Navigating Car Loans Vancouver: Your Ultimate Expert Guide to Driving Away with Confidence

Navigating Car Loans Vancouver: Your Ultimate Expert Guide to Driving Away with Confidence Carloan.Guidemechanic.com

Driving in Vancouver offers unparalleled freedom, whether you’re commuting to work, exploring the scenic Sea-to-Sky Highway, or simply running errands. However, securing the right vehicle often starts with understanding the intricate world of Car Loans Vancouver. For many, this process can seem daunting, riddled with jargon and choices that feel overwhelming.

As an expert blogger and professional SEO content writer, my mission is to demystify car financing in this vibrant city. This comprehensive guide will arm you with the knowledge and confidence needed to secure a loan that fits your financial situation, ensuring you drive away happy. We’ll dive deep into every aspect, from understanding interest rates to navigating bad credit, providing actionable advice every step of the way.

Navigating Car Loans Vancouver: Your Ultimate Expert Guide to Driving Away with Confidence

Why Car Ownership in Vancouver Matters: More Than Just a Convenience

Vancouver’s unique geography and lifestyle often make a personal vehicle more than just a luxury; it can be a necessity. While public transit is robust in some areas, reaching destinations like the North Shore mountains, the Fraser Valley, or even certain parts of Richmond and Surrey often requires a car. Having your own transport opens up opportunities for weekend getaways, family adventures, and greater flexibility in daily life.

Based on my experience working with countless Vancouver residents, the desire for a car often stems from a need for independence and efficiency. Navigating the city’s spread-out nature or accessing job opportunities outside central hubs frequently necessitates reliable transportation. Understanding this core need is the first step in appreciating the importance of finding the right Car Loans Vancouver.

Understanding the Vancouver Car Loan Landscape: A Local Perspective

The car loan market in Vancouver, much like its housing market, has specific characteristics. High living costs can influence what lenders are willing to offer and what borrowers can comfortably afford. Interest rates, loan terms, and even the types of vehicles available are all factors shaped by the local economic climate.

Our local market often sees a strong demand for reliable, fuel-efficient vehicles, given gas prices and the prevalence of urban driving. This demand can influence car prices, which in turn affects the size and terms of Vancouver auto financing packages. Being aware of these local nuances is crucial for any prospective car buyer.

Types of Car Loans in Vancouver: Your Options Explored

When considering Car Loans Vancouver, you’ll encounter a variety of financing avenues. Each has its own benefits and drawbacks, and understanding them is key to making an informed decision. Choosing the right type of loan depends on your financial health, the kind of vehicle you’re buying, and your long-term goals.

Let’s break down the most common options available to Vancouver residents. This detailed exploration will help you identify the path that best suits your individual circumstances and financial strategy.

1. Dealership Financing

Most car dealerships in Vancouver offer in-house financing options. They act as intermediaries, connecting you with various lenders (banks, credit unions, and specialized finance companies) with whom they have established relationships. This convenience allows for a one-stop-shop experience, where you can choose your car and arrange financing simultaneously.

Pro tips from us: Dealerships often have access to competitive rates, especially for new vehicles or during promotional periods. However, it’s always wise to compare their offer with pre-approvals you might secure independently. Don’t be afraid to negotiate the interest rate and loan terms they present, as there’s often room for flexibility.

2. Bank and Credit Union Loans

Traditional financial institutions like major banks (e.g., RBC, TD, BMO, Scotiabank) and local credit unions (e.g., Vancity, Coast Capital Savings) are reliable sources for car loans. They typically offer competitive interest rates to customers with good credit histories. These loans are often straightforward, with clear terms and conditions.

The process usually involves applying directly to the institution, providing financial documents, and waiting for approval. If approved, you receive a cheque or direct deposit, which you then use to purchase the vehicle from a dealer or private seller. This approach gives you significant leverage as a cash buyer.

3. Online Lenders

The digital age has brought forth a multitude of online lenders specializing in car financing. Companies like AutoCapital Canada or CarsFast offer quick application processes, often with same-day approvals. They can be a great option for those who prefer the convenience of applying from home and comparing offers from multiple lenders without visiting physical branches.

Online lenders often cater to a wider range of credit scores, including those seeking bad credit car loans Vancouver. However, it’s essential to research their reputation and read reviews to ensure you’re dealing with a legitimate and trustworthy company. Always scrutinize their terms and conditions carefully before committing.

4. Private Sale Loans (PPR Loans)

Purchasing a vehicle from a private seller in Vancouver can often save you money compared to buying from a dealership, as there are no dealer markups or associated fees. However, securing financing for a private sale can be a bit different. Many banks and credit unions offer specific loans for private purchases, but they might require more stringent vehicle inspections or appraisals.

When considering a private sale, ensure the vehicle’s history is thoroughly checked (e.g., using a CarFax report) and consider an independent mechanical inspection. Some online lenders also specialize in private sale financing, providing a convenient way to fund your purchase from an individual seller.

5. Leasing vs. Buying: A Quick Comparison

While not strictly a "loan," leasing is a popular alternative to outright purchasing a car in Vancouver. When you lease, you essentially rent the car for a fixed period (typically 2-5 years) and make monthly payments. At the end of the lease, you can return the car, purchase it, or lease a new one.

Leasing often results in lower monthly payments than financing a purchase, as you’re only paying for the depreciation of the vehicle during your lease term. However, you don’t own the car, and mileage restrictions apply. Buying, on the other hand, means you own the vehicle outright once the loan is repaid, allowing for full customization and no mileage limits. Your choice depends on your long-term needs and preferences.

The Car Loan Application Process: Your Step-by-Step Vancouver Guide

Applying for Car Loans Vancouver doesn’t have to be a confusing ordeal. With the right preparation and understanding of the steps involved, you can navigate the process smoothly and efficiently. Based on my experience, a methodical approach almost always leads to a better outcome.

Let’s walk through the essential stages, from initial preparation to signing on the dotted line. Being proactive and organized will significantly improve your chances of securing favourable terms.

1. Preparation is Key: Laying the Groundwork

Before you even look at cars, take time to prepare your financial foundation. This crucial step can save you time, stress, and money in the long run. Skipping this part is a common mistake that can lead to unexpected hurdles later on.

- Determine Your Budget: Understand what you can realistically afford for a monthly car payment, factoring in insurance, fuel, maintenance, and potential parking costs. Use a budget calculator to get a clear picture of your disposable income. A general rule of thumb is that your car payment should not exceed 10-15% of your net monthly income.

- Check Your Credit Score and Report: Your credit score is the single most important factor lenders consider. Obtain a copy of your credit report from Equifax or TransUnion. Review it for accuracy and identify any errors. If your score is lower than desired, take steps to improve it, such as paying down existing debts or addressing collection accounts. A higher credit score translates directly to better car loan rates Vancouver.

- Gather Necessary Documents: Having your paperwork ready streamlines the application process. Typically, you’ll need:

- Proof of identity (Driver’s License, SIN card)

- Proof of residency (utility bill, lease agreement)

- Proof of income (pay stubs, employment letter, tax returns for self-employed)

- Bank statements

- Vehicle information (if you’ve already chosen one)

2. Shopping for a Loan: Comparing Your Options

Once prepared, it’s time to actively seek out loan offers. Don’t settle for the first offer you receive; comparison shopping is vital to securing the best possible terms for your Vancouver auto financing.

- Get Pre-Approved: Applying for pre-approval from multiple lenders (banks, credit unions, online lenders) allows you to compare actual offers without committing to a specific car. Pre-approvals typically involve a "soft" credit inquiry, which doesn’t negatively impact your credit score. This gives you a clear understanding of the interest rate and loan amount you qualify for, empowering you to negotiate at the dealership as a "cash buyer."

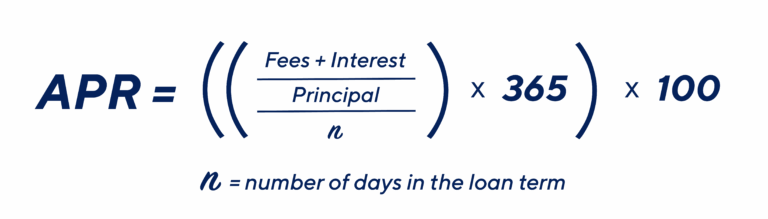

- Compare Interest Rates and Terms: Look beyond just the monthly payment. A longer loan term (e.g., 84 months) might offer lower monthly payments but will result in paying significantly more interest over the life of the loan. Compare the Annual Percentage Rate (APR), which includes interest and certain fees, to get a true sense of the loan’s cost.

- Understand All Fees: Be aware of any origination fees, administration fees, or early repayment penalties associated with the loan. These can add to the overall cost and should be factored into your decision.

3. Finalizing the Deal: The Last Steps

You’ve found your car and secured a great loan offer. Now it’s time to finalize everything. This stage requires careful attention to detail.

- Read the Loan Contract Thoroughly: Before signing, read every clause of the loan agreement. Ensure all terms (interest rate, loan amount, payment schedule, any fees) match what you agreed upon. If anything is unclear, ask for clarification. Common mistakes to avoid are rushing through this step or signing documents you don’t fully understand.

- Understand Insurance Requirements (ICBC): In British Columbia, basic vehicle insurance is provided by ICBC. However, you’ll likely need additional coverage (collision, comprehensive) to protect your vehicle, especially if it’s financed. Lenders typically require full coverage insurance to protect their investment. Get insurance quotes before finalizing your purchase to understand the total cost of ownership.

- Complete Vehicle Registration and Transfer: Ensure all necessary paperwork for vehicle registration and ownership transfer is completed accurately and promptly. This is crucial for legal ownership and to avoid any future issues.

Navigating Bad Credit Car Loans Vancouver: Hope is Not Lost

A less-than-perfect credit score can feel like a major roadblock when you’re seeking Car Loans Vancouver. However, it’s important to know that securing financing with bad credit is absolutely possible. While the terms might not be as favourable as for those with excellent credit, there are viable pathways available.

The key is to understand how bad credit impacts your options and to approach the process strategically. Many Vancouver lenders specialize in helping individuals rebuild their credit through responsible car loan repayment.

How Bad Credit Affects Your Loan

When your credit score is low, lenders perceive you as a higher risk. This typically translates to:

- Higher Interest Rates: To offset the perceived risk, lenders will charge a higher Annual Percentage Rate (APR). This means your monthly payments will be higher, and you’ll pay more interest over the loan term.

- Stricter Approval Criteria: You might need a larger down payment or a co-signer to get approved.

- Limited Loan Options: Fewer lenders might be willing to offer you a loan, and the maximum loan amount might be lower.

Options for Bad Credit Car Loans Vancouver

Don’t despair if your credit score isn’t ideal. Here are several avenues you can explore:

- Subprime Lenders: Many specialized lenders in Vancouver and online focus specifically on bad credit car loans Vancouver. They are more lenient with credit scores but will charge higher interest rates. Research these lenders carefully to ensure they are reputable.

- Secure a Co-Signer: If you have a trusted friend or family member with good credit willing to co-sign your loan, it can significantly improve your chances of approval and potentially secure a lower interest rate. A co-signer takes on equal responsibility for the loan, so choose someone who understands this commitment.

- Make a Larger Down Payment: A substantial down payment reduces the amount you need to borrow, making you a less risky borrower in the eyes of lenders. It also immediately builds equity in your vehicle.

- Consider a Less Expensive Vehicle: Opting for a more affordable, reliable used car can make the loan more manageable and increase your chances of approval. This approach can help you establish a positive payment history.

Pro tips from us: The most effective strategy for someone with bad credit is to view their car loan as an opportunity to rebuild their credit. Make every payment on time, and your credit score will gradually improve, opening doors to better financing options in the future, including the possibility of refinancing your current Vancouver auto financing.

Key Factors Influencing Your Car Loan in Vancouver

Beyond your credit score, several other elements play a significant role in determining the terms and approval of your Car Loans Vancouver. Understanding these factors will help you prepare and present yourself as a strong borrower. Each point contributes to the lender’s overall assessment of your financial reliability.

By optimizing these aspects, you can improve your chances of securing the most favorable car loan rates Vancouver has to offer. This proactive approach is a hallmark of an informed buyer.

- Credit Score: As discussed, this is paramount. A higher score (generally 650+) indicates lower risk and qualifies you for prime rates. Scores below this might lead to higher rates or specialized lenders.

- Down Payment: A larger down payment reduces the loan amount, decreases your monthly payments, and signifies your financial commitment. Lenders view a substantial down payment favorably, as it reduces their risk.

- Loan Term: This refers to the length of time you have to repay the loan (e.g., 60 months, 72 months). Shorter terms mean higher monthly payments but less interest paid overall. Longer terms mean lower monthly payments but more total interest and extended debt.

- Interest Rate (APR): The Annual Percentage Rate is the cost of borrowing, expressed as a percentage. It directly impacts your monthly payment and the total cost of the loan. Always aim for the lowest APR possible.

- Debt-to-Income (DTI) Ratio: Lenders look at your DTI ratio (your total monthly debt payments divided by your gross monthly income) to assess your ability to handle additional debt. A lower DTI ratio (typically below 40%) is more appealing.

- Vehicle Type and Age: Lenders often prefer to finance newer, more reliable vehicles, as they hold their value better. Older or high-mileage vehicles might be harder to finance or come with higher interest rates, as their resale value is lower, increasing the lender’s risk. This is particularly relevant for used car loans Vancouver.

Beyond the Loan: Protecting Your Investment in Vancouver

Securing your Car Loans Vancouver is just the beginning of your car ownership journey. To ensure your investment is protected and your financial health remains stable, there are several other considerations you must address. These ongoing costs and protective measures are crucial for long-term satisfaction.

Being prepared for these additional aspects of car ownership will prevent unexpected financial strain and ensure you get the most out of your vehicle. It’s about more than just the monthly payment; it’s about the entire ownership experience.

- Insurance (ICBC Specifics): In British Columbia, basic auto insurance is mandatory and provided by ICBC. However, for financed vehicles, lenders almost always require comprehensive and collision coverage to protect against damage or theft. Get quotes for this additional coverage before committing to a car, as rates can vary significantly based on the vehicle, your driving history, and where you live in Vancouver.

- Maintenance Costs: All vehicles require regular maintenance, from oil changes to tire rotations and brake inspections. Factor these ongoing costs into your budget. Neglecting maintenance can lead to more expensive repairs down the line and affect your car’s longevity and resale value.

- Refinancing Options: If your credit score improves after a year or two of on-time payments, or if interest rates drop, consider refinancing your car loan. Refinancing can potentially secure you a lower interest rate, reduce your monthly payments, or shorten your loan term, saving you a significant amount over time. This is a smart strategy for those who initially took out bad credit car loans Vancouver.

- Extended Warranties: Dealerships often offer extended warranties. While they can provide peace of mind, carefully weigh the cost against the potential benefits. Research the warranty provider and what exactly is covered. Sometimes, the manufacturer’s warranty is sufficient, especially for newer vehicles.

Expert Advice and Pro Tips for Vancouver Car Buyers

Drawing on years of experience in the auto financing landscape, I’ve compiled some invaluable pro tips to help you navigate Car Loans Vancouver with utmost confidence. These insights go beyond the basics, offering strategic advice that can save you money and headaches.

Applying these expert strategies will empower you to make smarter decisions and secure the best possible deal. Remember, knowledge is your strongest negotiating tool.

- Negotiate More Than Just the Price: When buying a car, everything is negotiable. Don’t just focus on the vehicle’s sticker price. Negotiate the trade-in value of your old car, the interest rate on your loan, and any additional fees. A professional salesperson expects you to negotiate.

- Get Pre-Approved, Then Visit the Dealership: As mentioned, securing pre-approval from an external lender (bank or credit union) gives you a powerful negotiating tool. It means you walk into the dealership with a financing offer already in hand, forcing the dealer to beat or match it. This strategy ensures you get competitive car loan rates Vancouver.

- Don’t Discuss Your Budget Too Early: When a salesperson asks, "What monthly payment are you looking for?" deflect the question. Discussing monthly payments first can lead to a focus on extending the loan term rather than getting the best overall price for the car and a low interest rate. Focus on the total price of the car and the APR of the loan separately.

- Read the Fine Print (Seriously!): I cannot stress this enough. Every contract has fine print for a reason. Understand all clauses, especially those related to early repayment penalties, late payment fees, and what happens in case of default. Common mistakes to avoid are signing without fully comprehending the terms or feeling pressured to sign quickly.

- Beware of Add-ons: Dealerships often offer additional products like rustproofing, paint protection, or extended warranties. While some might have value, many are high-profit items for the dealership. Carefully evaluate if you truly need them and if the price is fair. Don’t let them roll these into your Vancouver auto financing without conscious thought.

- Check the Vehicle’s History (VIN Check): Always run a VIN check (Vehicle Identification Number) through services like CarFax or CarProof, especially for used car loans Vancouver. This report reveals accident history, lien status, previous owners, and odometer discrepancies. This is critical for both private sales and dealership purchases.

For further insights into managing your finances effectively, we recommend exploring resources from reputable financial institutions or government consumer protection agencies. For instance, the Financial Consumer Agency of Canada offers excellent advice on car financing and debt management, helping you make informed decisions.

Driving Forward with Confidence: Your Vancouver Car Loan Journey

Securing Car Loans Vancouver is a significant financial decision, but with the right knowledge and preparation, it can be a smooth and rewarding process. From understanding the types of loans available to mastering the application process and navigating specific challenges like bad credit, this guide has equipped you with the expertise needed to make informed choices.

Remember, the goal is not just to get a car loan, but to secure the right car loan – one that aligns with your financial goals and allows you to enjoy the freedom of driving in beautiful British Columbia without undue stress. By following the expert advice and pro tips shared here, you are well on your way to driving away with confidence, knowing you’ve made a smart financial move. Take control of your car buying journey today!