Navigating Car Loans in Tucson, AZ: Your Ultimate Guide to Smart Auto Financing

Navigating Car Loans in Tucson, AZ: Your Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

Securing a car loan is often the gateway to owning your dream vehicle, and for residents of the Old Pueblo, understanding the nuances of car loans in Tucson, AZ is crucial. The vibrant city of Tucson, with its unique blend of urban charm and desert landscapes, offers a diverse automotive market. Whether you’re a first-time buyer, looking to upgrade, or seeking to refinance, finding the right auto financing can feel like a complex journey.

This comprehensive guide is designed to demystify the process of obtaining car loans in Tucson, AZ. We’ll delve deep into everything you need to know, from understanding different loan types and finding the best lenders to navigating the application process and avoiding common pitfalls. Our goal is to empower you with the knowledge to make informed decisions, ensuring you drive away with not just a great car, but also a smart financial deal. Let’s explore the world of auto financing in Tucson together.

Navigating Car Loans in Tucson, AZ: Your Ultimate Guide to Smart Auto Financing

Understanding the Landscape of Car Loans in Tucson, AZ

Tucson’s automotive market is dynamic, reflecting the city’s growth and diverse population. From bustling dealerships along the Auto Mall to local credit unions deeply embedded in the community, options for auto financing in Tucson are plentiful. However, this abundance can sometimes lead to confusion.

A car loan is essentially an agreement where a lender provides you with funds to purchase a vehicle, and you agree to repay that amount, plus interest, over a set period. This repayment structure is typically broken down into monthly installments. The key elements of any car loan include the principal amount (the money borrowed), the interest rate (the cost of borrowing), and the loan term (the duration of repayment).

Why Tucson’s Market Matters

The local economy, interest rate trends, and even the prevalence of certain car types (like those suited for Arizona’s climate) can subtly influence the availability and terms of car loans Tucson AZ. Local lenders, for instance, often have a better understanding of the community’s financial needs and may offer more personalized services or flexible terms compared to larger national institutions. This local insight can be a significant advantage when you’re shopping for the best financing deal.

Types of Car Loans Available to Tucson Residents

The world of auto financing isn’t one-size-fits-all. Different situations call for different types of loans. Understanding these distinctions is your first step towards choosing the right path for your next vehicle purchase in Tucson.

New Car Loans

When you’re eyeing a brand-new vehicle, you’ll typically apply for a new car loan. These loans are often considered less risky by lenders because new cars generally hold their value better initially and come with manufacturer warranties. This reduced risk often translates into lower interest rates for qualified borrowers.

New car loans usually feature competitive rates and longer repayment terms, which can lead to lower monthly payments. However, it’s crucial to remember that a longer term also means you’ll pay more interest over the life of the loan. Always consider the total cost, not just the monthly payment, when evaluating new car loan offers.

Used Car Loans

Used car loans in Tucson are a popular choice, given the excellent value proposition that pre-owned vehicles often offer. While the interest rates for used car loans might be slightly higher than new car loans due to perceived higher risk (older cars can have more unknown variables), they are still very accessible. The exact rate will depend heavily on the vehicle’s age, mileage, and condition, as well as your personal creditworthiness.

When considering a used car loan, pay close attention to the vehicle’s history report. A well-maintained used car can be a fantastic investment, and many reputable dealerships in Tucson offer certified pre-owned vehicles that come with their own warranties, bridging the gap between new and used car confidence.

Refinancing Car Loans

Perhaps you already have a car loan but are looking for better terms. This is where refinance car loan Tucson options come into play. Refinancing involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate or with more favorable terms. This can be a smart move if your credit score has improved since you first took out the loan, or if interest rates have dropped.

Based on my experience, many people overlook the opportunity to refinance. It can significantly reduce your monthly payments or the total amount of interest you’ll pay over time. It’s always worth reviewing your current loan periodically, especially if you’ve made consistent payments and your financial situation has strengthened.

Lease Agreements

While not strictly a "loan," leasing is another common way to acquire a vehicle. With a lease, you essentially rent the car for a set period, making monthly payments without owning the vehicle. At the end of the lease term, you typically return the car, or you might have the option to purchase it.

Leasing can offer lower monthly payments compared to buying, and you often get to drive a new car more frequently. However, you don’t build equity, and there are mileage restrictions and potential wear-and-tear charges. It’s a different financial commitment entirely, so weigh your priorities carefully between ownership and flexibility.

Where to Find Car Loans in Tucson, AZ

Once you understand the types of loans, the next crucial step is knowing where to look. Tucson offers a variety of lending institutions, each with its own advantages. Shopping around is key to finding the best car loans Tucson AZ.

Banks (Local & National Branches)

Both large national banks and smaller local banks operate in Tucson and offer auto loans. National banks often have a wide range of products and competitive rates, especially for borrowers with excellent credit. They provide convenience through extensive branch networks and online banking platforms.

Local banks, on the other hand, might offer more personalized service and may be more flexible with borrowers who have a strong local banking relationship. It’s always a good idea to check with your current bank first, as they may offer preferred rates or streamlined processes for existing customers.

Credit Unions

For many Tucson residents, credit unions are an excellent option for car loans. These member-owned financial cooperatives often boast some of the lowest interest rates because they operate on a not-for-profit basis, passing savings back to their members. Tucson has several reputable credit unions, such as Hughes Federal Credit Union or Pima Federal Credit Union, which are well-regarded for their auto loan offerings.

Pro tips from us: Don’t dismiss credit unions just because you’re not a member yet. Joining is often easy, requiring just a small deposit into a savings account, and the potential savings on your car loan interest can be substantial. Their focus on member satisfaction often translates to better customer service and more flexible loan terms.

Dealership Financing

Most Tucson car dealerships offer on-site financing options. This can be incredibly convenient, as you can often complete the entire car-buying and financing process in one place. Dealerships work with multiple lenders (banks, credit unions, and their own captive finance companies) to secure financing for their customers.

While convenient, it’s essential to be prepared. Dealerships sometimes mark up interest rates to earn a profit, so having a pre-approved loan offer from an external lender can give you significant leverage. This allows you to compare their offers directly and negotiate for the best possible rate.

Online Lenders

The digital age has brought a new wave of online-only lenders that specialize in auto financing. Companies like LightStream, Capital One Auto Finance, or Carvana Financing offer streamlined online application processes and often provide quick approval decisions. They can be a great option for comparing rates from multiple lenders without leaving your home.

Online lenders are particularly useful for those who prefer a completely digital experience or want to cast a wide net for the best rates. However, always ensure you’re dealing with a reputable lender by checking reviews and looking for transparent terms and conditions.

The Car Loan Application Process: Your Step-by-Step Guide

Navigating the application for car loans in Tucson, AZ can seem daunting, but breaking it down into manageable steps makes it much simpler. Being prepared and organized will significantly improve your chances of securing a favorable loan.

Step 1: Check Your Credit Score and Report

Before you even start looking at cars, take the time to understand your financial standing. Your credit score is arguably the most significant factor lenders consider when determining your interest rate and loan eligibility. A higher score typically means a lower interest rate.

Access your free credit reports from the three major bureaus (Experian, Equifax, TransUnion) annually. Review them carefully for any errors that could negatively impact your score. If you find discrepancies, dispute them immediately. For more insights on managing your credit, check out our guide on .

Step 2: Determine Your Budget and Down Payment

Knowing what you can truly afford is paramount. Consider not just the monthly loan payment, but also insurance, maintenance, fuel, and registration costs. A significant down payment can lower your monthly payments, reduce the total interest paid, and even help you secure a better interest rate, especially for bad credit car loans Tucson.

Aim for at least 10-20% of the vehicle’s purchase price as a down payment if possible. This shows lenders your commitment and reduces their risk.

Step 3: Gather Necessary Documents

Lenders will require various documents to verify your identity, income, and financial stability. Having these ready in advance can expedite the application process.

Typically, you’ll need:

- Proof of identity (driver’s license, passport)

- Proof of residence (utility bill, lease agreement)

- Proof of income (pay stubs, tax returns, bank statements)

- Social Security number

- Information about the vehicle you intend to purchase (if known)

Step 4: Get Pre-Approved for a Loan

This is a pro tip from us that can save you time and money. Getting pre-approved means a lender reviews your financial information and tentatively approves you for a loan up to a certain amount, at a specific interest rate, before you even choose a car. This offer is usually valid for a set period (e.g., 30-60 days).

Pre-approval offers several benefits:

- It clarifies your budget, so you know exactly how much car you can afford.

- It turns you into a cash buyer at the dealership, giving you stronger negotiating power on the car’s price.

- It allows you to compare the pre-approved rate with any financing offers from the dealership, ensuring you get the best deal.

Step 5: Compare Offers and Choose the Best Loan

Once you have a pre-approval in hand and perhaps a few offers from different lenders, compare them meticulously. Don’t just look at the monthly payment.

Key factors to compare include:

- Interest Rate (APR): This is the true cost of borrowing.

- Loan Term: Shorter terms mean higher monthly payments but less interest paid overall.

- Fees: Look out for origination fees, application fees, or prepayment penalties.

- Total Cost: Calculate the total amount you’ll pay over the life of the loan.

Key Factors Affecting Your Car Loan in Tucson

Several elements come into play when lenders evaluate your application for car loans in Tucson, AZ. Understanding these factors can help you improve your chances of approval and secure more favorable terms.

Credit Score

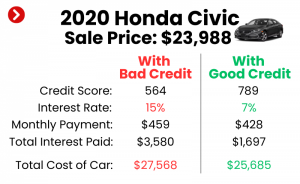

As mentioned, your credit score is paramount. It reflects your creditworthiness and your history of managing debt. Lenders use it to assess the risk of lending to you. Generally, a score of 660 and above is considered good for auto loans, while scores below 600 might fall into the subprime category, leading to higher interest rates.

Maintaining a good credit history, paying bills on time, and keeping credit utilization low are crucial for securing low interest car loans Tucson.

Down Payment Amount

A larger down payment signals to lenders that you are serious about the purchase and have a vested interest in the vehicle. It reduces the amount you need to borrow, which lowers the lender’s risk. This can be particularly impactful for those seeking bad credit car loans Tucson, as it can offset some of the perceived risk associated with a lower credit score.

Loan Term

The loan term is the length of time you have to repay the loan, typically ranging from 36 to 84 months. A shorter loan term means higher monthly payments but less interest paid over the life of the loan. Conversely, a longer loan term reduces your monthly payments, making the car more "affordable" on a month-to-month basis, but significantly increases the total interest you’ll pay.

Carefully consider your financial situation and find a balance between manageable monthly payments and the total cost of the loan.

Interest Rate (APR)

The Annual Percentage Rate (APR) is the most critical figure to understand. It represents the total cost of your loan annually, including interest and any fees. Even a small difference in APR can lead to thousands of dollars in savings or extra costs over the loan’s term.

Your credit score, the loan term, the down payment, and even the type of vehicle (new vs. used) all influence the APR you’re offered. Shopping around for the best APR is the single most effective way to save money on your car loan.

Debt-to-Income Ratio (DTI)

Lenders also look at your debt-to-income ratio, which compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have more disposable income to cover your new car payments, making you a less risky borrower. Most lenders prefer a DTI of 40% or less.

Navigating Car Loans with Less-Than-Perfect Credit in Tucson, AZ

Having a less-than-stellar credit score doesn’t mean you can’t get a car loan in Tucson. It simply means the process might require a bit more strategic planning and awareness. Bad credit car loans Tucson are available, but they often come with higher interest rates.

Understanding Subprime Lending

Lenders categorize borrowers based on credit scores. Those with scores typically below 600 are considered "subprime." Subprime lenders specialize in offering loans to these individuals, understanding they carry a higher risk. While the interest rates will be higher, these loans can be a vital stepping stone to rebuilding credit.

It’s crucial to understand that higher interest rates mean you’ll pay significantly more over the life of the loan. Therefore, exploring strategies to improve your credit before applying, or making a larger down payment, becomes even more important.

Strategies for Approval with Bad Credit

- Larger Down Payment: As discussed, a substantial down payment reduces the loan amount and the lender’s risk, making you a more attractive borrower.

- Co-signer: If you have a trusted friend or family member with good credit willing to co-sign, it can significantly improve your chances of approval and secure a better interest rate. The co-signer is equally responsible for the loan, so ensure they understand this commitment.

- Secured Loan: Some lenders might offer a secured loan, where another asset (like savings) acts as collateral. This is less common for auto loans but can be an option.

- Buy Here, Pay Here Dealerships: Some Tucson car dealerships offer "buy here, pay here" financing, where the dealership itself is the lender. While they cater to those with bad credit, these loans often come with very high interest rates and may not report to all credit bureaus, limiting your ability to build credit. Exercise extreme caution and compare all options before considering this route.

- Focus on Building Credit First: If possible, take some time to improve your credit score before applying. Even a small improvement can make a difference in your interest rate.

Common Mistakes to Avoid with Bad Credit Car Loans

- Focusing Only on Monthly Payments: High interest rates can lead to a very high total cost, even if monthly payments seem manageable. Always look at the total amount you’ll pay.

- Ignoring the APR: This is the true cost of borrowing. Don’t let a low monthly payment distract you from a sky-high APR.

- Accepting the First Offer: Even with bad credit, it’s essential to shop around and compare offers from multiple lenders. You might be surprised by the variations.

Pro Tips for Securing the Best Car Loan in Tucson

Based on my experience helping countless individuals navigate auto financing, here are some invaluable pro tips from us to ensure you secure the best possible car loans in Tucson, AZ.

1. Shop Around Aggressively

This cannot be stressed enough. Never settle for the first loan offer you receive, whether it’s from a bank, credit union, or dealership. Contact at least three to five different lenders and compare their rates and terms. The difference of even one percentage point on your interest rate can save you hundreds, if not thousands, of dollars over the life of the loan.

Remember that most credit inquiries for auto loans made within a short period (typically 14-45 days, depending on the credit bureau) are treated as a single inquiry, minimizing the impact on your credit score. So, shop diligently within that window.

2. Get Pre-Approved Before Visiting the Dealership

As previously mentioned, walking into a dealership with a pre-approval from your bank or credit union gives you immense negotiating power. You know your maximum loan amount and interest rate, allowing you to focus solely on negotiating the vehicle’s price, rather than getting caught up in the financing side of the deal.

It sets a benchmark for the dealership. If they can beat your pre-approved rate, great! If not, you have a solid backup.

3. Negotiate More Than Just the Monthly Payment

Dealerships often try to focus buyers on the "affordable" monthly payment. While important, this can be misleading. A low monthly payment might be achieved by extending the loan term significantly, leading to a much higher total cost.

Always negotiate the total purchase price of the vehicle first, then discuss the interest rate, and finally, consider the loan term and monthly payment. Understanding the total cost of ownership is crucial.

4. Read the Fine Print – Every Single Word

Loan documents can be lengthy and filled with jargon, but it’s your responsibility to understand every clause. Pay close attention to:

- Prepayment Penalties: Some loans charge a fee if you pay off the loan early.

- Late Payment Fees: Understand the penalties for missed or late payments.

- Additional Fees: Look for any hidden administrative fees or charges.

- GAP Insurance: While often useful, ensure you’re not overpaying for it or that it’s not being bundled without your explicit consent.

If something is unclear, ask for clarification. Don’t sign anything until you’re completely comfortable with all terms.

5. Be Wary of Add-Ons

When you’re finalizing the purchase at the dealership, you’ll likely be presented with a host of add-on products like extended warranties, rustproofing, paint protection, or VIN etching. While some of these might offer value, many are high-profit items for the dealership and may not be necessary or worth the cost.

Critically evaluate each add-on. If you decide to purchase them, try to negotiate their price separately. Adding them to your loan simply increases the principal amount you’re borrowing and paying interest on.

6. Consider Refinancing Later

Your financial situation can change. If you secure a loan with a higher interest rate due to a lower credit score, make consistent payments and work on improving your credit. Once your score improves, or if market rates drop, explore refinance car loan Tucson options.

Refinancing can be a powerful tool to lower your interest rate, reduce your monthly payments, or even shorten your loan term, saving you money in the long run.

Common Mistakes to Avoid When Getting a Car Loan in Tucson

Even experienced buyers can fall into common traps when seeking auto financing. Being aware of these pitfalls can help you avoid costly errors and ensure a smoother process for car loans Tucson AZ.

1. Not Checking Your Credit Score and Report

This is a fundamental mistake. Without knowing your credit standing, you’re going into negotiations blind. You won’t know if the interest rate you’re offered is fair, or if there are errors on your report that could be easily fixed to improve your rate. Always start with a thorough credit check.

2. Focusing Only on the Monthly Payment

As discussed, fixating solely on the monthly payment can lead to accepting a longer loan term or a higher interest rate, resulting in a much larger total cost for the vehicle. Always ask for the total cost of the loan and compare APRs.

3. Ignoring the Total Cost of the Loan

The sticker price of the car and the monthly payment are just parts of the equation. The true measure of a good deal is the total amount you will pay over the life of the loan, including principal and all interest. A loan with a slightly higher monthly payment over a shorter term can often be significantly cheaper in the long run.

4. Not Getting Pre-Approved

Skipping pre-approval means you lose a significant negotiation advantage. You’re less likely to get the best deal on the vehicle’s price if the dealership knows you haven’t secured your own financing and are relying on their options.

5. Rushing the Process

Buying a car and securing a loan are major financial decisions. Don’t feel pressured by a salesperson to make a quick decision. Take your time, do your research, compare offers, and only sign when you’re fully confident and understand everything. Haste often leads to regret and unnecessary expenses.

6. Letting Add-Ons Drive Up Your Loan Amount

It’s common for dealerships to present various add-ons in the finance office. While some might be beneficial, many simply inflate the total loan amount, meaning you pay interest on items you might not truly need or could get cheaper elsewhere. Be firm and only accept what you truly want and understand.

Beyond the Loan: Protecting Your Investment in Tucson

Once you’ve secured your ideal car loan in Tucson, AZ and driven off the lot, your financial responsibilities don’t end. Protecting your new investment is just as important as securing the right financing.

Insurance Considerations in Arizona

Arizona requires minimum liability insurance, but for financed vehicles, lenders will typically mandate full coverage insurance (including collision and comprehensive). The cost of auto insurance in Tucson can vary based on your vehicle, driving record, and even your specific zip code within the city.

Always get insurance quotes before finalizing your car purchase to factor this cost into your overall budget. Sometimes, the difference in insurance premiums for two similar vehicles can be substantial. If you’re also exploring options for motorcycle financing, we have a detailed article dedicated to that might interest you.

Regular Maintenance

Tucson’s desert climate, with its intense heat and dust, can be tough on vehicles. Regular maintenance, such as oil changes, tire rotations, and checking fluid levels, is crucial to prolong your car’s lifespan and prevent costly repairs. Sticking to the manufacturer’s recommended service schedule not only keeps your car running smoothly but also helps maintain its resale value. This is especially important when you’re still paying off a loan.

Understanding Your Rights

As a consumer, you have rights regarding financial transactions. It’s important to be aware of these rights, especially when dealing with loan agreements. The Consumer Financial Protection Bureau (CFPB) offers valuable resources and information to help you understand your protections. To understand more about your rights as a consumer in financial transactions, the Consumer Financial Protection Bureau (CFPB) offers valuable resources.

Conclusion: Driving Forward with Confidence in Tucson

Securing car loans in Tucson, AZ doesn’t have to be a stressful ordeal. By understanding the different loan types, knowing where to find lenders, meticulously preparing for the application process, and being aware of the factors that influence your loan terms, you can navigate the journey with confidence. Remember to leverage the power of pre-approval, shop around aggressively for the best rates, and always read the fine print.

Whether you’re exploring the scenic drives around Mount Lemmon or simply commuting across the city, having reliable transportation is key to enjoying all that Tucson has to offer. By following the advice in this guide, you’ll not only secure a great vehicle but also a smart financial deal, setting you on the road to financial success. Start your journey today and drive away with the peace of mind that comes from making an informed decision.