Navigating SCCU Used Car Loan Rates: Your Ultimate Guide to Smart Auto Financing

Navigating SCCU Used Car Loan Rates: Your Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

Buying a used car can be a brilliant financial move, offering significant savings compared to purchasing a brand-new vehicle. However, securing the right financing is crucial to making that smart decision truly pay off. For many in Florida, Space Coast Credit Union (SCCU) stands out as a trusted financial partner, and their used car loan rates are often a point of interest for prospective buyers.

This comprehensive guide is designed to demystify SCCU used car loan rates, walking you through everything you need to know to secure the best possible deal. From understanding how rates are determined to mastering the application process and avoiding common pitfalls, we’ll equip you with the knowledge to drive away confident in your auto financing choice. Our goal is to make this complex topic easy to understand, providing you with actionable insights that genuinely put you in the driver’s seat of your financial future.

Navigating SCCU Used Car Loan Rates: Your Ultimate Guide to Smart Auto Financing

What is SCCU? A Trusted Partner in Your Financial Journey

Before diving into the specifics of used car loan rates, it’s essential to understand who Space Coast Credit Union (SCCU) is. Founded in 1951, SCCU has grown into one of the largest credit unions in Florida, serving members across 34 counties. Unlike traditional banks, credit unions are not-for-profit financial cooperatives owned by their members. This fundamental difference often translates into better rates on loans, higher returns on savings, and more personalized service for their members.

Being a member-owned institution means SCCU’s primary focus is on the financial well-being of its members, rather than maximizing profits for shareholders. This philosophy extends to their lending products, including their used car loans. Based on my experience in the financial sector, credit unions like SCCU often offer highly competitive rates because any surplus earnings are typically returned to members in the form of lower loan rates, higher savings rates, or reduced fees. This makes them a compelling option for anyone seeking auto financing.

Why Choose a Used Car Loan? The Smart Financial Path

The decision to buy a used car often comes down to financial prudence. A new car depreciates significantly the moment it’s driven off the lot, sometimes losing 20-30% of its value in the first year alone. Used cars, on the other hand, have already absorbed the steepest part of this depreciation curve, making them a more cost-effective option.

Opting for a used car loan can save you a substantial amount of money in several ways. You’ll typically pay a lower purchase price, which means a smaller loan amount and consequently less interest over the life of the loan. Furthermore, insurance premiums are often lower for used vehicles, contributing to overall savings. Many reliable used cars are available today, thanks to advancements in manufacturing and better maintenance practices. This makes the used car market an attractive avenue for budget-conscious buyers who still desire quality and reliability.

Unpacking SCCU Used Car Loan Rates: The Core Factors

Understanding SCCU used car loan rates isn’t just about looking up a number; it’s about comprehending the various elements that influence that number. The Annual Percentage Rate (APR) you receive is a personalized figure, reflecting your financial profile and the specifics of the vehicle you intend to purchase. It encompasses not just the interest rate but also any fees associated with the loan, giving you a true picture of the total cost of borrowing.

Several critical factors contribute to how your SCCU used car loan rate is ultimately determined. These elements are standard across most lenders, but SCCU’s member-focused approach often provides an edge. Knowing these factors beforehand empowers you to take steps to improve your position. Our professional advice is to always approach loan applications with a clear understanding of these variables.

1. Your Credit Score: The Ultimate Indicator

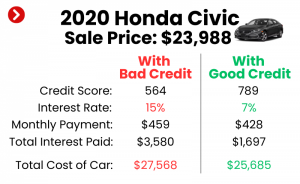

Your credit score is arguably the most significant factor influencing your loan rate. It’s a numerical representation of your creditworthiness, derived from your payment history, amounts owed, length of credit history, new credit, and credit mix. Lenders use this score to assess the risk of lending to you. A higher credit score signals to SCCU that you are a responsible borrower, making you eligible for lower interest rates.

For instance, borrowers with excellent credit (typically 760+) will almost always qualify for the most favorable rates. Those with good credit (670-759) will also find competitive rates, while fair (580-669) or poor credit (below 580) scores will likely result in higher APRs to offset the perceived risk. Pro tips from us: Before you even start shopping for a car, check your credit score and report. This gives you time to correct any errors and understand where you stand.

2. The Loan Term: Length Matters

The loan term refers to the duration over which you agree to repay the loan, usually expressed in months (e.g., 36, 48, 60, 72 months). While a longer loan term might offer lower monthly payments, it typically comes with a higher overall interest rate. This is because lenders assume more risk over an extended period. Conversely, a shorter loan term usually results in a higher monthly payment but a lower interest rate and less interest paid over the life of the loan.

For example, a 72-month loan might seem appealing due to its lower monthly burden, but you could end up paying thousands more in interest compared to a 48-month loan for the same amount. SCCU, like other responsible lenders, balances affordability with the total cost of borrowing. It’s crucial to find a term that fits your budget without unnecessarily extending the repayment period.

3. Your Down Payment: Showing Commitment

A substantial down payment can significantly impact your SCCU used car loan rate. When you put down a larger sum upfront, you reduce the amount you need to borrow, which lowers the lender’s risk. This reduced risk often translates into a more attractive interest rate for you. Moreover, a larger down payment means you’ll have more equity in the vehicle from day one, reducing the likelihood of being "upside down" on your loan (owing more than the car is worth).

Based on my experience, a down payment of 10-20% of the vehicle’s purchase price is generally recommended. Not only does it help secure a better rate, but it also lowers your monthly payments and the total interest you’ll pay. It demonstrates your financial commitment to the purchase.

4. Vehicle Age and Mileage: Asset Value

The specific details of the used car you’re purchasing also play a role in rate determination. Older vehicles or those with very high mileage are generally considered higher risk by lenders. This is because they are more prone to mechanical issues, which could affect their resale value and your ability to repay the loan if the car becomes unreliable. SCCU will assess the vehicle’s value, condition, and depreciation rate.

Newer used cars (e.g., 1-3 years old) with lower mileage typically qualify for better rates than much older models. This is due to their higher perceived reliability and resale value. SCCU often has specific rate tiers based on the vehicle’s model year, so it’s wise to consider this when making your selection.

5. Debt-to-Income (DTI) Ratio: Your Financial Capacity

Your debt-to-income (DTI) ratio is another key metric SCCU will consider. It’s calculated by dividing your total monthly debt payments by your gross monthly income. A lower DTI ratio indicates that you have sufficient income to manage your existing debts, including the new car loan, without financial strain. Lenders prefer applicants with a DTI ratio of 36% or less, though some may approve up to 43% depending on other factors.

A high DTI ratio can signal to SCCU that you might be overextended financially, increasing the perceived risk of default. This could lead to a higher interest rate or even a loan denial. Managing your existing debts and improving your DTI ratio before applying for a loan is a smart strategy.

The SCCU Application Process: A Smooth Ride to Approval

Applying for a used car loan with SCCU is designed to be a straightforward process. They prioritize member convenience and clear communication. Understanding each step can help you prepare thoroughly and avoid unnecessary delays.

Step 1: Pre-Approval – Your Power Play

One of the most valuable steps you can take is to get pre-approved for a loan before you even set foot on a dealership lot. Pre-approval from SCCU means they have reviewed your financial information and determined how much you can borrow, at what estimated interest rate, and under what terms. This transforms you into a cash buyer, giving you significant negotiation leverage with dealerships.

Pro tips from us: Pre-approval helps you establish a realistic budget, ensuring you only shop for cars you can truly afford. It also streamlines the purchasing process, as you already have your financing in place. Most importantly, it separates the financing conversation from the car price negotiation, allowing you to focus on getting the best deal on the vehicle itself.

Step 2: Gathering Your Documentation

Once you’re ready to apply, either for pre-approval or a final loan, SCCU will require certain documents to verify your identity, income, and financial stability. Common documents include:

- Government-issued photo identification (driver’s license, passport)

- Proof of income (pay stubs, tax returns, bank statements)

- Proof of residency (utility bill, lease agreement)

- Social Security Number

- Information about the vehicle you intend to purchase (if applicable, for final approval)

Having these documents organized and ready can significantly speed up the application process. SCCU’s loan officers are there to guide you if you have any questions about specific requirements.

Step 3: Submitting Your Application

You can typically apply for an SCCU used car loan online, over the phone, or in person at one of their branch locations. The application will ask for personal details, employment information, income, and financial history. Be honest and accurate with all the information you provide. SCCU’s secure online portal makes the process efficient and convenient.

Step 4: Review and Approval

After submitting your application, SCCU’s lending team will review your information, pull your credit report, and assess your overall financial profile. They will then determine your eligibility and the specific loan terms, including your APR. They strive to provide quick decisions, often within the same business day, especially for pre-approvals.

Step 5: Funding Your Loan

Upon approval, SCCU will work with you to finalize the loan agreement. If you’re purchasing from a dealership, the funds can often be directly disbursed to the dealer. If you’re buying from a private seller, the funds can be provided to you to complete the transaction. The entire process, from application to funding, is designed to be as seamless as possible for SCCU members.

Tips for Securing the Best SCCU Used Car Loan Rate

Getting a used car loan is more than just filling out a form; it’s about strategic planning. Here are some pro tips from us to help you secure the most favorable SCCU used car loan rate possible:

- Improve Your Credit Score: This is paramount. Pay down existing debts, make all payments on time, and avoid opening new lines of credit before applying for a car loan. Even a small improvement in your score can lead to a noticeable difference in your APR.

- Save for a Larger Down Payment: As discussed, a bigger down payment reduces your loan amount and the lender’s risk, often resulting in a better rate. It also helps you build equity faster.

- Choose a Shorter Loan Term: While it means higher monthly payments, a shorter term almost always results in a lower interest rate and less total interest paid over the life of the loan. Carefully evaluate what you can comfortably afford each month.

- Shop Around (Even Within SCCU): While SCCU offers competitive rates, it’s always wise to compare their offers with those from other credit unions or lenders. This ensures you’re getting the best deal for your specific situation. Don’t be afraid to ask if there are any special promotions for members.

- Be Aware of Your DTI Ratio: If your DTI is high, consider paying down other debts before applying. This demonstrates financial responsibility and improves your chances of getting a lower rate.

- Negotiate Wisely: With a pre-approval in hand, you have the power to negotiate the vehicle price confidently, knowing your financing is already secured. This separation of concerns can save you money on both ends.

Benefits of Choosing SCCU for Your Used Car Loan

Beyond competitive rates, choosing SCCU for your used car loan offers several distinct advantages that underscore their commitment to members:

- Member-Focused Service: As a credit union, SCCU prioritizes its members. You’re not just a number; you’re an owner. This often leads to more personalized attention and flexible solutions tailored to your needs.

- Competitive Rates & Flexible Terms: SCCU consistently strives to offer some of the most competitive used car loan rates in the market, often lower than traditional banks. They also provide a range of flexible terms to fit various budgets.

- Local Presence & Community Involvement: With numerous branches across Florida, SCCU offers convenient access to in-person support. They are also deeply involved in the communities they serve, fostering trust and loyalty.

- Financial Education & Resources: SCCU often provides resources and guidance to help members make informed financial decisions, extending beyond just the loan itself. This commitment to financial literacy is a significant value add.

- Convenient Online Tools: From online applications to payment portals, SCCU provides modern digital tools to make managing your loan easy and efficient.

Common Mistakes to Avoid When Applying for a Used Car Loan

Based on my experience, several common pitfalls can derail your efforts to secure the best used car loan. Avoiding these can save you money and stress:

- Ignoring Your Credit Score: Not checking your credit report before applying is a major mistake. You might be surprised by errors or a lower score than anticipated, which can impact your rates.

- Not Getting Pre-Approved: Walking into a dealership without pre-approval puts you at a significant disadvantage. You lose negotiation power and might feel pressured into higher-interest dealer financing.

- Focusing Only on Monthly Payments: While important, fixating solely on the monthly payment can lead to extending the loan term unnecessarily, resulting in much higher total interest paid. Always consider the total cost of the loan.

- Skipping the Budget: Don’t apply for a loan without a clear understanding of your overall budget. Factor in not just the car payment but also insurance, fuel, maintenance, and registration.

- Not Reading the Fine Print: Always thoroughly review all loan documents before signing. Understand the APR, any fees, prepayment penalties (though rare with SCCU), and all terms and conditions.

- Taking the First Offer: Even if the offer seems good, always compare it with at least one or two other lenders to ensure you’re getting the most competitive rate available to you.

Refinancing Your Existing Used Car Loan with SCCU

What if you already have a used car loan but aren’t happy with the rate? SCCU also offers options for refinancing. Refinancing involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate or with more favorable terms. This can be a smart move if:

- Your credit score has significantly improved since you took out the original loan.

- Interest rates have dropped since your initial purchase.

- You want to lower your monthly payments (though be mindful of extending the loan term).

- You want to change your loan term to better suit your current financial situation.

Refinancing with SCCU could potentially save you hundreds or even thousands of dollars over the life of your loan. It’s definitely worth exploring if your financial circumstances have improved or market rates have shifted.

Conclusion: Drive Away with Confidence

Securing an SCCU used car loan can be a fantastic way to finance your next vehicle, offering competitive rates and the personalized service that credit unions are known for. By understanding the factors that influence your rate, meticulously preparing for the application process, and implementing our expert tips, you can significantly improve your chances of getting the best possible deal.

Remember, your credit score, loan term, down payment, and the specifics of the vehicle all play a crucial role. Arm yourself with knowledge, get pre-approved, and don’t hesitate to leverage SCCU’s member-focused approach. Our ultimate goal is to empower you to make an informed decision, ensuring your journey to owning a used car is as smooth and financially sound as possible.

Ready to take the next step? Visit SCCU’s official website or stop by a local branch to explore their current used car loan rates and start your application today. Your dream used car, financed smartly, awaits!