Navigating LMCU Car Loan Rates: Your Expert Guide to Securing the Best Auto Financing

Navigating LMCU Car Loan Rates: Your Expert Guide to Securing the Best Auto Financing Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is exciting, but securing the right financing can often feel like navigating a complex maze. For many, Lake Michigan Credit Union (LMCU) stands out as a beacon of member-focused service and potentially competitive rates. As an expert blogger and professional SEO content writer, I’ve delved deep into the world of auto financing, and understanding LMCU car loan rates is a topic that consistently surfaces for those seeking value and reliability.

This comprehensive guide is designed to be your ultimate resource, providing an in-depth look at LMCU car loan rates, what influences them, how to apply, and crucial tips for securing the most favorable terms. Our goal is to empower you with the knowledge to make informed decisions, ensuring your vehicle ownership dream becomes a financially sound reality.

Navigating LMCU Car Loan Rates: Your Expert Guide to Securing the Best Auto Financing

Why Choose LMCU for Your Car Loan? The Credit Union Advantage

Before we dive into the specifics of LMCU car loan rates, it’s essential to understand the fundamental difference between a credit union and a traditional bank. Lake Michigan Credit Union, like other credit unions, is a not-for-profit financial cooperative owned by its members. This unique structure directly translates into benefits for you, the borrower.

Member-Centric Philosophy: Unlike banks that focus on shareholder profits, credit unions prioritize their members’ financial well-being. This often means they can offer more competitive interest rates on loans and higher returns on savings accounts. Based on my experience, this core philosophy is a significant reason why many savvy consumers turn to credit unions for their financing needs.

Personalized Service: LMCU prides itself on its community roots and personalized approach. When you apply for a car loan, you’re not just a number; you’re a member. This can lead to a more supportive application process and tailored solutions that fit your individual financial situation. It’s this human touch that often makes the borrowing experience less daunting.

Community Investment: By choosing LMCU, you’re also supporting an institution that reinvests its earnings back into the community and its members through better rates and services. This creates a virtuous cycle that benefits everyone involved. The collective strength of members allows for financial products that truly serve their needs.

Deconstructing LMCU Car Loan Rates: What Factors Are at Play?

Understanding the precise LMCU car loan rates you might qualify for involves more than just glancing at a published chart. Several critical factors converge to determine your individual interest rate. Grasping these elements is your first step towards securing the best possible auto financing.

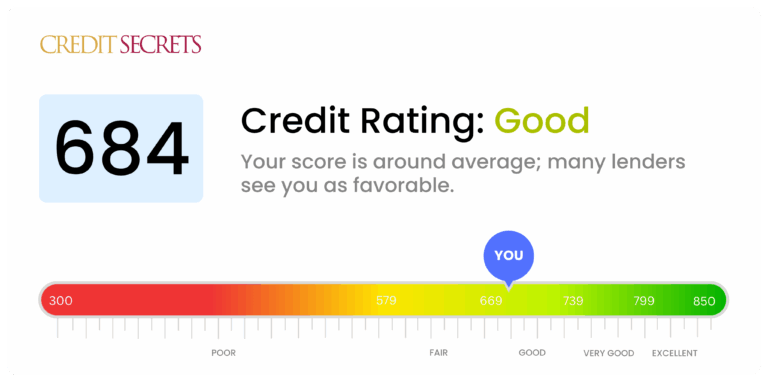

1. Your Credit Score: The Cornerstone of Your Rate

Without a doubt, your credit score is the most significant determinant of the interest rate you’ll be offered. Lenders, including LMCU, use this three-digit number to assess your creditworthiness and the perceived risk of lending to you. A higher credit score signals a lower risk, typically translating into lower interest rates.

Credit Score Tiers:

- Excellent (780-850): Borrowers in this tier usually qualify for the absolute best LMCU car loan rates, often the lowest advertised rates. They demonstrate a consistent history of responsible borrowing and repayment.

- Good (670-779): Most applicants fall into this category. You’ll still receive very competitive rates, though perhaps not the rock-bottom rates reserved for the excellent tier. This range shows a strong likelihood of repayment.

- Fair (580-669): While you can still obtain a loan, your interest rates will likely be higher to compensate for the increased risk. LMCU might look more closely at your overall financial picture.

- Poor (Below 580): Securing a car loan can be more challenging, and if approved, the interest rates will be significantly higher. This indicates a history of missed payments or high debt.

Pro Tip from us: Before even thinking about applying, check your credit score and report from all three major bureaus (Experian, Equifax, TransUnion). Correct any errors you find, as these could negatively impact your rate. Understanding where you stand is crucial for setting realistic expectations and strategizing.

2. The Loan Term: Length Matters for Your Wallet

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). While a longer term might offer a lower monthly payment, it almost always results in paying more interest over the life of the loan.

Shorter Terms (e.g., 36-48 months): These usually come with lower interest rates because the lender’s risk is reduced over a shorter period. Your monthly payments will be higher, but you’ll save a substantial amount on interest.

Longer Terms (e.g., 60-84 months): These terms provide lower monthly payments, making a more expensive car seem affordable. However, LMCU car loan rates for longer terms are typically higher, and you’ll pay significantly more in total interest. Based on my observations, many borrowers gravitate towards longer terms for lower payments without fully realizing the long-term cost.

3. New vs. Used Vehicle: A Subtle Difference in Rates

Generally, new cars tend to have slightly lower interest rates than used cars. This is primarily due to the lower perceived risk associated with new vehicles – they typically have a higher resale value and are less likely to require immediate costly repairs. Used cars, especially older models, carry a higher risk for lenders.

However, LMCU is known for offering competitive rates across both new and used vehicle categories. It’s always worth comparing the specific rates for the car you’re interested in.

4. Loan-to-Value (LTV) Ratio and Down Payment

The Loan-to-Value (LTV) ratio compares the amount you’re borrowing to the vehicle’s appraised value. A lower LTV, meaning you’re borrowing less relative to the car’s value, is favorable to lenders. This is where a substantial down payment comes into play.

Benefits of a Down Payment:

- Lower LTV: Reduces the risk for LMCU, potentially leading to a better interest rate.

- Reduced Loan Amount: Decreases your monthly payments and the total interest paid.

- Instant Equity: You start with equity in your car, protecting you against depreciation.

Common mistakes to avoid are stretching your budget to the absolute limit and not putting down a sufficient down payment. This can leave you "upside down" on your loan, owing more than the car is worth, especially in the early years of ownership.

5. Membership History and Relationship with LMCU

While not always explicitly stated, your existing relationship with Lake Michigan Credit Union can sometimes influence the rates or terms you receive. Long-standing members with multiple accounts (checking, savings, other loans) might be seen as more reliable borrowers. This demonstrates a commitment to the credit union.

Understanding Current LMCU Car Loan Rates: What to Expect

It’s crucial to understand that specific LMCU car loan rates are dynamic and fluctuate based on market conditions, the prime rate, and the factors discussed above. Therefore, I cannot provide exact real-time rates in this article.

However, I can offer general guidance based on industry trends and LMCU’s reputation:

- Competitive Edge: LMCU consistently aims to offer rates that are competitive, often beating those from large national banks, thanks to its credit union structure.

- Rate Tiers: Expect rates to be presented in tiers, primarily dictated by your credit score (e.g., "as low as X% for excellent credit").

- Promotional Rates: Keep an eye out for special promotions LMCU might offer, such as lower rates for specific vehicle types (e.g., electric vehicles) or during certain times of the year.

- Official Source is Key: The most accurate and up-to-date LMCU car loan rates will always be found directly on their official website or by contacting one of their loan officers. This ensures you’re getting information tailored to the current market and LMCU’s specific offerings.

The LMCU Car Loan Application Process: A Step-by-Step Guide

Applying for an auto loan with Lake Michigan Credit Union is a straightforward process, especially if you come prepared. Here’s a breakdown of what to expect:

Step 1: Become an LMCU Member (If You Aren’t Already)

As a credit union, LMCU serves its members. If you’re not already a member, you’ll need to join. Membership is typically open to individuals who live, work, worship, or attend school in Michigan’s Lower Peninsula, or who are family members of an existing LMCU member. Joining usually involves opening a savings account with a small initial deposit.

Step 2: Get Pre-Approved for Your Loan

This is a step I cannot emphasize enough. Securing LMCU loan pre-approval is one of the smartest moves you can make in your car-buying journey.

What is Pre-Approval? It means LMCU has reviewed your credit and financial information and has conditionally approved you for a specific loan amount at an estimated interest rate. This is usually valid for a certain period, typically 30-60 days.

Why is Pre-Approval Crucial?

- Budget Clarity: You know exactly how much you can afford, preventing you from falling in love with a car outside your price range.

- Negotiating Power: You walk into the dealership with your own financing, turning you into a cash buyer. This allows you to negotiate the car price separately from the financing, often leading to a better deal.

- Saves Time: Speeds up the buying process at the dealership.

- Compares Rates: You can compare LMCU’s pre-approved rate with any financing offered by the dealership, ensuring you get the best deal.

Pro Tip: Be aware that pre-approval often involves a "hard inquiry" on your credit report, which can slightly ding your score. However, multiple hard inquiries for the same type of loan within a short window (typically 14-45 days, depending on the credit bureau) are usually treated as a single inquiry, so shop around for rates within that timeframe. For more details, consider reading our (link to internal article).

Step 3: Gather Your Documents

Having your paperwork ready streamlines the application process. While specific requirements can vary, generally you’ll need:

- Personal Identification: Driver’s license or state ID.

- Proof of Income: Recent pay stubs, W-2s, or tax returns (for self-employed individuals).

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Vehicle Information (if you’ve chosen a car): VIN, make, model, year, mileage, and purchase price.

Step 4: Submit Your Application

You can typically apply for an LMCU car loan in several ways:

- Online: The most convenient method, available 24/7.

- By Phone: Speak directly with an LMCU loan officer.

- In-Person: Visit an LMCU branch to discuss your options face-to-face.

Step 5: Approval and Funding

Once your application is approved, LMCU will provide you with the final loan terms and disclosures. You’ll then sign the necessary documents, and the funds will be disbursed. If you have pre-approval, this final step is usually very quick.

Pro Tips for Securing the Best LMCU Car Loan Rates

Even with LMCU’s competitive offerings, there are strategies you can employ to further enhance your chances of securing the most favorable auto loan rates.

- Elevate Your Credit Score: This cannot be overstressed. Pay all your bills on time, keep credit card balances low, and avoid opening new credit lines just before applying for a car loan. Even a 20-point increase can sometimes move you into a better rate tier. Based on my experience, focusing on credit health is the single most impactful action.

- Save for a Larger Down Payment: As discussed, a larger down payment reduces the loan amount and the LTV, making you a less risky borrower. Aim for at least 10-20% of the vehicle’s purchase price if possible.

- Keep Your Loan Term Realistic: While lower monthly payments are appealing, resist the temptation to stretch your loan over 7 or 8 years if you can comfortably afford a shorter term. You’ll save thousands in interest and build equity faster.

- Consider a Co-Signer (If Necessary): If your credit score is fair or you have a limited credit history, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower rate. Ensure both parties understand the responsibilities involved.

- Leverage Your Pre-Approval: Use your LMCU loan pre-approval as a powerful negotiation tool at the dealership. They may try to beat LMCU’s rate or offer attractive financing packages, but you’ll have a solid baseline to compare against.

- Explore Refinancing Options: If you already have a car loan with another lender at a higher interest rate, or if your credit score has improved significantly since you first bought your car, LMCU might offer competitive refinancing options. Refinancing an existing loan can potentially lower your monthly payments or reduce the total interest you’ll pay. This is a common strategy many borrowers overlook.

Common Mistakes to Avoid When Applying for an LMCU Car Loan

Navigating the auto loan landscape can be tricky, and even seasoned borrowers can make missteps. Here are some common mistakes I’ve observed over the years that you should actively avoid:

- Not Checking Your Credit Report: Assuming your credit is in good standing without verifying it is a significant oversight. Errors on your report can unfairly inflate your interest rate. Always check your credit report well in advance.

- Skipping Pre-Approval: As highlighted, entering a dealership without pre-approval from LMCU or another lender puts you at a disadvantage. You lose negotiating power and might end up with less favorable terms.

- Focusing Solely on the Monthly Payment: While important, an obsession with the lowest possible monthly payment can lead to longer loan terms and significantly higher total interest paid. Always consider the total cost of the loan.

- Borrowing More Than You Can Afford: It’s easy to get carried away with a shiny new car. Create a realistic budget and stick to it, accounting for not just the monthly payment but also insurance, fuel, and maintenance.

- Ignoring Additional Fees: Be aware of any origination fees, documentation fees, or other charges associated with the loan. LMCU is transparent, but it’s always wise to review all disclosures carefully.

Beyond the Rate: Other LMCU Benefits for Car Owners

While competitive LMCU car loan rates are a primary draw, Lake Michigan Credit Union often offers additional services that can benefit car owners and enhance the overall value of your financing package.

- GAP (Guaranteed Asset Protection) Coverage: If your car is totaled or stolen, your insurance payout might be less than what you still owe on the loan due to depreciation. GAP coverage bridges this "gap," preventing you from being upside down on a car you no longer have. LMCU typically offers this at a reasonable cost.

- Payment Protection: Life can be unpredictable. LMCU may offer payment protection plans that can help cover your loan payments in the event of unforeseen circumstances like disability, involuntary unemployment, or death.

- Auto Insurance Services: As a full-service financial institution, LMCU often partners with insurance providers or has its own agency to help you secure competitive auto insurance rates, sometimes offering discounts for members.

These additional offerings underscore LMCU’s commitment to providing comprehensive financial solutions, not just standalone loan products.

Conclusion: Your Road to Affordable Auto Financing with LMCU

Securing a car loan is a significant financial decision, and understanding LMCU car loan rates is a critical step towards making an informed choice. Lake Michigan Credit Union stands out as a strong contender in the auto financing landscape, offering competitive rates, personalized service, and a member-focused approach that often surpasses what traditional banks can provide.

By understanding the factors that influence your interest rate – primarily your credit score, loan term, and down payment – and by diligently preparing for the application process, you put yourself in the best position to secure favorable terms. Remember to prioritize pre-approval, gather your documents, and always review all loan disclosures carefully.

We hope this comprehensive guide has illuminated the path to obtaining your next vehicle with confidence. Don’t hesitate to visit LMCU’s official website or contact their loan specialists directly for the most current rates and to begin your application. Your journey to affordable auto financing with Lake Michigan Credit Union starts now!