan payments. Lenders factor this increased likelihood of mechanical issues into their risk assessment.

Finally, the resale value of high-mileage cars is generally lower. Should the lender need to repossess the vehicle, they want to be confident they can sell it quickly and for a decent price to cover the outstanding loan balance. A car with a substantial amount of miles often has a smaller market of potential buyers, making it harder to liquidate.

Is It Even Possible? The Good News About Financing High-Mileage Cars

Despite the challenges outlined above, the good news is that securing car loans for cars over 100k miles is indeed possible. The market for used cars is vast, and many reliable vehicles can easily exceed 100,000 miles and still have plenty of life left in them. Lenders understand this reality and have adapted their criteria to accommodate these scenarios.

The key is to present yourself and the vehicle as low-risk as possible. Lenders are looking for indicators of financial stability from you and mechanical soundness from the car. It’s a balancing act where your creditworthiness and the car’s condition play equally important roles in the approval process.

Based on my experience in the automotive finance industry, many lenders are open to financing older vehicles, provided certain conditions are met. They often have specific programs or adjusted terms for these types of loans, acknowledging that not every buyer needs or can afford a brand-new car. The market for affordable, reliable transportation is significant, and lenders want to serve that need responsibly.

Key Factors Lenders Consider When Approving Loans for Cars Over 100k Miles

When you apply for a loan for a high-mileage vehicle, lenders will scrutinize several aspects of both the car and your financial profile. Understanding these factors can help you prepare a stronger application.

Vehicle Age vs. Mileage: The Often-Overlooked Distinction

While 100,000 miles is a significant number, lenders often look at the age of the vehicle in conjunction with its mileage. A 5-year-old car with 100,000 miles (20,000 miles/year) might be viewed differently than a 10-year-old car with 100,000 miles (10,000 miles/year). The younger car, despite its higher mileage, might be seen as less aged and potentially better maintained.

A newer car, even with higher mileage, often benefits from more modern safety features and better engineering. This can sometimes make it a more attractive lending proposition than a much older car with the same or even slightly lower mileage. Lenders often have cut-off points for vehicle age, regardless of mileage, such as not financing cars older than 10-12 years.

Vehicle Condition: More Than Just the Odometer Reading

The actual physical and mechanical condition of the car is paramount. A well-maintained vehicle with 120,000 miles is far more appealing to a lender than a neglected one with 80,000 miles. Lenders want to see evidence that the car has been cared for.

This includes a clean exterior, a well-kept interior, and most importantly, a robust service history. A pre-purchase inspection by an independent mechanic is often highly recommended, as it provides an objective assessment of the car’s health.

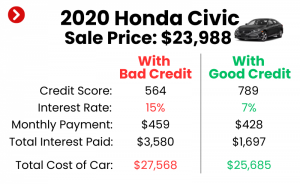

Borrower’s Credit Score: Your Ultimate Trump Card

Your personal credit score is arguably the most critical factor. A strong credit score (typically 670 or higher) demonstrates to lenders that you are a responsible borrower with a history of making timely payments. This significantly mitigates the perceived risk associated with a high-mileage vehicle.

Even if the car itself is considered high-risk, a stellar credit score can often sway a lender in your favor. It tells them that you are reliable, even if the car’s future reliability is a question mark. Conversely, a low credit score combined with a high-mileage car makes for a very challenging loan application.

Down Payment: Reducing Lender Risk

Offering a substantial down payment significantly improves your chances of approval and can lead to better interest rates. A larger down payment reduces the amount of money you need to borrow, thereby decreasing the lender’s exposure to risk. It also shows your commitment to the purchase.

Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price as a down payment when seeking car loans for cars over 100k miles. This not only makes your application more attractive but also reduces your monthly payments and the total interest paid over the life of the loan.

Loan Term: Shorter is Often Sweeter

Lenders generally prefer shorter loan terms for high-mileage vehicles. A 36-month or 48-month loan term is often more appealing than a 60-month or 72-month term. This is because a shorter term means the loan is paid off faster, before the vehicle potentially experiences major mechanical failures or depreciates too much.

While a shorter term means higher monthly payments, it reduces the overall interest you’ll pay and minimizes the time you’re "underwater" on the loan (owing more than the car is worth). Be realistic about what monthly payment you can comfortably afford within a shorter repayment period.

Interest Rates: Expect Higher, But Understand Why

It’s common for car loans for cars over 100k miles to come with higher interest rates compared to loans for newer, lower-mileage vehicles. This is directly tied to the increased risk lenders perceive. The higher interest rate compensates the lender for taking on that additional risk.

Don’t be discouraged by a slightly higher rate, but do compare offers from multiple lenders to ensure you’re getting a competitive rate for your specific situation. Focus on the total cost of the loan over its term, not just the monthly payment.

Debt-to-Income Ratio

Lenders will also look at your debt-to-income (DTI) ratio. This is a measure of how much of your monthly income goes towards debt payments. A low DTI indicates that you have plenty of disposable income to cover new loan payments, making you a less risky borrower.

A high DTI, on the other hand, suggests that your finances are already stretched thin, and adding another loan payment could make it difficult for you to meet your obligations. Aim to keep your DTI below 36% for the best chances of approval.

Types of Lenders Willing to Finance High-Mileage Vehicles

Not all lenders are created equal when it comes to financing older, higher-mileage cars. Knowing where to look can save you significant time and frustration.

Traditional Banks

Major banks can offer loans for high-mileage cars, but they often have the strictest criteria. They typically prefer newer vehicles with lower mileage and borrowers with excellent credit scores. If you have a long-standing relationship with your bank and an impeccable credit history, they might be an option.

However, their interest rates might not always be the most competitive for this specific niche. It’s always worth checking, but keep your expectations realistic.

Credit Unions

Credit unions are often a fantastic option for car loans for cars over 100k miles. As member-owned institutions, they are typically more flexible and willing to work with individuals who might not fit the strict criteria of traditional banks. They often offer competitive interest rates and may have more lenient age or mileage restrictions on vehicles.

Becoming a member is usually straightforward, and the personalized service can be a huge advantage. They often look beyond just the numbers and consider your overall financial picture.

Online Lenders

The rise of online lenders has created more options for all types of borrowers. Many online platforms specialize in various credit profiles, including those seeking loans for older vehicles. They often have streamlined application processes and can provide quick decisions.

Some online lenders specifically cater to borrowers with less-than-perfect credit or those looking to finance non-traditional vehicles. Always read reviews and verify the legitimacy of online lenders before sharing your personal information.

Dealership Financing

Many dealerships offer in-house financing or work with a network of lenders. This can be convenient, as you can often complete the purchase and financing in one place. Dealerships might have access to lenders who are more willing to finance high-mileage vehicles, especially if they are selling them.

However, be cautious. Dealership financing can sometimes come with higher interest rates, especially if you’re not pre-approved elsewhere. Always compare their offer with any pre-approvals you’ve secured.

Buy Here, Pay Here (BHPH) Dealerships

Buy Here, Pay Here dealerships directly finance the cars they sell, often targeting buyers with poor credit or those who can’t get approved elsewhere. While they might be a last resort for car loans for cars over 100k miles, they typically charge very high interest rates and often have unfavorable terms.

Pro tips from us: Exhaust all other options before considering a BHPH dealership. The cost of borrowing can be exorbitant, and you might find yourself in a financially difficult situation.

For more on choosing the right lender, check out our guide on .

Preparing for Your High-Mileage Car Loan Application

Preparation is key to a successful loan application, especially when dealing with high-mileage vehicles. A well-prepared application signals responsibility and seriousness to lenders.

Pre-Approval vs. Application

Before you even step onto a dealership lot, consider getting pre-approved for a loan. Pre-approval involves a soft credit pull (which doesn’t harm your score) and gives you a clear idea of how much you can borrow and at what interest rate. This empowers you as a buyer, allowing you to negotiate with confidence, knowing your financing is already in place.

Common mistakes to avoid are applying for loans only after finding the car you want. This puts you at a disadvantage and can rush you into less favorable terms.

Gathering Documents

Have all your necessary documents ready. This typically includes:

- Proof of identity (driver’s license, passport)

- Proof of residence (utility bill, lease agreement)

- Proof of income (pay stubs, tax returns, bank statements)

- Social Security Number

- Vehicle information (VIN, mileage, make, model, year)

Being organized shows you’re a responsible individual, which subtly influences a lender’s perception.

Checking Your Credit Score and Report

Before applying, obtain a free copy of your credit report from all three major bureaus (Equifax, Experian, TransUnion) and check your credit score. Look for any errors or discrepancies that could negatively impact your score and dispute them immediately.

Knowing your score allows you to target lenders who work with your credit tier and gives you a realistic expectation of the interest rates you might be offered. It’s also crucial for understanding where you stand.

Getting the Car Inspected (Pre-Purchase Inspection)

For any high-mileage vehicle, a pre-purchase inspection (PPI) by an independent, certified mechanic is non-negotiable. This inspection can uncover hidden issues that might not be apparent during a test drive. A clean PPI report can be a powerful tool when applying for a loan, as it reassures the lender about the car’s current condition.

It also gives you leverage in price negotiation if any minor issues are found. Remember, a PPI is an investment that can save you thousands down the road.

Service Records: A Golden Ticket

If the seller has meticulous service records, these are invaluable. A complete maintenance history shows that the car has been regularly serviced and cared for, which significantly reduces the perceived risk for lenders. It proves that the high mileage is a result of consistent driving, not neglect.

Keep these records organized and readily available for the lender to review. They can be the deciding factor in securing approval for car loans for cars over 100k miles.

Strategies to Improve Your Chances of Approval and Get Better Rates

Even if you’re aiming for a high-mileage car, there are proactive steps you can take to make your loan application more appealing and secure more favorable terms.

Boost Your Credit Score

If time permits, work on improving your credit score. Pay down existing debts, make all payments on time, and avoid opening new credit accounts. Even a slight improvement in your score can translate into significantly better interest rates.

Small changes can make a big difference over the long term, impacting not just your car loan but your overall financial health.

Save for a Larger Down Payment

As mentioned, a larger down payment reduces the amount you need to borrow and lowers the lender’s risk. If you can save up more than the typical 10-20%, you’ll present an even stronger application. This is especially true when seeking car loans for cars over 100k miles, where every advantage helps.

Consider if waiting a few extra months to save more could result in thousands of dollars saved in interest over the life of the loan.

Consider a Co-Signer

If your credit score isn’t ideal, or if you’re struggling to get approved, a co-signer with excellent credit can dramatically improve your chances. The co-signer essentially guarantees the loan, taking on the responsibility if you default.

However, both parties must understand the implications. The loan will appear on both credit reports, and the co-signer is legally obligated to pay if you cannot.

Look for a Newer High-Mileage Car

This might sound counterintuitive, but a newer car with high mileage (e.g., a 3-year-old car with 100,000 miles) can sometimes be a better bet than an older car with the same or even less mileage (e.g., a 10-year-old car with 80,000 miles). Newer cars often have more modern safety features, better fuel efficiency, and potentially longer remaining lifespan for major components.

Lenders often have age limits, so a younger car, even with higher mileage, might fall within their acceptable parameters.

Shop Around for Rates

Never settle for the first loan offer you receive. Apply to multiple lenders (banks, credit unions, online lenders) within a short window (typically 14-45 days, depending on the credit bureau) to minimize the impact on your credit score. This allows you to compare offers and choose the one with the best interest rate and terms.

This competitive shopping is crucial, especially for car loans for cars over 100k miles, where rates can vary significantly.

Be Realistic About the Car’s Value

Research the market value of the specific high-mileage car you’re interested in using resources like Kelley Blue Book (KBB) or Edmunds. Lenders will not finance a car for more than its perceived market value. Being realistic about the car’s worth ensures you’re not overpaying and helps align your expectations with the lender’s appraisal.

Before you commit, ensure you’re getting the best deal by reading our tips on .

Understanding the Costs: Beyond the Monthly Payment

When budgeting for a high-mileage car, it’s vital to look beyond just the monthly loan payment. Several other costs can significantly impact your overall financial picture.

Higher Interest Rates

As discussed, expect higher interest rates for car loans for cars over 100k miles. This means a larger portion of your monthly payment will go towards interest, especially in the early stages of the loan. Factor this into your long-term budget.

A higher interest rate can add hundreds or even thousands of dollars to the total cost of the car over the loan term.

Potential for More Maintenance Costs

This is perhaps the most critical consideration for high-mileage vehicles. While a pre-purchase inspection helps, older cars are simply more prone to needing repairs. Budgeting for unexpected maintenance is not just wise; it’s essential.

Pro tips from us: Set aside a dedicated "car repair fund" for your high-mileage vehicle. Aim for at least $50-$100 per month, even if you don’t use it immediately.

Insurance Considerations

The age and mileage of a car can also influence insurance premiums. While older cars generally have lower collision and comprehensive costs, some insurers might view them as higher risk for breakdowns, potentially affecting roadside assistance or rental car coverage options.

Always get an insurance quote for the specific vehicle before finalizing your purchase to avoid any surprises.

Gap Insurance: Is It Worth It for an Older Car?

Gap insurance covers the difference between what you owe on your loan and the car’s actual cash value if it’s totaled or stolen. For newer cars, it’s often recommended, as depreciation can quickly make you "underwater."

For high-mileage vehicles, the decision is trickier. The car’s value is already significantly depreciated. If your down payment was substantial and the loan amount is low, gap insurance might not be necessary, as the gap between what you owe and what the car is worth could be minimal or non-existent. Evaluate this based on your specific loan amount and the car’s market value.

Alternatives to a Traditional Car Loan for High-Mileage Vehicles

If securing a traditional car loan for cars over 100k miles proves too difficult or too expensive, there are other avenues to consider.

Personal Loans

An unsecured personal loan can be an option. Unlike a car loan, a personal loan is not tied to the vehicle as collateral. This means the lender takes on more risk, which often translates to higher interest rates than a secured auto loan.

However, if you have excellent credit, you might qualify for a personal loan with a reasonable rate, giving you the flexibility to buy any car you want, regardless of mileage or age.

Saving Up and Paying Cash

The most financially sound option, if possible, is to save up and pay cash for the vehicle. This eliminates interest payments entirely, reduces your monthly financial obligations, and allows you to own the car outright from day one.

While it requires patience, paying cash frees up your budget and gives you complete control over your asset.

Refinancing (Later, If Conditions Improve)

If you initially secure a loan with less favorable terms due to a high-mileage vehicle or your credit situation, you might be able to refinance it later. If your credit score improves, or if the car proves to be exceptionally reliable, you could qualify for a better interest rate and lower monthly payments down the line.

Refinancing can be a smart strategy to incrementally improve your loan terms over time.

Making a Smart Purchase: What to Look for in a High-Mileage Car

Beyond the financing, making a wise choice about the car itself is paramount when buying a high-mileage vehicle. Your loan is only as good as the asset it finances.

Reliable Makes and Models

Some car brands and models are renowned for their longevity and ability to rack up high mileage without major issues. Research vehicles known for their reliability, such as certain Honda, Toyota, or Subaru models. These cars often hold their value better and are less likely to incur significant repair costs.

A quick online search for "most reliable cars over 100k miles" can provide valuable insights. For a deeper dive into reliable high-mileage vehicles, consider resources like Consumer Reports or Kelley Blue Book.

Maintenance History is Gold

Always prioritize cars with a complete and verifiable maintenance history. This shows that the previous owner invested in preventative care, which is crucial for a vehicle’s longevity. Records of oil changes, fluid flushes, timing belt replacements, and other major services are indicators of a well-cared-for car.

Independent Inspection

Reiterating this point because it’s that important: always get a pre-purchase inspection from a trusted, independent mechanic. This unbiased assessment can uncover potential problems and give you peace of mind before committing to the purchase and the loan.

Test Drive Thoroughly

Don’t rush the test drive. Drive the car on various road types (city, highway) and at different speeds. Listen for unusual noises, feel for vibrations, and test all features (AC, radio, power windows). Pay attention to how the transmission shifts and how the brakes feel.

A comprehensive test drive can reveal many things about the car’s condition that might not be immediately obvious.

Conclusion: Driving Forward with Confidence

Securing car loans for cars over 100k miles is a journey that requires diligence, preparation, and a strategic approach. While lenders view high-mileage vehicles as inherently riskier, it is far from an impossible feat. By understanding the factors lenders consider, preparing a strong application, and exploring all your financing options, you significantly increase your chances of approval.

Remember, your creditworthiness, the car’s condition, and your financial planning are the pillars of a successful high-mileage car loan. Don’t let the odometer intimidate you; with the right information and a bit of effort, you can confidently drive away in a reliable, affordable vehicle that meets your needs. Embrace the challenge, be proactive, and you’ll find that a high-mileage car can be a smart and economical choice for years to come.