Navigating Car Loans Of America: Your Ultimate Guide to Driving Away with Confidence

Navigating Car Loans Of America: Your Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

The dream of owning a car is deeply woven into the fabric of American life. For many, it represents freedom, independence, and the ability to access opportunities. However, turning that dream into a reality often involves securing a car loan. Understanding the intricacies of car loans of America is paramount for making a financially sound decision.

This comprehensive guide will demystify the world of auto financing in the United States. We’ll explore everything from the types of loans available to the application process, key factors influencing your rates, and crucial tips for securing the best deal. Our goal is to empower you with the knowledge needed to navigate the market confidently and drive away with a vehicle that fits your budget and lifestyle.

Navigating Car Loans Of America: Your Ultimate Guide to Driving Away with Confidence

Understanding the Landscape of Car Loans in America

Before diving into the application process, it’s essential to grasp what a car loan entails and the various forms it can take. A car loan is a secured loan, meaning the vehicle itself acts as collateral. If you fail to make payments, the lender has the right to repossess the car.

This fundamental concept underpins all auto financing. It makes car loans generally easier to obtain than unsecured personal loans, but also highlights the importance of responsible borrowing. Your car payment will be a significant monthly expense, so understanding its components is vital.

What Exactly is a Car Loan?

At its core, a car loan is an agreement where a financial institution lends you money to purchase a vehicle. In return, you agree to repay the borrowed amount, plus interest, over a predetermined period. This period, known as the loan term, can range from a few months to several years.

The principal amount is the actual price of the car you are financing. Interest is the cost of borrowing that money, expressed as a percentage. Together, these elements determine your monthly payment and the total cost of the loan.

Diverse Types of Car Loans Available

The market for car loans in America offers a variety of options, each tailored to different needs and circumstances. Knowing these types can help you identify the best fit for your situation.

New Car Loans: These loans are for purchasing brand-new vehicles directly from a dealership. They often come with the lowest interest rates due to the vehicle’s higher value and perceived lower risk for lenders. Lenders see new cars as less likely to have immediate mechanical issues, which reduces their risk.

However, new cars depreciate rapidly once driven off the lot. This means you could owe more on the loan than the car is worth, a situation known as being "upside down" or having negative equity. It’s a common consideration when opting for a new car loan.

Used Car Loans: When you’re buying a pre-owned vehicle, you’ll apply for a used car loan. These loans typically carry slightly higher interest rates than new car loans, reflecting the increased risk associated with an older vehicle’s unknown history and potential for mechanical issues. Lenders will often consider the age and mileage of the used car when determining rates and terms.

Many financial institutions have specific requirements for the age or mileage of a used car they will finance. It’s wise to check these criteria before falling in love with a particular pre-owned model. Always get a pre-purchase inspection for a used car to ensure its condition.

Refinance Loans: A refinance loan involves replacing your existing car loan with a new one, often with different terms. People typically refinance to secure a lower interest rate, reduce their monthly payments, or change the loan term. This can be a smart move if your credit score has improved since you first took out the loan.

Refinancing can also be beneficial if market interest rates have dropped. It’s a strategic way to save money over the life of your loan. We’ll delve deeper into refinancing later in this guide, as it’s a powerful tool for many car owners.

Private Party Loans: If you’re buying a car directly from an individual seller rather than a dealership, you’ll need a private party loan. These can be more challenging to obtain because lenders may perceive a higher risk. They lack the established processes and inspections that dealerships provide.

Lenders might require an appraisal of the vehicle or a more thorough inspection to verify its value and condition. Based on my experience, securing a private party loan often requires more legwork, but it can also lead to better deals on the car itself. Be prepared with all vehicle documentation, including the title and maintenance records.

The Essential Steps: Applying for a Car Loan

The process of applying for a car loan can seem daunting, but breaking it down into manageable steps makes it much clearer. Following these stages will help you stay organized and make informed decisions. This methodical approach is key to securing favorable terms for your US auto loan.

Step 1: Assess Your Financial Health

Before you even start looking at cars, take a hard look at your personal finances. This foundational step is critical for understanding what you can realistically afford. Knowing your financial standing empowers you during negotiations and helps prevent overspending.

Begin by checking your credit score and reviewing your credit report. This will give you an idea of how lenders will perceive you. Simultaneously, create a detailed budget to understand your income, expenses, and current debt-to-income (DTI) ratio. Lenders use DTI to assess your ability to take on additional debt.

Step 2: Get Pre-Approved

One of the most powerful steps you can take is getting pre-approved for a loan before visiting any dealerships. Pre-approval means a lender has provisionally agreed to lend you a specific amount of money at a certain interest rate, pending a final vehicle choice. It’s a crucial advantage when shopping for car loans of America.

Pro tips from us: Pre-approval transforms you into a cash buyer in the eyes of a dealership. This gives you significant leverage to negotiate the vehicle’s price, as you’re not reliant on their financing options. It also helps you set a realistic budget for your car purchase.

Step 3: Choose Your Vehicle & Negotiate

With your pre-approval in hand, you can confidently shop for a car that fits your budget. Remember to negotiate the price of the car separately from the financing. Dealerships often try to combine these, but it’s always best to get the lowest possible vehicle price first.

Focus on the "out-the-door" price of the car, which includes all fees and taxes. Once you’ve agreed on a price, you can then compare your pre-approved loan offer with any financing options the dealership might present. This allows you to choose the most advantageous loan.

Step 4: Finalize Your Loan & Paperwork

Once you’ve selected your car and decided on the best financing option, it’s time to finalize the loan. This involves carefully reviewing all the loan documents. Pay close attention to the interest rate, loan term, monthly payment, and any fees.

Ensure that there are no hidden charges or clauses you don’t understand. Don’t hesitate to ask questions until everything is clear. Signing the final papers means you’ve committed to the loan, so thorough review is paramount.

Key Factors Influencing Your Car Loan Offer

When you apply for car loans of America, lenders evaluate several factors to determine your eligibility, the interest rate you’ll receive, and the terms of your loan. Understanding these elements can help you prepare and potentially secure a better deal. Each factor plays a significant role in shaping your overall auto financing experience.

Your Credit Score: The Cornerstone

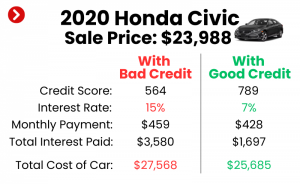

Your credit score is arguably the most critical factor lenders consider. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. Higher credit scores indicate a lower risk to lenders, often leading to lower interest rates and more favorable terms.

FICO scores, which range from 300 to 850, are widely used. Generally, a score above 700 is considered good, while scores above 780 are excellent. If your score is lower, you might still qualify for a loan, but you’ll likely face higher interest rates. Improving your credit score before applying can save you thousands over the life of the loan. For more detailed advice on improving your financial standing, consider reading our article on How to Boost Your Credit Score for Better Loan Opportunities (Internal Link Placeholder).

Income and Debt-to-Income (DTI) Ratio

Lenders need to be confident that you can comfortably afford your monthly loan payments. They assess this by looking at your income and your debt-to-income (DTI) ratio. Your income demonstrates your earning capacity, while your DTI ratio compares your total monthly debt payments to your gross monthly income.

A lower DTI ratio indicates that you have more disposable income available to cover new loan payments. Lenders typically prefer a DTI ratio below 43%, though some may have stricter guidelines. A high DTI can signal to lenders that you might be overextended, making them hesitant to approve your loan or offering less favorable terms.

Down Payment: A Powerful Tool

Making a down payment means paying a portion of the car’s price upfront. This significantly reduces the amount you need to borrow, which can lead to several benefits. A larger down payment can lower your monthly payments, decrease the total interest paid over the loan term, and immediately give you equity in the vehicle.

Common mistakes to avoid are underestimating the power of a solid down payment. Lenders also view a substantial down payment favorably, as it demonstrates your commitment and reduces their risk. A common recommendation is to put down at least 10-20% for a new car and 10% for a used car, if possible.

Loan Term: Balancing Monthly Payments and Total Cost

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A longer loan term results in lower monthly payments, which can make a more expensive car seem affordable. However, this comes at a cost.

A longer term means you’ll pay more interest over the life of the loan. You’ll also build equity more slowly, increasing the risk of being "upside down" on your loan. Conversely, a shorter loan term means higher monthly payments but less total interest paid and quicker ownership. Choosing the right loan term involves balancing affordability with the total cost of borrowing.

Interest Rates and APR: What You’re Really Paying

Understanding interest rates and the Annual Percentage Rate (APR) is crucial for any car loan in America. The interest rate is the percentage charged by the lender for the money you borrow. The APR, however, is a more comprehensive measure of the cost of borrowing.

APR includes the interest rate plus any additional fees associated with the loan, such as origination fees. It provides a truer picture of the total annual cost of your loan. Always compare APRs when shopping for loans, not just the interest rate, to get an accurate comparison of offers. Interest rates can be fixed, meaning they stay the same throughout the loan term, or variable, meaning they can fluctuate with market conditions. Most auto loans are fixed-rate, offering predictability in your monthly payments.

Beyond the Basics: Strategic Considerations for Car Loans Of America

Beyond the fundamental aspects of securing a car loan, there are several strategic considerations that can significantly impact your financial well-being. These elements often involve long-term planning and a deeper understanding of the automotive market. Being aware of these options and potential pitfalls is essential for any savvy car buyer.

The Power of Refinancing Your Car Loan

Refinancing your car loan can be a highly effective financial strategy. It involves taking out a new loan to pay off your existing auto loan. This move is typically considered when you can secure a lower interest rate, which in turn reduces your monthly payments or the total interest paid over time.

You might consider refinancing if your credit score has improved since you first bought the car, if current market interest rates are lower, or if you need to adjust your monthly payment due to a change in your financial situation. It’s also an option if you simply want to change your loan term, perhaps to pay off the car faster or to lower payments temporarily. Many online lenders specialize in auto loan refinancing, making the process relatively straightforward.

Understanding Additional Costs and Add-ons

When finalizing your car loan, you might encounter various additional costs and optional add-ons. It’s vital to scrutinize these thoroughly. Some fees, like documentation fees or state registration charges, are unavoidable. However, others are optional and might not be in your best interest.

- GAP Insurance: Guaranteed Asset Protection (GAP) insurance covers the "gap" between what you owe on your car loan and what your car is worth if it’s totaled or stolen. Since new cars depreciate quickly, this can be a valuable safeguard, especially if you made a small down payment or have a long loan term.

- Extended Warranties: Dealerships often push extended warranties. While they offer peace of mind, they can be costly and may overlap with the manufacturer’s warranty. Carefully evaluate if an extended warranty is necessary for your vehicle and if the cost justifies the coverage.

- Early Payoff Penalties: While rare in auto loans, some agreements might include penalties for paying off your loan ahead of schedule. Always check your loan agreement for any such clauses.

Based on my experience, many of these add-ons are profit centers for dealerships, so assess their value to you critically. Don’t feel pressured to accept them if they don’t align with your needs.

Lease vs. Buy: A Fundamental Decision

While this article focuses on car loans of America, the broader decision of whether to lease or buy a car is fundamental. Each option has distinct financial implications and suits different lifestyles.

- Buying means you own the vehicle after paying off the loan. You have full control over modifications, mileage, and eventual resale. It’s generally better for those who drive a lot, want to keep a car for many years, or prefer building equity.

- Leasing is essentially long-term renting. You make monthly payments for the use of a car for a set period (usually 2-4 years) and then return it. This often results in lower monthly payments and the ability to drive a new car every few years. However, you don’t build equity, and there are mileage restrictions and potential wear-and-tear charges.

Your choice depends on your driving habits, financial goals, and desire for ownership versus flexibility.

Pro Tips & Common Mistakes to Avoid with US Auto Loans

Navigating the world of car loans of America can be complex, but armed with the right strategies and awareness of common pitfalls, you can significantly improve your chances of securing a favorable deal. These insights come from years of observing how consumers interact with the auto financing market.

Our Top Pro Tips for a Smooth Car Loan Journey

Here are some actionable tips to help you secure the best possible auto loan:

- Research Thoroughly: Don’t just settle for the first car or loan offer you receive. Research vehicle prices, read reviews, and understand average interest rates for someone with your credit profile. Knowledge is power.

- Shop Around for Lenders: Don’t limit yourself to the dealership’s financing. Explore options from banks, credit unions, and online lenders. Each might offer different rates and terms. Getting multiple quotes allows you to compare and choose the most competitive offer.

- Get Pre-Approved from Multiple Sources: As mentioned earlier, pre-approval is a game-changer. Obtain pre-approvals from a few different lenders to have strong leverage when negotiating at the dealership.

- Read the Fine Print Carefully: Before signing anything, read every line of the loan agreement. Understand all terms, conditions, fees, and penalties. If something is unclear, ask for clarification.

- Focus on the Total Cost, Not Just Monthly Payments: Dealerships often try to make a car seem affordable by stretching out the loan term to lower monthly payments. Always ask about the total amount you will pay over the life of the loan. A lower monthly payment often means paying significantly more in interest overall.

- Consider the Entire Cost of Car Ownership: Beyond the loan, remember to budget for car insurance, maintenance, fuel, and registration fees. These can add up quickly. For guidance on protecting your investment, you might find our guide on Understanding Car Insurance Options helpful (Internal Link Placeholder).

Common Pitfalls to Sidestep

Even well-intentioned buyers can fall into common traps. Being aware of these can save you money and headaches:

- Skipping Pre-Approval: Going to a dealership without pre-approval leaves you vulnerable to their financing offers, which may not be the most competitive. You lose your negotiation power.

- Not Checking Your Credit Report: Errors on your credit report can negatively impact your score. Always review it before applying for a loan and dispute any inaccuracies. You can get a free copy of your credit report from AnnualCreditReport.com (External Link: https://www.annualcreditreport.com/index.action).

- Accepting the First Offer: Whether it’s the car price or the loan terms, never take the first offer. Always be prepared to negotiate.

- Extending the Loan Term Too Much: While a longer term reduces monthly payments, it drastically increases the total interest paid and puts you at higher risk of negative equity.

- Forgetting About Insurance Costs: The car you can afford monthly might have sky-high insurance premiums, especially for younger drivers or certain vehicle types. Get insurance quotes before finalizing your purchase.

- Being Pressured into Add-ons: Don’t feel obligated to purchase extended warranties, fabric protection, or other extras if you don’t genuinely need or want them. They significantly inflate the total cost.

The Future of Car Loans in America

The landscape of car loans of America is continually evolving. We’re seeing a clear trend towards digitalization, with more online lenders offering streamlined application processes and competitive rates. Electric Vehicle (EV) financing is also becoming a specialized area, with unique incentives and loan products emerging.

As technology advances and consumer preferences shift, lenders are adapting to meet new demands. Staying informed about these trends can give you an edge in future car purchases. The emphasis on transparency and personalized offers is likely to grow, benefiting informed consumers.

Drive Away with Confidence

Securing a car loan is a significant financial decision, but it doesn’t have to be a stressful one. By understanding the different types of car loans of America, meticulously preparing for the application process, and being aware of the factors that influence your offer, you can navigate the market with confidence.

Remember to prioritize your financial health, shop around for the best rates, and always read the fine print. With the insights provided in this ultimate guide, you are well-equipped to make an informed decision and drive away in your desired vehicle on your own terms. Your journey to car ownership starts with smart financial planning.