Navigating Chemical Bank Used Car Loan Rates: Your Ultimate Guide to Smart Financing

Navigating Chemical Bank Used Car Loan Rates: Your Ultimate Guide to Smart Financing Carloan.Guidemechanic.com

Embarking on the journey to purchase a used car can be an exciting prospect, offering a fantastic balance between affordability and reliability. For many, financing that purchase through a trusted institution like Chemical Bank becomes a crucial step. Understanding the intricacies of used car loan rates, particularly what influences them and how to secure the best possible terms, is absolutely essential. This comprehensive guide will illuminate the path, helping you navigate Chemical Bank’s used car loan landscape with confidence and expertise.

Buying a used car isn’t just about saving money on the initial purchase; it’s also about smart financial planning for the long haul. Used cars often depreciate slower than new ones, making them a wise investment for many drivers. However, securing the right financing can significantly impact the overall cost of your vehicle.

Navigating Chemical Bank Used Car Loan Rates: Your Ultimate Guide to Smart Financing

This article serves as your definitive resource, designed to equip you with the knowledge needed to make informed decisions. We’ll delve deep into every aspect, from what shapes your interest rate to mastering the application process, ensuring you drive away with not just a great car, but also a great loan.

Why Consider Chemical Bank for Your Used Car Loan?

When it comes to financing a significant purchase like a car, choosing the right lender is paramount. Chemical Bank, like many established financial institutions, offers a range of benefits that can make it an attractive option for your used car loan. Their reputation, stability, and potential for competitive offerings often draw in prospective borrowers.

Based on my experience in the financial landscape, working with a reputable bank provides a sense of security and transparency that might not always be present with smaller, less established lenders. This peace of mind is invaluable when committing to a multi-year loan. Chemical Bank, or any similar well-regarded bank, typically operates under stringent regulations, offering a layer of protection for consumers.

One of the primary advantages of opting for a bank like Chemical Bank is the potential for competitive interest rates. While rates are always individualized based on various factors, established banks often have the capacity to offer favorable terms, especially to borrowers with strong credit profiles. They aim to attract and retain customers, and competitive loan products are a key part of that strategy.

Beyond rates, the quality of customer service and the availability of resources are significant considerations. Many large banks offer personalized assistance, whether through dedicated loan officers or comprehensive online support. This can be incredibly helpful if you have questions during the application process or need guidance on managing your loan account.

Understanding Used Car Loan Rates: What Drives the Numbers?

The interest rate you receive on a used car loan isn’t a random figure; it’s a carefully calculated number influenced by a multitude of factors. Understanding these elements is crucial because it empowers you to take steps to improve your eligibility for the best possible rates. Knowing what lenders, including Chemical Bank, consider will help you prepare and potentially save thousands over the life of your loan.

From our perspective, many borrowers mistakenly believe that all loan rates are the same, or that a single factor determines their eligibility. In reality, it’s a dynamic interplay of personal financial health, market conditions, and even the specifics of the vehicle you intend to purchase. Let’s break down the key drivers.

Your Credit Score: The Cornerstone of Your Rate

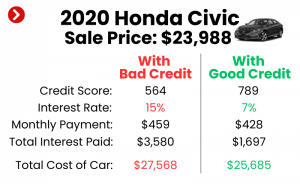

Without a doubt, your credit score stands as the most influential factor in determining the interest rate you’ll be offered for a used car loan. Lenders, including Chemical Bank, use this three-digit number as a quick snapshot of your financial reliability and your history of managing debt. A higher credit score signals lower risk to the lender.

Individuals with excellent credit scores (generally 720 and above) are typically offered the lowest interest rates because they have a proven track record of repaying their debts responsibly. Conversely, a lower credit score indicates a higher risk, prompting lenders to charge higher interest rates to compensate for that perceived risk. This isn’t punitive; it’s a risk management strategy.

Before you even begin shopping for a car or a loan, a pro tip from us is to check your credit score and review your credit report. You can obtain a free copy of your credit report from each of the three major credit bureaus annually. This allows you to identify any errors that might be negatively impacting your score and dispute them before applying for a loan.

Loan Term Length: Short vs. Long

The length of your loan, known as the loan term, is another significant factor that impacts both your monthly payment and the total interest you’ll pay. Loan terms for used cars typically range from 24 to 72 months, and sometimes even longer. Choosing a term involves a trade-off between lower monthly payments and higher overall costs.

A shorter loan term, for example, 36 or 48 months, usually comes with a lower interest rate. Your monthly payments will be higher, but you’ll pay off the loan faster and incur less total interest over time. This is because the lender’s money is at risk for a shorter period.

Conversely, a longer loan term, such as 60 or 72 months, will result in lower monthly payments, making the car seem more affordable in the short term. However, longer terms almost always come with higher interest rates, and you’ll end up paying significantly more in total interest over the life of the loan. Common mistakes to avoid include extending the loan term solely to achieve a lower monthly payment without considering the increased total cost.

Down Payment: Lowering Your Risk, Lowering Your Rate

Making a substantial down payment on your used car can have a very positive impact on the interest rate you qualify for. A down payment reduces the amount of money you need to borrow, which in turn lowers the lender’s risk. When you have more equity in the car from the start, you are less likely to default on the loan.

From a lender’s perspective, a larger down payment demonstrates your financial commitment to the purchase. It signals that you have been able to save money and are serious about owning the vehicle. This perceived lower risk often translates into more favorable interest rates and better loan terms.

Beyond just the rate, a significant down payment can also prevent you from being "upside down" on your loan, a situation where you owe more than the car is worth. This is particularly relevant for used cars, which can continue to depreciate. Aiming for at least a 10-20% down payment is a smart financial strategy.

Vehicle Age and Mileage: Lenders’ Perspective

The specific used car you plan to purchase also plays a role in the loan rate offered by lenders like Chemical Bank. The age, mileage, and overall condition of the vehicle are factors that influence its resale value and the likelihood of mechanical issues. Lenders consider these aspects when assessing their risk.

Older vehicles with higher mileage generally carry more risk for lenders. They are more prone to mechanical breakdowns, which could impact your ability to make payments if unexpected repair costs arise. They also tend to depreciate faster, making it harder for the lender to recoup their investment if the loan defaults.

As a result, loans for very old or high-mileage vehicles might come with higher interest rates or more restrictive terms. Some lenders may even have limits on the age or mileage of vehicles they are willing to finance. It’s important to clarify these policies with Chemical Bank or any potential lender upfront.

Debt-to-Income Ratio: Ensuring Affordability

Your debt-to-income (DTI) ratio is another critical metric that lenders use to evaluate your financial health. This ratio compares your total monthly debt payments to your gross monthly income. It essentially tells the lender how much of your income is already committed to other debts, indicating your capacity to take on new obligations.

A lower DTI ratio suggests that you have more disposable income available to comfortably manage a new car loan payment. Lenders typically prefer a DTI ratio below 36%, though some might go slightly higher depending on other compensating factors. A high DTI ratio, conversely, signals that you might be overextended financially.

Chemical Bank will likely scrutinize your DTI ratio to ensure that adding a car loan won’t strain your finances to an unsustainable degree. This is a measure designed to protect both you and the lender from financial hardship. Keeping your existing debts manageable is a powerful way to prepare for a new loan application.

Market Conditions: Interest Rate Fluctuations

Finally, broader economic factors and market conditions also influence used car loan rates. The federal funds rate set by the Federal Reserve, inflation rates, and the overall supply and demand for credit in the economy all play a part. These external forces are largely beyond your control but are important to acknowledge.

When the Federal Reserve raises its benchmark interest rate, it typically leads to an increase in interest rates across various loan products, including auto loans. Conversely, a cut in the federal funds rate can lead to lower borrowing costs. These shifts can affect the rates offered by all lenders, including Chemical Bank.

Staying informed about general economic trends and interest rate forecasts can give you a better sense of when might be an opportune time to apply for a loan. While you can’t control these factors, understanding them helps set realistic expectations for the rates you might receive.

The Chemical Bank Used Car Loan Application Process: A Step-by-Step Walkthrough

Applying for a used car loan with Chemical Bank, or any financial institution, can seem daunting, but it’s a straightforward process when you know what to expect. Being prepared and understanding each stage can significantly streamline your experience and increase your chances of approval for favorable terms. Our pro tip is always to approach the application with thoroughness and transparency.

Preparation is Key: Gathering Your Documents

Before you even fill out the application form, gather all necessary documentation. This proactive step saves time and prevents delays in the approval process. Lenders need specific information to verify your identity, income, and financial stability.

Common documents you’ll likely need include:

- Proof of Identity: A valid government-issued ID, such as a driver’s license or passport.

- Proof of Income: Recent pay stubs (typically for the last 1-2 months), W-2 forms, or tax returns if you are self-employed.

- Proof of Residence: Utility bills, lease agreements, or mortgage statements to confirm your address.

- Social Security Number: Essential for a credit check.

- Vehicle Information: Details about the used car you intend to purchase, including its VIN (Vehicle Identification Number), make, model, year, and mileage. This is crucial for the lender to assess the collateral.

- Existing Debt Information: Details on other loans or credit cards you hold.

Having these documents organized and readily available will make the application process much smoother. Common mistakes to avoid are waiting until the last minute to gather these, which can lead to unnecessary stress and delays.

Submitting Your Application: Online, In-Branch, or Phone

Chemical Bank typically offers multiple convenient ways to submit your used car loan application. You can choose the method that best suits your preferences and schedule. Each option has its own advantages.

Applying online is often the quickest and most convenient method. You can complete the application from the comfort of your home at any time, uploading documents digitally. This is ideal for those who are tech-savvy and prefer a self-service approach.

Visiting a local branch allows for a more personalized experience. You can speak directly with a loan officer who can answer your questions, guide you through the process, and help you understand the terms. This is particularly beneficial if you prefer face-to-face interaction or have complex financial situations.

Some banks also offer the option to apply over the phone, providing a balance between convenience and direct assistance. Whichever method you choose, ensure you provide accurate and complete information to avoid any potential issues.

The Approval Process: What Lenders Look For

Once your application is submitted, Chemical Bank’s underwriting team will begin their assessment. This involves a comprehensive review of all the information and documents you’ve provided. Their goal is to determine your creditworthiness and the level of risk associated with lending you money.

They will pull your credit report and score, verify your income, confirm your employment history, and calculate your debt-to-income ratio. They will also evaluate the specific vehicle you intend to purchase, considering its age, mileage, and market value to ensure it serves as adequate collateral for the loan.

The approval process can take anywhere from a few hours to a few business days, depending on the complexity of your application and the bank’s current volume. During this time, the lender may contact you for additional information or clarification. Promptly responding to these requests can expedite the process.

Understanding Your Offer: APR, Monthly Payment, Total Cost

Upon approval, Chemical Bank will present you with a loan offer detailing the terms and conditions. It’s absolutely crucial to thoroughly understand every aspect of this offer before you sign anything. Don’t just focus on the monthly payment; look at the bigger picture.

- Annual Percentage Rate (APR): This is the most important number to focus on. The APR represents the true annual cost of your loan, encompassing both the interest rate and any additional fees. A lower APR means a lower overall cost for your loan. Compare APRs, not just interest rates, when evaluating offers.

- Monthly Payment: This is the amount you will pay each month. Ensure it fits comfortably within your budget without stretching your finances too thin.

- Loan Term: Reconfirm the length of the loan (e.g., 60 months) and understand its implications for total interest paid.

- Total Cost of the Loan: This figure represents the sum of all your monthly payments over the entire loan term. It’s the ultimate indicator of how much the car will truly cost you after financing.

Common mistakes include only looking at the monthly payment and neglecting the APR or total cost. A seemingly low monthly payment over an extended term can hide a much higher total cost due to increased interest. Always ask for the total cost of the loan and compare this across different offers.

Pro Tips for Securing the Best Chemical Bank Used Car Loan Rates

Getting a used car loan is more than just applying and hoping for the best; it’s about strategic preparation and smart decision-making. Based on my experience, proactive steps can significantly improve your chances of securing the most favorable Chemical Bank used car loan rates. These insights are designed to empower you as a borrower.

1. Improve Your Credit Score

As discussed, your credit score is king. Before applying for any loan, dedicate time to boosting your score if it’s not in the excellent range. Pay all your bills on time, reduce outstanding credit card balances, and avoid opening new lines of credit. Even small improvements can lead to better rates.

2. Save for a Larger Down Payment

The more you put down upfront, the less you need to borrow, and the less risk the lender takes. Aim for at least 10-20% of the car’s purchase price. A significant down payment often translates directly into lower interest rates and more flexible loan terms from Chemical Bank.

3. Shop Around for Rates (Even Within Chemical Bank)

While you might be set on Chemical Bank, it’s wise to get pre-approved offers from a few different lenders. This gives you leverage and a benchmark. Even within Chemical Bank, discussing different loan products or terms with a loan officer can sometimes uncover better options. Having multiple offers in hand allows you to choose the most competitive one.

4. Consider a Co-signer

If your credit score is less than ideal, or if you’re a first-time borrower with limited credit history, a co-signer with excellent credit can significantly improve your chances of approval and secure a lower interest rate. A co-signer shares responsibility for the loan, reducing the lender’s risk. Ensure both parties understand the full implications of co-signing.

5. Negotiate the Car Price First

Separate the car negotiation from the loan negotiation. Focus on getting the best possible price for the used car before you discuss financing. When these two processes are blended, it’s easy to lose track of where you might be overpaying. Once you have a firm price, then apply for your loan with Chemical Bank.

Common Pitfalls to Avoid When Financing a Used Car

Navigating the used car loan process can have its challenges, and it’s easy to fall into common traps that can cost you money and cause unnecessary stress. Being aware of these pitfalls is the first step toward avoiding them. Our pro tips highlight these crucial areas.

Not Checking Your Credit Report

One of the biggest mistakes borrowers make is not reviewing their credit report before applying. Errors on your report can unfairly lower your score, leading to higher interest rates. Always get your free annual credit reports and dispute any inaccuracies well in advance.

Skipping Pre-approval

Applying for pre-approval from Chemical Bank or other lenders is a powerful tool. It gives you a clear idea of how much you can borrow and at what interest rate before you even step onto a dealership lot. This strengthens your negotiating position, allowing you to focus on the car’s price rather than worrying about financing.

Extending the Loan Term Too Long

While a longer loan term offers lower monthly payments, it almost always means paying significantly more in total interest. It also increases the risk of being "upside down" on your loan, where the car is worth less than you owe. Aim for the shortest loan term you can comfortably afford.

Ignoring the Total Cost of the Loan

As mentioned, focusing solely on the monthly payment is a common pitfall. Always look at the Annual Percentage Rate (APR) and the total amount you will pay over the life of the loan. A slight difference in APR can translate to thousands of dollars in savings over several years.

Falling for Add-ons

Dealerships often try to sell various add-ons like extended warranties, GAP insurance, or paint protection. While some might be beneficial, others are overpriced or unnecessary. Be firm in declining add-ons you don’t want or need, especially if they are rolled into your loan, increasing your total debt and interest.

Used Car Loans vs. New Car Loans: A Comparison

The decision between buying a new or used car often comes down to budget and priorities. When it comes to financing, there are distinct differences between new and used car loans that are important to understand. Chemical Bank offers both, but the terms and rates can vary significantly.

New Car Loans:

- Pros: Generally lower interest rates (due to lower perceived risk), longer loan terms available, manufacturer incentives and rebates, brand-new car with no history of issues.

- Cons: Rapid depreciation (especially in the first few years), higher purchase price, higher insurance costs.

Used Car Loans:

- Pros: Lower purchase price, slower depreciation, lower insurance costs, wider selection of models within budget.

- Cons: Potentially higher interest rates (depending on car age/mileage and borrower credit), shorter loan terms for older vehicles, unknown vehicle history (though CARFAX/AutoCheck helps), potential for more repairs.

Ultimately, the choice depends on your financial situation, driving habits, and what you value most in a vehicle. Used car loans from Chemical Bank can be an excellent way to get a reliable vehicle without the significant financial burden of new car depreciation.

Frequently Asked Questions About Chemical Bank Used Car Loans

To further clarify the process and address common concerns, here are answers to some frequently asked questions regarding used car loans, applicable to Chemical Bank or similar institutions.

Q: Can I get pre-approved for a used car loan from Chemical Bank?

A: Yes, absolutely. Chemical Bank, like most major lenders, encourages pre-approval. Getting pre-approved gives you a clear understanding of your borrowing power and interest rate before you shop, which can significantly streamline the car-buying process.

Q: What’s the minimum credit score required for a Chemical Bank used car loan?

A: While there isn’t a single "minimum" score that guarantees approval, most traditional banks prefer applicants with a credit score in the good to excellent range (typically 670 or higher). However, they may still offer loans to individuals with lower scores, though usually at higher interest rates or with stricter terms.

Q: Does Chemical Bank finance private party used car sales?

A: Many banks, including Chemical Bank, do offer financing for private party sales, but the requirements can be stricter than for dealership purchases. You’ll likely need to provide more documentation about the vehicle, such as a clear title, inspection reports, and a bill of sale. It’s best to confirm their specific policies directly with Chemical Bank.

Q: What if I have bad credit? Can I still get a loan?

A: While challenging, it’s not impossible. If you have bad credit, Chemical Bank might still consider your application, possibly with a higher interest rate, a larger down payment requirement, or the need for a co-signer. Alternatively, they might have specific programs or refer you to their personal loan options. It’s always worth discussing your situation with a loan officer.

Q: Can I refinance my existing used car loan with Chemical Bank?

A: Yes, refinancing is often an option. If your credit score has improved since you first took out your loan, or if market rates have dropped, refinancing with Chemical Bank could potentially lower your interest rate and monthly payments. It’s a smart move to explore if your current loan terms are less favorable.

Final Thoughts: Driving Away with Confidence

Securing a used car loan from Chemical Bank doesn’t have to be a complex or intimidating process. By understanding the factors that influence your interest rates, meticulously preparing your application, and proactively seeking the best terms, you can confidently navigate the financing landscape. Remember, knowledge is your most powerful tool in this journey.

Your used car loan is a significant financial commitment, and approaching it with a well-informed strategy will pay dividends for years to come. Focus on improving your credit, making a solid down payment, and always scrutinizing the total cost of the loan, not just the monthly payment. With these strategies in mind, you’re well on your way to making a smart financial decision.

We encourage you to reach out to Chemical Bank directly to discuss their current used car loan rates and explore options tailored to your specific financial situation. Armed with the insights from this guide, you are now better equipped to engage in those conversations and secure a loan that truly works for you. Drive away not just with a great car, but with peace of mind knowing you made an excellent financial choice.

For further reading on smart auto financing, consider exploring resources from trusted financial education bodies. For example, the Consumer Financial Protection Bureau offers excellent, unbiased information on understanding auto loans and your rights as a borrower.