Navigating STCU Car Loan Rates: Your Ultimate Guide to Driving Away with the Best Deal

Navigating STCU Car Loan Rates: Your Ultimate Guide to Driving Away with the Best Deal Carloan.Guidemechanic.com

Buying a car is an exciting milestone, but securing the right financing can often feel like navigating a complex maze. When it comes to finding competitive rates and exceptional service, credit unions like STCU (Spokane Teachers Credit Union) frequently stand out. But what exactly are STCU car loan rates, and how can you ensure you’re getting the best possible deal?

As an expert blogger and professional SEO content writer with extensive experience in personal finance, I understand the nuances of auto loans. My goal with this comprehensive guide is to demystify STCU car loan rates, providing you with in-depth insights, actionable strategies, and insider tips to help you make an informed decision. We’ll cover everything from understanding what influences your rate to navigating the application process, ensuring you drive away not just with a new car, but with a smart financial choice.

Navigating STCU Car Loan Rates: Your Ultimate Guide to Driving Away with the Best Deal

What Makes STCU Unique for Car Loans? A Credit Union Advantage

Before diving into the specifics of rates, it’s crucial to understand the fundamental difference between a credit union like STCU and a traditional bank. This distinction directly impacts the kind of experience and potential benefits you might receive when seeking an auto loan.

Credit unions are not-for-profit financial cooperatives owned by their members. This member-centric philosophy often translates into several advantages, especially when it comes to lending products like car loans. Unlike banks, which aim to maximize profits for shareholders, credit unions prioritize returning value to their members through lower fees, higher savings rates, and, importantly, more competitive loan rates.

Based on my experience, this model fosters a strong sense of community and personalized service. STCU, serving the Spokane and broader Pacific Northwest regions, embodies this principle. They are often able to offer car loan rates that are significantly lower than those found at many commercial banks, making them a top choice for individuals looking to finance a vehicle responsibly.

Moreover, credit unions typically have a more flexible approach to lending. While stringent credit requirements still apply, they often consider a broader range of factors beyond just a credit score, especially for existing members. This can be a huge benefit for those with less-than-perfect credit history, who might find it challenging to secure favorable terms elsewhere.

Understanding STCU Car Loan Rates: The Core Factors

When you look at STCU car loan rates, you’ll notice they aren’t a one-size-fits-all number. Several critical factors come into play, shaping the specific rate you’ll be offered. Grasping these elements is the first step toward optimizing your loan.

Your Credit Score: The Ultimate Rate Influencer

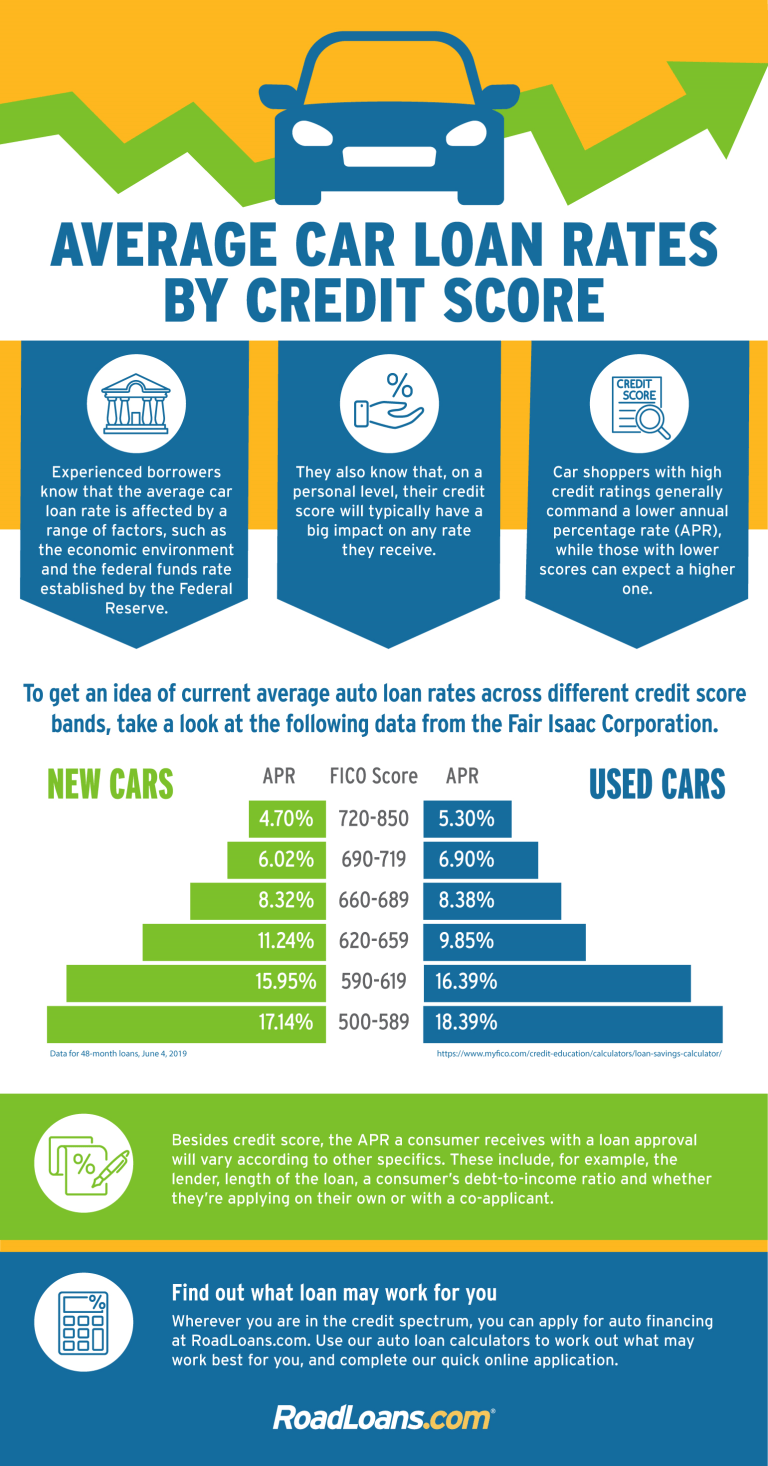

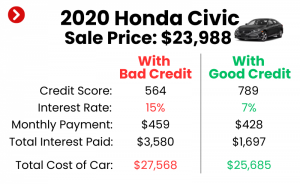

Your credit score is arguably the most significant determinant of the interest rate you’ll receive on an STCU car loan. Lenders use this three-digit number to assess your creditworthiness – essentially, how likely you are to repay your debt. A higher credit score signals lower risk to the lender, which typically translates into a lower interest rate for you.

For instance, an applicant with an excellent credit score (typically 760+) might qualify for STCU’s absolute lowest advertised rates. Conversely, someone with a fair or good score (e.g., 620-699) will likely be offered a higher rate to compensate for the perceived increased risk. This isn’t just about qualifying; it’s about the financial impact over the life of the loan.

Pro tips from us: Always check your credit score and credit report before applying for any significant loan. Websites like AnnualCreditReport.com allow you to get a free report from each of the three major bureaus (Experian, EquiFax, TransUnion) once a year. Rectifying any errors or improving your score even slightly can make a substantial difference in your STCU car loan rates.

Loan Term: Balancing Monthly Payments and Total Cost

The loan term, or the length of time you have to repay the loan, also plays a crucial role in your interest rate. Generally, shorter loan terms (e.g., 36 or 48 months) come with lower interest rates because the lender’s risk exposure is reduced. However, shorter terms also mean higher monthly payments.

Conversely, longer loan terms (e.g., 60 or 72 months) often carry slightly higher interest rates. While they offer the appeal of lower monthly payments, this convenience comes at a cost. The longer you take to repay, the more interest you’ll accrue over the life of the loan, significantly increasing the total amount you pay for the vehicle.

Based on my experience, many borrowers opt for longer terms to keep monthly payments affordable, but it’s essential to weigh this against the total cost. A slightly higher monthly payment for a shorter term could save you thousands in interest over the life of the loan. STCU offers a range of flexible terms, allowing you to find a balance that suits your budget and financial goals.

Vehicle Type and Age: New vs. Used Car Rates

The type and age of the vehicle you’re financing also impact STCU car loan rates. New cars typically qualify for the lowest rates because they are considered less risky to lenders. They have a predictable value, come with warranties, and are less likely to require immediate costly repairs.

Used cars, on the other hand, often come with slightly higher interest rates. The reasoning is simple: used vehicles have already depreciated, their condition can vary, and they present a higher risk of mechanical issues. However, STCU still offers very competitive rates for used car loans, often depending on the vehicle’s age and mileage. For example, a nearly new used car (1-2 years old) might qualify for rates very close to new car rates.

It’s also worth noting that private party sales might be financed differently than vehicles purchased from a dealership. STCU is adept at handling various scenarios, so always discuss your specific vehicle purchase plans with them.

Down Payment: Your Financial Lever

Making a significant down payment can positively influence your STCU car loan rate. A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. When you have more equity in the vehicle from the start, you’re less likely to default on the loan, making you a more attractive borrower.

Common mistakes to avoid are thinking you must finance 100% of the vehicle. While zero down payment options exist, they often come with higher interest rates and mean you’ll owe more than the car is worth as soon as you drive it off the lot. Aiming for at least a 10-20% down payment can not only secure a better rate but also provide a buffer against rapid depreciation.

Understanding APR vs. Interest Rate

When comparing loan offers, you’ll encounter two terms: interest rate and Annual Percentage Rate (APR). While often used interchangeably, there’s a crucial difference. The interest rate is simply the cost of borrowing the principal amount. The APR, however, represents the total cost of the loan, including the interest rate plus any additional fees (like origination fees, if applicable).

STCU, like other reputable lenders, will provide you with the APR. This is the number you should focus on when comparing offers, as it gives you the most accurate picture of the total cost of financing. Always ask for the APR to ensure an apples-to-apples comparison.

How to Find Your Best STCU Car Loan Rate (and Improve It!)

Securing the most favorable STCU car loan rate requires a proactive approach. It’s not just about what STCU offers, but also about how you position yourself as a borrower.

Deep Dive into Credit Score Improvement

As mentioned, your credit score is paramount. If your score isn’t in the "excellent" range, there are steps you can take to improve it, potentially unlocking better STCU car loan rates.

- Pay Bills on Time: Payment history is the most significant factor in your credit score. Set up automatic payments or reminders to ensure you never miss a due date.

- Reduce Credit Card Balances: High credit utilization (using a large percentage of your available credit) negatively impacts your score. Pay down balances to below 30% of your credit limit, ideally even lower.

- Avoid New Credit Inquiries (Temporarily): Each time you apply for new credit, a hard inquiry appears on your report, which can temporarily ding your score. Try to avoid applying for other loans or credit cards in the months leading up to your car loan application.

- Review Your Credit Report for Errors: Mistakes on your credit report can unjustly lower your score. Dispute any inaccuracies immediately with the credit bureaus.

Based on my experience, even a 20-30 point improvement in your credit score can shift you into a better rate tier, saving you hundreds or even thousands over the loan’s life. This effort is well worth the time invested.

STCU Membership Benefits: More Than Just a Number

One of the most powerful ways to secure excellent STCU car loan rates is by being an active member. While STCU is open to anyone living, working, or worshipping in certain counties (primarily in Eastern Washington and Northern Idaho), deepening your relationship can yield benefits.

- Exclusive Rate Discounts: STCU often provides rate discounts to members who sign up for automatic payments from an STCU checking account, or those who maintain a certain level of relationship with the credit union. Always ask about these potential discounts.

- Relationship Pricing: Some credit unions offer "relationship pricing" where your rate is slightly better if you have multiple accounts or services with them (e.g., checking, savings, mortgage, credit card).

- Financial Counseling: STCU, like many credit unions, offers financial education and counseling services. Utilizing these can help you manage your finances better, which indirectly supports a stronger credit profile for future loans.

Becoming a member is usually straightforward, involving opening a savings account with a small deposit. This simple step can unlock a world of benefits, including potentially superior STCU car loan rates.

Comparing Rates: Don’t Settle for the First Offer

Even if you love STCU, it’s always a smart financial move to compare offers from a few different lenders. This doesn’t mean you have to abandon STCU; rather, it empowers you with negotiation leverage and confirms you’re getting the best deal.

- Pre-Approval from Multiple Lenders: Apply for pre-approval with STCU and one or two other reputable lenders. Because car loan inquiries are often grouped together within a short period (typically 14-45 days, depending on the scoring model), they usually count as a single hard inquiry on your credit report, minimizing impact.

- Dealer Financing vs. Credit Union: Dealerships often offer their own financing options, sometimes with promotional rates. However, based on my experience, credit unions like STCU frequently beat dealer rates, especially once all dealer markups and fees are considered. Always get a quote from STCU before you visit the dealership.

The STCU Car Loan Application Process: A Step-by-Step Guide

Applying for an STCU car loan is designed to be a straightforward process. Knowing what to expect can ease any anxiety and help you prepare efficiently.

Pre-Approval: Your Secret Weapon at the Dealership

Getting pre-approved for an STCU car loan is, in my opinion, one of the most crucial steps you can take. Pre-approval means STCU has reviewed your financial information and determined how much they are willing to lend you, at what interest rate, before you even pick out a specific car.

- Empowerment: You walk into the dealership with financing already secured, turning you into a cash buyer. This shifts the negotiation power in your favor, allowing you to focus purely on the vehicle’s price, rather than getting entangled in financing discussions with the salesperson.

- Budget Clarity: Pre-approval clearly defines your budget, preventing you from falling in love with a car outside your financial comfort zone.

- Speed: It significantly speeds up the car-buying process, as much of the paperwork is already handled.

To get pre-approved, you can apply online, by phone, or in person at an STCU branch.

Required Documents: Get Organized

While the exact list can vary slightly, having these documents ready will streamline your application:

- Identification: Government-issued ID (driver’s license, passport).

- Income Verification: Pay stubs (most recent 1-2 months), W-2s, or tax returns (if self-employed). This helps STCU confirm your ability to repay the loan.

- Proof of Residence: Utility bill or lease agreement.

- Vehicle Information (if already chosen): VIN, make, model, year, mileage. If you’re pre-approved, you’ll provide this later.

- Current Debt Information: Details on existing loans or mortgages.

Common mistakes to avoid are providing incomplete or inaccurate information. Double-check everything before submitting to prevent delays.

Online vs. In-Person Application: Which is Best for You?

STCU offers multiple ways to apply, each with its advantages:

- Online Application: This is often the quickest and most convenient option. You can apply from anywhere, anytime, and usually get a decision rapidly. It’s excellent for those who are comfortable with digital processes and have all their documents ready electronically.

- In-Person Application: Visiting an STCU branch allows for personalized guidance. You can ask questions directly, discuss your specific situation, and receive immediate assistance. This is ideal if you prefer face-to-face interaction or have a complex financial situation.

- Phone Application: A good middle ground, offering personalized assistance without needing to travel to a branch.

Regardless of your chosen method, STCU’s member service is typically highly rated, ensuring you’ll receive support throughout the process.

Beyond the Rate: Other Factors to Consider with STCU

While STCU car loan rates are a primary concern, the overall value of a loan extends beyond just the interest percentage. STCU offers several features that enhance the borrowing experience and provide additional financial protection.

Flexible Loan Terms: Tailoring to Your Life

STCU understands that financial situations vary. They typically offer a range of loan terms, allowing you to choose one that best fits your budget and repayment strategy. Whether you prefer a shorter term to pay off your loan faster and save on interest, or a longer term to reduce your monthly payments, STCU can work with you.

This flexibility is a significant benefit. Pro tips from us: always consider your long-term financial goals when selecting a loan term. While a longer term might seem appealing due to lower monthly payments, remember the increased total interest paid. Aim for the shortest term you can comfortably afford.

No Prepayment Penalties: The Freedom to Pay Early

A huge advantage of STCU car loans is the absence of prepayment penalties. This means you can pay off your loan early without incurring any extra fees. This feature offers immense financial freedom.

If your financial situation improves, or you receive an unexpected windfall, you have the option to pay down or pay off your loan ahead of schedule. Doing so directly reduces the amount of interest you’ll pay over the life of the loan, saving you money. Based on my experience, not all lenders offer this, making it a key differentiator for STCU.

Payment Protection Options: Peace of Mind

STCU offers various payment protection options designed to safeguard your financial well-being in unforeseen circumstances. These can include:

- Guaranteed Asset Protection (GAP) Insurance: If your car is stolen or totaled, your regular insurance might only cover the vehicle’s market value, which could be less than what you still owe on your loan (especially early in the loan term). GAP insurance covers this difference, preventing you from being upside down on your loan.

- Debt Protection: This coverage can help make your loan payments or even pay off your loan in the event of disability, involuntary unemployment, or death. It provides a crucial safety net for you and your family.

While these options add to your monthly payment, they can offer invaluable peace of mind. It’s important to understand what they cover and assess if they align with your personal risk tolerance.

Excellent Member Service: Your Partner in Finance

As a credit union, STCU prides itself on its member service. This often means more personalized attention, readily available financial advice, and a genuine interest in your financial success. If you have questions about your loan, need to adjust payments (within terms), or explore other financial products, their team is typically responsive and helpful.

This level of service can be a huge asset, especially for first-time car buyers or those who appreciate a more human touch in their financial dealings.

Refinancing Your Car Loan with STCU: A Smart Move for Savings

Perhaps you already have a car loan, but your financial situation has improved, or you’ve discovered STCU’s competitive rates. Refinancing your car loan with STCU could be a very smart financial move.

When is Refinancing a Good Idea?

- Improved Credit Score: If your credit score has significantly improved since you took out your original loan, you might qualify for a much lower STCU car loan rate.

- Lower Current Rates: If general interest rates have dropped, or STCU is offering a promotional rate, refinancing could save you money.

- Change in Financial Situation: If you need to lower your monthly payments, refinancing to a longer term (though this might increase total interest) could provide temporary relief. Conversely, if you want to pay off faster, refinancing to a shorter term could be an option.

- Eliminate Prepayment Penalties: If your current loan has prepayment penalties, refinancing with STCU means you can pay off your new loan early without fees.

The process for refinancing is similar to applying for a new loan. You’ll submit an application to STCU, they’ll review your creditworthiness, and if approved, they will pay off your old loan, and you’ll begin making payments to STCU at your new, hopefully lower, rate.

Pro Tips for Securing the Best STCU Car Loan Rates

To truly maximize your chances of getting the best possible STCU car loan rate, keep these expert tips in mind:

- Shop Around, Even if You Love STCU: While STCU offers excellent rates, getting pre-approvals from 2-3 different lenders allows you to compare and negotiate effectively. This confirms you’re getting the best deal available to you.

- Negotiate the Car Price First, Then the Financing: This is a golden rule of car buying. Keep the car’s price negotiation separate from the financing. Secure your STCU pre-approval, then focus on getting the best price for the vehicle itself. Don’t let a salesperson distract you with financing tricks.

- Understand the Total Cost of the Loan: Don’t just look at the monthly payment. Calculate the total interest you’ll pay over the loan term. STCU’s loan calculators can help with this. A lower monthly payment over a longer term might mean significantly more money out of your pocket in the long run.

- Consider All Associated Costs: Remember to budget for car insurance, registration fees, maintenance, and fuel. Your car loan is just one piece of the car ownership puzzle.

- Be Honest and Transparent: Provide accurate information on your application. Any discrepancies can lead to delays or even loan denial.

Conclusion: Drive Away Confidently with an STCU Car Loan

Securing a car loan doesn’t have to be a stressful experience. By understanding the factors that influence STCU car loan rates, proactively managing your credit, and leveraging the benefits of STCU membership, you can position yourself for a truly excellent deal. STCU’s commitment to competitive rates, flexible terms, and exceptional member service makes them a compelling choice for financing your next vehicle.

Remember, the goal is not just to get a car, but to make a financially sound decision that supports your overall well-being. By following the in-depth advice provided in this guide, you’ll be well-equipped to navigate the process, understand the true cost of borrowing, and drive away with confidence, knowing you’ve secured the best possible STCU car loan rate for your needs.

Ready to take the next step? Visit STCU’s official website or stop by a local branch to learn more about their current car loan rates and begin your pre-approval process today.

Disclaimer: This article provides general information and is not financial advice. Car loan rates and terms are subject to change and depend on individual creditworthiness and market conditions. Always consult with a qualified financial advisor and STCU directly for personalized guidance and the most current information.

Further Reading: