Navigating Car Loans With No Job: Your Comprehensive Guide to Getting Approved

Navigating Car Loans With No Job: Your Comprehensive Guide to Getting Approved Carloan.Guidemechanic.com

Securing a car loan can feel like a monumental task even with a steady job. When you’re unemployed or working outside traditional employment structures, the challenge amplifies significantly. The thought of getting a car loan with no job might seem impossible, pushing many into despair. However, it’s a common misconception that traditional employment is the only gateway to vehicle financing.

While lenders typically prefer a stable employment history as proof of repayment ability, the financial landscape is evolving. There are indeed avenues and strategies you can explore to secure a car loan, even if your income doesn’t come from a standard paycheck. This comprehensive guide will dissect the complexities of getting a car loan without traditional employment, providing you with actionable insights, expert tips, and a clear roadmap to increase your chances of approval. Our goal is to empower you with the knowledge to navigate this challenging terrain successfully, transforming a seemingly impossible dream into a tangible reality.

Navigating Car Loans With No Job: Your Comprehensive Guide to Getting Approved

The Core Challenge: Why Lenders Hesitate (and How to Understand Them)

To truly understand how to secure a car loan with no job, it’s crucial to first grasp the lender’s perspective. For financial institutions, lending money is always a risk calculation. Their primary concern is whether you can consistently make your monthly payments on time, thus minimizing their potential losses.

Traditional employment serves as a straightforward and easily verifiable indicator of a borrower’s financial stability. A regular paycheck provides clear evidence of a predictable income stream, which directly impacts your debt-to-income (DTI) ratio – a critical metric lenders use. A low DTI, where your debt obligations are a small percentage of your income, signals less risk.

Without this conventional employment, the risk assessment becomes more complex. Lenders struggle to verify a consistent income, making them hesitant to approve loans. They are not intentionally trying to make your life harder; rather, they are adhering to strict lending guidelines and regulatory requirements designed to protect their assets and ensure responsible lending practices. Understanding this fundamental principle is your first step towards building a compelling case for your loan application.

What Counts as "Income" When You Don’t Have a Traditional Job?

The good news is that "income" in the eyes of a lender isn’t always synonymous with a W-2 paycheck. The financial world recognizes various forms of consistent revenue streams. Your task is to identify and effectively present these non-traditional sources as reliable proof of your ability to repay a loan.

Non-Traditional Employment: Beyond the 9-to-5

The modern economy offers a plethora of ways to earn a living that don’t involve a traditional employer. Lenders are increasingly recognizing these diverse income sources.

Gig Economy Income: If you work for platforms like Uber, Lyft, DoorDash, Instacart, or engage in freelance work through platforms like Upwork or Fiverr, this is absolutely considered income. The key here is consistency and documentation. You’ll need to provide detailed bank statements, earnings summaries from the platforms, and potentially tax returns (Schedule C) that clearly show a regular inflow of funds from these activities. Based on my experience, lenders want to see at least 6-12 months of consistent earnings to establish a reliable pattern.

Self-Employment/Small Business Owner: Even if you’re just starting a small business or working as an independent contractor, your earnings count. Lenders will look for business bank statements, invoices, client contracts, and tax returns that reflect your business income. Pro tips from us: Maintain meticulous records from day one. Separate personal and business finances to demonstrate professionalism and clarity in your financial reporting. This can significantly bolster your application, even if your business is relatively new.

Passive Income Streams: Earning While You Sleep

Passive income is particularly attractive to lenders because it often requires less active effort to maintain, suggesting a more stable and less volatile income source.

Rental Income: If you own property and receive rent, this is a prime example of passive income. You’ll need to provide copies of lease agreements and bank statements showing consistent rent deposits. Lenders will typically factor in your mortgage payments on the rental property when calculating your DTI, so be prepared to show those expenses as well.

Investment Dividends/Interest: Income generated from stocks, bonds, mutual funds, or other investments can also be considered. Provide statements from your brokerage accounts or investment portfolios that clearly show regular dividend payouts or interest earned. The more consistent and substantial these earnings are, the better.

Alimony/Child Support: These payments, when court-ordered and consistently received, are generally accepted as verifiable income. You’ll need to provide official court documents and bank statements demonstrating the regular receipt of these funds over an extended period. Lenders may require proof of continued payment for a certain duration into the future.

Government & Disability Benefits: Reliable Lifelines

Certain government and disability benefits are considered highly reliable by lenders because they are often long-term or permanent.

Social Security Benefits (Retirement/Disability): If you receive Social Security retirement or disability benefits, these are strong forms of verifiable income. You’ll need to provide your benefit award letter and bank statements showing regular deposits. These are typically viewed as very stable income sources.

Pension Income: For retirees, pension income is an excellent form of stable income. Provide official statements from your pension provider and bank statements showing regular deposits. This is often treated similarly to a traditional salary by lenders due to its predictable nature.

Unemployment Benefits: While unemployment benefits provide temporary income, they are generally not considered a stable long-term income source for car loan approval. Lenders understand these benefits have an expiration date and do not indicate long-term repayment ability. However, if you are transitioning from unemployment to a new job with a confirmed start date and offer letter, some lenders might consider it in conjunction with other factors.

Savings and Assets: Your Financial Foundation

Even without a regular income stream, your existing financial resources can speak volumes about your ability to repay a loan.

Proof of Significant Savings: Having a substantial amount in savings or checking accounts demonstrates financial prudence and a safety net. While not "income," it shows you have funds to cover payments, especially in the short term, or to make a larger down payment. Lenders appreciate seeing a healthy reserve.

Collateral (Existing Assets): If you own other valuable assets, such as another vehicle (with a clear title), real estate, or high-value collectibles, some lenders might consider a secured loan against these assets. This reduces their risk considerably. This is less common for car loans but can be an option for personal loans used to purchase a car.

Preparing Your Application: Boosting Your Chances

Once you’ve identified your sources of non-traditional income, the next crucial step is to meticulously prepare your loan application. This involves more than just filling out forms; it’s about building a compelling financial narrative that instills confidence in lenders.

Build a Strong Financial Narrative: Show, Don’t Just Tell

Simply stating you have income won’t suffice. You need robust documentation to back up every claim.

Proof of Stable Non-Job Income: As discussed, gather all relevant documents. For gig workers, this means earnings reports from platforms and bank statements. For self-employed individuals, it includes tax returns (especially Schedule C or K-1), business bank statements, invoices, and client contracts. For passive income, provide lease agreements, investment statements, and court orders. The more consistent and well-documented your income, the stronger your case.

Detailed Financial Statements: Provide several months (typically 3-6) of bank statements for all your accounts. Lenders will scrutinize these for consistent deposits, responsible spending habits, and an overall positive cash flow. Any large, unexplained withdrawals or overdrafts can raise red flags.

Tax Returns: Even if you don’t have a W-2, your tax returns (especially if you’re self-employed or have significant passive income) are invaluable. They provide an official, government-verified record of your earnings, demonstrating consistency over a longer period.

Improve Your Credit Score: Your Financial Reputation

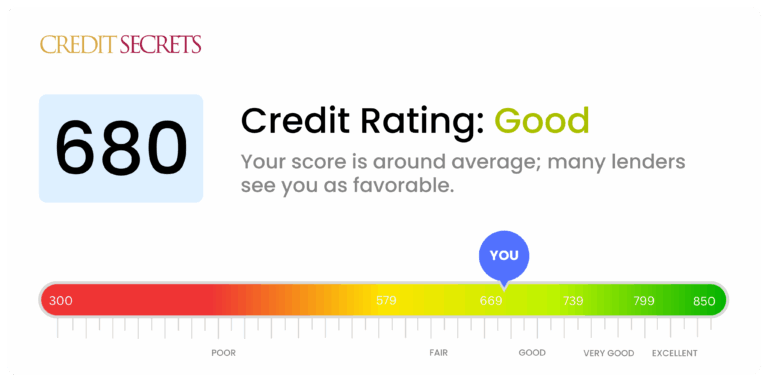

Your credit score is arguably the most critical factor after income verification. A strong credit score signals responsible financial behavior and a lower risk profile, which is paramount when you lack traditional employment.

Importance of Good Credit: A higher credit score (typically 670 and above) indicates that you’ve managed credit responsibly in the past. This can significantly offset the perceived risk of not having a W-2 job. Lenders are more willing to take a chance on a borrower with excellent credit, even with non-traditional income, because their payment history is stellar.

Tips for Quick Credit Boosts: While a complete credit overhaul takes time, there are immediate steps you can take. Pro tips from us:

- Pay down revolving credit card balances: Aim to keep utilization below 30% of your available credit.

- Correct errors on your credit report: Obtain free reports from Equifax, Experian, and TransUnion and dispute any inaccuracies.

- Ensure all payments are current: Even one late payment can significantly ding your score.

- Consider becoming an authorized user on someone else’s well-managed credit card (with their permission).

For more detailed strategies, you might want to check out our article on "Boosting Your Credit Score: A Quick Guide" (Internal Link Placeholder).

Gather a Substantial Down Payment: Reducing Lender Risk

A significant down payment is one of the most effective ways to mitigate risk for a lender, especially when you’re seeking a car loan with no job.

Reduces Lender Risk: When you put down a large chunk of money upfront, the loan amount decreases, and so does the lender’s exposure. In the event of default, they have a smaller principal to recover. This shows your commitment and reduces the likelihood of you walking away from the loan.

Lowers Loan Amount and Monthly Payments: A larger down payment means you’re borrowing less, which translates to lower monthly payments. This improves your DTI ratio and makes the loan more affordable, further strengthening your application.

Pro Tip: Aim for at least 20% of the vehicle’s purchase price as a down payment. If you can manage more, even better. This demonstrates serious intent and financial capability. Common mistakes to avoid are underestimating the power of a down payment or assuming a small amount is enough.

Consider a Co-Signer: Shared Responsibility, Shared Risk

If you’ve exhausted other options or want to significantly improve your chances, a co-signer can be a game-changer.

Who Makes a Good Co-Signer: A co-signer is someone with excellent credit and a stable, verifiable income who agrees to be equally responsible for the loan. If you default, the co-signer is legally obligated to make the payments. Ideal co-signers are typically close family members who trust you implicitly.

Risks and Responsibilities for Both Parties: This is a serious commitment. For you, it means maintaining perfect payment history to protect your co-signer’s credit. For the co-signer, their credit score will be impacted by the loan, and they will be on the hook if you cannot pay. This can strain relationships if things go wrong.

Common Mistakes to Avoid:

- Asking someone without understanding the implications: Both parties must fully comprehend the legal and financial responsibilities.

- Assuming the co-signer will never have to pay: Life happens, and they might.

- Not having a clear agreement: Discuss what happens if payments become difficult.

Exploring Your Financing Options

Not all lenders are created equal, especially when it comes to non-traditional income. Knowing where to look can save you time and increase your chances of finding a favorable deal.

Dealership Financing (Special Finance Departments): Convenience with Caveats

Many dealerships offer in-house financing or work with a network of lenders, including those who specialize in challenging credit situations.

Their Role, Pros and Cons: Dealerships, particularly those with "Special Finance" departments, are often equipped to handle applications from individuals with non-traditional income or less-than-perfect credit. The main advantage is convenience – you can often apply and get approved on the spot. However, the interest rates might be higher, and you might have fewer options compared to shopping independently.

Buy-Here-Pay-Here (BHPH) Lots: These dealerships finance their own loans directly to customers. They are often a last resort for those with very poor credit or no verifiable income, as they prioritize your ability to make payments over traditional credit scores. Pros: High approval rates, even with significant challenges. Cons: Be extremely cautious. BHPH lots often charge exorbitant interest rates, may require frequent (weekly/bi-weekly) payments, and might equip vehicles with GPS tracking/kill switches for easy repossession. Based on my experience, this option should only be considered if all others have failed, and you must thoroughly understand the terms before committing.

Credit Unions and Community Banks: Relationship-Based Lending

These institutions often offer more flexibility and personalized service than large national banks.

Often More Flexible: Credit unions, being member-owned, often have more lenient lending criteria and are more willing to consider individual circumstances. They value relationships and might be more understanding of non-traditional income sources, especially if you have an established banking history with them.

Relationship Lending: If you’re an existing member with a good standing, a credit union might be more inclined to work with you. They might consider your overall financial picture, including savings and other accounts, rather than just strict income criteria.

Online Lenders Specializing in Non-Traditional Situations: A Growing Market

The digital age has brought forth numerous online lenders, some of whom specifically cater to unique financial situations.

Convenience, Range of Options: Online platforms allow you to compare multiple loan offers from various lenders quickly and easily, often without impacting your credit score with multiple hard inquiries (initially, they use soft inquiries). Many online lenders use advanced algorithms that can assess risk differently, sometimes favoring non-traditional income.

Due Diligence Required: While convenient, it’s crucial to research online lenders thoroughly. Check reviews, look for transparency in their terms and conditions, and ensure they are reputable. Common mistakes to avoid are falling for phishing scams or lenders that promise "guaranteed approval" without any credit checks – these are often predatory.

Personal Loans (Unsecured vs. Secured): An Alternative Route

Sometimes, a traditional car loan isn’t the best fit, and a personal loan can be an alternative way to finance your vehicle.

Can Be an Option, But Often Higher Interest: An unsecured personal loan doesn’t require collateral but relies solely on your creditworthiness and income. If approved with non-traditional income, the interest rates can be higher than a secured car loan due to the increased risk for the lender. The loan funds are deposited directly into your bank account, and you use them to purchase the car outright.

Secured Personal Loans Using Collateral: If you have valuable assets, you might be able to secure a personal loan against them. This reduces the lender’s risk and can result in lower interest rates. However, be aware that if you default, you risk losing the collateral.

The Application Process: Step-by-Step

Navigating the application process for a car loan with no job requires meticulous planning and execution.

-

Assess Your Financial Health: Before approaching any lender, conduct a thorough self-assessment. Understand your exact income sources, their consistency, your current expenses, and your credit score. Be realistic about what you can afford.

-

Gather Documents: This cannot be stressed enough. Compile every piece of documentation that supports your income claims: bank statements, tax returns, freelance invoices, benefit letters, lease agreements, investment statements, and any other proof of funds. The more organized and complete your documentation, the smoother the process.

-

Shop Around for Lenders: Don’t settle for the first offer. Contact multiple credit unions, community banks, and reputable online lenders. Compare interest rates, loan terms, fees, and their flexibility regarding non-traditional income. Use pre-qualification tools where available to get an idea of potential rates without a hard credit pull.

-

Be Honest and Transparent: When discussing your financial situation with lenders, always be truthful. Attempting to obscure or misrepresent your income sources will likely lead to rejection and can damage your credibility. Explain your situation clearly and confidently, presenting your documentation as evidence.

-

Understand the Terms: Before signing anything, read the loan agreement carefully. Pay close attention to the interest rate (APR), the loan term, monthly payment amount, any fees (origination, late payment), and the total cost of the loan over its lifetime. Ask questions until you fully understand every clause.

Common Pitfalls and How to Avoid Them

The journey to getting a car loan with no job is fraught with potential traps. Being aware of them can save you significant financial heartache.

Falling for "Guaranteed Approval" Scams: There is no such thing as "guaranteed approval" for any loan, especially if you have no traditional job or a low credit score. Lenders always assess risk. Any offer that promises guaranteed approval without a thorough application process is likely predatory or a scam. Pro tips from us: If it sounds too good to be true, it almost certainly is.

Taking on Unaffordable Payments: It’s easy to get excited about getting approved and overlook the long-term affordability. Don’t commit to monthly payments that stretch your budget thin. Factor in not just the loan payment, but also insurance, fuel, maintenance, and unexpected repairs. Common mistakes to avoid are focusing only on the monthly payment without considering the total cost or your overall budget.

Not Reading the Fine Print: Loan agreements can be dense and filled with jargon. However, skipping the fine print can lead to unpleasant surprises down the line, such as hidden fees, prepayment penalties, or unfavorable clauses. Take your time, and if necessary, have a trusted advisor review it.

Ignoring the Total Cost of the Loan: Focus on the Annual Percentage Rate (APR) and the total amount you will pay over the life of the loan, not just the monthly payment. A lower monthly payment over a longer term often means paying significantly more in interest overall.

Pro Tips from an Expert

Based on my experience in the financial sector, here are some invaluable insights to help you succeed:

-

Be Patient and Persistent: Securing a car loan without a traditional job can take time and effort. You might face rejections, but don’t give up. Learn from each interaction and refine your approach. Your persistence will pay off.

-

Start Small (Cheaper Car): Instead of aiming for your dream car, consider a more affordable, reliable used vehicle for your first loan. A smaller loan amount is less risky for lenders and easier for you to manage. Successfully paying off a smaller loan will also build your credit history, making future loans easier to obtain.

-

Consider Transportation Alternatives First: Before committing to a loan, evaluate if public transport, ride-sharing, or borrowing a car temporarily can meet your needs. A car loan is a significant financial commitment; ensure it’s absolutely necessary and the right decision for your current circumstances.

-

Focus on Long-Term Financial Stability: Use this process as a catalyst to strengthen your overall financial health. Work towards building more stable income streams, increasing your savings, and continuously improving your credit score. These actions will not only help with a car loan but with all future financial endeavors.

-

Understand Your Debt-to-Income Ratio: This ratio is crucial. Calculate it accurately and understand how lenders view it. Aim for a DTI below 36% if possible. For more insights on this, you can refer to resources like the Consumer Financial Protection Bureau (CFPB) on Understanding Your Debt-to-Income Ratio. (External Link Placeholder)

Conclusion

Obtaining a car loan with no job is undoubtedly a challenging endeavor, but as this comprehensive guide illustrates, it is far from impossible. By understanding the lender’s perspective, meticulously documenting all forms of non-traditional income, bolstering your credit score, and exploring a range of financing options, you significantly enhance your chances of approval.

Remember, success in this journey hinges on preparation, transparency, and patience. It requires you to be your own best advocate, presenting a compelling financial story backed by solid evidence. While the path may have its hurdles, with the right strategy and a proactive approach, you can navigate the complexities of securing a car loan and achieve the mobility you need. Your financial future is a marathon, not a sprint; make wise choices today that pave the way for a stable tomorrow.