Navigating the $20,000 Car Loan: Your Ultimate Guide to Smart Financing

Navigating the $20,000 Car Loan: Your Ultimate Guide to Smart Financing Carloan.Guidemechanic.com

Securing a car loan is a significant financial decision, and for many, a $20,000 car loan represents a sweet spot – enough to purchase a reliable new vehicle or a fantastic used one without breaking the bank. However, navigating the world of auto financing can feel overwhelming. With so many options, terms, and conditions, it’s easy to get lost.

This comprehensive guide is designed to empower you with the knowledge and strategies needed to secure the best possible $20,000 car loan. We’ll delve deep into every aspect, from understanding interest rates and credit scores to the application process and common pitfalls to avoid. Our goal is to make your journey to owning your dream car as smooth and affordable as possible.

Navigating the $20,000 Car Loan: Your Ultimate Guide to Smart Financing

Understanding the $20,000 Car Loan Landscape

A $20,000 car loan is a common and accessible financing option that opens up a wide range of vehicle choices. This amount can finance a brand-new compact car, a well-equipped mid-size sedan, or a highly reliable, low-mileage used SUV. It’s a versatile budget that offers both practicality and a degree of comfort.

The journey to securing this loan involves understanding several interconnected factors. These include your personal financial health, the type of vehicle you choose, and the current economic climate. Each element plays a crucial role in determining your eligibility and the ultimate cost of your financing.

Our aim is to demystify this process, providing clear insights into how lenders assess your application. By the end of this article, you’ll be equipped to approach your $20,000 car loan application with confidence and a solid plan.

Key Factors Influencing Your $20,000 Car Loan Approval and Terms

When you apply for a $20,000 car loan, lenders evaluate several critical aspects of your financial profile. Understanding these factors is paramount to securing favorable terms and ensuring approval. Let’s break down the most influential elements.

A. Your Credit Score: The Cornerstone of Loan Approval

Your credit score is arguably the single most important factor in determining your car loan interest rate and approval chances. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. A higher score signals less risk to lenders.

For a $20,000 car loan, a strong credit score (generally 700+) can unlock the lowest interest rates, significantly reducing your total cost. Conversely, a lower score will likely result in higher interest rates, as lenders compensate for the perceived increased risk. This means you’ll pay more over the life of the loan.

Based on my experience, even a small improvement in your credit score can translate into substantial savings on interest. It’s always advisable to check your credit report well before applying for a loan to identify and rectify any errors. If your score is on the lower side, focusing on timely payments and reducing existing debt can make a big difference.

B. Down Payment: Lowering Your Loan Burden

A down payment is the initial amount of money you pay upfront for the car, reducing the total amount you need to borrow. Making a significant down payment for your $20,000 car loan offers numerous advantages. It immediately lowers your monthly payments, as you’re financing a smaller principal amount.

Furthermore, a larger down payment often helps you secure a better interest rate. Lenders view borrowers who put down more money as less risky, as they have more equity in the vehicle from the start. This can be a powerful negotiating tool.

Pro tips from us: Aim for at least a 10-20% down payment on your $20,000 car loan. For a $20,000 vehicle, that means putting down $2,000 to $4,000. This strategy not only saves you money on interest but also helps avoid being "upside down" on your loan, where you owe more than the car is worth, especially in the early years of ownership.

C. Loan Term (Duration): The Payment vs. Interest Trade-Off

The loan term is the length of time you have to repay your loan, typically expressed in months (e.g., 36, 48, 60, or 72 months). A shorter loan term means higher monthly payments but significantly less interest paid over the life of the loan. This is because you’re paying off the principal faster.

Conversely, a longer loan term results in lower monthly payments, making the car more "affordable" on a month-to-month basis. However, extending the term means you’ll pay substantially more in total interest. For a $20,000 car loan, choosing a 72-month term over a 48-month term could add thousands to your overall cost.

Common mistakes to avoid are solely focusing on the lowest possible monthly payment without considering the total cost. While a longer term might seem appealing, it can tie you to a depreciating asset for an extended period, increasing the risk of being upside down on your loan. Always weigh your monthly budget against the total interest paid.

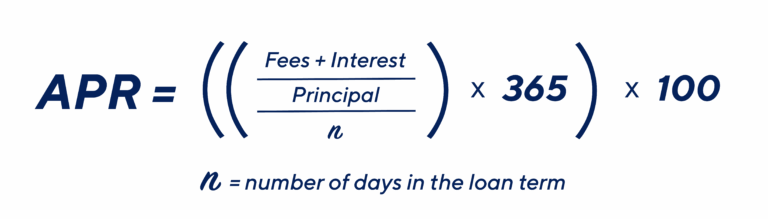

D. Interest Rate (APR): The True Cost of Borrowing

The interest rate, often expressed as an Annual Percentage Rate (APR), is the cost of borrowing money from a lender. It’s added to your principal balance and paid back over the loan term. Your APR is directly influenced by your credit score, down payment, and the chosen loan term.

A lower APR means you pay less for the privilege of borrowing the $20,000. Even a difference of one or two percentage points can translate into hundreds or even thousands of dollars saved over the life of the loan. This is why shopping around for the best rate is so crucial.

From our perspective, lenders consider various factors beyond your credit score, such as your debt-to-income ratio and employment history, when determining your APR. Demonstrating financial stability and a low debt burden can help you secure a more favorable rate. Don’t be afraid to negotiate, especially if you have a strong credit profile.

Where to Secure Your $20,000 Car Loan

Once you understand the factors that influence your loan, the next step is to explore your financing options. There are several avenues available for securing a $20,000 car loan, each with its own set of advantages and disadvantages.

A. Banks and Credit Unions: Traditional and Reliable

Traditional banks and credit unions are often the first stop for many car loan applicants. They offer competitive interest rates, especially to customers with good credit and existing banking relationships. Credit unions, in particular, are known for their member-focused approach and often provide slightly lower rates.

The application process with banks and credit unions can be a bit more structured, sometimes requiring in-person visits or extensive documentation. However, they typically offer personalized service and transparent loan terms. It’s a reliable choice for those who value established financial institutions.

B. Dealership Financing: Convenience at a Cost?

Many car dealerships offer in-house financing options, often through partnerships with various banks and captive finance companies (e.g., Toyota Financial Services, Ford Credit). This can be incredibly convenient, allowing you to handle the entire car-buying and financing process in one place.

While convenient, dealership financing might not always offer the absolute best rates. Dealers sometimes mark up interest rates to increase their profit. However, they can also have special promotions or incentives, especially on new vehicles, that might make their offer competitive.

Pro tips from us: Always get pre-approved for a loan from an outside lender (bank or credit union) before you visit the dealership. This provides you with a baseline interest rate and empowers you to negotiate. If the dealership can beat your pre-approval rate, great! If not, you already have a solid financing option.

C. Online Lenders: Speed, Variety, and Comparison

The digital age has brought forth a plethora of online lenders specializing in auto loans. These platforms offer unparalleled speed and convenience, allowing you to apply and get approved for a $20,000 car loan from the comfort of your home. They often provide quick decisions, sometimes within minutes.

Online lenders also excel at comparison shopping. Many platforms allow you to fill out one application and receive multiple loan offers from various lenders, making it easy to compare rates, terms, and fees side-by-side. This competitive environment can often lead to excellent deals.

When considering online lenders, ensure you choose reputable companies with strong customer reviews. Websites like Bankrate or NerdWallet can be great resources for comparing different online auto loan providers and understanding their offerings. Always read the fine print carefully before committing.

D. Private Seller Financing: Specific Considerations

While less common for a full $20,000 loan, it’s worth noting that some individuals might consider private party auto loans, especially for used cars. These loans are typically obtained from banks or credit unions, specifically designated for private party sales. Dealers usually handle the financing in-house.

If you’re buying a used car from a private seller, you’ll still need to secure financing from a traditional lender. The process is similar to buying from a dealer, but the lender will require specific vehicle information (VIN, mileage, condition) to approve the loan. Ensure you get a pre-purchase inspection for any private sale.

The Application Process for a $20,000 Car Loan: Step-by-Step

Applying for a car loan doesn’t have to be a daunting task. By following a structured approach, you can streamline the process and increase your chances of securing the best terms for your $20,000 car loan.

A. Pre-Approval: Your Secret Weapon

Getting pre-approved for a car loan is perhaps the most crucial step in the financing process. Pre-approval means a lender has provisionally agreed to lend you a specific amount (like $20,000) at a certain interest rate, based on a preliminary review of your credit and finances. This is before you even step foot in a dealership.

Why is it crucial? Pre-approval gives you immense negotiating power at the dealership. You walk in knowing exactly how much you can spend and what interest rate you qualify for. This shifts the focus from "Can I afford this car?" to "Which car do I want?" and allows you to negotiate the car’s price, not just the loan terms.

B. Gathering Documents: Be Prepared

Lenders require various documents to verify your identity, income, and financial stability. Having these ready beforehand will expedite your application process. While requirements can vary slightly, common documents include:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (2-3 months), W-2s, or tax returns (if self-employed).

- Proof of Residence: Utility bill or lease agreement with your current address.

- Social Security Number: For credit checks.

- Vehicle Information: If you’ve already chosen a car (VIN, make, model, mileage).

- Proof of Insurance: Required before driving off with the car.

C. Comparing Offers: Shop Around for the Best Deal

Never settle for the first loan offer you receive. Apply to several different lenders – banks, credit unions, and online providers. Each lender has its own criteria and risk assessment models, which means rates and terms can vary significantly for the same $20,000 car loan.

Compare not just the interest rate (APR) but also the loan term, any associated fees (origination fees, prepayment penalties), and the total cost of the loan. Use online calculators to see how different APRs and terms affect your monthly payment and overall expenditure. This due diligence can save you hundreds, if not thousands, of dollars.

D. Finalizing the Loan: Read the Fine Print

Once you’ve chosen the best offer, it’s time to finalize the loan. Before signing any documents, carefully read through the entire loan agreement. Understand every clause, especially those related to the interest rate, monthly payment, total loan amount, fees, and what happens if you miss a payment.

Don’t hesitate to ask questions if anything is unclear. Ensure all the agreed-upon terms are accurately reflected in the final paperwork. This is your last chance to catch any discrepancies before committing to your $20,000 car loan.

Budgeting and Affordability for Your $20,000 Car Loan

Securing a $20,000 car loan is only half the battle; ensuring it fits comfortably within your budget is the other. Many people focus solely on the monthly payment, but the true cost of car ownership extends far beyond that.

A. The 20/4/10 Rule: A Smart Guideline

A widely recommended guideline for car financing is the 20/4/10 rule:

- 20% Down Payment: Aim to put down at least 20% of the car’s purchase price. For a $20,000 car, that’s $4,000. This helps reduce your loan amount and often secures a better interest rate.

- 4-Year Loan Term: Keep your loan term to no more than four years (48 months). While longer terms offer lower monthly payments, they lead to significantly more interest paid and a higher risk of being upside down on your loan.

- 10% of Gross Income for Car Expenses: Your total monthly car expenses (loan payment, insurance, fuel, maintenance) should not exceed 10% of your gross monthly income. This ensures you have enough disposable income for other necessities and savings.

B. Beyond the Monthly Payment: The Hidden Costs

Your $20,000 car loan payment is just one piece of the puzzle. Overlooking other car-related expenses can quickly lead to financial strain.

- Insurance Costs: Car insurance is mandatory and can be a significant monthly expense, varying based on your age, driving record, vehicle type, and location. Get quotes before buying the car.

- Maintenance and Repairs: Every car requires regular maintenance (oil changes, tire rotations) and will eventually need repairs. Budget for these unforeseen costs.

- Fuel: Consider the vehicle’s fuel efficiency and your typical driving habits. A gas guzzler can quickly erode your budget.

- Registration and Fees: Annual registration, inspection fees, and potential emissions tests are recurring costs that vary by state.

C. Creating a Realistic Budget: Know Your Limits

Before committing to a $20,000 car loan, create a detailed personal budget. List all your income sources and fixed expenses (rent, utilities, existing loan payments). Then, factor in variable expenses (groceries, entertainment). This will show you exactly how much disposable income you have available for car payments and related costs.

Don’t stretch your budget thin. Leave some wiggle room for unexpected expenses or emergencies. Based on our experience, many car owners underestimate the cumulative cost of ownership. A prudent budget ensures your new car brings joy, not financial stress. For a deeper dive into managing your finances, consider reading our guide on "Budgeting for Your First Car: Smart Strategies for New Owners" (Internal Link Placeholder).

Common Mistakes to Avoid When Getting a $20,000 Car Loan

Even with all the right information, it’s easy to fall into common traps. Being aware of these pitfalls can save you significant money and stress.

- Not Getting Pre-Approved: As discussed, this is a powerful tool you should always leverage. Walking into a dealership without pre-approval puts you at a disadvantage.

- Focusing Only on Monthly Payments: This is perhaps the biggest mistake. A low monthly payment can be achieved by extending the loan term significantly, leading to a much higher total cost due to increased interest. Always ask for the total cost of the loan.

- Ignoring the Total Cost of the Loan: Beyond the monthly payment, understand the total amount you’ll pay over the life of the loan, including principal and all interest. This provides a clearer picture of affordability.

- Not Comparing Multiple Lenders: Relying on the first offer you receive, or solely on dealership financing, means you’re likely leaving money on the table. Always shop around.

- Buying More Car Than You Can Afford: It’s tempting to stretch for a slightly more expensive model, but stick to your budget. An extra $2,000 on the car price can add hundreds to your total loan cost and increase monthly payments.

- Neglecting Your Credit Score: Not knowing your credit score or trying to improve it before applying can lead to higher interest rates and limited loan options.

- Skipping a Test Drive or Inspection: For a $20,000 car, especially a used one, always test drive thoroughly and consider a pre-purchase inspection by an independent mechanic. This ensures you’re not financing a money pit.

Based on years of observing car buyers, these mistakes are surprisingly common. A little preparation and patience can prevent costly errors and ensure you get the best deal for your $20,000 car loan.

What If You Have Bad Credit and Need a $20,000 Car Loan?

While a strong credit score is ideal, it’s still possible to get a $20,000 car loan with bad credit. However, you’ll need to adjust your expectations and employ specific strategies. Lenders offering bad credit car loans often have higher interest rates to offset the increased risk.

Here’s how to approach it:

- Realistic Expectations: Accept that your interest rate will likely be higher, and your loan terms might be less flexible. Focus on getting approved first, with a plan to refinance later.

- Larger Down Payment: A substantial down payment can significantly improve your chances of approval and reduce your interest rate, even with bad credit. It shows the lender you’re serious and committed.

- Find a Co-Signer: If you have a trusted friend or family member with good credit, asking them to co-sign can dramatically improve your loan terms. Be aware that they become equally responsible for the debt.

- Subprime Lenders: Some lenders specialize in bad credit auto loans. While their rates are higher, they might be your only option. Research them thoroughly to ensure they are reputable.

- Focus on Rebuilding Credit: View this loan as an opportunity to rebuild your credit. Make all payments on time, every time. After 12-18 months of consistent payments, you might be able to refinance your $20,000 car loan at a lower rate. For more strategies on improving your credit, check out our guide on "Improving Your Credit Score: A Step-by-Step Guide" (Internal Link Placeholder).

Refinancing Your $20,000 Car Loan

Refinancing means taking out a new loan to pay off your existing car loan. This is a strategy many car owners use to secure better terms, especially if their financial situation has improved since they first took out the loan.

You might consider refinancing your $20,000 car loan if:

- Interest Rates Have Dropped: If market rates have fallen since you got your original loan, you might qualify for a lower APR.

- Your Credit Score Has Improved: If you’ve diligently worked on improving your credit score, you’re now a less risky borrower and can likely get a better rate.

- You Want Lower Monthly Payments: Refinancing to a lower interest rate or a longer term (though be mindful of total interest) can reduce your monthly outflow.

- You Want a Shorter Loan Term: If your financial situation allows, you might refinance to a shorter term to pay off the loan faster and save on interest.

The process for refinancing is similar to applying for your initial $20,000 car loan. You’ll shop around, compare offers from different lenders, and submit an application with your updated financial information. It’s a proactive way to manage your debt and potentially save a significant amount over time.

Conclusion: Your Path to a Smart $20,000 Car Loan

Navigating the process of securing a $20,000 car loan doesn’t have to be a source of stress. By understanding the key factors that influence your loan, exploring various financing avenues, and adopting a disciplined approach to budgeting, you can make an informed decision that benefits your financial future. Remember, preparation and comparison are your most powerful tools.

Always prioritize your financial well-being over the excitement of a new car. A smart $20,000 car loan is one that fits comfortably within your budget, allows you to save on interest, and contributes positively to your long-term financial health. With the insights provided in this guide, you are now well-equipped to drive away with confidence, knowing you’ve made the best possible choice for your next vehicle.