Navigating Regions Used Car Loans: Your Ultimate Guide to Driving Away with Confidence

Navigating Regions Used Car Loans: Your Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

Embarking on the journey to purchase a used car can be both exciting and daunting. While the allure of a new-to-you vehicle is strong, securing the right financing is crucial. For many, a trusted financial institution like Regions Bank comes to mind. Understanding the intricacies of Regions Used Car Loans is the first step toward making an informed decision and driving away with confidence.

This comprehensive guide is designed to cut through the jargon and provide you with an in-depth look at everything you need to know about securing a used car loan through Regions. We’ll explore eligibility, the application process, how to get the best terms, and common pitfalls to avoid. Our goal is to equip you with the knowledge to navigate this process smoothly, ensuring you find a financing solution that fits your budget and lifestyle.

Navigating Regions Used Car Loans: Your Ultimate Guide to Driving Away with Confidence

Why Choose Regions for Your Used Car Loan? Understanding the Benefits

When considering a used car loan, a key decision is choosing the right lender. Regions Bank, a prominent financial institution, offers several compelling reasons for prospective car buyers to consider their financing options. Their approach often blends competitive offerings with a strong focus on customer service and community presence.

A Trusted Financial Partner

Regions Bank has a long-standing history and a significant presence across the Southern, Midwestern, and Texas regions of the United States. This heritage often translates into a sense of trust and reliability for its customers. Choosing a lender with a solid reputation can provide peace of mind throughout the loan term.

Based on my experience in the financial landscape, working with an established bank like Regions often means you’re dealing with well-defined processes and robust customer support. They have a vested interest in maintaining their reputation, which can be a significant advantage if you encounter any issues or have questions down the line. This stability is invaluable when making a large financial commitment like a car loan.

Competitive Rates and Flexible Terms

Regions aims to offer competitive interest rates on its used car loans, which can significantly impact the total cost of your vehicle over time. While rates are influenced by various factors such as your credit score, loan amount, and loan term, Regions strives to be a strong contender in the market. They often provide a range of loan terms, allowing borrowers to choose a payment schedule that aligns with their financial capacity.

Pro tips from us: Always compare the Annual Percentage Rate (APR) from several lenders, not just the interest rate. The APR includes fees and other costs, giving you a truer picture of the loan’s total expense. Regions’ commitment to competitive pricing means you have a good starting point for your comparisons, potentially leading to substantial savings.

Personalized Service

One of the distinct advantages of banking with a regional institution like Regions is the potential for more personalized service. With a network of physical branches, you have the option to speak directly with a loan officer who can walk you through the application process, explain terms, and address your specific concerns. This face-to-face interaction can be particularly beneficial if you prefer a more personal touch or have complex financial questions.

This human element can be incredibly reassuring, especially for first-time car buyers or those who appreciate direct guidance. While online applications are convenient, having the option to sit down with an expert and discuss your situation can provide clarity and build confidence. It’s a level of service that can sometimes be harder to find with purely online lenders.

Convenience and Accessibility

Regions Bank embraces modern banking convenience while maintaining its traditional branch network. You can often apply for a used car loan online, from the comfort of your home, at any time that suits you. They also provide digital tools and mobile banking apps that allow you to manage your loan, make payments, and access account information easily.

This blend of digital convenience and physical accessibility means you can choose the application method that best suits your lifestyle. Whether you’re tech-savvy and prefer an entirely online experience, or you value the option of visiting a branch, Regions aims to make the process as straightforward as possible.

Demystifying Regions Used Car Loan Eligibility: What You Need to Know

Understanding the eligibility criteria for a Regions Used Car Loan is paramount before you even consider applying. Meeting these requirements increases your chances of approval and helps you gauge what kind of rates and terms you might qualify for. Regions, like most lenders, assesses a combination of financial health, personal details, and vehicle specifics.

Credit Score Requirements

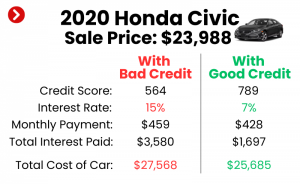

Your credit score is arguably the most significant factor in determining your loan eligibility and the interest rate you’ll receive. Regions will review your FICO score or a similar credit scoring model to assess your creditworthiness. Generally, a higher credit score indicates a lower risk to the lender, resulting in more favorable loan terms.

While Regions doesn’t publicly disclose a minimum credit score, based on industry standards, borrowers with scores in the "good" to "excellent" range (typically 670 and above) will likely qualify for the best rates. Those with fair credit (around 580-669) might still qualify but could face higher interest rates. Pro tip: Always check your credit score and report before applying for a loan. This allows you to identify any errors and understand your standing, giving you time to improve it if necessary. For detailed information on understanding your credit report and scores, a trusted resource like the Consumer Financial Protection Bureau (CFPB) offers comprehensive guidance.

Income and Employment Stability

Lenders need assurance that you have the financial capacity to repay the loan. Regions will require proof of a stable income and employment history. This often involves providing pay stubs, W-2 forms, or tax returns. They will also look at your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income.

A lower DTI ratio indicates that you have more disposable income available to cover your new car loan payments, making you a less risky borrower. Common mistakes to avoid are applying for a loan that would push your DTI ratio too high, as this can signal financial strain to the lender. Ensure your income is consistent and sufficient to comfortably handle the monthly payments alongside your existing financial obligations.

Vehicle Requirements

Not just any used car will qualify for a loan. Regions, like other lenders, has specific criteria for the vehicles they will finance. These often include restrictions on the vehicle’s age, mileage, and sometimes even the make or model. Typically, vehicles that are too old or have excessive mileage are considered higher risk due to potential mechanical issues and depreciation.

Common mistakes to avoid are falling in love with a car that doesn’t meet the lender’s criteria before checking. Always confirm the vehicle’s eligibility with Regions, especially if it’s an older model or has high mileage. The car must also have a clear title, meaning no outstanding liens, and be registered in your name or soon to be.

Residency and Age

Basic personal criteria also apply. You must be a legal resident of the United States and meet the minimum age requirement, typically 18 years old, to enter into a loan agreement. Regions will verify your identity and residency through documents such as a valid driver’s license or state ID. These are standard requirements across virtually all lending institutions.

The Regions Used Car Loan Application Process: A Step-by-Step Walkthrough

Applying for a used car loan can feel complex, but breaking it down into manageable steps makes the process much clearer. Regions strives to make its application process as straightforward as possible, whether you apply online, over the phone, or in person at a branch. Understanding each stage will help you prepare and move through it efficiently.

Step 1: Pre-Approval – Your Strategic Advantage

Getting pre-approved for a used car loan before you start shopping is one of the smartest moves you can make. Pre-approval means Regions has reviewed your financial information and determined how much they are willing to lend you, at what estimated interest rate, and under what terms. This gives you a clear budget and significant negotiating power at the dealership.

Based on my experience, walking into a dealership with a pre-approval letter is like having cash in hand. It allows you to focus on negotiating the car price, rather than the financing, which often leads to a better deal. It also saves time and reduces stress, as you’ve already handled a major part of the financial legwork.

Step 2: Gathering Your Documents

Preparation is key to a smooth application. Before you apply, gather all necessary documents. This typically includes a valid government-issued ID (like a driver’s license), proof of income (pay stubs, W-2s, tax returns), proof of residency (utility bill, lease agreement), and potentially information about the vehicle you intend to purchase (if you have one in mind).

Having these documents ready will prevent delays in your application processing. It shows the lender you are organized and serious about your commitment. Common mistakes to avoid include submitting incomplete applications, which can prolong the approval process or even lead to denial.

Step 3: Submitting Your Application

Once you have your documents and understand the pre-approval process, you can submit your application. Regions offers several convenient ways to apply: online through their website, by calling their customer service line, or by visiting a local Regions branch. The application will ask for personal details, employment history, income information, and your financial obligations.

Be honest and accurate with all the information you provide. Any discrepancies could raise red flags and delay or even jeopardize your application. Take your time to fill out every section completely and double-check for errors before submitting.

Step 4: The Underwriting Review

After you submit your application, Regions’ underwriting team will review all the information provided. This involves checking your credit report, verifying your income and employment, and assessing your overall financial health. They are looking for assurance that you are a reliable borrower who can meet the loan obligations.

This stage might involve a hard inquiry on your credit report, which can slightly lower your score temporarily. This is normal for loan applications. The underwriting team may also reach out for additional documentation or clarification if needed, so be responsive to their requests.

Step 5: Loan Offer and Closing

If your application is approved, Regions will present you with a loan offer detailing the approved loan amount, interest rate, loan term, and monthly payment. It’s crucial to thoroughly review this offer. Understand all the terms and conditions before you sign. Don’t hesitate to ask questions if anything is unclear.

Once you accept the offer, you’ll proceed to the closing stage, where you sign the final loan documents. At this point, the funds will be disbursed, either directly to the dealership or sometimes to you, to complete the car purchase. Congratulations, you’re one step closer to driving your new-to-you car!

Securing the Best Rates and Terms for Your Regions Used Car Loan

Getting approved for a loan is one thing, but securing the best possible rates and terms is another. Even small differences in interest rates can save you hundreds or even thousands of dollars over the life of a used car loan. Here are key strategies to help you optimize your Regions Used Car Loan.

Boost Your Credit Score

Your credit score is the single most influential factor in determining your interest rate. A higher score signals less risk to the lender, resulting in lower rates. Before applying, take steps to improve your credit: pay bills on time, reduce existing debt, and avoid opening new credit accounts.

Even a slight improvement in your score can translate to significant savings. For more insights on managing your personal finances, check out our guide on . This proactive approach can give you a strong advantage when negotiating loan terms.

Make a Larger Down Payment

A larger down payment reduces the amount you need to borrow, which directly lowers your monthly payments and the total interest paid over the life of the loan. It also signals to the lender that you are financially committed to the purchase, often leading to better loan offers.

Pro tips from us: Aim for at least 10-20% of the car’s purchase price as a down payment if possible. This not only reduces your loan burden but also helps prevent you from being "underwater" on your loan (owing more than the car is worth) early in its life.

Consider a Shorter Loan Term

While a longer loan term means lower monthly payments, it almost always results in paying significantly more in total interest. If your budget allows, opting for a shorter loan term (e.g., 36 or 48 months instead of 60 or 72) can save you a substantial amount of money over time.

This strategy requires a careful assessment of your monthly budget. While the payments will be higher, the overall financial benefit can be immense. It also helps you build equity in your vehicle faster.

Negotiate the Car Price

Remember that the loan amount is based on the purchase price of the car. The lower you can negotiate the car’s price with the dealership, the less money you will need to borrow. Every dollar saved on the purchase price is a dollar less you’ll pay interest on.

Focus on getting the best deal on the vehicle first, separate from the financing discussion. This strategy allows you to leverage your pre-approval and avoid getting caught up in a "four-square" financing game at the dealership.

Understand APR vs. Interest Rate

It’s crucial to understand the difference between the interest rate and the Annual Percentage Rate (APR). The interest rate is the cost of borrowing money, but the APR includes the interest rate plus any additional fees or charges associated with the loan, such as origination fees.

Always compare APRs when evaluating loan offers, as it provides a more accurate representation of the true annual cost of your loan. Regions will provide a clear APR, allowing you to make an informed comparison with other lenders.

Common Pitfalls and How to Avoid Them with Regions Used Car Loans

Even with a trusted lender like Regions, navigating a used car loan can present challenges. Being aware of common mistakes can help you avoid costly errors and ensure a smoother, more financially sound purchase.

Not Getting Pre-Approved

One of the biggest mistakes car buyers make is not getting pre-approved for a loan before stepping onto a dealership lot. Without pre-approval, you lack a baseline for what you qualify for, making you vulnerable to less favorable financing offers from dealerships.

The dangers of dealership financing without a baseline are significant. Dealerships often mark up interest rates to increase their profit, and without a pre-approved offer from Regions in hand, you might not realize you’re paying more than you should. Always secure your own financing first.

Overlooking the Total Cost

It’s easy to get fixated on the monthly payment, but focusing solely on this figure can be misleading. A low monthly payment often comes with a longer loan term and a higher total interest paid over time. Always consider the total cost of the loan, including principal and all interest.

This is a common pitfall that can lead to long-term financial strain. Pro tip from us: Use an online loan calculator to compare different scenarios (loan terms, interest rates) and understand the full financial commitment before signing any agreement.

Ignoring Your Credit Report

Many people don’t review their credit report until they need a loan. This is a mistake. Your credit report can contain errors that negatively impact your score. These errors can cost you in terms of higher interest rates or even loan denial.

Regularly checking your credit report (you’re entitled to a free one annually from each of the three major bureaus) allows you to dispute any inaccuracies and ensure your credit profile is strong before applying for a Regions Used Car Loan.

Extending Loan Terms Too Long

While longer loan terms offer lower monthly payments, they come with significant drawbacks. You’ll pay more in total interest, and you risk entering a state of negative equity, where you owe more on the car than it’s worth, especially as used cars depreciate rapidly.

This "underwater" situation can be problematic if you need to sell or trade in the car before the loan is paid off. It’s generally advisable to choose the shortest loan term you can comfortably afford to minimize interest costs and mitigate depreciation risk.

Forgetting About Additional Costs

The loan payment is just one part of car ownership. Many buyers overlook other significant costs associated with owning a vehicle. These include insurance, maintenance, registration fees, taxes, and fuel.

Pro tip: Budget beyond just the loan payment. Create a comprehensive monthly budget that includes all potential car-related expenses. Ignoring these can lead to unexpected financial strain, even if your Regions Used Car Loan payment is manageable.

Managing Your Regions Used Car Loan Effectively

Once you’ve secured your Regions Used Car Loan and driven away in your new vehicle, the journey isn’t over. Effective loan management is crucial to maintain good financial health, avoid late fees, and potentially save money over the life of the loan. Regions provides various tools and options to help you manage your auto loan.

Setting Up Auto Payments

One of the easiest ways to ensure you never miss a payment and avoid late fees is to set up automatic payments. Regions typically offers this option, allowing you to link your checking or savings account for automatic deductions on your due date.

This not only provides convenience but also helps you build a strong payment history, which positively impacts your credit score. Based on my experience, automation reduces stress and eliminates the risk of human error or forgetfulness.

Understanding Your Statements

Regularly review your monthly loan statements, whether they are physical or digital. These statements provide crucial information, including your current balance, payment history, the amount applied to principal versus interest, and any fees incurred.

Understanding your statements allows you to track your progress, identify any discrepancies, and stay informed about your loan’s status. If you have questions, Regions’ customer service is available to help clarify any details.

Early Payoff Strategies

If your financial situation improves, consider strategies to pay off your Regions Used Car Loan early. This can save you a significant amount in interest over time. Common strategies include making bi-weekly payments (which results in one extra full payment per year) or making extra principal-only payments whenever possible.

Before implementing an early payoff strategy, always confirm with Regions that there are no prepayment penalties associated with your loan. Most auto loans do not have them, but it’s always wise to check. If you’re also exploring options for securing your financial future, our article on might be helpful.

What to Do if You Face Financial Hardship

Life can be unpredictable. If you suddenly face financial hardship that makes it difficult to make your Regions Used Car Loan payments, the worst thing you can do is ignore the problem. Immediately contact Regions Bank to discuss your options.

Many lenders are willing to work with borrowers who are proactive and transparent. They might offer temporary payment deferrals, modified payment plans, or other solutions to help you get back on track. Open communication is key to avoiding default and protecting your credit score.

Exploring Alternatives and Next Steps

While Regions offers a strong option for used car loans, it’s always wise to be aware of the broader financing landscape. Understanding other alternatives and knowing when to consider refinancing can further empower your decision-making.

Other Financing Options

Regions is a reputable bank, but it’s not the only player in the used car loan market. Other financing options include:

- Credit Unions: Often known for competitive rates and a member-focused approach. If you’re eligible to join a credit union, they can be a great alternative.

- Online Lenders: Companies specializing in online loans can offer quick approvals and competitive rates, often with streamlined digital processes.

- Dealership Financing: While convenient, approach dealership financing with caution. As mentioned, they may mark up interest rates. Always compare their offers to your pre-approval from Regions or another independent lender.

Common mistakes to avoid are accepting the first offer without comparison. Always shop around and get quotes from at least three different lenders to ensure you’re getting the best deal.

Refinancing Your Regions Auto Loan

Even after you’ve secured a loan, circumstances can change. Refinancing your auto loan means taking out a new loan to pay off your existing one, often with a different lender or different terms. This might be a smart move if:

- Your credit score has improved: A higher score could qualify you for a lower interest rate.

- Interest rates have dropped: Market rates can fluctuate, making refinancing a viable option.

- You want to change your loan term: You might want to shorten the term to save on interest or lengthen it to reduce monthly payments (though this increases total interest).

Before refinancing, calculate the potential savings and consider any fees associated with the new loan. Regions itself may offer refinancing options if you’re an existing customer, or you can explore other lenders.

Final Thoughts: Driving Smart with Regions Used Car Loans

Securing a used car loan from Regions Bank can be a straightforward and beneficial process, provided you approach it with knowledge and preparation. We’ve covered everything from understanding the benefits of choosing Regions to navigating eligibility, the application process, and critical strategies for securing the best rates and terms. Remember to prioritize financial health, avoid common pitfalls, and actively manage your loan once approved.

By being proactive, comparing offers, and understanding all aspects of your loan, you can ensure your Regions Used Car Loan helps you drive away with not just a great vehicle, but also a sound financial decision. Empower yourself with information, and you’ll be well on your way to a successful car ownership experience. Check Regions’ current used car loan offers and take the first step towards your next vehicle today.