Navigating Subprime Car Loans Near Me: Your Ultimate Guide to Driving Away with Confidence

Navigating Subprime Car Loans Near Me: Your Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

Finding yourself in need of a car but facing a less-than-perfect credit score can feel like navigating a maze blindfolded. Many people believe that a low credit score automatically disqualifies them from car ownership. However, that’s simply not true. The reality is, options exist, and one of the most prominent is a subprime car loan.

This comprehensive guide is designed to demystify subprime auto financing, particularly focusing on how to find subprime car loans near me. We’ll delve deep into what these loans entail, how to prepare for them, and most importantly, how to use them as a stepping stone to improve your financial standing. Our goal is to equip you with the knowledge and confidence to make informed decisions, ensuring you drive away with a car and a clear path toward better credit.

Navigating Subprime Car Loans Near Me: Your Ultimate Guide to Driving Away with Confidence

Understanding Subprime Car Loans: What Are They Really?

Before we dive into finding "subprime car loans near me," let’s clarify what a subprime car loan truly is. Essentially, these are auto loans offered to individuals who have credit scores below a certain threshold, typically below 660 on the FICO scale. This range often includes scores considered "fair," "poor," or "very poor."

Lenders categorize these borrowers as having a higher risk of defaulting on their payments. Because of this elevated risk, subprime loans typically come with higher interest rates compared to loans offered to borrowers with excellent credit. This higher interest rate compensates the lender for the increased risk they are taking on.

Why do these loans exist? They serve a crucial purpose in the auto financing market by providing access to transportation for millions of Americans who might otherwise be denied. For many, a car isn’t a luxury; it’s a necessity for work, school, and daily life. Subprime loans bridge this gap, offering a vital lifeline to those with imperfect credit histories.

Based on my experience working with countless individuals, subprime loans are not just about getting a car; they represent an opportunity. They allow you to demonstrate financial responsibility, rebuild your credit, and eventually qualify for more favorable lending terms. It’s a chance to turn a challenging situation into a positive financial journey.

Is a Subprime Car Loan Right for You? Weighing the Pros and Cons

Deciding whether to pursue a subprime car loan requires careful consideration. While they offer a valuable solution for many, it’s essential to understand both the advantages and disadvantages before committing.

The Advantages: More Than Just a Car

- Access to Essential Transportation: For many, a car is non-negotiable. It’s critical for commuting to work, taking children to school, attending appointments, and managing daily responsibilities. A subprime loan provides the means to acquire this essential asset when traditional financing avenues are closed.

- Opportunity to Rebuild Your Credit: This is arguably the most significant long-term benefit. By consistently making on-time payments on a subprime auto loan, you demonstrate reliability to credit bureaus. This positive payment history is a powerful factor in improving your credit score over time, opening doors to better rates on future loans and credit cards.

- Emergency Solution: Life throws unexpected curveballs. If you suddenly need a vehicle due to an old car breaking down beyond repair, a subprime loan can provide a quick solution when other options aren’t available. It helps you avoid prolonged disruption to your life and livelihood.

The Disadvantages: Understanding the Trade-offs

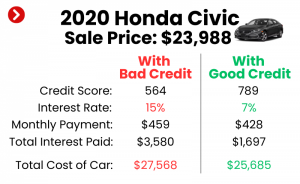

- Higher Interest Rates and Overall Cost: The most prominent drawback is the increased cost of borrowing. Subprime loans carry significantly higher Annual Percentage Rates (APRs) than prime loans. This means you’ll pay much more in interest over the life of the loan, making the car considerably more expensive in the long run.

- Stricter Terms and Conditions: Lenders offering subprime loans often impose more stringent terms. This could include shorter repayment periods, higher down payment requirements, or specific conditions regarding the type of vehicle you can purchase (e.g., newer models might be harder to finance).

- Risk of Negative Equity: Due to higher interest and potentially longer loan terms, you might find yourself in a situation where you owe more on the car than it’s worth. This is known as negative equity, and it can be a problem if you need to sell or trade in the vehicle before the loan is significantly paid down.

- Limited Choice of Vehicles: Depending on the lender and your specific credit profile, you might have fewer options when it comes to the make, model, or age of the car you can finance. Lenders often prefer to finance vehicles that hold their value better or are within a certain price range for subprime borrowers.

Common mistakes to avoid are rushing into a loan without fully understanding the total cost, or focusing solely on the monthly payment without considering the interest rate and total amount paid over time. Always read the fine print carefully and ask questions until you’re completely clear on all terms.

Preparing for Your Subprime Car Loan Journey

Success with a subprime car loan isn’t just about finding a lender; it’s about preparation. Approaching the process strategically can significantly improve your chances of approval and help you secure the best possible terms.

1. Know Your Credit Score and Report Inside Out

Your credit score is the first thing lenders will look at. Obtain a copy of your credit report from all three major credit bureaus (Experian, Equifax, and TransUnion) and review them thoroughly. Look for any errors or inaccuracies that could be negatively impacting your score. Disputing and correcting these can sometimes boost your score surprisingly quickly.

Understanding what’s on your report also helps you anticipate what lenders will see. It allows you to explain any past issues proactively, showing lenders that you’re aware of your financial history and are committed to improvement. This transparency can build trust.

2. Create a Realistic Budget

Before even looking at cars, determine how much you can truly afford for a monthly car payment, insurance, fuel, and maintenance. Remember that a car loan is just one part of the total cost of ownership. Don’t stretch your budget too thin, as missing payments will only worsen your credit situation.

Pro tips from us: Factor in all potential costs. Use an online car loan calculator to estimate payments based on different interest rates and loan terms. This will give you a clearer picture of what’s financially feasible for you each month without creating additional stress.

3. Save for a Down Payment

A significant down payment is one of the most powerful tools you have when applying for a subprime car loan. Lenders view a larger down payment as a sign of your commitment and reduces their risk. It immediately lowers the amount you need to borrow, which in turn reduces your monthly payments and the total interest you’ll pay over the life of the loan.

Aim for at least 10-20% of the car’s purchase price, if possible. Even a smaller down payment is better than none. It demonstrates your ability to save and invest in the purchase, making you a more attractive borrower.

4. Gather All Necessary Documents

Being prepared with your documents can streamline the application process and show lenders you’re serious. Typically, you’ll need:

- Proof of identity (driver’s license, state ID)

- Proof of residence (utility bill, lease agreement)

- Proof of income (recent pay stubs, bank statements, tax returns if self-employed)

- Proof of insurance (or be ready to obtain it)

- References (sometimes requested)

Having these documents organized and ready can save you time and potential frustration during the application phase. It shows you’re a responsible applicant.

Finding "Subprime Car Loans Near Me": Your Local Search Strategy

The phrase "subprime car loans near me" is more than just a search query; it’s a quest for local, accessible solutions. While the internet offers a vast array of options, understanding where to look locally can provide distinct advantages, including face-to-face interaction and potentially faster processing.

1. Online Search: Your Starting Point

Begin your search with specific online queries like "subprime auto loans ," "bad credit car dealerships near me," or "car loans for poor credit ." This will generate a list of local dealerships and lenders that specialize in or are open to working with individuals with lower credit scores.

Look for lenders or dealerships that explicitly advertise "bad credit financing," "second-chance auto loans," or "special finance programs." These are typically indicators that they have departments dedicated to helping borrowers in your situation.

2. Dealerships with Special Finance Departments

Many larger dealerships, particularly those part of a chain or brand, have dedicated "special finance" or "credit re-establishment" departments. These departments employ finance managers who specialize in working with a network of subprime lenders. They understand the nuances of bad credit auto financing and can often match you with a suitable loan product.

When visiting these dealerships, be upfront about your credit situation. This transparency can save time and help them identify the right lending partners for you more quickly. They often have relationships with multiple lenders, increasing your chances of approval.

3. Buy-Here-Pay-Here (BHPH) Dealerships: A Last Resort?

Buy-Here-Pay-Here (BHPH) dealerships are another option for those struggling to secure traditional financing. These dealerships act as both the seller and the lender, meaning you make your car payments directly to them. They are often more lenient with credit requirements, as they primarily focus on your income stability.

However, BHPH dealerships often come with significant drawbacks: higher interest rates, limited vehicle selection (often older, higher-mileage cars), and sometimes less transparent pricing. Based on my experience, while they offer immediate solutions, they should generally be considered if other avenues for subprime car loans near me have been exhausted. Always exercise extreme caution, read contracts meticulously, and ensure the vehicle is thoroughly inspected before committing.

4. Local Banks and Credit Unions

While traditional banks and credit unions are often perceived as only lending to those with excellent credit, some do offer programs for borrowers with less-than-perfect scores. Credit unions, in particular, are member-focused and might be more flexible. They sometimes offer "fresh start" or "credit builder" loans.

It’s worth contacting local branches to inquire about their specific auto loan programs. Even if they don’t offer direct subprime loans, they might be able to refer you to a trusted partner lender in the area. Building a relationship with a local financial institution can also be beneficial for your long-term financial health.

5. Online Subprime Lenders

Beyond local options, numerous online lenders specialize in subprime car loans. Companies like Capital One Auto Finance, myAutoloan, or Carvana (which also offers financing) often cater to a wider range of credit scores. Applying online can provide quick pre-approvals and allow you to compare offers from multiple lenders without visiting multiple dealerships.

However, be diligent when applying online. Ensure the lender is reputable, read reviews, and understand their terms. While convenient, the personal touch of a local dealer or bank might be preferred by some.

Navigating the Application and Approval Process

Once you’ve identified potential lenders for subprime car loans near me, the next step is the application process. Understanding what lenders look for and how to present yourself can significantly impact your approval odds and the terms you receive.

1. Pre-qualification vs. Pre-approval: Know the Difference

- Pre-qualification: This is an initial, soft inquiry into your creditworthiness, usually based on basic information you provide. It gives you an estimate of what loan amount you might qualify for and what interest rate to expect, without impacting your credit score. It’s a great way to gauge your options without commitment.

- Pre-approval: This involves a more thorough review, including a hard credit inquiry, which might slightly ding your credit score. However, a pre-approval means a lender has provisionally agreed to lend you a specific amount at a specific interest rate, subject to final verification. Having a pre-approval in hand gives you significant bargaining power at the dealership, as you know your financing is secured.

Pro tips from us: Always aim for pre-approval from at least one or two lenders before stepping onto a dealership lot. This shifts the focus from "can I get a loan?" to "which car can I get with my approved loan?"

2. What Lenders Look For

When evaluating your application for a subprime car loan, lenders consider several key factors:

- Income Stability: Lenders want to see a consistent, verifiable source of income. This demonstrates your ability to make regular payments. The longer you’ve been employed at your current job, the better.

- Debt-to-Income Ratio (DTI): This ratio compares your total monthly debt payments to your gross monthly income. Lenders prefer a lower DTI, as it indicates you have enough disposable income to comfortably afford a car payment.

- Down Payment: As mentioned, a larger down payment reduces the loan amount and the lender’s risk, making you a more attractive borrower.

- Payment History: Even with bad credit, a lender will look for any recent positive payment history or signs of improvement. They want to see that past issues are in the past and you’re now committed to financial responsibility.

Common mistakes to avoid are applying to too many lenders at once. While comparing offers is good, multiple hard inquiries in a short period can further lower your credit score. Group your applications within a 14-45 day window, as credit bureaus often count these as a single inquiry for rate shopping purposes.

3. The Power of a Co-signer

If you’re struggling to get approved or offered very high interest rates, a co-signer can significantly improve your chances. A co-signer is someone with good credit who agrees to take on legal responsibility for the loan if you default. Their strong credit profile can help you secure better terms.

However, a co-signer takes on significant risk. If you miss payments, their credit score will be negatively impacted, and they will be legally obligated to pay the loan. Only consider a co-signer if you are absolutely confident in your ability to make all payments on time, and only with someone you trust implicitly and who fully understands the risks involved.

Making the Most of Your Subprime Car Loan: Rebuilding Your Credit

Securing a subprime car loan is not the end of the journey; it’s the beginning of an opportunity to transform your financial future. The most crucial step after getting approved is to use this loan as a tool to rebuild your credit.

1. Consistent On-Time Payments: Your Top Priority

This cannot be stressed enough: making every single car payment on time, every month, is paramount. Payment history is the most significant factor (35%) in your credit score calculation. Each on-time payment contributes positively to your credit report, slowly but surely raising your score.

Set up automatic payments if possible, or mark your calendar with reminders. Avoid late payments at all costs, as even one can severely damage the progress you’re making. Think of each payment as an investment in your financial future.

2. Refinancing Opportunities: A Path to Lower Rates

As you make consistent on-time payments, your credit score will improve. After 6-12 months of diligent payments, you might qualify for refinancing. Refinancing means taking out a new loan, often with a lower interest rate, to pay off your existing subprime loan.

This can significantly reduce your monthly payments and the total interest you’ll pay over the life of the loan. Shop around for refinance options once your credit score shows substantial improvement. It’s a smart financial move that rewards your hard work. offers more insights into this process.

3. Monitoring Your Credit Regularly

Keep an eye on your credit report and score throughout your loan term. You can get free copies of your credit report annually from AnnualCreditReport.com. Many credit card companies and banks also offer free credit score monitoring services.

Monitoring helps you track your progress, identify any potential errors, and understand how your consistent payments are positively impacting your score. Seeing your score improve can be a great motivator to continue your financial discipline.

4. Financial Discipline Beyond the Car Loan

While the subprime car loan is a major focus, remember that your overall financial habits contribute to your credit health. Continue to pay all other bills on time, keep credit card balances low, and avoid taking on unnecessary new debt. A holistic approach to financial responsibility will yield the best results for your credit score.

Avoiding Pitfalls and Protecting Yourself

While subprime car loans near me offer a valuable path to vehicle ownership, it’s crucial to approach them with caution and awareness. There are common pitfalls and predatory practices to avoid.

1. Beware of High-Pressure Sales Tactics

Some dealerships or lenders might try to rush you into a decision or pressure you into buying a more expensive car than you need or can afford. They might highlight low monthly payments without fully disclosing the high interest rate or extended loan term.

Do not feel obligated to make a decision on the spot. Take the contract home, review it, and if possible, have someone you trust look it over. A reputable lender will give you time to consider your options.

2. Understand the Fine Print

The loan contract is a legally binding document. Read every single clause carefully before signing. Pay close attention to:

- Annual Percentage Rate (APR): This is the true cost of the loan, including interest and certain fees. Compare APRs, not just interest rates.

- Loan Term: How many months will you be making payments? Longer terms mean lower monthly payments but significantly more interest paid over time.

- Total Amount Paid: Ensure you understand the total cost of the car and the loan over its entire duration.

- Prepayment Penalties: Some loans charge a fee if you pay off the loan early. Know if your loan has this clause, especially if you plan to refinance.

Ask questions about anything you don’t understand. If a lender or dealer is unwilling to clarify terms, that’s a red flag.

3. Be Wary of Unnecessary Add-ons and Extras

Dealerships often try to sell you additional products like extended warranties, gap insurance, paint protection, or VIN etching. While some of these might be useful (like gap insurance for a subprime loan where you might quickly owe more than the car is worth), many are overpriced or unnecessary.

These add-ons increase the total amount you’re financing, which means more interest and higher monthly payments. Decide what you truly need before you go to the dealership and stick to your budget.

4. Protect Yourself from Scams

Unfortunately, the subprime lending market can attract unscrupulous actors. Be wary of lenders who:

- Guarantee approval without checking your credit or income.

- Ask for upfront fees before processing your application.

- Pressure you into signing blank documents.

- Don’t have a physical address or verifiable contact information.

If something feels too good to be true, it probably is. Stick to reputable dealerships and lenders with established track records.

Conclusion: Your Road to Financial Freedom Starts Here

Securing subprime car loans near me is a journey that requires research, patience, and a strategic approach. While your credit history may present challenges, it doesn’t have to be a permanent roadblock to owning a reliable vehicle. By understanding what subprime loans are, preparing meticulously, exploring your local and online options, and diligently managing your payments, you can turn a perceived disadvantage into a powerful opportunity for financial growth.

Remember, a subprime auto loan isn’t just about getting from point A to point B; it’s a vital tool for rebuilding your credit and establishing a stronger financial future. With the right mindset and disciplined execution, you can navigate this process successfully, drive away with confidence, and pave the way for better lending opportunities down the road. Take control of your financial narrative – your journey to better credit starts with that first responsible car payment.