Navigating Financial Crossroads: Your Comprehensive Guide to Car Loan Extension

Navigating Financial Crossroads: Your Comprehensive Guide to Car Loan Extension Carloan.Guidemechanic.com

Life throws curveballs. One moment you’re cruising, confidently making your car loan payments, and the next, an unexpected expense or a sudden shift in income leaves you scrambling. When faced with financial strain, the thought of missing an auto loan payment can be daunting, bringing fears of late fees, credit score damage, or even repossession. This is precisely where a car loan extension can come into play, offering a potential lifeline when you need it most.

As an expert in automotive financing and debt management, I’ve seen countless individuals grapple with these very challenges. This article is designed to be your ultimate, in-depth guide to understanding car loan extensions – what they are, when they’re beneficial, their potential pitfalls, and how to navigate the process. Our goal is to equip you with the knowledge to make an informed decision, ensuring you maintain your financial stability and keep your wheels turning.

Navigating Financial Crossroads: Your Comprehensive Guide to Car Loan Extension

What Exactly is a Car Loan Extension? Unpacking the Details

At its core, a car loan extension is a temporary agreement between you and your lender to modify the original terms of your auto loan. Specifically, it involves lengthening the repayment period. When you extend your car loan, the remaining balance is spread out over a longer duration than initially agreed upon, which in turn reduces the amount you owe each month.

Think of it like this: if you had 24 months left on a loan with a $400 monthly payment, an extension might stretch that to 36 months, potentially bringing your monthly payment down to, say, $280. It’s a mechanism designed to provide relief during periods of financial difficulty, allowing borrowers to adjust their budgets without immediately defaulting on their vehicle. This differs significantly from refinancing, which often involves getting a new loan with potentially different interest rates from a new or existing lender. With an extension, you’re simply adjusting the timeline of your current loan.

When Should You Consider a Car Loan Extension? Identifying the Right Moment

Deciding whether to pursue a car loan extension isn’t a decision to take lightly. It’s often a tactical move best employed during specific financial circumstances. Based on my experience, it’s typically considered when a borrower faces a temporary, but significant, disruption to their income or an unexpected financial obligation.

For instance, a sudden job loss, a medical emergency, or an unforeseen major home repair can quickly deplete savings and make regular car payments unsustainable. In these situations, an extension can provide crucial breathing room. It prevents you from missing payments, which could severely damage your credit score and potentially lead to the car being repossessed. It’s important to stress that this is usually a short-term solution for a short-term problem, not a permanent fix for chronic financial instability. If your financial struggles are long-term, other solutions might be more appropriate.

The Benefits: Why Extending Your Car Loan Can Be a Smart Move

When facing financial headwinds, a car loan extension can offer several compelling advantages that provide immediate relief and protect your financial standing. Understanding these benefits is key to appreciating its role as a valuable tool.

-

Lower Monthly Payments: This is arguably the most direct and appealing benefit. By extending the loan term, your remaining balance is spread over more payments, resulting in a reduced amount due each month. This can free up much-needed cash flow, making your budget more manageable during challenging times. For someone facing a tight budget, even a reduction of $50-$100 can make a significant difference.

-

Temporary Financial Relief: An extension offers a vital reprieve from the pressure of high monthly payments. This temporary relief can allow you to address other pressing financial obligations, rebuild your emergency savings, or simply catch your breath while you work to stabilize your income. It’s a way to weather a storm without letting your auto loan sink your ship.

-

Avoidance of Default and Repossession: Missing car payments can lead to severe consequences, including late fees, a significant drop in your credit score, and ultimately, repossession of your vehicle. An extension can help you avoid these detrimental outcomes by making your payments more affordable. Maintaining consistent, albeit lower, payments keeps your account in good standing and protects your asset.

-

Preservation of Your Credit Score: Consistently making on-time payments, even extended ones, is crucial for a healthy credit score. By extending your loan and continuing to pay, you prevent the negative marks associated with missed payments or defaults. While an extension itself might be noted on your credit report, it’s far less damaging than a repossession or a series of late payments.

-

Increased Disposable Income (Short-Term): With lower monthly car payments, you’ll have more money available for other necessities or to put towards building a financial cushion. This increased disposable income, even if temporary, can reduce overall financial stress and provide a sense of control during an otherwise uncertain period.

The Downsides: What Are the Drawbacks of a Car Loan Extension?

While a car loan extension offers immediate relief, it’s crucial to understand that this convenience often comes at a cost. Overlooking these drawbacks can lead to greater financial burden in the long run. Transparency is key when making such a significant financial decision.

-

Increased Total Interest Paid: This is the most significant downside. When you extend the loan term, you’re paying interest for a longer period. Even if your interest rate remains the same, the sheer duration means you’ll accrue and pay substantially more in total interest over the life of the loan. For example, extending a loan by just 12 months could add hundreds, if not thousands, of dollars to your overall cost. It’s essential to calculate this impact before committing.

-

Longer Debt Period: Your car loan will linger on for a longer time. If you initially planned to be debt-free in three years, an extension might push that timeline out to four or five years. This can delay other financial goals, such as saving for a down payment on a home, retirement, or investing. You’re effectively postponing your financial freedom.

-

Potential for Negative Equity: Extending your loan increases the likelihood of being "upside down" on your car, meaning you owe more than the car is worth. Cars depreciate quickly, and by extending your loan, you’re paying off the principal balance at a slower rate while the car continues to lose value. This can create a precarious situation if you need to sell or trade in your vehicle before the loan is fully paid off.

-

Impact on Future Borrowing Capacity: While an extension helps preserve your credit score by preventing default, the extended loan term can still impact your debt-to-income ratio. Lenders assessing future loan applications (e.g., for a mortgage or another car) might view a longer-term auto loan as a higher ongoing commitment, potentially affecting your eligibility or the terms they offer.

-

Fees and Administrative Costs: Some lenders may charge an administrative fee to process a loan extension. While often minor compared to the interest implications, it’s another cost to factor into your decision. Always inquire about any associated fees before agreeing to an extension.

How to Apply for a Car Loan Extension: A Step-by-Step Guide

Applying for a car loan extension doesn’t have to be complicated, but it requires a proactive and organized approach. Following these steps can help streamline the process and increase your chances of approval.

-

Assess Your Current Financial Situation: Before contacting your lender, take an honest look at your finances. Determine exactly how much you can realistically afford to pay each month. Understand if your financial hardship is temporary or long-term. This clarity will help you articulate your needs effectively to your lender.

-

Contact Your Lender Immediately: Don’t wait until you’ve missed a payment. As soon as you anticipate difficulty, reach out to your auto loan provider. Many lenders are more willing to work with proactive borrowers. Explain your situation clearly and express your desire to avoid default. You can usually find their customer service number on your loan statements or their website.

-

Understand Your Lender’s Policies: Not all lenders offer extensions, and those that do will have specific criteria. Inquire about their extension programs, eligibility requirements, and any associated fees. Ask if they offer a "deferment" (skipping payments and adding them to the end of the loan) or a true "extension" (recalculating the remaining payments over a longer period).

-

Gather Necessary Documentation: Your lender will likely request documents to verify your financial hardship. This could include proof of income reduction (e.g., termination letter, reduced hours), medical bills, or other relevant financial statements. Having these ready will expedite the application process.

-

Review and Understand the New Terms: If approved, your lender will provide you with new loan terms. Pro tips from us: Always read the fine print carefully. Pay close attention to the new monthly payment, the new total loan term, and most importantly, the total interest you will pay over the extended period. Ask for a written breakdown of the original versus the extended loan costs.

-

Sign the Agreement: Once you fully understand and agree to the revised terms, sign the necessary paperwork. Ensure you keep copies of all documents for your records. Remember, this is a legally binding modification to your original loan agreement.

Common Mistakes to Avoid When Extending Your Car Loan

While an extension can be a lifesaver, certain missteps can turn a helpful solution into a bigger problem. Being aware of these common pitfalls can help you navigate the process more effectively.

-

Not Understanding the True Cost: One of the most common mistakes is focusing solely on the lower monthly payment without considering the increased total interest. Always ask your lender for the total cost of the loan both before and after the extension. This transparency is vital for making an informed decision.

-

Ignoring Alternatives: An extension isn’t the only solution. Common mistakes to avoid are jumping straight to an extension without exploring other options like refinancing your car loan for a lower interest rate, selling the car, or even negotiating with your lender for a temporary forbearance.

-

Waiting Too Long to Act: Delaying action until you’ve already missed payments significantly reduces your options and damages your credit. Lenders are much more willing to work with borrowers who are proactive and communicate their difficulties before a problem escalates. Early communication is key.

-

Not Reading the Fine Print: Never sign an agreement without thoroughly reading and understanding every clause. Pay attention to any new fees, changes in interest rates (though less common with extensions), or specific conditions related to the extension. If anything is unclear, ask for clarification.

-

Extending for the Wrong Reasons: An extension is best for temporary financial setbacks. If you’re consistently struggling to afford your car payments, even with an extension, it might indicate a deeper financial issue or that you purchased a car beyond your means. Using an extension as a permanent solution to an ongoing problem will likely lead to further debt.

Alternatives to a Car Loan Extension: Exploring Other Paths

A car loan extension is one tool in your financial toolkit, but it’s not the only one. Depending on your specific circumstances, other strategies might be more beneficial or cost-effective in the long run.

-

Refinancing Your Car Loan: This involves taking out a new loan, often with a different lender, to pay off your existing car loan. If your credit score has improved since you first bought the car, or if interest rates have dropped, you might qualify for a lower interest rate or a more favorable loan term. This could reduce your monthly payments without significantly increasing the total interest paid, unlike an extension.

-

Selling the Car: If your financial struggles are severe and long-term, selling the vehicle might be the most responsible decision. This can eliminate the debt entirely, freeing up your budget. However, be mindful of negative equity; if you owe more than the car is worth, you’ll need to pay the difference out of pocket.

-

Paying Extra on Principal (When Able): While seemingly counter-intuitive when discussing financial difficulty, if your situation improves quickly, consider making extra payments towards the principal balance. This can help offset the additional interest accrued during the extension period and get you back on track faster.

-

Debt Consolidation: If you have multiple high-interest debts, consolidating them into a single, lower-interest loan (like a personal loan) could simplify payments and potentially reduce your overall interest burden. However, this often requires good credit and careful planning.

-

Temporary Forbearance: Some lenders might offer a temporary forbearance, allowing you to skip one or two payments, with those payments then added to the end of your loan term. This is similar to an extension but often for a shorter, more defined period.

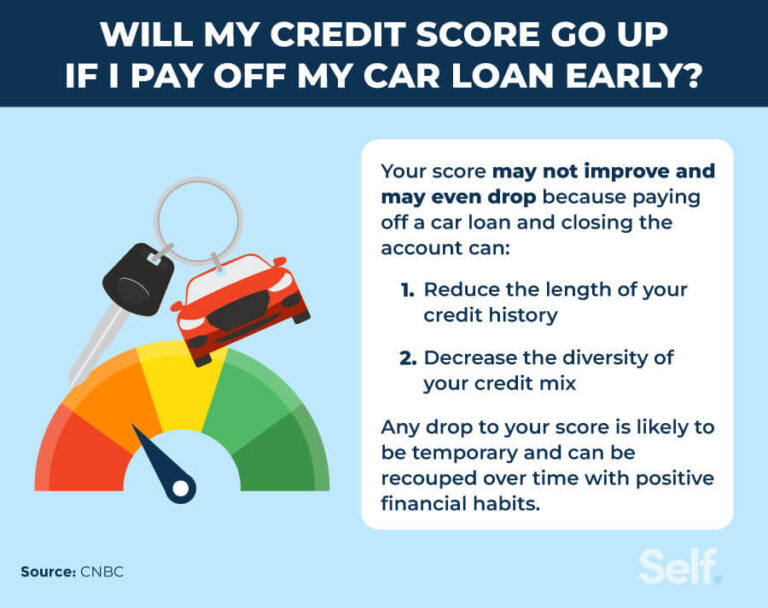

Impact on Your Credit Score: What to Expect

The impact of a car loan extension on your credit score is nuanced. It’s generally less damaging than missing payments or defaulting, but it’s not entirely without consequence.

On the positive side, successfully extending your loan and continuing to make all your new, lower payments on time will help maintain or even improve your payment history, which is the most significant factor in your credit score. This prevents the severe negative impact of late payments, collections, or repossession.

However, an extension might be noted on your credit report as a modification to the original loan terms. While this isn’t inherently negative, it could be viewed by future lenders as a sign that you experienced financial difficulty. It also lengthens the period you carry debt, which can affect your credit utilization ratio over time. The key is to avoid missed payments at all costs; an extension is a tool to help you achieve that. For more detailed information on how loan modifications can affect credit, you can consult resources from the Consumer Financial Protection Bureau (CFPB), a trusted external source for consumer financial information.

Is a Car Loan Extension Right for You? Making an Informed Decision

Ultimately, the decision to extend your car loan is a personal one, heavily dependent on your unique financial circumstances. There’s no one-size-fits-all answer, but by carefully weighing the pros and cons, you can make an informed choice that aligns with your financial goals.

Consider if your financial hardship is genuinely temporary. If you expect your income to rebound or your expenses to decrease within a few months, an extension could provide the necessary bridge. If, however, you’re facing long-term financial instability, an extension might merely postpone the inevitable and increase your overall debt burden. It’s crucial to look beyond the immediate relief of lower payments and consider the long-term financial implications.

Weigh the added interest against the immediate relief. Is the cost of extending worth avoiding default and maintaining your credit? Sometimes, the answer is a resounding yes. Other times, exploring alternatives like refinancing or even selling the vehicle might be the more prudent long-term strategy. Don’t hesitate to consult with a financial advisor who can offer personalized guidance based on your specific situation.

Conclusion: Empowering Your Financial Journey

A car loan extension can be a valuable tool for managing temporary financial difficulties, offering a much-needed reduction in monthly payments and safeguarding your credit. However, like any financial instrument, it comes with its own set of trade-offs, particularly the increased total interest paid over the life of the loan.

By understanding what a car loan extension entails, when it’s appropriate, and what alternatives exist, you empower yourself to make intelligent financial decisions. Proactive communication with your lender, thorough research, and a clear understanding of your financial outlook are paramount. Remember, your financial journey is unique, and taking the time to explore all options will lead to the best possible outcome for you and your vehicle.