Navigating My Car Loan: Your Ultimate Guide to Smart Auto Financing

Navigating My Car Loan: Your Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

The thrill of a new car is undeniable – the fresh scent, the gleaming paint, the promise of new adventures on the open road. For most of us, turning that dream into a reality involves securing a car loan. It’s a significant financial commitment, and understanding the ins and outs of "my car loan" journey is paramount to making smart decisions and avoiding costly pitfalls.

This comprehensive guide is designed to empower you with the knowledge needed to navigate the complex world of auto financing. We’ll delve deep into every aspect, from preparing your finances to managing your loan responsibly, ensuring you secure the best possible terms for your vehicle. By the end of this article, you’ll be well-equipped to approach your car loan with confidence, clarity, and control.

Navigating My Car Loan: Your Ultimate Guide to Smart Auto Financing

Understanding Car Loans: The Basics of "My Car Loan" Journey

At its core, a car loan is a sum of money borrowed from a financial institution to purchase a vehicle. You agree to repay this amount, known as the principal, along with an additional charge for borrowing the money, called interest, over a predetermined period, or term. This repayment is typically made through fixed monthly installments.

Most car loans are "secured loans." This means the car itself acts as collateral for the loan. Should you fail to make your payments as agreed, the lender has the legal right to repossess the vehicle to recover their losses. Understanding this fundamental aspect is crucial, as it highlights the importance of responsible repayment.

When you’re exploring "my car loan" options, several key terms will frequently come up. The principal is the initial amount of money you borrow. The interest rate is the percentage charged by the lender for the use of their money, usually expressed as an Annual Percentage Rate (APR), which includes some fees in addition to the base interest rate. Finally, the loan term is the duration, typically measured in months, over which you agree to repay the loan. A longer term might mean lower monthly payments, but often results in paying more interest over the life of the loan.

Preparing for Your Car Loan Application: Laying the Groundwork

Securing a favorable car loan begins long before you even step foot into a dealership or submit an application. Thorough preparation is the cornerstone of a successful and affordable financing experience. By taking the time to get your financial house in order, you can significantly improve your chances of approval and secure better terms.

Your Credit Score: The Unseen Force Behind "My Car Loan"

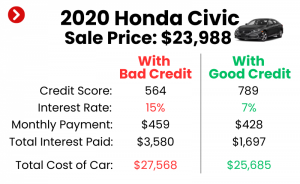

Your credit score is arguably the most critical factor lenders consider when evaluating "my car loan" application. It’s a three-digit number that reflects your creditworthiness, essentially telling lenders how reliable you are at repaying debts. A higher credit score signals lower risk, which typically translates to lower interest rates and more favorable loan terms.

Based on my experience, many applicants overlook the profound impact of their credit score. Lenders use it to determine not just whether to approve your loan, but also the interest rate they’ll offer. A difference of even a few points can save you hundreds, if not thousands, of dollars over the life of the loan. Therefore, checking your credit report and score well in advance is a non-negotiable step.

If your score isn’t where you want it to be, take steps to improve it. Pay down existing debts, make all payments on time, and avoid opening new credit accounts right before applying for a car loan. For a deeper dive into improving your credit, you might find our guide on incredibly helpful.

Budgeting Beyond the Monthly Payment: What Can I Truly Afford?

It’s tempting to focus solely on the monthly payment when considering a car loan, but this can be a dangerous oversight. A truly responsible budget accounts for the total cost of car ownership, which extends far beyond the loan installment. This holistic approach ensures that your new vehicle doesn’t become a financial burden.

Before even looking at cars, determine a realistic budget for your entire car-related expenses. This includes not only your potential car loan payment but also insurance premiums, fuel costs, routine maintenance, and unexpected repairs. Failing to factor these into your budget can lead to financial strain down the road.

A significant down payment can dramatically reduce the amount you need to borrow, thereby lowering your monthly payments and the total interest paid. Aim for at least 10-20% of the vehicle’s purchase price if possible. This also helps reduce the risk of becoming "upside down" on your loan, where you owe more than the car is worth.

Researching Your Ride: New vs. Used and Loan Implications

The type of vehicle you choose directly impacts your loan options and overall cost. New cars typically come with lower interest rates but depreciate rapidly, meaning their value drops significantly the moment you drive them off the lot. Used cars, while often having higher interest rates, have already absorbed the initial depreciation hit, offering potentially better long-term value.

Consider the reliability and projected maintenance costs of different models. A seemingly cheap car might become expensive due to frequent repairs. Your choice between new and used should align with your budget and long-term financial goals, as it will shape the nature of "my car loan." For a comprehensive comparison, check out our insights on .

Gathering Your Arsenal of Documents: Be Prepared

When it’s time to apply for "my car loan," having all your necessary documents readily available will streamline the process. Lenders require specific information to verify your identity, income, and residence. Being organized shows preparedness and can expedite your application.

Typically, you’ll need a valid driver’s license, proof of income (such as recent pay stubs or tax returns if self-employed), proof of residence (utility bill or lease agreement), and bank statements. If you have a trade-in, you’ll also need its title or lien information. Having these documents ready avoids delays and potential frustration.

Finding the Right Car Loan: Where to Look and What to Compare

Once your finances are in order, the next step is to find the best car loan for your needs. The lending landscape is diverse, offering various options beyond just the dealership. Smart comparison shopping is key to uncovering the most competitive rates and terms available to you.

The Diverse Lending Landscape for "My Car Loan"

You have several avenues to explore when seeking "my car loan." Traditional banks are a common choice, offering competitive rates to customers with good credit. Credit unions, known for their member-focused approach, often provide highly competitive rates and more flexible terms, especially for those with excellent credit or established relationships. Pro tip: Always check with your local credit union; their rates can sometimes beat larger banks.

Dealership financing is convenient, as you can arrange the loan at the point of sale. However, dealers often act as intermediaries, working with multiple lenders and sometimes marking up interest rates for their own profit. Online lenders have emerged as a popular option, offering quick pre-approvals and competitive rates, often with a streamlined digital application process. Exploring all these options before committing is crucial.

The Art of Comparison Shopping: Beyond the Monthly Payment

When comparing loan offers, resist the temptation to focus solely on the monthly payment. While important, it doesn’t tell the whole story. The Annual Percentage Rate (APR) is your most important metric, as it represents the true cost of borrowing, encompassing the interest rate plus certain fees. A lower APR directly translates to less money paid over the loan’s term.

Carefully consider the loan term. While a longer term means lower monthly payments, it also means you’ll pay significantly more in interest over time. Conversely, a shorter term has higher monthly payments but saves you money on interest and allows you to pay off the car faster. Balance your budget with your long-term financial goals.

Always scrutinize the fine print for hidden fees, such as origination fees or documentation fees. Also, check for prepayment penalties, which some lenders charge if you pay off your loan early. Ideally, you want a loan without such penalties, giving you the flexibility to pay it down faster if your financial situation improves.

Pre-approval: Your Power Play in "My Car Loan" Negotiations

Getting pre-approved for a car loan before you even start shopping for a vehicle is one of the smartest moves you can make. Pre-approval means a lender has conditionally agreed to lend you a specific amount of money at a particular interest rate, based on your creditworthiness. This gives you immense leverage at the dealership.

With a pre-approval in hand, you walk into the dealership as a cash buyer, knowing exactly how much you can spend and what your interest rate will be. This separates the car-buying negotiation from the financing negotiation. You can then compare the dealer’s financing offer against your pre-approval, ensuring you get the best deal possible. It empowers you to focus on the car’s price, not just the monthly payment.

Navigating the Car Loan Application Process: Steps to Success

Once you’ve found the right lender and are ready to apply for "my car loan," the application process itself requires attention to detail. Understanding each step and knowing what to expect can help you navigate it smoothly and avoid common pitfalls that could jeopardize your approval or lead to less favorable terms.

The Application Itself: Honesty and Accuracy are Key

When filling out your car loan application, accuracy and honesty are paramount. Provide all requested information truthfully and completely. Lenders will verify your income, employment, and other details, so any discrepancies could delay your application or even lead to rejection. Double-check all figures and personal details before submitting.

Be mindful of submitting multiple loan applications within a short period. While comparing rates is smart, too many hard inquiries on your credit report can temporarily lower your score. It’s best to get all your rate shopping done within a concentrated window, typically 14-45 days, as credit bureaus often group these inquiries as a single event for rate shopping purposes.

Decoding the Fine Print: Read Every Word

Once you receive a loan offer, resist the urge to sign immediately. This is the critical juncture where you must read every single word of the loan agreement. Common mistakes to avoid when securing "my car loan" include rushing through this step and failing to fully understand the terms. The document will outline your APR, loan term, total interest paid, monthly payment, and any fees or penalties.

Ensure that all the terms discussed verbally match what is written in the contract. Pay close attention to clauses regarding early repayment, late payment penalties, and default conditions. If anything is unclear, do not hesitate to ask for clarification from the lender. It’s your right to fully understand what you’re signing.

Negotiation: It’s Not Just for the Car Price

Many people assume car loan terms are non-negotiable, but this isn’t always true. Especially if you have a strong credit score and have secured pre-approval from another lender, you may have room to negotiate the interest rate or other terms with the dealership’s finance department. Leverage your pre-approval as a bargaining chip.

Be wary of dealer add-ons that can significantly inflate your loan amount, such as extended warranties, paint protection, or VIN etching. While some of these might offer value, they often come at a premium and can be purchased separately, often for less. Always consider whether these add-ons are truly necessary and if they provide good value for your money before rolling them into your loan.

After "My Car Loan" is Approved: Managing Your Auto Loan Responsibly

Getting your car loan approved is a major milestone, but the journey doesn’t end there. Responsible loan management is crucial to protecting your credit score, minimizing interest paid, and ensuring your new vehicle remains a joy, not a financial burden. Pro tips from us include setting up a robust payment strategy from day one.

Payment Discipline: The Foundation of Good Credit

The most fundamental aspect of managing "my car loan" is making all your payments on time, every time. Late payments can incur fees, negatively impact your credit score, and even lead to repossession in severe cases. Set up automatic payments from your bank account to ensure you never miss a due date.

Consider setting up payment reminders or scheduling payments a few days before the actual due date, just in case there are any processing delays. Consistency is key here; a history of on-time payments will strengthen your credit profile for future financial endeavors.

Understanding Your Statements: Know Where Your Money Goes

Don’t just pay your bill; understand it. Your monthly loan statement provides valuable information about your outstanding balance, how much of your payment went towards principal versus interest, and any fees incurred. Regularly reviewing your statements helps you track your progress and identify any potential discrepancies.

Initially, a larger portion of your payment goes towards interest, gradually shifting more towards the principal as the loan matures. Understanding this amortization schedule can motivate you to make extra payments, especially early in the loan term, to reduce the overall interest paid.

Refinancing: A Second Chance at Better Terms for "My Car Loan"

Life circumstances change, and sometimes, so do interest rates. Refinancing your car loan means taking out a new loan to pay off your existing one, often with a different lender. This can be a smart move if interest rates have dropped, your credit score has significantly improved since you took out the original loan, or if you want to change your loan term (e.g., shorten it to pay less interest, or lengthen it to lower monthly payments).

Before considering refinancing, calculate the potential savings. Factor in any fees associated with the new loan. It’s generally a good idea to refinance if you can secure a significantly lower interest rate or if it helps you achieve a better financial position without incurring excessive costs.

Strategies for Early Payoff: Save on Interest

Paying off "my car loan" early can save you a substantial amount in interest over the loan’s term. If your financial situation allows, consider making extra payments whenever possible. Even small additional amounts can make a big difference, especially if applied early in the loan.

One popular strategy is to make bi-weekly payments. Instead of 12 monthly payments, you make 26 half-payments a year, effectively making one extra full payment annually. This can shave months or even a year off your loan term and save you considerable interest without feeling like a huge financial burden.

Common Questions and Expert Answers About Car Loans

Navigating "my car loan" journey often brings up specific questions. Here are some common inquiries and our expert insights:

-

Q1: What if I have bad credit? Can I still get a car loan?

- A: Yes, it’s often still possible to get a car loan with bad credit, but expect higher interest rates and potentially less favorable terms. Lenders specializing in subprime loans cater to this market. Focus on a larger down payment, consider a co-signer with good credit, and explore options at credit unions. Improving your credit before applying is always the best strategy.

-

Q2: Should I put down a large down payment?

- A: Absolutely, if you can afford it. A larger down payment reduces the principal amount you borrow, which lowers your monthly payments and the total interest paid over the life of the loan. It also helps prevent you from being "upside down" on your loan, where you owe more than the car is worth, especially given rapid vehicle depreciation.

-

Q3: What about extended warranties and other dealer add-ons?

- A: Exercise caution with these. While some extended warranties can offer peace of mind, they are often marked up significantly by dealerships. Research third-party warranty providers and compare costs. For other add-ons like paint protection or fabric treatments, consider if they truly offer value or if you can purchase similar products or services more affordably elsewhere. Never feel pressured to include them in your loan.

-

Q4: Can I sell my car if I still have a loan on it?

- A: Yes, but it requires a few extra steps. You’ll need to pay off the remaining loan balance to get the title from the lender. If the sale price covers the loan, you simply use the proceeds to pay off the loan. If you owe more than the car is worth (you’re "upside down"), you’ll need to cover the difference out of pocket to clear the title. Always inform your lender of your intent to sell.

-

Q5: What is the difference between APR and Interest Rate?

- A: The interest rate is simply the cost of borrowing the principal amount, expressed as a percentage. The Annual Percentage Rate (APR) is a broader measure of the total cost of borrowing, which includes the interest rate plus certain other fees associated with the loan, such as origination fees. APR provides a more accurate picture of the overall cost of "my car loan" than the interest rate alone.

Pro Tips for a Smooth Car Loan Experience

Based on years of observing car loan trends and consumer experiences, here are some invaluable pro tips to ensure your "my car loan" journey is as smooth and cost-effective as possible:

- Don’t Rush the Process: Car buying and loan securing can be exciting, but haste often leads to costly mistakes. Take your time to research, compare, and understand every detail.

- Know Your Credit Before You Go: Get your credit score and report in advance. This knowledge is your power when negotiating and comparing offers.

- Get Pre-approved: This separates the loan negotiation from the car negotiation, giving you significant leverage and clarity on your budget.

- Compare Offers from Multiple Lenders: Don’t settle for the first offer you receive, especially from the dealership. Explore banks, credit unions, and online lenders.

- Focus on the APR, Not Just the Monthly Payment: A low monthly payment might hide a long loan term and high total interest. The APR tells you the true cost.

- Read Every Word of the Contract: Understand all terms, fees, and conditions before you sign. If something is unclear, ask for clarification.

- Consider the Total Cost of Ownership: Factor in insurance, maintenance, fuel, and potential repairs, not just the loan payment, into your budget.

Conclusion: Take Control of "My Car Loan" Journey

Securing "my car loan" is a significant financial step, but it doesn’t have to be daunting. By equipping yourself with knowledge, understanding the process, and making informed decisions, you can navigate the world of auto financing with confidence and secure terms that truly benefit you. Remember, the goal isn’t just to get a car, but to get a car on terms that fit comfortably within your financial landscape.

From understanding your credit score and budgeting effectively to meticulously comparing loan offers and managing your debt responsibly, every step contributes to a successful outcome. Take control of your car loan journey, empower yourself with information, and drive away not just with a new vehicle, but with peace of mind. Your smart choices today will pave the way for a financially sound future.