Navigating Car Loans with a 670 Credit Score: Unlocking Favorable Interest Rates and Approval

Navigating Car Loans with a 670 Credit Score: Unlocking Favorable Interest Rates and Approval Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is exciting, but for many, the financing aspect can feel like navigating a complex maze. If your credit score hovers around 670, you might find yourself in a unique position—neither at the top tier of "excellent" nor struggling with "poor" credit. This "fair to good" range often leaves prospective car buyers wondering what kind of car loan interest rates they can expect and how to secure the best possible deal.

As an expert in auto financing and credit, I’ve seen firsthand how a 670 credit score can be a stepping stone to great financing, provided you know the right strategies. This comprehensive guide will demystify the process, offering in-depth insights into obtaining a car loan with a 670 credit score, understanding the associated interest rates, and equipping you with the knowledge to drive away with a favorable agreement. We’ll dive deep into what lenders look for, how to prepare your application, and crucial tips to save you money in the long run.

Navigating Car Loans with a 670 Credit Score: Unlocking Favorable Interest Rates and Approval

Understanding Your 670 Credit Score: What It Means to Lenders

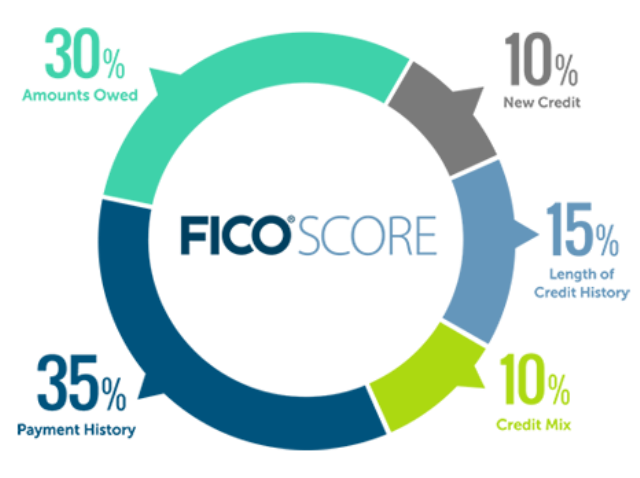

A 670 FICO credit score places you firmly in the "Good" category, according to many credit scoring models. While it’s not "Excellent" (typically 800+), nor "Very Good" (740-799), it’s a strong indicator of financial responsibility compared to scores in the "Fair" (580-669) or "Poor" (under 580) ranges. Lenders generally view a 670 score as a solid foundation, suggesting you are a reliable borrower with a history of managing debt reasonably well.

This score indicates a lower risk than someone with a fair or poor credit score, but it doesn’t guarantee the absolute lowest interest rates available. Lenders will still scrutinize other aspects of your financial profile. They want to ensure you have the capacity to repay the loan, even with a decent credit history.

Your 670 score signals that you’ve likely made most of your payments on time and managed credit accounts responsibly. However, there might be some minor blemishes, such as a late payment or higher credit utilization, preventing it from reaching the "Very Good" or "Excellent" tiers. Understanding this nuance is key to setting realistic expectations and preparing for your loan application.

The Reality of Car Loan Interest Rates with a 670 Credit Score

When it comes to car loan interest rates, your 670 credit score positions you for competitive, though not necessarily prime, offers. You’ll generally qualify for better rates than someone with a sub-600 score, but likely higher rates than someone with an 800+ score. The exact interest rate you receive will depend on a multitude of factors, not just your credit score alone.

Based on my experience in the auto financing industry, borrowers with a 670 credit score can typically expect interest rates ranging from 7% to 12% on a new car loan, and slightly higher for a used car, potentially 8% to 15%. These figures are broad estimates, and the actual rate can fluctuate based on market conditions, the specific lender, and other elements of your financial profile. It’s crucial to remember that these are just averages; your unique situation will dictate your specific offer.

Factors beyond your credit score, such as the down payment amount, the loan term, and the vehicle itself, significantly influence the final interest rate. For instance, a larger down payment demonstrates less risk to the lender, often resulting in a lower rate. Similarly, opting for a shorter loan term can also lead to a better interest rate, as the lender’s risk exposure is reduced over a shorter period.

Factors Beyond Your Credit Score That Influence Your Car Loan

While a 670 credit score is a great starting point, it’s only one piece of the puzzle. Lenders assess your overall financial health to determine your eligibility and interest rate. Understanding these additional factors can empower you to strengthen your application.

-

Debt-to-Income Ratio (DTI): This crucial metric compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover new loan payments, making you a less risky borrower. Lenders typically prefer a DTI below 43%, though lower is always better. For a deeper dive into this, you might find our article on helpful. (Internal Link Placeholder 1)

-

Down Payment Amount: The more money you put down upfront, the less you need to borrow, and the less risk the lender assumes. A substantial down payment (10-20% or more) can significantly lower your interest rate and monthly payments. It also helps prevent you from being "upside down" on your loan, where you owe more than the car is worth.

-

Vehicle Age and Type: Lenders often view newer vehicles as less risky because they hold their value better and typically have fewer mechanical issues. Older, higher-mileage vehicles might come with higher interest rates due to increased depreciation and potential maintenance costs. The type of vehicle (e.g., luxury vs. economy) can also play a role.

-

Loan Term Length: This is the duration over which you agree to repay the loan. While longer terms (e.g., 72 or 84 months) offer lower monthly payments, they usually come with higher interest rates because the lender’s money is tied up for a longer period, increasing their risk. Shorter terms (e.g., 36 or 48 months) typically have lower interest rates and result in less interest paid overall, but with higher monthly payments.

-

Co-signer Option: If you have a co-signer with excellent credit, their strong financial profile can help you secure a lower interest rate. A co-signer essentially guarantees the loan, mitigating the lender’s risk. However, it’s a significant responsibility for the co-signer, as they are equally liable for the debt.

-

Trade-in Value: If you’re trading in your current vehicle, its value can act like a down payment, reducing the amount you need to finance. A good trade-in value can positively impact your loan terms. Ensure you get a fair valuation for your trade-in.

Preparing for Your Car Loan Application

A well-prepared application can make a substantial difference in the interest rate you secure. Don’t rush into the process; strategic preparation can save you thousands over the life of the loan.

-

Check Your Credit Report (and Dispute Errors): Before approaching any lender, pull your credit reports from all three major bureaus (Experian, Equifax, and TransUnion). You can do this for free annually at AnnualCreditReport.com. Scrutinize them for any inaccuracies or errors. Disputing and correcting these can potentially boost your score, even if only by a few points, which could translate to a better interest rate.

-

Budgeting for a Car: Beyond the monthly loan payment, consider insurance, fuel, maintenance, and registration fees. Use a realistic budget to determine what you can truly afford. Overextending your budget can lead to financial strain down the road.

-

Saving for a Down Payment: Aim for at least 10% of the car’s purchase price, but ideally 20% or more. A larger down payment reduces the principal amount borrowed, lowers your monthly payments, and can significantly improve your chances of securing a lower interest rate. It also provides immediate equity in the vehicle.

-

Gathering Necessary Documents: Be ready with essential paperwork. This typically includes proof of income (pay stubs, tax returns), proof of residence (utility bills, lease agreement), identification (driver’s license), and details of your current debts and assets. Having everything organized will streamline the application process.

Strategies to Secure the Best Car Loan with a 670 Credit Score

While a 670 credit score is good, proactive strategies can help you outperform average expectations and secure truly favorable terms. Don’t settle for the first offer you receive.

-

Get Pre-Approved from Multiple Lenders: This is perhaps the most powerful strategy. Approach several lenders—banks, credit unions, and online auto loan providers—to get pre-approved before stepping foot in a dealership. Pre-approvals give you a solid offer, including the interest rate and maximum loan amount, allowing you to shop for a car with confidence.

Pro tips from us: All credit inquiries for auto loans within a short period (typically 14-45 days, depending on the scoring model) are usually grouped as a single inquiry, minimizing the impact on your score. This means you can shop around for the best rates without harming your credit. Don’t just rely on the dealership’s financing; they may not always offer the best rates upfront.

-

Shop Around for the Best Offers: Don’t limit yourself to just one lender. Different financial institutions have varying lending criteria and interest rate structures. What one bank considers a high risk, another might view more favorably. Compare interest rates, loan terms, and any associated fees from at least three to five different lenders.

-

Negotiate, Negotiate, Negotiate: Be prepared to negotiate not only the price of the car but also the terms of your loan. With a pre-approval in hand, you have leverage. You can use a lower interest rate offer from one lender to encourage another to match or beat it. Remember, everything is negotiable.

-

Consider a Larger Down Payment: As mentioned, a significant down payment is one of the most effective ways to lower your interest rate. It reduces the lender’s risk and shows your commitment to the purchase. If you can save up a bit more, it will pay dividends in the long run.

-

Shorten the Loan Term: While longer terms offer lower monthly payments, they come with higher overall interest costs. If your budget allows, opt for the shortest loan term possible (e.g., 36 or 48 months). This will often result in a lower interest rate and significantly reduce the total interest you pay over the life of the loan.

-

Improve Your Credit Score (Pre-Application): If you have a few months before you need a car, focus on boosting your credit score. Pay down existing debts, especially credit card balances, to lower your credit utilization. Make all payments on time. Even a 20-30 point increase could move you into a lower interest rate tier. For practical steps, consider our guide on . (Internal Link Placeholder 2)

-

Consider a Co-signer (If Necessary): If, after exploring all options, the interest rates are still higher than you’d like, a co-signer with an excellent credit score might be an option. Their strong credit history can help you qualify for a much lower interest rate. Be sure both parties understand the full implications and responsibilities of co-signing.

Common Mistakes to Avoid When Getting a Car Loan

Even with a good credit score, missteps during the car loan process can cost you money and cause unnecessary stress. Being aware of these common pitfalls can help you navigate the process more smoothly.

-

Not Checking Your Credit Report: This is a fundamental error. Failing to review your credit report means you might be unaware of errors that are dragging down your score, or you might enter negotiations without knowing your true credit standing. Always check your reports well in advance.

-

Only Applying at the Dealership: While convenient, relying solely on dealership financing can limit your options. Dealerships often work with a limited number of lenders and might not always offer the most competitive rates, especially if you haven’t done your homework beforehand. Always come armed with an external pre-approval.

-

Focusing Solely on Monthly Payments: It’s easy to get fixated on a low monthly payment. However, a low monthly payment often comes at the cost of a longer loan term and a higher overall interest paid. Always consider the total cost of the loan, including the interest, over its entire duration.

-

Extending the Loan Term Too Much: While a 72- or 84-month loan might seem appealing for its low monthly payments, it significantly increases the total interest you pay. It also keeps you in debt longer and increases the risk of being "upside down" on your loan, where the car depreciates faster than you pay it off.

-

Not Understanding All Fees: Car loans can come with various fees, including origination fees, documentation fees, and pre-payment penalties. Make sure you understand every charge before signing the agreement. Ask for a detailed breakdown of all costs.

-

Falling for "Payment Packing": This is a deceptive practice where dealerships add extras like extended warranties or GAP insurance into your monthly payment without clearly disclosing the individual costs. Always review the itemized list of what you’re paying for and question any charges you don’t understand or didn’t agree to.

What if Your Application Isn’t Approved, or Rates are Too High?

Even with a 670 credit score, there’s a chance your initial offers might not be ideal, or in rare cases, an application might be denied if other factors like DTI are unfavorable. Don’t be discouraged. This is an opportunity to improve your financial standing for future loans.

-

Focus on Credit Improvement Strategies: If you need to boost your score, prioritize paying all bills on time, every time. Reduce your credit card balances to keep utilization below 30% (ideally below 10%). Avoid opening too many new credit accounts at once.

-

Consider a Secured Loan or Credit Builder Loan: These can be excellent tools for building or rebuilding credit. A secured loan is backed by collateral (like a savings account), making it less risky for lenders. A credit builder loan involves you making payments into a savings account that is released to you at the end of the loan term, all while reporting your good payment history to credit bureaus.

-

Wait and Reapply: Sometimes, the best strategy is to wait a few months, implement credit improvement techniques, and then reapply. Even a small increase in your score can make a significant difference in interest rates.

After Approval: Managing Your Car Loan Responsibly

Congratulations on securing your car loan! The journey doesn’t end here. Responsible loan management is crucial for maintaining your good credit score and potentially saving money in the future.

-

Making Timely Payments: This is paramount. Consistent on-time payments are the single most important factor in maintaining and improving your credit score. Set up automatic payments to avoid missing due dates.

-

Refinancing Options Later: If your credit score improves significantly after a year or two of on-time payments, or if market interest rates drop, consider refinancing your car loan. You might be able to secure a lower interest rate, reducing your monthly payments or the total interest paid over the remaining term. Many lenders offer refinancing, and it’s worth exploring if your financial situation improves.

-

Impact on Credit Score: Managing your car loan responsibly will positively impact your credit mix and payment history, contributing to an even higher credit score. Conversely, missed payments can severely damage your score. Your car loan is a major factor in your credit profile, so treat it with care.

Conclusion

Securing a car loan with a 670 credit score is not only possible but often leads to quite favorable terms if you approach the process strategically. While you might not automatically qualify for the absolute lowest interest rates, your "Good" credit score provides a strong foundation. By understanding how lenders evaluate your application, diligently preparing your finances, and employing smart shopping tactics, you can unlock better interest rates and drive away with a deal that truly benefits you.

Remember to prioritize getting pre-approved from multiple lenders, focus on a substantial down payment, and always negotiate. Avoid common mistakes like only considering dealership financing or fixating solely on monthly payments. With a proactive and informed approach, your 670 credit score can be a powerful asset in your car buying journey, leading you to a manageable loan and the car of your dreams. Drive confidently, knowing you’ve made a well-informed financial decision.

External Resource: For more information on what different credit scores mean and how they are calculated, visit MyFICO’s official website: https://www.myfico.com/credit-education/whats-a-good-credit-score