Navigating Car Loans with a 580 Credit Score: Understanding Average Interest Rates and How to Secure the Best Deal

Navigating Car Loans with a 580 Credit Score: Understanding Average Interest Rates and How to Secure the Best Deal Carloan.Guidemechanic.com

Getting a car is often more than just a convenience; for many, it’s a necessity for work, family, and daily life. The dream of driving off the lot in a new or reliable used vehicle is exciting, but the reality of financing can quickly dampen spirits, especially if your credit score isn’t in the prime range. If you find yourself with a 580 credit score, you’re likely wondering: what kind of interest rate can I expect for a car loan?

This article is designed to be your definitive guide. We’ll dive deep into the world of auto financing for borrowers with a 580 credit score, exploring the average interest rates, the factors that influence them, and most importantly, actionable strategies to help you secure the most favorable terms possible. Our goal is to empower you with knowledge, turning what might seem like a hurdle into a manageable step towards car ownership and even credit improvement.

Navigating Car Loans with a 580 Credit Score: Understanding Average Interest Rates and How to Secure the Best Deal

Understanding Your 580 Credit Score and Its Impact

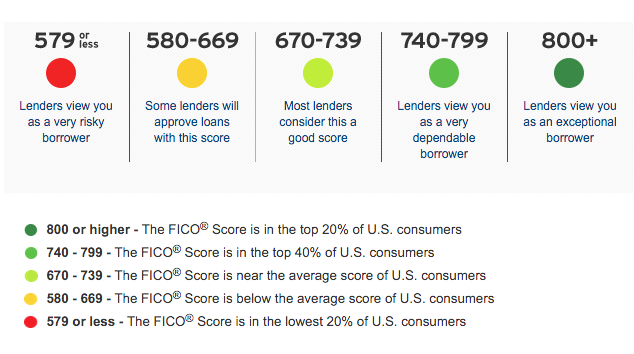

Before we talk numbers, let’s understand what a 580 credit score truly signifies to a lender. Credit scores, like the widely used FICO Score, range from 300 to 850. A score of 580 falls squarely into the "Fair" category, which is often considered "subprime" by lenders.

What does "subprime" mean in practical terms? It indicates a higher level of risk from the lender’s perspective. Individuals with scores in this range have typically had some challenges managing credit in the past, such as late payments, high credit utilization, or even collection accounts. Lenders see these past behaviors as indicators of potential future payment difficulties.

Because of this perceived risk, lenders often compensate by charging higher interest rates. This higher rate acts as a form of insurance for them, offsetting the increased likelihood of a borrower defaulting on the loan. It’s a way for them to make lending to higher-risk individuals financially viable.

The impact of a 580 credit score on a car loan is significant. You won’t qualify for the promotional low-interest rates advertised by dealerships, nor will you likely receive the single-digit rates offered to borrowers with excellent credit. Instead, you’ll be looking at rates that reflect your credit tier.

The Reality of Average Interest Rates for a Car Loan With a 580 Credit Score

So, what is the average interest rate for a car loan with a 580 credit score? Based on my experience and industry data, borrowers with a 580 credit score often face rates ranging from 10% to 20% or even higher, depending on various factors. It’s crucial to understand that this is a broad average, and your specific rate could fall anywhere within or even outside this range.

Why such a wide spectrum? A 580 credit score alone doesn’t tell the whole story. Lenders consider a multitude of data points when assessing your application. While a 580 score immediately places you in a higher-risk category, other elements of your financial profile will fine-tune the exact interest rate you’re offered.

To put this into perspective, consider that a borrower with excellent credit (750+) might secure a car loan with an interest rate as low as 3-5% in a favorable market. The difference in monthly payments and the total cost of the car over the loan term can be staggering. For example, on a $20,000 car loan over five years, a 5% interest rate means you’d pay around $377 per month and roughly $2,600 in total interest. At a 15% interest rate, that jumps to about $476 per month and over $8,500 in total interest. This illustrates why understanding and influencing your interest rate is so critical.

Factors That Influence Your Car Loan Rate (Beyond Credit Score)

While your 580 credit score is a major hurdle, it’s not the only determinant of your car loan interest rate. Several other factors play a pivotal role in a lender’s decision-making process. Understanding these can help you position yourself for a better deal.

Loan Term (Length of the Loan)

The length of your car loan significantly impacts both your monthly payment and the total interest you’ll pay. Generally, shorter loan terms (e.g., 36 or 48 months) result in higher monthly payments but lower overall interest paid. This is because the lender is exposed to risk for a shorter period.

Conversely, longer loan terms (e.g., 60, 72, or even 84 months) lead to lower monthly payments, making the car seem more affordable. However, you’ll pay significantly more in total interest over the life of the loan. For borrowers with a 580 credit score, lenders might sometimes offer slightly higher rates on longer terms due to the extended risk exposure, or they might offer them to make the payment affordable, knowing the total interest will be substantial.

Down Payment Amount

A substantial down payment is one of your most powerful tools when seeking a car loan with a 580 credit score. When you put down a larger sum of money upfront, you reduce the amount you need to borrow. This immediately lowers the lender’s risk.

Why is this so effective? A larger down payment demonstrates your financial commitment and reduces the likelihood of owing more on the car than it’s worth (being "upside down" on the loan). Lenders are more comfortable financing a smaller portion of the vehicle’s value, which can translate into a more favorable interest rate for you. Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price as a down payment if possible.

Debt-to-Income Ratio (DTI)

Your Debt-to-Income (DTI) ratio is a critical metric lenders use to assess your ability to manage monthly payments. It’s calculated by dividing your total monthly debt payments (including the prospective car loan) by your gross monthly income. A lower DTI indicates that you have more disposable income available to comfortably cover your loan payments.

A high DTI, on the other hand, suggests that a significant portion of your income is already allocated to other debts, making you a higher risk for defaulting on a new car loan. Even with a 580 credit score, a very low DTI might slightly improve your chances of getting a better rate than someone with the same credit score but a high DTI.

Vehicle Age and Type

The type and age of the vehicle you intend to finance also influence your interest rate. Newer, more reliable vehicles generally hold their value better, making them more attractive collateral for lenders. This can sometimes lead to slightly lower rates compared to financing an older, higher-mileage vehicle, which depreciates faster and carries more mechanical risk.

Luxury or performance vehicles, while appealing, often come with higher price tags and insurance costs. Financing such a vehicle with a 580 credit score can be challenging, as lenders may perceive it as an unnecessary risk. Opting for a more modest, reliable used car can often result in better loan terms.

Presence of a Co-signer

Having a co-signer with excellent credit can dramatically improve your chances of securing a more favorable interest rate, even with a 580 credit score. A co-signer essentially guarantees the loan, promising to make payments if you default.

This significantly reduces the lender’s risk, as they now have two individuals responsible for the debt. While it can be a great strategy, remember that a co-signer takes on equal responsibility for the loan, and any missed payments will negatively impact their credit score as well. This is a commitment that requires careful consideration and mutual trust.

Lender Type

Not all lenders are created equal, especially when it comes to financing with a 580 credit score. Your interest rate can vary significantly depending on whether you apply through a traditional bank, a credit union, a captive finance company (like Toyota Financial Services), or a subprime lender.

Credit unions, for example, are often known for offering more competitive rates and being more flexible with borrowers who have less-than-perfect credit because they are member-owned. Subprime lenders specialize in higher-risk loans and might be more willing to approve you, but often at much higher interest rates. Shopping around is crucial here.

Strategies to Secure a Better Car Loan Rate with a 580 Credit Score

While a 580 credit score presents challenges, it doesn’t mean you’re without options. There are several proactive strategies you can employ to improve your chances of securing a more manageable interest rate and a car loan approval.

1. Save for a Larger Down Payment

As discussed, a significant down payment is your best ally. It reduces the loan amount, lowers the lender’s risk, and demonstrates your commitment. If you can save up 15-20% of the car’s purchase price, you’ll be in a much stronger negotiating position.

Consider delaying your car purchase for a few months to build up your savings. Even an extra few hundred or a thousand dollars can make a noticeable difference in your loan terms. This not only potentially lowers your interest rate but also reduces your monthly payments and the total amount of interest you’ll pay over the life of the loan.

2. Consider a Co-signer Wisely

If you have a trusted friend or family member with a strong credit score, asking them to co-sign could be a game-changer. Their excellent credit history can offset the risk associated with your 580 score, potentially unlocking significantly lower interest rates.

However, this decision should not be taken lightly. The co-signer is equally responsible for the debt. If you miss payments, their credit score will suffer, and they will be legally obligated to pay. Ensure you have an honest conversation about the responsibilities and risks involved.

3. Shop Around and Get Pre-Approved

One of the biggest mistakes borrowers make is only applying for financing at the dealership. Dealerships often work with a limited number of lenders and may not always offer you the best rate.

Pro tips from us: Always shop around for financing before you step onto a car lot. Apply for pre-approval with several different types of lenders – banks, credit unions, and online lenders. Pre-approval allows you to compare actual offers without impacting your credit score too much (multiple inquiries within a short period often count as one for FICO scoring models). This gives you leverage at the dealership, as you’ll know what kind of rate you qualify for independently.

4. Choose the Right Vehicle

Be realistic about the car you can afford. With a 580 credit score, aiming for a brand-new luxury SUV is likely out of reach and financially unwise. Focus on reliable, affordable used cars.

A less expensive vehicle means a smaller loan amount, which translates to lower monthly payments and less overall risk for the lender. Consider models known for their durability and low maintenance costs. This approach not only makes approval easier but also helps you manage your budget.

5. Improve Your Credit Score (Even Marginally)

While a significant jump from 580 to 700+ won’t happen overnight, even a small improvement can make a difference. Before applying for a loan, take a few months to focus on boosting your score.

- Check your credit report: Obtain free copies from AnnualCreditReport.com and dispute any errors. Even one inaccurate negative item removed can give you a boost.

- Pay down existing debt: Focus on reducing balances on credit cards, especially those close to their limits. Lowering your credit utilization ratio is one of the fastest ways to improve your score.

- Make all payments on time: Payment history is the biggest factor in your credit score. Ensure all your bills are paid promptly.

Even a 20-30 point increase can sometimes move you into a slightly better lending tier, potentially shaving a percentage point or two off your interest rate. For more detailed strategies, consider reading our guide on Tips for Improving Your Credit (placeholder for internal link).

6. Provide Extensive Documentation

When you have a 580 credit score, lenders will want to see as much proof of financial stability as possible. Be prepared to provide comprehensive documentation:

- Proof of income (pay stubs, tax returns)

- Proof of residency (utility bills)

- Proof of employment stability (employment verification letter)

- Bank statements

- References

The more complete and organized your documentation, the smoother the process and the more confident the lender will be in your ability to repay.

Common Mistakes to Avoid When Getting a Car Loan with Bad Credit

Navigating the car loan process with a 580 credit score can be tricky, and it’s easy to fall into common traps. Being aware of these pitfalls can save you money, stress, and protect your financial future.

1. Not Checking Your Credit Report Beforehand

Many borrowers make the mistake of applying for a loan without first knowing what’s on their credit report. This is a critical oversight. Your credit report might contain errors that are unfairly dragging down your score.

Common mistakes to avoid are signing a loan agreement without fully understanding your credit standing. By reviewing your report, you can identify and dispute inaccuracies, potentially boosting your score before you even apply. It also helps you understand why your score is 580, preparing you for conversations with lenders. We recommend checking your full credit report from all three major bureaus. For more on understanding your score, check out our article on Understanding Your Credit Score (placeholder for internal link).

2. Only Applying to One Lender (or Just the Dealership)

As mentioned earlier, limiting your loan search to a single source, especially the dealership, is a common and costly error. Dealerships often have partnerships that benefit them, not necessarily you.

By not shopping around, you miss the opportunity to compare multiple offers and find the most competitive interest rate. Always get pre-approved by several lenders to ensure you have a benchmark.

3. Buying More Car Than You Can Afford

The temptation to buy a nicer, more expensive car than your budget allows is strong, especially when you finally get approved. However, this is a dangerous path, particularly with a high interest rate.

A higher car price combined with a high interest rate can lead to crippling monthly payments and a high risk of default. Focus on affordability first. Remember, the goal is reliable transportation, not a status symbol that drains your finances.

4. Focusing Only on the Monthly Payment

Dealerships often try to "sell the payment," meaning they’ll negotiate the monthly amount to make it seem affordable, often by extending the loan term. While a lower monthly payment is appealing, it usually means you’ll pay significantly more in total interest over the life of the loan.

Always look at the total cost of the loan, including all interest and fees. A slightly higher monthly payment over a shorter term can save you thousands of dollars in the long run.

5. Falling for Predatory Lending Tactics

Unfortunately, some lenders prey on individuals with poor credit. Common mistakes to avoid are signing without reading the fine print, especially when your credit score is in the 580 range. Be wary of deals that sound too good to be true, extremely high fees, or balloon payments (a large lump sum due at the end of the loan).

Always read the entire loan agreement carefully. If something feels off, don’t hesitate to walk away. If a lender pressures you to sign immediately or discourages you from reading the terms, it’s a major red flag.

The Path to Rebuilding Credit Through a Car Loan

While a 580 credit score means higher interest rates now, a car loan can actually be a powerful tool for improving your credit score in the long run. By making all your car loan payments on time, every time, you demonstrate responsible financial behavior to credit bureaus.

Consistent, on-time payments for a significant installment loan like a car loan can positively impact your payment history, which is the most influential factor in your credit score. Over time, as your score improves, you’ll gain access to better financial products, lower interest rates on future loans, and a stronger financial foundation. Think of this car loan not just as transportation, but as an investment in your credit future.

Conclusion: Your Journey to Car Ownership and Beyond

Securing a car loan with a 580 credit score presents undeniable challenges, particularly when it comes to the average interest rate for car loan with 580 credit score, which typically falls between 10% and 20% or even higher. However, it is by no means an insurmountable obstacle. By understanding how lenders view your credit score and the various factors that influence your loan terms, you can approach the financing process strategically and confidently.

Remember to prioritize saving for a larger down payment, explore the possibility of a co-signer, diligently shop around for the best loan offers, and choose a vehicle that truly fits your budget. Most importantly, avoid common mistakes that can lead to unfavorable terms or financial distress. A car loan with a 580 credit score can be more than just a means to transportation; it can be a significant step towards rebuilding your credit and opening doors to better financial opportunities in the future. Armed with knowledge and a proactive approach, you can navigate this journey successfully.