Navigating Golden 1 Credit Union Car Loan Rates: Your Ultimate Guide to Smart Auto Financing

Navigating Golden 1 Credit Union Car Loan Rates: Your Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

Securing a car loan can feel like navigating a complex maze, especially when you’re trying to find the best rates and terms. For many Californians, Golden 1 Credit Union stands out as a beacon of member-focused financial services. But what exactly do their car loan rates entail, and how can you ensure you’re getting the best possible deal?

This comprehensive guide will demystify Golden 1 Credit Union car loan rates, providing you with an in-depth understanding of everything from application to approval. Our goal is to equip you with the knowledge and strategies to confidently finance your next vehicle, turning a potentially stressful process into a smooth, informed journey. Get ready to unlock the secrets to smart auto financing with Golden 1.

Navigating Golden 1 Credit Union Car Loan Rates: Your Ultimate Guide to Smart Auto Financing

What Exactly is Golden 1 Credit Union, and Why Does it Matter for Your Car Loan?

Before diving into the specifics of car loan rates, it’s crucial to understand the foundation of Golden 1 Credit Union. Unlike traditional banks, which are for-profit entities answerable to shareholders, Golden 1 is a not-for-profit financial cooperative. This fundamental difference significantly impacts how they operate and, most importantly, how they serve their members.

As a credit union, Golden 1 is owned by its members. This means that instead of maximizing profits for external shareholders, their primary focus is on providing financial benefits back to their members. These benefits often manifest in the form of lower loan rates, higher savings rates, and fewer fees compared to commercial banks.

For anyone seeking an auto loan, this structure translates into a tangible advantage. Golden 1’s mission is to help its members thrive financially, and that commitment is often reflected in highly competitive Golden 1 Credit Union car loan rates. By understanding this core principle, you can appreciate the unique value proposition they offer in the auto financing landscape.

The Credit Union Advantage: Why Golden 1 Stands Out for Auto Loans

Choosing a credit union like Golden 1 for your car loan offers several distinct benefits that often surpass what traditional banks or dealership financing can provide. These advantages are rooted in their member-centric philosophy and operational model.

Firstly, credit unions are renowned for their personalized service. When you apply for a loan at Golden 1, you’re not just a number; you’re a co-owner of the institution. This often leads to more flexible lending decisions and a willingness to work with members through various financial situations.

Secondly, and perhaps most importantly for car buyers, credit unions typically offer more favorable interest rates. Because they aren’t driven by profit margins for shareholders, they can pass on savings directly to their members in the form of lower Annual Percentage Rates (APRs). This can significantly reduce the total cost of your vehicle over the life of the loan.

Finally, Golden 1, like many credit unions, emphasizes financial education and community support. They often provide resources to help members improve their financial literacy and make sound decisions, which is invaluable when making a significant purchase like a car. This holistic approach makes them a strong contender for your auto financing needs.

Understanding Golden 1 Car Loan Rates: The Core Concept

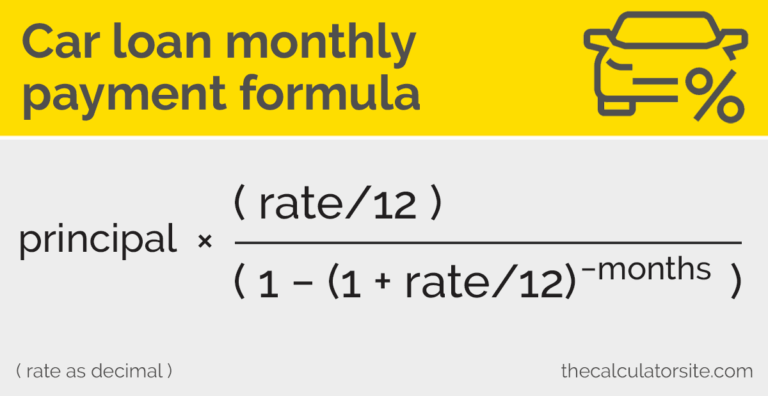

At its heart, a car loan rate is the cost you pay to borrow money for your vehicle. When you see Golden 1 Credit Union car loan rates advertised, they represent the Annual Percentage Rate (APR) at which you’ll repay the borrowed sum, in addition to the principal amount. This rate is not a one-size-fits-all figure; it’s highly individualized.

The advertised rates you see are typically the lowest possible rates offered to applicants with excellent credit scores and specific loan terms. It’s important to remember that your actual rate will be determined by a combination of factors unique to your financial profile and the specifics of the loan itself.

Therefore, while these advertised rates provide a good benchmark, your personal rate might differ. Understanding the variables that influence your specific offer is key to securing the most favorable terms possible from Golden 1 Credit Union.

How Your Rate is Determined: Key Influencing Factors

Several critical elements come into play when Golden 1 Credit Union calculates your specific car loan rate. Being aware of these factors allows you to proactively work towards improving your standing and securing a better deal.

1. Your Credit Score: This is arguably the most significant factor. A higher credit score signals to lenders that you are a reliable borrower with a history of responsible debt management. Applicants with excellent credit (typically 720+) will qualify for the lowest advertised Golden 1 Credit Union car loan rates.

Conversely, a lower credit score indicates a higher risk, leading to a higher interest rate to compensate the lender for that perceived risk. Based on my experience, focusing on improving your credit score before applying can yield substantial savings over the life of the loan.

2. Loan Term: The length of your repayment period plays a crucial role. Shorter loan terms (e.g., 36 or 48 months) generally come with lower interest rates because the lender’s risk is reduced over a shorter period. While monthly payments will be higher, the total interest paid will be less.

Longer loan terms (e.g., 60, 72, or even 84 months) result in lower monthly payments, making the car more "affordable" on a month-to-month basis. However, they almost always come with higher interest rates and mean you’ll pay significantly more in total interest over the life of the loan.

3. Loan Amount & Down Payment: The total amount you need to borrow impacts the lender’s risk assessment. A larger loan amount, especially relative to your income, might lead to a slightly higher rate. Conversely, making a substantial down payment reduces the amount you need to finance.

A larger down payment also signals financial stability and reduces the lender’s exposure, often resulting in a more attractive interest rate. Pro tips from us: Aim for at least a 10-20% down payment if possible, as it demonstrates commitment and lowers your overall loan-to-value (LTV) ratio.

4. Vehicle Type (New vs. Used): Lenders often view new car loans as less risky than used car loans. New vehicles typically hold their value better initially, and their depreciation is more predictable. As a result, new car loans often come with slightly lower interest rates than used car loans.

Used cars, especially older models, can have higher interest rates due to their greater depreciation, potential for mechanical issues, and less predictable resale value. However, Golden 1 still offers competitive rates for both, so it’s always worth checking their specific offerings.

Types of Golden 1 Car Loans: Finding Your Perfect Match

Golden 1 Credit Union provides a diverse range of auto loan options designed to meet various member needs. Understanding these categories will help you identify the best fit for your next vehicle purchase.

New Car Loans

If you’re eyeing a brand-new vehicle, Golden 1’s new car loans are tailored for you. These loans typically apply to vehicles that are current model year or up to one or two years old, often with very low mileage.

New car loans from Golden 1 usually feature their most competitive Golden 1 Credit Union car loan rates, reflecting the lower risk associated with financing a new asset. They often come with flexible terms and a straightforward application process, making them an attractive option for first-time new car buyers.

Used Car Loans

Purchasing a pre-owned vehicle is a popular and often more budget-friendly choice. Golden 1 offers robust used car loan options for vehicles that are several years old. While the rates might be slightly higher than new car loans, they remain highly competitive compared to other lenders.

The terms for used car loans can vary based on the age and mileage of the vehicle. Golden 1 will typically have specific guidelines regarding the maximum age or mileage they will finance, so it’s wise to check these details before you start shopping.

Auto Loan Refinancing

Perhaps you already have a car loan but are looking for a better deal. Golden 1’s auto loan refinancing option allows you to replace your current loan with a new one, potentially at a lower interest rate or with more favorable terms. This can be incredibly beneficial if your credit score has improved since you first took out your loan, or if market rates have dropped.

Refinancing your auto loan with Golden 1 could lead to lower monthly payments, significant savings on interest over time, or a shorter repayment period. It’s a smart move for anyone looking to optimize their existing auto financing.

Lease Buyout Loans

At the end of a car lease, you often have the option to purchase the vehicle. Golden 1 offers lease buyout loans to facilitate this process. These loans cover the residual value of the car, allowing you to transition from leasing to owning.

This can be a great option if you love your leased car and want to avoid the hassle of finding a new one. Golden 1’s lease buyout loans provide a clear path to ownership with competitive rates, turning a temporary vehicle into a permanent one.

The Golden 1 Car Loan Application Process: A Step-by-Step Guide

Applying for a car loan with Golden 1 Credit Union is a straightforward process, but understanding each step can ensure a smooth experience. Preparation is key to a successful application.

Step 1: Membership Requirements

First and foremost, to obtain a loan from Golden 1, you must be a member. Golden 1 Credit Union serves individuals who live or work in California. If you meet this general requirement, becoming a member is usually a simple process, often involving opening a savings account with a small initial deposit.

You can typically apply for membership online or at a branch. Once you’re a member, you gain access to all their financial products, including their competitive auto loans.

Step 2: Get Pre-Approved

One of the most powerful steps you can take is getting pre-approved for a loan. Pre-approval means Golden 1 has reviewed your financial information and tentatively approved you for a specific loan amount at an estimated interest rate. This is a soft credit pull, which won’t impact your credit score.

Pro tips from us: Obtaining pre-approval gives you immense negotiating power at the dealership. You walk in knowing exactly how much you can afford and what your interest rate will be, effectively allowing you to negotiate the car price as a cash buyer. This separation of car price and financing negotiation is invaluable.

Step 3: Gather Required Documents

Before or during your application, you’ll need to provide several documents. While the exact list may vary, common requirements include:

- Proof of identity (driver’s license, state ID)

- Proof of residence (utility bill, lease agreement)

- Proof of income (pay stubs, tax returns, employment verification)

- Vehicle information (for an existing car you want to refinance, or details of the car you plan to buy if known)

- Social Security Number

Having these documents ready will significantly speed up your application. Common mistakes to avoid are not having recent pay stubs or incomplete tax returns, which can cause delays.

Step 4: Submit Your Application

You can apply for a Golden 1 car loan online, over the phone, or in person at one of their branches. The online application is often the quickest and most convenient option, allowing you to apply from anywhere.

During the application, you’ll provide personal, employment, and financial details. Be thorough and accurate to avoid any discrepancies that could delay approval.

Step 5: Loan Review and Approval

Once submitted, Golden 1 will review your application, perform a hard credit inquiry (which may slightly impact your credit score), and verify your information. They will then notify you of their decision.

If approved, you’ll receive the final loan terms, including your specific interest rate, loan amount, and repayment schedule. Carefully review all terms before signing.

Demystifying Golden 1 Car Loan Rates: What to Look For Beyond the Number

While the interest rate is a critical component, a truly smart car loan decision involves looking at the bigger picture. Several other factors influence the true cost and convenience of your Golden 1 Credit Union car loan.

APR vs. Interest Rate

It’s essential to understand the difference between the interest rate and the Annual Percentage Rate (APR). The interest rate is simply the cost of borrowing the principal amount. The APR, however, includes the interest rate plus any additional fees associated with the loan, expressed as an annual percentage.

The APR provides a more accurate representation of the total annual cost of your loan. When comparing loan offers, always compare the APR, not just the interest rate, for a true apples-to-apples comparison.

Loan Terms: Short vs. Long

As discussed, the length of your loan term profoundly impacts your monthly payments and the total interest paid. A shorter term (e.g., 36 or 48 months) means higher monthly payments but less interest overall.

A longer term (e.g., 60, 72, or 84 months) offers lower monthly payments, which can seem attractive. However, you’ll pay significantly more in total interest and risk owing more than the car is worth (being "upside down" on your loan) as depreciation outpaces your principal payments.

Down Payment Impact

A larger down payment directly reduces the amount you need to borrow, thereby decreasing your monthly payments and the total interest you’ll pay. It also improves your loan-to-value (LTV) ratio, often qualifying you for better rates.

Common mistakes to avoid are putting down too little or no down payment. While tempting for immediate affordability, it dramatically increases your total loan cost and risk.

Fees and Charges

Always inquire about any potential fees associated with the loan. While credit unions are known for fewer fees, it’s still wise to confirm. Look for origination fees, application fees, or prepayment penalties.

Golden 1 is generally transparent about its fee structure, but a thorough review of the loan agreement ensures no surprises. Being informed about all potential costs is part of being a savvy borrower.

Pro Tips for Securing the Best Golden 1 Car Loan Rates

Getting the most favorable Golden 1 Credit Union car loan rates isn’t just about applying; it’s about strategic preparation and smart decision-making. Based on my experience in the financial world, these pro tips can significantly improve your chances.

1. Boost Your Credit Score: Before you even think about applying, check your credit report. Address any errors and work to improve your score. Pay down existing debts, make all payments on time, and avoid opening new lines of credit. Even a 20-30 point increase can move you into a better rate tier.

2. Save for a Larger Down Payment: As discussed, a substantial down payment reduces the loan amount and signals financial responsibility. Aim for at least 10-20% of the vehicle’s price. This not only lowers your monthly payments but can also qualify you for a lower APR.

3. Opt for a Shorter Loan Term if Possible: While longer terms offer lower monthly payments, they come with higher overall interest costs. If your budget allows, choose the shortest loan term you can comfortably afford. This will save you thousands in interest over time.

4. Get Pre-Approved Before You Shop: This is a game-changer. Getting pre-approved by Golden 1 before stepping onto a dealership lot gives you a concrete loan offer in hand. You’ll know your maximum loan amount and interest rate, allowing you to negotiate the car price with confidence, separate from the financing.

5. Understand Your Budget Beyond the Monthly Payment: Don’t just focus on the monthly payment. Calculate the total cost of the loan, including all interest. Factor in insurance, maintenance, and fuel costs as well. A holistic view prevents future financial strain.

6. Leverage Your Golden 1 Relationship: If you’re an existing Golden 1 member with a good financial history with them, don’t hesitate to mention it. Your established relationship might give you a slight edge or additional flexibility in terms.

Common Mistakes to Avoid When Applying for a Car Loan

Even with the best intentions, car loan applicants can fall into common traps. Avoiding these pitfalls will save you time, money, and stress.

1. Not Checking Your Credit Score: A common mistake is to apply for a loan without knowing your credit standing. This leaves you vulnerable to unexpected rejections or higher rates. Always get a free copy of your credit report from AnnualCreditReport.com and review it thoroughly before applying.

2. Skipping Pre-Approval: As emphasized, pre-approval is your superpower. Common mistakes to avoid are going straight to the dealership and letting them handle all the financing. This puts you at a disadvantage, as they might mark up interest rates or push less favorable terms.

3. Focusing Only on Monthly Payments: Dealerships often try to anchor you to a "comfortable" monthly payment. While important, it shouldn’t be your sole focus. A lower monthly payment might mean a longer loan term and significantly more interest paid over time. Always ask for the total cost of the loan.

4. Ignoring the Total Cost of the Loan: Beyond the monthly payment, consider the total amount you will pay back, including all interest. A loan that seems affordable monthly might be surprisingly expensive overall. Always crunch the numbers.

5. Not Comparing Offers: Even if you love Golden 1, it’s wise to compare their offer with at least one or two other reputable lenders. This ensures you’re getting the most competitive rate available for your profile. For more insights on securing the best financing, check out our guide on .

Comparing Golden 1 with Other Lenders: A Strategic Approach

While Golden 1 Credit Union offers compelling advantages, it’s always smart to understand their position relative to other types of lenders. This strategic comparison ensures you’re making the most informed decision.

Banks vs. Credit Unions

Traditional banks, while offering convenience and a wide range of services, are profit-driven. Their loan rates might be higher than credit unions because they need to generate returns for shareholders. Credit unions like Golden 1, being member-owned, often pass profits back to members in the form of lower rates and fees.

However, banks may have more lenient membership requirements. If you don’t qualify for Golden 1 membership, a bank might be your next best option.

Online Lenders

Online lenders have emerged as a strong force, offering speed and convenience. They often have streamlined application processes and can sometimes provide competitive rates. However, they may lack the personalized service and community focus that Golden 1 provides.

Always read reviews and ensure any online lender is reputable. Their rates can vary widely, so thorough comparison is crucial.

Dealer Financing

Dealerships often offer their own financing or work with a network of lenders. While this can be convenient, it’s crucial to be cautious. Dealerships sometimes mark up interest rates to increase their profit margins.

Pro tips from us: Always arrive at the dealership with a pre-approval from Golden 1 (or another independent lender). This gives you leverage and a benchmark against which to compare any dealer-offered financing. Never let the dealer be your only source of financing.

Beyond the Rate: Other Benefits of Golden 1 Auto Loans

While Golden 1 Credit Union car loan rates are a major draw, the benefits of financing with them extend far beyond just the numbers. These additional perks contribute to a more positive and secure borrowing experience.

Firstly, Golden 1 offers truly personalized service. As a member, you’re not just a transaction; you’re part of their community. This often translates to more understanding and flexible support, especially if you encounter financial difficulties during your loan term.

Secondly, their commitment to financial education is invaluable. Golden 1 frequently provides resources and advice to help members make sound financial decisions, which can be incredibly helpful for managing a car loan and other aspects of your finances. Discover other strategies to optimize your vehicle purchase in our article, .

Finally, the inherent community focus of a credit union means your money stays within and supports local initiatives. Choosing Golden 1 isn’t just a financial decision; it’s a vote for a community-driven financial institution. This external link to Golden 1 Credit Union’s official website can provide more direct information on their offerings and community involvement.

Conclusion: Driving Towards Smart Auto Financing with Golden 1

Navigating the world of car loans can be daunting, but with the right knowledge, you can secure a deal that perfectly fits your financial goals. Golden 1 Credit Union stands out as a strong contender for anyone in California seeking a fair, transparent, and member-focused auto financing solution.

By understanding how Golden 1 Credit Union car loan rates are determined, preparing thoroughly for your application, and leveraging their unique credit union advantages, you empower yourself to make a truly smart decision. Remember to focus on your credit score, save for a solid down payment, get pre-approved, and always consider the total cost of the loan.

Embark on your next vehicle purchase with confidence, knowing you have the insights to secure the best possible Golden 1 Credit Union car loan rates. Your journey to a new car, financed intelligently, starts now.