Navigating Car Loans Reno: Your Ultimate Guide to Driving Off the Lot with Confidence

Navigating Car Loans Reno: Your Ultimate Guide to Driving Off the Lot with Confidence Carloan.Guidemechanic.com

Buying a car is an exciting milestone, offering freedom, convenience, and a gateway to exploring the stunning landscapes surrounding Reno. However, the path to ownership often involves securing a car loan, a process that can feel daunting without the right guidance. Whether you’re a long-time Reno resident or new to the Biggest Little City, understanding the nuances of car loans is crucial for making a smart financial decision.

This comprehensive guide is designed to be your definitive resource for navigating car loans in Reno. We’ll break down every aspect, from understanding the basics to finding the best lenders, ensuring you’re equipped with the knowledge to secure a deal that fits your budget and lifestyle. Our goal is to empower you to drive off the lot with confidence, knowing you’ve made an informed choice.

Navigating Car Loans Reno: Your Ultimate Guide to Driving Off the Lot with Confidence

Why Understanding Car Loans in Reno Matters

Reno’s vibrant community and surrounding natural beauty make personal transportation essential. From daily commutes to work to weekend adventures in Lake Tahoe or the Sierra Nevada, a reliable vehicle is often a necessity. Securing the right car loan isn’t just about getting a car; it’s about setting yourself up for financial success and enjoying the freedom that comes with mobility in this unique Nevada city.

The local market for car loans Reno can vary, with numerous dealerships, banks, and credit unions vying for your business. Each offers different rates, terms, and conditions. Without a clear understanding of your options and financial standing, you could end up paying significantly more than necessary. This guide aims to demystify the process, helping you find competitive auto loans Reno that truly benefit you.

Understanding the Fundamentals of Car Loans: Your Financial Compass

Before diving into the specifics of obtaining car loans in Reno, it’s essential to grasp the core concepts of vehicle financing. Think of these as the building blocks of your loan agreement. Understanding these terms will allow you to compare offers effectively and ask the right questions.

A car loan is essentially an agreement where a lender provides you with funds to purchase a vehicle, and you agree to repay that amount, plus interest, over a set period. This repayment is typically made through regular monthly installments.

Key Terms You Need to Know

Principal: This is the initial amount of money you borrow to buy the car. If the car costs $25,000 and you put down $5,000, your principal loan amount would be $20,000.

Interest Rate: Expressed as a percentage, the interest rate is the cost of borrowing money. It’s the fee the lender charges you for using their funds. A lower interest rate means you’ll pay less over the life of the loan.

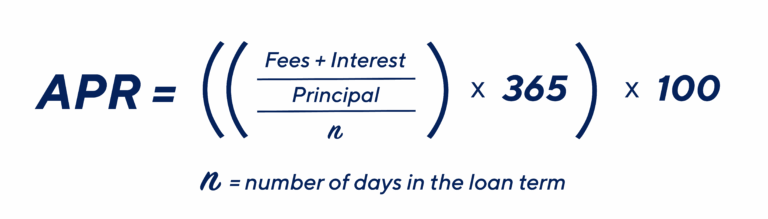

Annual Percentage Rate (APR): The APR is a broader measure of the cost of borrowing money. It includes the interest rate plus any additional fees or charges associated with the loan, such as administrative fees. The APR gives you a more accurate picture of the total annual cost of your loan. Based on my experience, many people confuse interest rate and APR; always compare APRs when looking at different loan offers for a true apples-to-apples comparison.

Loan Term: This refers to the duration, usually expressed in months, over which you agree to repay the loan. Common loan terms range from 36 to 84 months. A shorter term generally means higher monthly payments but less total interest paid, while a longer term offers lower monthly payments but accrues more interest over time.

Down Payment: This is the initial sum of money you pay upfront towards the purchase price of the vehicle. A larger down payment reduces the amount you need to borrow, which can lead to lower monthly payments and less interest paid over the life of the loan. It also often makes you a more attractive borrower to lenders.

Trade-In: If you have an existing vehicle, you might be able to trade it in to the dealership. The value of your trade-in can be applied towards the purchase price of your new car, effectively acting as a down payment. This can significantly reduce the amount you need to finance.

Exploring the Different Types of Car Loans Available in Reno

Not all car loans are created equal. The type of vehicle you’re purchasing, its age, and even where you’re buying it from can influence the kind of financing available to you. Understanding these distinctions is crucial for finding the most suitable auto loans Reno option.

New Car Loans

These loans are specifically for brand-new vehicles purchased from a dealership. They often come with the lowest interest rates due to the car’s high value and typically predictable depreciation. Lenders view new cars as lower risk.

New car loans usually offer a wider range of loan terms, giving you flexibility in your monthly payments. However, remember that new cars depreciate rapidly, so consider how long you plan to keep the vehicle.

Used Car Loans

Used car loans are for pre-owned vehicles, whether purchased from a dealership or a private seller. The interest rates for used car loans are typically a bit higher than for new cars, reflecting the increased risk associated with an older vehicle and potentially higher maintenance costs.

The age and mileage of the used car can also impact the loan terms and rates. Older vehicles or those with very high mileage might have fewer financing options or shorter loan terms.

Car Loan Refinancing

If you already have a car loan but believe you could get a better deal, refinancing might be an excellent option. Refinancing involves taking out a new loan to pay off your existing car loan, ideally with a lower interest rate, a shorter term, or more favorable conditions. This can significantly reduce your monthly payments or the total amount of interest you pay over time.

Pro tips from us: Refinancing is especially beneficial if your credit score has improved since you initially took out the loan, or if interest rates have dropped. It’s always worth exploring if you think you’re paying too much.

Private Party Car Loans

Buying a car directly from an individual (private party) often means you’ll need a specific type of loan, as traditional auto dealerships won’t be involved in the financing. Many banks and credit unions in Reno offer private party car loans.

These loans can sometimes be more challenging to secure than dealership financing, as lenders might require additional inspections or appraisals of the vehicle. However, buying from a private party can often lead to a lower purchase price for the car itself.

Your Credit Score: The Undeniable Key to Car Loans Reno

Your credit score is arguably the most critical factor in determining the interest rate and terms you’ll be offered for car loans in Reno. Lenders use this three-digit number to assess your creditworthiness – essentially, how likely you are to repay the loan on time. A higher score signals less risk to lenders, typically resulting in better loan offers.

How Your Credit Score Impacts Your Loan

- Excellent Credit (780+): If you fall into this category, congratulations! You’re likely to qualify for the absolute best interest rates and most favorable terms available. Lenders will compete for your business.

- Good Credit (670-779): Most consumers fall into this range. You’ll still qualify for competitive rates, though perhaps not the very lowest. You’ll have a wide range of options for car loans Reno.

- Fair Credit (580-669): You can still get approved for a car loan with a fair credit score, but you’ll likely face higher interest rates. Lenders might also require a larger down payment or offer shorter loan terms to mitigate their risk.

- Poor Credit (Below 580): Securing a car loan with poor credit can be challenging, but it’s not impossible. You’ll likely encounter significantly higher interest rates, and some lenders may require a co-signer or substantial down payment. There are specialized lenders in Reno that cater to bad credit car loans, but always compare their offers carefully.

Strategies for Improving Your Credit Score Before Applying

If your credit score isn’t where you’d like it to be, taking steps to improve it before applying for a loan can save you thousands of dollars in interest.

- Check Your Credit Report: Obtain free copies of your credit report from Equifax, Experian, and TransUnion. Review them for any errors or inaccuracies and dispute them immediately.

- Pay Bills On Time: Payment history is the biggest factor in your credit score. Make sure all your credit card, utility, and other loan payments are made on or before their due dates.

- Reduce Existing Debt: Lowering your credit card balances, especially, can improve your credit utilization ratio, which is how much credit you’re using compared to your total available credit.

- Avoid New Credit: Resist opening new credit accounts in the months leading up to your car loan application, as this can temporarily ding your score.

For a deeper dive into improving your credit score, check out our guide on . Taking these steps can significantly impact the auto loans Reno offers you receive.

Navigating the Car Loan Application Process in Reno

The application process for car loans Reno can seem complex, but breaking it down into manageable steps makes it much easier. Being prepared and organized will streamline your experience and increase your chances of approval.

Step 1: Assess Your Budget and Needs

Before you even look at cars, determine how much you can comfortably afford each month for a car payment, including insurance, fuel, and maintenance. Use online car loan calculators to estimate payments based on different loan amounts, interest rates, and terms. This will help you set a realistic price range for your vehicle.

Consider your lifestyle in Reno. Do you need a robust truck for outdoor adventures, an efficient sedan for city commutes, or an SUV for family trips? Your needs will guide your vehicle choice and, subsequently, your loan amount.

Step 2: Check Your Credit Score and Report

As discussed, this is a critical preparatory step. Knowing your score upfront gives you a realistic expectation of the interest rates you might qualify for and allows you to address any issues before applying.

Step 3: Get Pre-Approved for a Loan

This is a powerful step many buyers overlook. Pre-approval means a lender has conditionally agreed to lend you a certain amount of money at a specific interest rate, before you even choose a car. It gives you significant leverage at the dealership because you walk in as a cash buyer.

Pro tips from us: Obtaining pre-approval from multiple lenders (banks, credit unions, online lenders) within a short window (typically 14-45 days, depending on the credit scoring model) will only count as a single hard inquiry on your credit report. This allows you to compare the best car loan rates Reno offers without further credit impact.

Step 4: Shop for Your Vehicle

With your budget and pre-approval in hand, you can now confidently shop for a car. Focus on vehicles within your pre-approved amount. Once you find the right car, you can negotiate the price knowing your financing is already largely secured.

Step 5: Finalize Your Loan

Once you’ve settled on a vehicle, you’ll finalize the loan. This involves reviewing all the terms, including the APR, loan term, and total cost. Ensure you understand every detail before signing the paperwork. If you have a pre-approval, you can compare it directly with any financing offered by the dealership.

Finding the Right Lender for Car Loans Reno

Reno offers a diverse landscape of lenders, each with its own advantages. Exploring all your options is key to securing the best car loan rates Reno has to offer.

Dealership Financing

Most car dealerships offer in-house financing, often working with a network of banks and captive lenders (e.g., Ford Credit, Toyota Financial Services).

- Pros: Convenience, one-stop shopping, potential for special manufacturer incentives (low APR or cash back offers). Dealerships can sometimes secure loans for buyers with less-than-perfect credit.

- Cons: Rates might not always be the most competitive, limited options compared to shopping independently, potential for "payment packing" where extra products are added without clear disclosure.

Banks

Traditional banks are a common source for car loans. They offer a variety of loan products and often provide competitive rates for borrowers with good credit.

- Pros: Reputable institutions, often familiar to consumers, may offer relationship discounts if you already bank with them.

- Cons: Stricter credit requirements, less flexibility for borrowers with poor credit, the application process can sometimes be slower than other options.

Credit Unions

Credit unions are non-profit financial cooperatives owned by their members. They are renowned for offering some of the best car loan rates Reno can provide, often beating out traditional banks.

- Pros: Typically lower interest rates, more personalized service, often more flexible with borrowers who have less-than-perfect credit, and lower fees.

- Cons: Requires membership (though often easy to join), may have fewer branch locations than large banks.

Online Lenders

A growing number of online lenders specialize in auto loans. These platforms allow you to apply and get approvals quickly from the comfort of your home.

- Pros: Quick application and approval process, often competitive rates, easy to compare multiple offers from various lenders.

- Cons: Less personal interaction, potential for scams if not using a reputable lender, may require more self-service during the process.

Pro tips from us: Always get pre-approved from at least two different types of lenders (e.g., a credit union and an online lender) before heading to the dealership. This gives you strong negotiating power and ensures you have a benchmark to compare against any dealership offers. For more unbiased information on choosing a lender, you can visit .

Essential Documents for Your Reno Car Loan Application

Being prepared with the necessary documentation will significantly speed up your car loan application process. Lenders need these documents to verify your identity, income, and ability to repay the loan.

Here’s a checklist of what you’ll likely need:

- Proof of Identity: A valid government-issued photo ID (e.g., driver’s license, passport).

- Proof of Residence: Utility bill, lease agreement, or mortgage statement showing your current Reno address.

- Proof of Income: Recent pay stubs (typically 1-2 months), W-2 forms, tax returns (especially if self-employed), or bank statements showing consistent deposits.

- Social Security Number (SSN): Required for credit checks.

- Vehicle Information (if already chosen): Make, model, year, VIN (Vehicle Identification Number), and purchase price.

- Proof of Auto Insurance: Lenders typically require you to have full coverage insurance before you can drive off with the vehicle. Have your insurance company information readily available.

- References: Some lenders, especially those for bad credit car loans Reno, may ask for personal references.

- Trade-in Information (if applicable): Title, registration, and any loan payoff information for your current vehicle.

Gathering these documents beforehand will make the application seamless, whether you’re applying in person or online for auto loans Reno.

Common Mistakes to Avoid When Getting Car Loans Reno

Based on my experience helping countless buyers, there are several common pitfalls that can lead to a less-than-ideal car loan experience. Being aware of these can save you money and stress.

1. Focusing Only on the Monthly Payment

This is perhaps the biggest mistake. While a low monthly payment is attractive, it often comes at the cost of a longer loan term, which means you’ll pay significantly more in total interest over the life of the loan. Always consider the total cost of the loan, including interest, not just the monthly installment.

2. Not Checking Your Credit Score First

Walking into a dealership or bank without knowing your credit score puts you at a disadvantage. You won’t know if the rates you’re being offered are fair or if you could qualify for something better. Always check your score and report beforehand.

3. Skipping Pre-Approval

Without a pre-approved loan, you lose significant negotiation power. The dealership knows you’re dependent on their financing, which can lead to higher interest rates or less favorable terms. Get pre-approved to establish a baseline.

4. Ignoring the APR

As mentioned, the APR gives you the true cost of borrowing. Don’t just look at the interest rate; compare the APRs from different lenders to get an accurate picture of the total annual cost. Common mistakes we’ve seen are buyers accepting a slightly lower interest rate from one lender without realizing another has a lower APR due to fewer fees.

5. Not Negotiating the Car Price Separately

Always negotiate the purchase price of the car before discussing financing. If you combine these negotiations, it becomes harder to tell if you’re getting a good deal on the car or on the loan. Treat them as two distinct transactions.

6. Falling for Unnecessary Add-ons

Dealerships often try to sell extended warranties, paint protection, GAP insurance, and other add-ons. While some might be beneficial, many are overpriced and can significantly increase your loan amount and monthly payment. Research these products independently and decide if you truly need them.

7. Not Reading the Fine Print

Always, always read the entire loan agreement before signing. Understand all the terms, conditions, penalties for late payments, and early payoff options. Don’t hesitate to ask questions if anything is unclear.

Strategies for Securing the Best Car Loan Deal in Reno

Getting a car loan doesn’t have to mean settling for the first offer. With a strategic approach, you can significantly improve your chances of securing the best possible terms for auto loans Reno.

1. Boost Your Credit Score

This cannot be overstressed. Even a small improvement in your credit score can move you into a different tier of interest rates, saving you hundreds or even thousands of dollars over the loan term. Dedicate time to improving your credit before you apply.

2. Shop Around Extensively for Lenders

Don’t just go with your current bank or the dealership’s offer. Apply for pre-approval with multiple banks, credit unions, and online lenders in Reno. This competitive shopping forces lenders to offer their best rates to win your business. Remember, multiple inquiries within a short period (rate shopping) generally only count as one hard inquiry for auto loans.

3. Make a Substantial Down Payment

A larger down payment reduces the amount you need to borrow, which directly translates to lower monthly payments and less interest paid over time. It also signals to lenders that you are a serious and responsible borrower, potentially leading to better loan terms. Aim for at least 10-20% of the car’s purchase price if possible.

4. Consider a Shorter Loan Term

While a longer loan term offers lower monthly payments, it costs you more in total interest. If your budget allows, opt for the shortest loan term you can comfortably afford. For example, a 48-month loan will almost always be cheaper overall than a 72-month loan, even if the monthly payment is higher.

5. Negotiate the Car Price First

As mentioned, keep the car price negotiation separate from the loan negotiation. Get the best possible price on the vehicle before you even mention financing options. This ensures you’re not paying too much for the car itself. To learn more about effective negotiation tactics at the dealership, read our article on .

6. Be Prepared to Walk Away

The most powerful negotiation tool you have is the ability to walk away from a deal that doesn’t feel right. If a lender or dealership isn’t offering terms that align with your research and pre-approvals, be ready to take your business elsewhere. There are always other options for car loans Reno.

Life After Loan Approval: Your Responsibilities

Once you’ve secured your car loan and driven off the lot in your new vehicle, your financial journey isn’t over. You now have ongoing responsibilities to ensure you remain in good standing with your lender and protect your investment.

Make Payments On Time, Every Time

This is paramount. Late payments can result in fees, negatively impact your credit score, and potentially lead to repossession of your vehicle. Set up automatic payments or calendar reminders to ensure you never miss a due date. Consistent, on-time payments are the best way to maintain a healthy credit profile.

Maintain Comprehensive Auto Insurance

Lenders require you to carry full coverage insurance (collision and comprehensive) for the duration of your loan. This protects their asset (the car) in case of an accident or theft. Ensure your policy meets the lender’s requirements and keep it current. Failing to do so can lead to forced-place insurance, which is often more expensive.

Understand Early Payoff Options

Some loans have prepayment penalties, though these are less common with auto loans than with mortgages. Always check your loan agreement to see if there are any fees associated with paying off your loan early. If not, making extra payments or paying off the loan ahead of schedule can save you a significant amount in interest.

Keep Up with Vehicle Maintenance

While not directly related to your loan, properly maintaining your vehicle protects its value. This is especially important if you plan to trade it in later or sell it to pay off the remaining loan balance. Regular service helps prevent costly repairs and ensures your car remains reliable.

Conclusion: Drive with Confidence with Car Loans Reno

Securing car loans in Reno doesn’t have to be a stressful ordeal. By understanding the fundamentals, preparing your finances, diligently shopping for the best rates, and avoiding common mistakes, you can navigate the process with confidence and clarity. Remember, knowledge is power when it comes to financial decisions.

Our ultimate goal is to empower you to make an informed choice that aligns with your budget and financial goals. Take the time to research, compare offers, and ask questions. With the right approach, you’ll not only find the perfect vehicle for your Reno lifestyle but also secure auto loans Reno that set you up for long-term financial success. Drive off the lot knowing you’ve made a smart, strategic decision, ready to explore all that Northern Nevada has to offer.