Navigating Special Financing Car Loans: Your Comprehensive Guide to Driving Forward

Navigating Special Financing Car Loans: Your Comprehensive Guide to Driving Forward Carloan.Guidemechanic.com

Buying a car is often a necessity, not just a luxury. For many, it represents freedom, access to work, and the ability to manage daily life. However, if your credit history isn’t perfect, the path to vehicle ownership can seem like a daunting uphill battle. This is where special financing car loans come into play.

As an expert blogger and SEO content writer with extensive experience in automotive finance, I understand the nuances of these loans. My mission with this comprehensive guide is to demystify special financing, providing you with the knowledge and confidence to make informed decisions. We’ll delve deep into what these loans are, who they’re for, how they work, and crucially, how you can use them to not only get a car but also rebuild your financial standing.

Navigating Special Financing Car Loans: Your Comprehensive Guide to Driving Forward

This article is designed to be your ultimate resource, ensuring you understand every facet of special financing car loans. Let’s embark on this journey together and unlock the road to your next vehicle.

What Exactly Are Special Financing Car Loans?

At its core, a special financing car loan is an auto loan designed for individuals who might not qualify for traditional financing due to challenges with their credit history. This can include those with poor credit scores, no credit history at all, past bankruptcies, or even previous repossessions. Think of it as a specialized financial product tailored to mitigate the perceived risk associated with these borrowers.

Traditional car loans are typically offered to individuals with good to excellent credit scores, reflecting a low risk of default. They often come with lower interest rates and more flexible terms. Special financing, on the other hand, acknowledges that life happens and people sometimes need a second chance or a starting point. It’s a bridge for those who are ready to prove their creditworthiness but need an initial opportunity.

The primary difference lies in the lender’s assessment of risk and the resulting loan terms. While conventional lenders might outright reject applicants with lower credit scores, special financing lenders are equipped to assess a broader range of factors. They look beyond just the FICO score, often considering income stability, job history, and the size of your down payment more heavily. This tailored approach makes car ownership accessible to a much wider demographic.

Who Needs Special Financing for a Car?

Special financing isn’t just for one type of borrower; it caters to a diverse group of individuals facing unique financial circumstances. Based on my experience, I’ve seen countless people benefit from these programs when traditional routes were closed. Understanding if you fall into one of these categories is the first step toward exploring your options.

Poor Credit Score (Subprime Borrowers)

This is perhaps the most common reason people seek special financing. If your credit score falls into the "subprime" category, typically below 620-660, you’ll likely find it challenging to secure a standard auto loan. A low score indicates to traditional lenders a higher risk of late payments or default.

For these borrowers, special financing lenders are willing to take on that increased risk. They do this by offering loans with terms that compensate for the risk, which often means higher interest rates. The goal here is to provide a lifeline, allowing you to get a vehicle while simultaneously offering a chance to improve your credit standing through consistent, on-time payments.

No Credit History

Many people, especially young adults just starting their financial journey or new immigrants, have no established credit history. This "thin file" can be just as problematic as bad credit for traditional lenders, as there’s no data to assess your repayment behavior. Without a credit score, lenders can’t predict your reliability.

Special financing addresses this by looking at alternative data points. They might consider your employment history, bank statements, and proof of residence. The aim is to establish a picture of your financial stability and ability to make payments, even without a formal credit score. This is a crucial entry point for building that all-important credit history.

Past Financial Troubles

Life can throw unexpected curveballs, leading to significant financial setbacks like bankruptcy, foreclosure, or vehicle repossession. These events severely impact your credit score and can make securing any form of credit incredibly difficult for years. Traditional lenders often see these as red flags, indicating a high probability of future default.

However, special financing lenders understand that these events don’t define a person’s future financial capability. They are often more willing to consider applicants who have a bankruptcy or repossession on their record, especially if time has passed and you can demonstrate a renewed commitment to financial responsibility. They might require a larger down payment or a co-signer, but the opportunity remains open.

High Debt-to-Income (DTI) Ratio

Even if you have a decent credit score, a high debt-to-income ratio can hinder your chances of traditional loan approval. Your DTI is the percentage of your gross monthly income that goes towards paying debts. If too much of your income is already allocated to other loans (mortgage, student loans, credit cards), lenders may worry about your ability to manage additional car payments.

Special financing lenders might be more flexible with DTI ratios, especially if you can show consistent income and a stable job history. They might also suggest slightly longer loan terms to lower monthly payments, making the loan more manageable within your existing financial commitments. This flexibility is key for those who are managing multiple financial obligations.

The Pros and Cons of Special Financing

Like any financial product, special financing car loans come with their own set of advantages and disadvantages. It’s essential to weigh these carefully before committing, ensuring you understand the full scope of what you’re signing up for. My experience has shown that a clear understanding of both sides helps borrowers make the best decisions for their unique situations.

The Pros: Driving Opportunities

- Access to Transportation: The most immediate and significant benefit is getting the car you need. For many, a vehicle is indispensable for work, family responsibilities, and daily life. Special financing provides a pathway to this essential asset when other doors are closed. It solves an immediate need, allowing you to maintain your lifestyle or secure employment.

- Opportunity to Rebuild Credit: This is arguably the most powerful long-term benefit. By consistently making on-time payments on a special financing car loan, you can demonstrate responsible financial behavior. This positive payment history is reported to credit bureaus and can significantly improve your credit score over time. It’s a tangible step towards financial rehabilitation and opening doors to better rates on future loans.

- Flexibility in Terms (Sometimes): While interest rates are generally higher, some special financing lenders offer flexibility in other areas. They might be more willing to work with different down payment amounts or structure payment plans that align with your income cycle. This adaptability can be crucial for those with fluctuating incomes or specific budget constraints.

The Cons: Navigating the Challenges

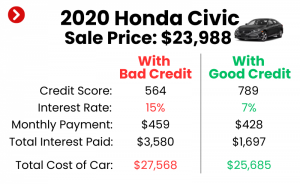

- Higher Interest Rates: This is the most common and significant drawback. Because special financing lenders take on a higher risk, they charge higher interest rates to compensate. This means you will pay substantially more over the life of the loan compared to someone with excellent credit. It’s the cost of access to credit when you need it most.

- Potentially Stricter Terms: Beyond interest rates, you might encounter other strict terms. Lenders might require a larger down payment to reduce their risk exposure. They could also insist on a shorter loan term, which means higher monthly payments, or vice versa, a longer term to reduce payments, which accumulates more interest. Common mistakes to avoid are focusing solely on the monthly payment without understanding the total cost of the loan or the impact of a long loan term.

- Limited Vehicle Choices: Special financing lenders often prefer to finance vehicles that are newer, have lower mileage, and hold their value well. This is because the car acts as collateral. This might mean you have fewer options when it comes to make, model, or year, potentially limiting you to vehicles that are easier for the lender to repossess and resell if necessary.

- Risk of Negative Equity: Due to higher interest rates and potentially faster depreciation, it’s easier to end up in a situation of "negative equity," or being "upside down" on your loan. This means you owe more on the car than it’s actually worth. If you need to sell the car or it gets totaled, you could still owe money on a vehicle you no longer own.

Navigating the Application Process for Special Financing

Applying for a special financing car loan doesn’t have to be overwhelming. With the right preparation and understanding of the steps involved, you can navigate the process smoothly and increase your chances of approval. Based on my expertise, I’ve outlined a step-by-step guide to empower you.

1. Assess Your Credit Situation

Before approaching any lender, get a clear picture of your current credit standing. Obtain a free copy of your credit report from all three major credit bureaus (Experian, Equifax, TransUnion) via AnnualCreditReport.com. Review it carefully for any errors and understand your credit score.

Knowing your score and identifying any negative marks will help you anticipate what lenders will see. It also allows you to address inaccuracies, which could potentially improve your score. This proactive step is crucial for setting realistic expectations.

2. Determine Your Budget

Realistically assess what you can afford for a monthly car payment, including insurance, fuel, and maintenance. Don’t just think about the loan payment; consider the total cost of car ownership. Use online calculators to estimate potential payments based on different loan amounts and interest rates.

Pro tips from us: Create a detailed monthly budget to see exactly how much disposable income you have. Factor in potential emergency expenses and ensure your car payment won’t strain your finances, leading to missed payments.

3. Gather Necessary Documents

Lenders will require documentation to verify your identity, income, and residence. Having these ready will streamline the application process.

Typically, you’ll need:

- Government-issued ID (driver’s license).

- Proof of income (pay stubs, bank statements, tax returns if self-employed).

- Proof of residence (utility bill, lease agreement).

- Proof of insurance (you’ll need this before driving off the lot).

- References (sometimes required, especially with lower credit scores).

4. Seek Out Specialized Lenders

Not all lenders offer special financing. Focus your search on those that do. This includes:

- Dealerships with Special Finance Departments: Many large dealerships have dedicated teams that work with a network of subprime lenders.

- Credit Unions: Often more flexible and willing to work with members, even those with less-than-perfect credit.

- Online Lenders: Numerous online platforms specialize in bad credit auto loans. They can often provide pre-approvals quickly.

- "Buy Here, Pay Here" Dealerships: These dealerships act as both the seller and the lender. While convenient, they often come with very high interest rates and should be approached with caution.

5. Get Pre-Approved

Getting pre-approved for a loan is a powerful step. It involves a "soft inquiry" on your credit, which doesn’t hurt your score, and gives you an idea of the loan amount and interest rate you qualify for.

With a pre-approval in hand, you walk into the dealership as a cash buyer, giving you stronger negotiation power. You’ll know your budget before you fall in love with a car outside your financial reach.

6. Choose the Right Vehicle

Given the higher interest rates associated with special financing, it’s prudent to choose an affordable and reliable vehicle. A newer, lower-mileage used car often strikes a good balance between cost and dependability. Avoid buying a vehicle that is overly expensive or prone to frequent repairs, as this adds to your financial burden.

Remember, the goal is not just to get a car, but to get a car that you can comfortably afford and make payments on consistently to rebuild your credit.

7. Understand the Loan Terms

Once you have an offer, meticulously review all the loan terms. This includes the Annual Percentage Rate (APR), the loan term (length of the loan), and the total cost of the loan. Don’t hesitate to ask questions until you fully understand every detail.

Common mistakes to avoid are rushing through the paperwork or signing without clarity. Ensure there are no hidden fees or prepayment penalties you weren’t expecting.

Key Factors Lenders Consider for Special Financing

While your credit score might be the primary hurdle, special financing lenders look at a broader spectrum of factors. Understanding these can help you present yourself as a more attractive borrower. My insights from years in the industry highlight these as crucial elements.

Credit Score (Still Matters, But Differently)

Even in special financing, your credit score provides a baseline. While a low score won’t disqualify you, it will influence the interest rate you’re offered. Lenders use it to categorize the level of risk you represent. A score that’s "poor" is different from "very poor," and this distinction can impact your terms. They also look for recent positive payment history, even if overall credit is challenged.

Income and Employment Stability

This is paramount. Lenders want to see a steady, verifiable source of income that is sufficient to cover your monthly loan payments and other living expenses. They often prefer applicants with a consistent employment history, ideally with the same employer for at least six months to a year. Proof of income, such as recent pay stubs or bank statements, will be heavily scrutinized.

Debt-to-Income (DTI) Ratio

As mentioned earlier, your DTI ratio (monthly debt payments divided by gross monthly income) is a significant indicator of your ability to handle additional debt. While special financing lenders might be more lenient, a very high DTI can still be a barrier. They want to ensure you’re not overextending yourself. A lower DTI indicates you have more disposable income available for loan payments.

Down Payment Amount

A substantial down payment is one of the most effective ways to improve your chances of approval and secure better terms with special financing. A larger down payment reduces the amount you need to borrow, which in turn reduces the lender’s risk. It also shows your commitment to the purchase and your financial discipline.

Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price. The more you put down, the less you finance, leading to lower monthly payments and less interest paid over time.

Co-signer

If your credit is particularly challenging, a co-signer with good credit can significantly strengthen your application. A co-signer legally agrees to be responsible for the loan payments if you fail to make them. This reduces the risk for the lender, making them more willing to approve the loan and potentially offer more favorable interest rates.

However, choosing a co-signer is a serious decision. It impacts their credit and financial obligations, so ensure both parties fully understand the commitment.

Vehicle Choice

The type of vehicle you choose also plays a role. Lenders prefer to finance cars that are newer, have lower mileage, and are known for their reliability and resale value. This is because the car serves as collateral for the loan. If you default, the lender needs to be able to recover their investment by reselling the vehicle. Financing an older, high-mileage, or less reliable car is riskier for them.

Strategies to Improve Your Chances of Approval & Get Better Terms

Securing a special financing car loan is achievable, but getting the best possible terms requires strategic planning. Here are some actionable steps, informed by my years of observing successful borrowers.

Boost Your Credit Score (Even Slightly)

Even a small improvement in your credit score can make a difference.

- Pay bills on time: This is the most impactful action. Even paying a few overdue bills can show immediate positive movement.

- Reduce credit card debt: Lowering your credit utilization (the amount of credit you’re using versus your total available credit) can quickly boost your score.

- Check for errors: Dispute any inaccuracies on your credit report.

Save for a Larger Down Payment

As highlighted earlier, a significant down payment is your secret weapon. The more cash you put down, the less you need to borrow, which directly translates to lower monthly payments and less interest over the loan’s lifetime. It also demonstrates financial responsibility and reduces the lender’s risk, making you a more attractive borrower.

Consider a Co-signer

If you have a trusted friend or family member with good credit who is willing to co-sign for you, this can dramatically improve your chances of approval and help you secure a lower interest rate. A co-signer provides an additional layer of security for the lender. However, ensure both parties understand the full implications, as the co-signer is equally responsible for the debt.

Choose an Affordable and Practical Vehicle

Resist the urge to buy the most expensive car you qualify for. Opt for a reliable, moderately priced vehicle that fits comfortably within your budget. Lenders prefer to finance cars that retain their value well. A more affordable car means lower loan amounts, which reduces the lender’s risk and your monthly financial burden.

Shop Around for Lenders

Don’t settle for the first offer you receive. Different lenders specialize in different types of special financing and may offer varying rates and terms. Apply to several dealerships with special finance departments, credit unions, and online lenders. Compare their offers diligently. Common mistakes to avoid are letting one rejection deter you or accepting an unfavorable deal out of desperation.

Negotiate Terms (Don’t Be Afraid to Ask)

Once you have multiple offers, use them as leverage. You can negotiate not only the purchase price of the car but also the interest rate, loan term, and even fees. If one lender offers a slightly better APR, see if another can match or beat it. Always ensure you understand the total cost, not just the monthly payment.

Consider a Shorter Loan Term (If Affordable)

While a longer loan term means lower monthly payments, it also means paying significantly more in interest over the life of the loan. If your budget allows, opt for the shortest loan term possible. This will save you money in the long run and help you pay off the car faster, freeing up your finances sooner.

Understanding Your Special Financing Loan Terms

When you’re offered a special financing car loan, it’s crucial to understand every detail of the agreement. Don’t let excitement or pressure lead you to sign anything you haven’t thoroughly reviewed. Based on my expertise, these are the key terms you must comprehend.

APR (Annual Percentage Rate)

The APR is arguably the most important number to understand. It represents the total cost of borrowing money for a year, expressed as a percentage. It includes not just the interest rate but also any additional fees or charges associated with the loan. A higher APR means a more expensive loan.

For special financing, APRs will typically be higher than for traditional loans, reflecting the increased risk. Always compare the APRs offered by different lenders, as even a small difference can save you hundreds or thousands of dollars over the loan’s term. Don’t confuse the interest rate with the APR; the APR gives you the full picture.

Loan Term

The loan term is the length of time you have to repay the loan, usually expressed in months (e.g., 36, 48, 60, 72 months).

- Shorter terms: Result in higher monthly payments but less total interest paid over time. They allow you to pay off the car faster and gain equity more quickly.

- Longer terms: Lead to lower monthly payments, making the car seem more affordable. However, you’ll pay significantly more in total interest, and you’re at a higher risk of being "upside down" on your loan (owing more than the car is worth).

Pro tips from us: While a longer term might be tempting for lower payments, consider if you can stretch your budget for a shorter term. This is a powerful way to reduce the overall cost of the loan and build equity faster.

Total Cost of the Loan

This is the sum of the principal loan amount plus all the interest you will pay over the entire loan term, including any fees. Lenders are legally required to disclose this. Always ask for the total cost of the loan before you sign. This figure provides the clearest picture of what you’re truly paying for the vehicle.

Common mistakes to avoid are focusing solely on the monthly payment. A low monthly payment might seem attractive, but it could mask a very long loan term and a significantly higher total cost.

Fees and Charges

Be aware of any additional fees. These can include:

- Origination fees: A fee charged by the lender for processing the loan.

- Documentation (doc) fees: Fees charged by the dealership for preparing paperwork.

- Late payment fees: Penalties for missing a payment deadline.

- Prepayment penalties: Some loans, especially subprime ones, might charge a fee if you pay off the loan early. This is less common now but still worth checking.

Ensure all fees are clearly itemized and explained. Don’t hesitate to question anything that seems unclear or excessive.

Prepayment Penalties

Before finalizing your loan, explicitly ask if there are any prepayment penalties. A prepayment penalty means you will be charged a fee if you decide to pay off your loan earlier than scheduled. While less common with auto loans than with mortgages, they do exist, particularly in subprime markets.

Ideally, you want a loan that allows you to pay it off early without penalty, especially if your goal is to rebuild credit and refinance later. This flexibility can save you a substantial amount of interest.

Rebuilding Credit with a Special Financing Car Loan

One of the most valuable aspects of a special financing car loan, beyond simply getting a vehicle, is its potential to significantly improve your credit score. Based on my years of observing individuals climb out of credit challenges, I can attest to the power of a well-managed auto loan.

How On-Time Payments Help

Your payment history is the single most important factor in your credit score, accounting for about 35% of your FICO score. Every time you make an on-time payment on your special financing car loan, that positive activity is reported to the major credit bureaus (Experian, Equifax, TransUnion).

Consistent, timely payments demonstrate to future lenders that you are a reliable borrower who honors their financial commitments. This steady stream of positive data slowly but surely counteracts previous negative marks, gradually elevating your credit score. It’s a marathon, not a sprint, but each payment is a step forward.

Importance of Consistency

The key to credit rebuilding is unwavering consistency. Missing even one payment can severely damage the progress you’ve made, and a pattern of late payments will negate any benefits. Set up automatic payments or calendar reminders to ensure you never miss a due date.

A stable payment history on a significant installment loan like a car loan shows a strong commitment to financial responsibility. This consistency is what lenders truly value and what will open doors to better financial opportunities in the future.

Monitoring Your Credit Report

As you make payments, regularly monitor your credit report to track your progress. You are entitled to a free credit report from each of the three major bureaus once every 12 months via AnnualCreditReport.com. Review it for accuracy and to see how your score is improving.

Seeing your score rise can be incredibly motivating and allows you to catch any potential errors that might be hindering your progress. It also helps you understand the impact of your responsible payment behavior.

Transitioning to Better Loans in the Future

Once you’ve consistently made on-time payments for 12-24 months and your credit score has improved significantly, you might be in a position to refinance your special financing car loan. Refinancing involves taking out a new loan, typically with a lower interest rate, to pay off your existing loan.

This can drastically reduce your monthly payments and the total amount of interest you pay. It’s a strategic move that allows you to leverage your improved credit to secure more favorable terms, completing the credit rebuilding cycle initiated by your special financing loan.

Common Pitfalls and How to Avoid Them

While special financing offers a valuable opportunity, it’s also ripe with potential pitfalls that can lead to further financial strain. My experience has taught me that awareness is your best defense. Here are common mistakes and how to steer clear of them.

Accepting the First Offer Without Comparison

Common mistakes to avoid are walking into a dealership and accepting the very first loan offer you receive. This is especially true if you’re dealing with credit challenges, as you might feel desperate. Different lenders will offer different rates and terms. Always shop around and get at least 2-3 competitive offers before making a decision. This comparison can save you thousands.

Focusing Only on Monthly Payments

While a low monthly payment might seem appealing, it can be deceptive. A low payment often means a longer loan term, which translates to paying significantly more interest over the life of the loan. Always consider the total cost of the loan, not just the monthly figure. Ask yourself: "How much will I pay for this car, including all interest and fees, by the time it’s paid off?"

Ignoring the Total Cost

Related to the above, neglecting to calculate the total cost of the loan (principal + interest + fees) is a major pitfall. A car advertised at $15,000 might end up costing you $25,000 or more with a high-interest, long-term special financing loan. Understand the full financial commitment before signing.

Falling for "Guaranteed Approval" Scams

Be wary of any lender promising "guaranteed approval" regardless of your credit history. While special financing is accessible, no legitimate lender can guarantee approval without reviewing your financial situation. These promises often hide predatory lending practices, excessively high interest rates, or hidden fees designed to trap you in an unfavorable loan. Always verify a lender’s legitimacy.

Buying More Car Than You Can Afford

It’s easy to get excited and buy a car that stretches your budget. However, overextending yourself can lead to missed payments, repossession, and further damage to your credit. Be realistic about what you can comfortably afford, considering not just the loan payment but also insurance, maintenance, and fuel. Pro tips from us: Aim for a total car cost (loan, insurance, fuel, maintenance) that doesn’t exceed 15-20% of your net monthly income.

Not Understanding the Fine Print

Loan agreements can be complex, filled with jargon and legal terms. Common mistakes to avoid are rushing through the document or signing without fully understanding every clause. Pay particular attention to the APR, loan term, total cost, any prepayment penalties, and late payment fees. If you have questions, ask for clarification until you are completely comfortable. Consider having a trusted advisor review the document if possible.

Conclusion: Your Journey to Driving Forward

Navigating the world of special financing car loans can seem challenging, but with the right knowledge and a strategic approach, it’s a powerful tool for achieving vehicle ownership and rebuilding your financial future. We’ve explored what these loans entail, who benefits from them, the crucial factors lenders consider, and how to optimize your application process.

Remember, a special financing loan isn’t just about getting a car today; it’s about leveraging that opportunity to demonstrate financial responsibility and pave the way for a stronger credit profile tomorrow. By understanding the pros and cons, meticulously preparing your application, and diligently managing your loan, you can transform a challenging credit situation into a stepping stone for future financial success.

The road ahead may have a few bumps, but armed with this comprehensive guide, you are well-equipped to drive forward with confidence. Make informed decisions, prioritize your financial well-being, and soon you’ll be enjoying the freedom of the open road, all while building a brighter financial future.

For more insights into managing your finances and understanding various loan options, feel free to explore our other articles such as How to Improve Your Credit Score Fast or Understanding Auto Loan Refinancing. Additionally, for independent credit advice and tools, you can visit a trusted external source like the Consumer Financial Protection Bureau at www.consumerfinance.gov.

Disclaimer: This article provides general information and guidance on special financing car loans and is not intended as financial advice. Always consult with a qualified financial advisor or credit counselor for personalized advice based on your specific financial situation.