Navigating SEFCU Car Loan Rates: Your Ultimate Guide to Driving Away with the Best Deal

Navigating SEFCU Car Loan Rates: Your Ultimate Guide to Driving Away with the Best Deal Carloan.Guidemechanic.com

Buying a new or used car is an exciting milestone, but the financing aspect can often feel like a complex maze. Understanding car loan rates is crucial, as even a small difference in the interest rate can save you hundreds, if not thousands, of dollars over the life of your loan. For residents of New York, SEFCU Car Loan Rates often stand out as a highly competitive option, offering a member-centric approach that many traditional banks simply can’t match.

This comprehensive guide will demystify everything you need to know about securing an auto loan through SEFCU. We’ll dive deep into their offerings, eligibility requirements, the application process, and most importantly, how you can position yourself to get the most favorable rates possible. Our goal is to equip you with the knowledge and confidence to make an informed decision, ensuring you drive away not just with your dream car, but also with a smart financial deal.

Navigating SEFCU Car Loan Rates: Your Ultimate Guide to Driving Away with the Best Deal

What is SEFCU? A Brief Overview of Your Local Credit Union Advantage

Before we delve into the specifics of SEFCU car loan rates, it’s important to understand what SEFCU is and how it operates. SEFCU, which stands for State Employees Federal Credit Union, is a not-for-profit financial cooperative dedicated to serving its members. Unlike traditional banks that focus on shareholder profits, credit unions like SEFCU prioritize their members’ financial well-being.

This fundamental difference often translates into better interest rates on loans, higher returns on savings, and lower fees. SEFCU has grown to be one of the largest credit unions in New York, built on a foundation of community support and a commitment to helping individuals and families achieve their financial goals. Their member-first philosophy is a significant advantage when you’re seeking financing options, particularly for something as substantial as a car loan.

Understanding Car Loan Rates: The Foundational Basics

Before comparing specific SEFCU auto loan offerings, it’s essential to grasp the fundamental concepts that govern all car loan rates. This knowledge empowers you to evaluate any loan offer critically and understand its long-term implications. A car loan isn’t just about the monthly payment; it’s about the total cost of borrowing.

What Influences Your Interest Rate?

Several key factors play a significant role in determining the interest rate you’ll be offered. These elements are assessed by lenders to gauge your risk profile. Understanding them is your first step toward securing a better deal.

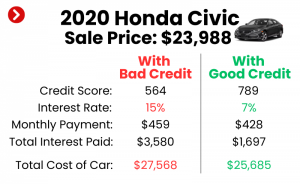

- Credit Score: Your credit score is arguably the most influential factor. It’s a numerical representation of your creditworthiness, based on your payment history, debt levels, and other financial behaviors. A higher credit score signals lower risk to lenders, often resulting in significantly lower interest rates.

- Loan Term: This refers to the length of time you have to repay the loan, typically measured in months (e.g., 36, 48, 60, 72 months). Shorter terms usually come with lower interest rates but higher monthly payments, while longer terms spread payments out, making them lower but often incurring more interest over time.

- Down Payment: The amount of money you pay upfront for the vehicle directly reduces the amount you need to borrow. A larger down payment can reduce your loan-to-value (LTV) ratio, making you a less risky borrower and potentially qualifying you for a better rate.

- New vs. Used Vehicle: Lenders often view used cars as higher risk due to their depreciation and potential for mechanical issues. Consequently, SEFCU used car loan rates, and those from other lenders, are typically slightly higher than rates for new vehicles.

- Market Conditions: Broader economic factors, such as the prime rate set by the Federal Reserve, also influence overall interest rates. When the prime rate rises, car loan rates tend to follow suit.

APR vs. Interest Rate: Knowing the Difference

It’s common to see both "interest rate" and "APR" (Annual Percentage Rate) when discussing loans. While related, they are not interchangeable.

The interest rate is simply the percentage charged on the principal amount of the loan. It’s the cost of borrowing money before any other fees are factored in.

The APR, on the other hand, represents the true annual cost of borrowing. It includes the interest rate plus any additional fees associated with the loan, such as administrative fees, origination fees, or closing costs. When comparing loans, always focus on the APR, as it provides a more accurate picture of the total cost.

Fixed vs. Variable Rates: Which is Right for You?

Car loans typically come with either a fixed or variable interest rate.

A fixed-rate loan means your interest rate will remain the same for the entire duration of the loan. Your monthly payment for principal and interest will be consistent, providing predictability and stability in your budget.

A variable-rate loan has an interest rate that can change over time, usually tied to a specific market index. While these can sometimes start lower than fixed rates, they carry the risk of increasing, leading to higher monthly payments later on. For car loans, fixed rates are overwhelmingly more common and generally preferred for their stability.

SEFCU Car Loan Rates: What to Expect from Your Credit Union

SEFCU is known for offering competitive SEFCU auto loan rates to its members, often beating what you might find at larger commercial banks. Their rates are transparent and designed to provide value, aligning with their member-first philosophy.

New Car Loan Rates at SEFCU

When you’re looking to finance a brand-new vehicle, SEFCU typically offers some of its most attractive rates. These rates are influenced by all the factors we discussed earlier – primarily your credit score and the loan term. Generally, individuals with excellent credit will qualify for the lowest advertised rates.

For instance, a shorter loan term, such as 36 or 48 months, will often come with a lower interest rate compared to a 60 or 72-month term. This is because the lender is exposed to less risk over a shorter period. It’s always wise to check SEFCU’s official website or speak with a loan officer for the most current rates and any ongoing promotions for SEFCU new car loan financing.

Used Car Loan Rates Through SEFCU

Financing a used car often comes with slightly higher rates than a new one. This is a standard practice across all lenders, reflecting the higher perceived risk associated with pre-owned vehicles due to depreciation, mileage, and potential for unforeseen repairs. However, SEFCU used car loan rates remain highly competitive within the market.

The age of the used car also plays a role. Older used cars might have slightly higher rates or shorter maximum loan terms compared to newer used cars (e.g., those less than 3 years old). Always consider the car’s age and mileage when budgeting for a used car loan.

Refinancing Your Car Loan with SEFCU

Did you get a car loan with a less-than-ideal rate in the past? Perhaps your credit score has improved significantly since then, or you’ve found better rates available elsewhere. SEFCU refinancing options can be a game-changer. Refinancing means taking out a new loan to pay off your existing car loan, ideally at a lower interest rate or with more favorable terms.

Based on my experience helping countless individuals navigate auto financing, refinancing can lead to substantial savings. It’s an excellent strategy if:

- Your credit score has improved.

- Market rates have dropped.

- You want to reduce your monthly payment by extending the loan term (though this might increase total interest paid).

- You want to shorten your loan term to pay off the car faster and save on interest.

The process for SEFCU refinancing is similar to applying for a new loan, requiring an application and financial documentation. It’s definitely worth exploring if you’re looking to improve your current car loan situation.

Special Offers and Discounts: Maximizing Your Savings

One of the significant advantages of being a credit union member is the potential for special offers and rate discounts. SEFCU often provides various incentives that can further reduce your SEFCU auto loan rates.

These might include:

- Loyalty Discounts: For long-standing members or those with multiple accounts (e.g., checking, savings, mortgage) with SEFCU.

- Automatic Payment Discounts: A small rate reduction for setting up automatic payments directly from a SEFCU checking account.

- Promotional Rates: Limited-time offers for specific loan products or during certain periods.

Always inquire about any available discounts when discussing your loan options with a SEFCU representative. These small reductions can add up over the loan term.

Eligibility and Application Process for a SEFCU Car Loan

Securing a SEFCU car loan is a straightforward process, especially if you’re prepared. Understanding the eligibility criteria and the application journey will help streamline your experience.

Membership Requirements: The First Step

Since SEFCU is a credit union, you must be a member to access their loan products. Eligibility for SEFCU membership is broad, often including:

- Individuals who live, work, worship, or attend school in specific counties in New York.

- Employees of certain companies or organizations.

- Family members of existing SEFCU members.

Joining is usually simple, requiring a small deposit into a savings account to establish your membership. It’s a worthwhile step, as membership opens the door to all of SEFCU’s competitive financial products and services.

Key Documents Needed for Your Application

To ensure a smooth application process for your SEFCU car loan, have the following documents ready:

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Income: Recent pay stubs, tax returns (if self-employed), or other income verification.

- Proof of Residence: Utility bill or lease agreement.

- Vehicle Information: If you’ve already found a car, you’ll need the VIN, make, model, year, and approximate mileage.

- Existing Loan Information: If refinancing, details of your current auto loan.

Gathering these documents beforehand will prevent delays and allow SEFCU to process your auto loan application efficiently.

The Application Journey: From Pre-Approval to Purchase

The SEFCU loan application process is designed for convenience and efficiency, offering multiple avenues for application.

- Online Application: The quickest and most common method. You can apply from the comfort of your home, and often receive a decision within minutes or hours.

- In-Branch Application: For those who prefer a personal touch, visiting a SEFCU branch allows you to speak directly with a loan officer, ask questions, and get personalized guidance.

- Pre-Approval: This is a crucial step that Pro tips from us strongly recommend. Applying for pre-approval means SEFCU evaluates your creditworthiness and provides you with a loan amount and estimated interest rate before you even step foot in a dealership.

Pre-approval for your SEFCU auto loan offers immense benefits:

- It gives you a clear budget, so you know exactly how much car you can afford.

- It strengthens your negotiating position at the dealership, as you arrive with your own financing secured. Dealers are more likely to offer their best price when they know you’re not dependent on their financing.

- It allows you to focus on finding the right car, rather than worrying about the financing details at the point of sale.

Factors That Influence Your SEFCU Car Loan Rate: An In-Depth Look

While we touched upon these factors earlier, understanding their nuances can help you strategically improve your chances of securing the best possible SEFCU car loan rates.

The Undeniable Power of Your Credit Score

Your credit score is not just a number; it’s a reflection of your financial responsibility. Lenders categorize scores into tiers (e.g., excellent, good, fair, poor), and each tier corresponds to a different risk level and, consequently, a different set of interest rates.

- Excellent Credit (780+): You’ll qualify for the absolute lowest SEFCU car loan rates, as you represent minimal risk.

- Good Credit (670-779): Still very strong, offering competitive rates, though perhaps not the absolute lowest.

- Fair Credit (580-669): You can still get approved, but expect rates to be notably higher.

- Poor Credit (Below 580): Approval might be challenging, and if granted, rates will be significantly higher to offset the perceived risk.

Based on my experience, a small improvement in your credit score can sometimes bump you into a better rate tier, saving you hundreds over the loan term. It’s worth reviewing your credit report well in advance of applying.

Loan Term: Balancing Monthly Payments and Total Interest

The length of your loan, or its term, has a dual impact: on your monthly payment and on the total interest you pay.

- Shorter Terms (e.g., 36-48 months): These typically come with lower interest rates from SEFCU. Your monthly payments will be higher, but you’ll pay off the loan faster and incur less total interest. This is often the most financially savvy option if your budget allows.

- Longer Terms (e.g., 60-72+ months): While these result in lower monthly payments, they usually come with slightly higher interest rates. More importantly, you’ll pay significantly more in total interest over the life of the loan. While appealing for budget flexibility, it’s a trade-off worth considering carefully.

The Impact of Your Down Payment

A substantial down payment reduces the amount you need to borrow, which directly lowers your monthly payments. More importantly, it reduces the risk for SEFCU.

- Lower Loan-to-Value (LTV): With a larger down payment, the loan amount is a smaller percentage of the car’s value. This means if you default, SEFCU is less likely to lose money, making you a more attractive borrower for better rates.

- Reduced Interest Paid: Less principal borrowed means less interest accrues over the loan term, saving you money regardless of the rate.

Aim for at least 10-20% down on a new car, and potentially more on a used car, to secure the most favorable SEFCU auto loan terms.

Vehicle Type & Age: New vs. Used Car Considerations

As mentioned, new cars generally command lower interest rates than used cars. This is due to several factors:

- Predictable Value: New cars depreciate at a more predictable rate, making them less risky collateral.

- Less Mechanical Risk: New cars come with warranties and are less likely to have immediate mechanical issues.

For used cars, SEFCU will also consider the vehicle’s age and mileage. Very old cars or those with exceptionally high mileage might face slightly higher rates or specific lending restrictions.

Your Relationship with SEFCU

Being an established, active member of SEFCU can sometimes provide an edge. If you have a long history of responsible banking with them, hold multiple accounts, or have direct deposit set up, these factors can subtly influence your standing as a borrower. Credit unions often reward loyalty with slightly better terms or expedited processing for SEFCU loan applications.

Pro Tips for Securing the Best SEFCU Car Loan Rate

Navigating the world of car loans requires a strategic approach. Here are some Pro tips from us to help you secure the most competitive SEFCU car loan rates possible:

- Boost Your Credit Score: Before you even think about applying, pull your credit report from all three major bureaus (Equifax, Experian, TransUnion). Dispute any errors and focus on paying down high-interest debt, especially credit card balances. A few months of diligent effort can significantly improve your score.

- Save for a Larger Down Payment: The more you put down, the less you borrow, and the lower your monthly payments will be. It also makes you a more attractive borrower, potentially unlocking lower rates. Aim for at least 20% if possible.

- Get Pre-Approved: This is perhaps the most powerful tool in your arsenal. Obtain a SEFCU pre-approval before visiting the dealership. It gives you a firm offer and empowers you to negotiate the car price as a cash buyer, rather than negotiating based on monthly payments.

- Consider a Shorter Loan Term: If your budget allows, opt for the shortest loan term you can comfortably afford. While monthly payments will be higher, you’ll pay less in total interest and own your car outright sooner.

- Leverage Your SEFCU Membership: Ask about any member-exclusive discounts, loyalty programs, or rate reductions for setting up automatic payments from a SEFCU account.

- Shop Around (Wisely): While this article focuses on SEFCU, it’s always wise to compare offers from 2-3 other lenders (other credit unions or banks). However, do this within a short window (typically 14-45 days) to minimize the impact on your credit score, as multiple inquiries within this period are usually counted as a single hard inquiry for rate shopping purposes.

- Negotiate the Car Price, Not Just the Loan: Remember, the best loan rate on an overpriced car is still a bad deal. Focus on getting the best possible purchase price for the vehicle itself first, and then apply your pre-approved financing.

Common Mistakes to Avoid When Applying for a Car Loan

Even experienced car buyers can fall prey to common pitfalls. Common mistakes to avoid are crucial to recognize to ensure a smooth and financially sound car buying experience.

- Not Checking Your Credit Report: Failing to review your credit report for inaccuracies or to understand your current score can lead to unpleasant surprises or missed opportunities for better rates. Always check it beforehand.

- Applying to Too Many Lenders Haphazardly: While rate shopping is good, submitting applications to numerous lenders over an extended period can negatively impact your credit score. Group your inquiries within a short timeframe.

- Focusing Only on the Monthly Payment: Dealerships often try to "sell the payment." Don’t fall into this trap. A low monthly payment achieved by extending the loan term too long can mean paying significantly more in total interest. Always look at the total cost of the loan and the interest rate.

- Skipping Pre-Approval: As discussed, foregoing pre-approval puts you at a significant disadvantage at the dealership. You lose negotiation power and might end up with less favorable financing.

- Not Understanding All Terms and Conditions: Read the loan agreement carefully. Understand the APR, any prepayment penalties, late fees, and what happens if you miss a payment. Don’t sign anything you don’t fully comprehend.

SEFCU vs. Traditional Banks: Why a Credit Union Might Be Your Best Bet

When it comes to affordable car loan options, credit unions like SEFCU often have a distinct advantage over traditional commercial banks. This difference stems from their core operational philosophies.

The Credit Union Philosophy

As non-profit cooperatives, credit unions are owned by their members. This means that any "profits" are typically reinvested into the credit union to offer better rates, lower fees, and enhanced services to those members. Banks, conversely, are for-profit entities primarily beholden to their shareholders.

Member-Centric Approach

This member-first approach translates directly into how credit unions structure their loan products. SEFCU car loan rates are often more favorable because the institution isn’t pressured to maximize profits. They aim to provide the best possible financial tools for their community.

Potentially Better Rates and Fewer Fees

Historically, credit unions have offered slightly lower interest rates on loans and higher yields on savings accounts compared to big banks. They also tend to have fewer and lower fees. This competitive edge can lead to significant savings over the life of your car loan.

Personalized Service

Many members report a more personalized and attentive service experience at credit unions. Being part of a smaller, community-focused institution often means you’re treated as an individual, not just an account number. This can be invaluable when navigating the complexities of a car loan application.

Conclusion: Driving Forward with Confidence and a Great SEFCU Car Loan Rate

Securing a car loan is a significant financial decision, and understanding all its facets is paramount. By choosing to explore SEFCU car loan rates, you’re already on the path to a potentially more favorable and member-focused financing experience. Their commitment to competitive rates, personalized service, and a straightforward application process makes them a standout choice for auto financing in New York.

Remember, the keys to unlocking the best rates lie in preparing your finances, understanding the loan terms, and leveraging the power of pre-approval. Don’t just settle for the first offer; empower yourself with knowledge and strategically pursue the most affordable car loan that aligns with your financial goals. With this comprehensive guide in hand, you are well-equipped to navigate the process with confidence and drive away knowing you’ve made a smart financial move.