Navigating Navy Federal Current Car Loan Rates: Your Ultimate Guide to Smart Auto Financing

Navigating Navy Federal Current Car Loan Rates: Your Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is an exciting prospect. For military members, veterans, and their families, one name often stands out as a beacon of trust and exceptional service in the financial world: Navy Federal Credit Union (NFCU). When it comes to securing a car loan, understanding Navy Federal Car Loan Rates is paramount to making an informed and financially sound decision.

This comprehensive guide is designed to be your definitive resource, unraveling the complexities of Navy Federal Auto Loan Rates and equipping you with the knowledge to navigate the application process confidently. We’ll delve deep into what influences these rates, how to secure the best possible terms, and why NFCU continues to be a top choice for so many. Our goal is to empower you with insights that truly add value, helping you drive away with not just a great car, but also a great deal.

Navigating Navy Federal Current Car Loan Rates: Your Ultimate Guide to Smart Auto Financing

Why Choose Navy Federal for Your Car Loan? Unpacking the Member Advantage

Before we dive into the specifics of rates, let’s explore why Navy Federal Credit Union consistently ranks high for auto financing. As a member-owned, not-for-profit financial institution, NFCU operates with a distinct philosophy: putting its members first. This commitment often translates into tangible benefits that set it apart from traditional banks.

One of the primary advantages of opting for a Navy Federal Auto Loan is the consistently competitive rates offered. Unlike some larger commercial banks focused purely on profit, NFCU aims to provide excellent value to its members. This often means lower interest rates, which can save you thousands of dollars over the life of your loan. It’s a significant factor when budgeting for your vehicle.

Beyond the attractive rates, NFCU is renowned for its exceptional member service. Based on my experience, their loan officers are knowledgeable, patient, and genuinely interested in finding the best solution for your individual circumstances. This personalized approach can make a significant difference, especially if you have questions or need guidance through the loan process. They understand the unique financial situations often faced by military families.

Furthermore, Navy Federal offers a wide array of loan products tailored to various needs, ensuring flexibility. Whether you’re eyeing a brand-new sedan, a reliable used truck, or even looking to refinance an existing loan, NFCU likely has a solution. This versatility, combined with their strong commitment to the military community, makes them an incredibly appealing choice for auto financing.

Decoding Navy Federal’s Current Car Loan Rates: What Drives the Numbers?

It’s crucial to understand that Current Navy Federal Car Loan Rates are not static, one-size-fits-all figures. They are dynamic, influenced by a multitude of factors, and ultimately personalized to each applicant. While NFCU strives for competitive pricing, the exact rate you qualify for will depend on several key variables. It’s always best to check the official Navy Federal website for the most up-to-date and personalized rate information.

Key Factors Influencing Your Car Loan Rate

Understanding these factors is the first step toward securing the best possible rate. Each element plays a significant role in how NFCU assesses your risk as a borrower. Let’s break down the most impactful components.

1. Your Credit Score: The Cornerstone of Loan Rates

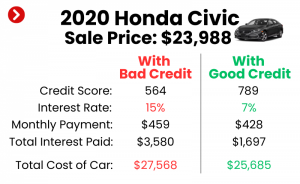

Your credit score is arguably the most critical factor determining your interest rate. A higher credit score signals to lenders that you are a responsible borrower with a history of timely payments. Typically, individuals with excellent credit scores (generally FICO scores above 720-760) will qualify for the lowest Navy Federal Car Loan Rates. Conversely, a lower credit score might result in a higher interest rate, reflecting a greater perceived risk to the lender.

It’s essential to review your credit report before applying for any loan. Identifying and correcting any inaccuracies can significantly improve your score and, consequently, your loan terms. Pro tips from us: Aim for a credit score check at least three months before you plan to apply, giving you time to address any issues.

2. Loan Term: How Long Will You Be Paying?

The loan term, or the length of time you have to repay the loan, directly impacts your interest rate. Shorter loan terms (e.g., 36 or 48 months) generally come with lower interest rates because the lender’s risk exposure is reduced over a shorter period. While shorter terms mean higher monthly payments, they often result in less total interest paid over the life of the loan.

Conversely, longer loan terms (e.g., 72 or 84 months) usually have slightly higher interest rates. These terms offer lower monthly payments, which can be appealing for budgeting, but you’ll end up paying more in total interest. NFCU, like most lenders, balances the convenience of lower payments with the increased cost of a longer repayment period.

3. Vehicle Type: New vs. Used and Age Matters

The type of vehicle you intend to purchase significantly affects the rate. Navy Federal New Car Loan Rates are often lower than Navy Federal Used Car Loan Rates. This is because new cars typically hold their value better initially and present less risk of mechanical issues. Lenders see them as more secure collateral.

For used cars, the age and mileage of the vehicle play a crucial role. Older vehicles or those with very high mileage are generally considered higher risk, leading to higher interest rates. NFCU may also have specific age or mileage limits for used car financing. Understanding these nuances is key to anticipating your potential rate.

4. Loan Amount and Down Payment: Your Financial Commitment

The total amount you wish to borrow and the size of your down payment also influence your rate. A larger down payment reduces the amount you need to finance, thereby lowering the lender’s risk. This can sometimes translate into a more favorable interest rate. It also demonstrates your financial commitment to the purchase.

While NFCU offers 100% financing for qualified members, making a down payment is often a smart financial move. It can reduce your monthly payments, decrease the total interest paid, and help you build equity in your vehicle faster.

5. Automatic Payment Discounts: A Simple Way to Save

Many lenders, including Navy Federal, offer slight interest rate reductions if you agree to set up automatic payments from your checking account. This provides the lender with greater assurance of timely payments. It’s a simple, hassle-free way to shave a few basis points off your rate and ensure you never miss a payment. Always inquire about such discounts when discussing your loan options.

New vs. Used Car Loan Rates at Navy Federal: A Closer Look

The distinction between financing a new car versus a used car is significant when it comes to Navy Federal Auto Loan Rates. While the general factors listed above apply to both, there are specific considerations for each category that impact the final rate.

Understanding Navy Federal New Car Loan Rates

When you’re looking at a brand-new vehicle, the rates tend to be more attractive. Navy Federal New Car Loan Rates are typically lower because new cars are perceived as less risky collateral. They come with manufacturer warranties, have no prior ownership history, and depreciate more predictably in their initial years. Lenders view new cars as more reliable assets, which translates into lower risk premiums for borrowers with good credit.

NFCU’s new car loans often feature competitive rates for various terms, from short 36-month periods to extended 84-month options. The lowest advertised rates are usually reserved for the shortest terms and for borrowers with impeccable credit. It’s also worth noting that special manufacturer incentives, which can sometimes be combined with NFCU financing, might influence your overall cost.

Navigating Navy Federal Used Car Loan Rates

Financing a used car can be a smart financial move, but it often comes with slightly higher interest rates compared to new cars. Navy Federal Used Car Loan Rates reflect the inherent differences in risk associated with pre-owned vehicles. Used cars have already undergone some depreciation, may have higher mileage, and their mechanical history can be less certain.

NFCU, like other lenders, categorizes used cars by age and sometimes mileage. For example, a "late model" used car (e.g., 1-3 years old) might qualify for a rate closer to a new car rate, while an older vehicle (e.g., 5+ years old) will likely carry a higher rate. It’s common for NFCU to have specific guidelines on the maximum age or mileage for vehicles they will finance. For instance, they might not finance vehicles older than 10 years or with more than 125,000 miles. Always confirm these specifics directly with NFCU.

Pro tips from us: When buying a used car, ensure you get a pre-purchase inspection from an independent mechanic. This due diligence can prevent costly surprises down the road and give you peace of mind, regardless of the interest rate. For more insights on securing a reliable pre-owned vehicle, you might find value in our article on The Ultimate Guide to Buying a Used Car Safely (Internal Link Example).

The Navy Federal Car Loan Application Process: A Step-by-Step Guide

Securing an auto loan from Navy Federal is a straightforward process, especially if you’re prepared. Following these steps can help ensure a smooth and efficient experience, bringing you closer to driving your new vehicle.

Step 1: Confirm Your Membership Eligibility

The first and most crucial step is to ensure you are eligible for Navy Federal Credit Union membership. NFCU serves members of the armed forces, veterans, Department of Defense civilians, and their families. If you or a family member falls into one of these categories, you’re likely eligible. If you’re not yet a member, you’ll need to join before applying for a loan. This often involves opening a checking or savings account.

Step 2: Research and Get Pre-Approved

This is perhaps the most powerful step in the car-buying process. Applying for Navy Federal Auto Loans pre-approval offers several significant advantages. It gives you a clear understanding of how much you can afford, the interest rate you qualify for, and your potential monthly payments, all before you even step foot in a dealership.

Pre-approval acts like cash in hand, giving you strong negotiating power at the dealership. You can focus on negotiating the car’s price, rather than getting caught up in financing details. For pre-approval, you’ll typically need to provide personal information, employment details, income, and allow NFCU to perform a credit check. Common mistakes to avoid are not getting pre-approved; this leaves you vulnerable to dealership financing, which might not be as favorable.

Step 3: Find Your Vehicle

With your pre-approval in hand, you’re ready to shop! You can use NFCU’s car buying service, which often partners with dealerships to streamline the process, or you can search independently. Remember your pre-approved loan amount and stick to your budget. Once you find the perfect car, ensure it meets any specific criteria NFCU might have for financing (e.g., age, mileage limits for used cars).

Step 4: Finalize Your Loan

Once you’ve chosen your vehicle, the final step is to finalize the loan with Navy Federal. This involves providing the vehicle’s details (VIN, mileage, sale price) and any remaining required documentation. NFCU will then issue the final loan documents for you to sign. Funds can often be disbursed directly to the dealership, making the purchase seamless.

Beyond the Rate: Other Important Considerations with Navy Federal Auto Loans

While the interest rate is a major component, it’s not the only factor to consider when evaluating Car Loan Rates Navy Federal. Understanding the broader terms and additional offerings can significantly impact your overall financial experience.

Loan Terms: Finding Your Sweet Spot

As discussed, loan terms vary widely, typically from 36 to 84 months. While a longer term can lead to lower monthly payments, it almost always results in paying more interest over time. Conversely, a shorter term means higher monthly payments but less overall interest. It’s crucial to find a balance that fits your budget without unnecessary long-term costs. Based on my experience, many people aim for a 60-month loan as a good compromise between manageable payments and reasonable total interest.

APR vs. Interest Rate: Know the Difference

It’s important to differentiate between the interest rate and the Annual Percentage Rate (APR). The interest rate is the cost of borrowing money, expressed as a percentage. The APR, however, includes the interest rate plus any additional fees associated with the loan, such as administrative fees. The APR provides a more accurate picture of the total annual cost of your loan. NFCU typically advertises APRs, ensuring transparency in their pricing.

Payment Options and Convenience

NFCU offers a variety of convenient payment options. Setting up automatic payments is highly recommended, not just for potential rate discounts, but also to ensure you never miss a payment. They also provide online portals and mobile apps for easy payment management, making it simple to track your loan balance and payment history.

GAP Insurance and Extended Warranties

When discussing your auto loan, NFCU may offer or recommend Guaranteed Asset Protection (GAP) insurance and extended warranties. GAP insurance covers the difference between what you owe on your loan and what your car insurance will pay if your car is totaled or stolen. This can be a wise investment, especially for new cars that depreciate quickly.

Extended warranties, while not directly part of the loan, can be financed with the vehicle. They provide coverage for mechanical breakdowns beyond the manufacturer’s warranty. Carefully weigh the costs and benefits of these add-ons, and remember you are not obligated to purchase them through NFCU if you find better options elsewhere.

Refinancing Options: When to Consider a New Loan

If you already have a car loan with another institution, or if your credit score has significantly improved since you first financed your vehicle, refinancing with Navy Federal could be a smart move. Navy Federal Auto Loans refinancing can potentially lower your interest rate, reduce your monthly payments, or shorten your loan term. It’s always worth exploring if you think you can secure better terms than your current loan.

Maximizing Your Chances for the Best Navy Federal Car Loan Rate

Securing the most favorable Navy Federal Car Loan Rates requires a strategic approach. By focusing on a few key areas, you can significantly improve your chances of getting the best possible deal.

- Improve Your Credit Score: This is foundational. Pay bills on time, reduce outstanding debt, and avoid opening new credit lines just before applying. A strong credit score is your best asset. For more detailed advice on credit, consider reading our article on Understanding Your Credit Score Before Applying for a Loan (Internal Link Example).

- Make a Larger Down Payment: Even a small increase in your down payment can reduce the loan amount and signal financial stability to NFCU, potentially leading to a better rate.

- Choose a Shorter Loan Term: If your budget allows, opting for a shorter loan term will almost always result in a lower interest rate and less total interest paid.

- Set Up Automatic Payments: This is an easy win. Inquire about any rate discounts for setting up direct payments from your Navy Federal account.

- Maintain a Strong Relationship with NFCU: Being a long-standing member with other accounts (checking, savings, credit cards) can sometimes contribute to a more favorable overall financial profile in the eyes of the credit union.

- Negotiate the Car Price, Not Just the Loan Rate: Remember that the total cost of the car and the loan rate both impact your overall expense. Negotiate the vehicle price first, then finalize the financing.

Based on my experience, preparedness is key. The more informed you are about your financial standing and the car market, the better positioned you’ll be to negotiate and secure the best terms for your auto loan.

Conclusion: Drive Away with Confidence with Navy Federal

Navigating the world of auto financing doesn’t have to be daunting, especially when you have a trusted partner like Navy Federal Credit Union. By understanding the factors that influence Navy Federal Car Loan Rates, differentiating between new and used car financing, and preparing for the application process, you empower yourself to make smart financial decisions.

NFCU’s commitment to competitive rates, exceptional member service, and flexible loan options makes them an outstanding choice for military members and their families. Remember, while this guide provides extensive information, the most Current Navy Federal Car Loan Rates will always be found directly on their official website. We strongly encourage you to visit Navy Federal’s Auto Loan Page (External Link) for the latest rates and to begin your pre-approval process.

Arm yourself with knowledge, leverage your membership benefits, and drive away not just in a new car, but with the peace of mind that comes from a well-secured loan. Your journey toward smart auto financing begins here, and Navy Federal is ready to help you every step of the way.