Navigating the Auto Financing Landscape: Your Expert Guide to the Car Loan Industry

Navigating the Auto Financing Landscape: Your Expert Guide to the Car Loan Industry Carloan.Guidemechanic.com

The dream of owning a car is a powerful one for many, symbolizing freedom, convenience, and independence. However, for the vast majority, this dream doesn’t materialize with a simple cash payment. This is where the car loan industry steps in, acting as the essential bridge between aspiration and reality. Understanding how auto loans work is not just about getting behind the wheel; it’s about making a smart financial decision that impacts your budget for years to come.

In this comprehensive guide, we’ll peel back the layers of the car financing world. We’ll delve into everything from the different types of car loans available to the intricacies of the application process, key factors affecting your rates, and expert strategies for securing the best deal. Our goal is to empower you with the knowledge and confidence to navigate the auto loan landscape like a seasoned professional, ensuring your car ownership journey starts on the right financial foot.

Navigating the Auto Financing Landscape: Your Expert Guide to the Car Loan Industry

Understanding the Car Loan Landscape: More Than Just a Loan

At its core, a car loan is a secured loan specifically designed for purchasing a vehicle. The car itself serves as collateral, meaning if you fail to make your payments, the lender can repossess the vehicle. This fundamental structure is what makes auto loans accessible to a broad range of consumers.

The car loan industry is a massive and dynamic sector, playing a crucial role in the global economy. It facilitates vehicle sales, supports manufacturing, and provides millions with essential transportation. Its widespread prevalence means competition among lenders is high, which can be a significant advantage for informed borrowers.

Based on my experience, many people view a car loan as a simple transaction, but it’s a complex ecosystem. Understanding the players involved is the first step toward smart car financing. You’ll encounter traditional banks, credit unions, and even specialized finance companies. Each offers distinct advantages and caters to different borrower profiles.

Who Are the Key Players in Car Financing?

The auto financing market is diverse, with various institutions vying for your business. Knowing who they are helps you shop smarter.

- Banks: Large financial institutions like Chase, Wells Fargo, or Bank of America offer competitive rates, especially for borrowers with strong credit. They often have established online platforms and branch networks.

- Credit Unions: These member-owned non-profits often provide lower interest rates and more flexible terms than traditional banks. Membership is usually required but often has broad eligibility criteria.

- Captive Finance Companies: These are financing arms of car manufacturers, such as Ford Credit, Toyota Financial Services, or GM Financial. They frequently offer attractive promotional rates and incentives, especially for new vehicles.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, or Carvana (which also sells cars) specialize in online applications, often providing quick approvals and competitive rates. They’re excellent for pre-approvals.

Each of these players has a unique lending philosophy and target demographic. Exploring options from multiple sources is crucial for securing the most favorable car loan terms.

Deciphering the Different Types of Car Loans

The term "car loan" is a broad umbrella covering several distinct financing products. Knowing the differences can significantly impact your financial strategy and the vehicle you choose. It’s not just about borrowing money; it’s about borrowing the right kind of money for your situation.

1. New Car Loans

These loans are for purchasing brand-new vehicles directly from a dealership. New car loans generally come with the lowest interest rates due to the vehicle’s higher value and expected longevity. Lenders perceive less risk with a new car.

Typically, the loan terms can extend for longer periods, sometimes up to 72 or even 84 months. While longer terms mean lower monthly payments, they also mean you pay more in total interest over the life of the loan. Pro tips from us: Always balance the monthly payment against the total cost of ownership.

2. Used Car Loans

Used car loans are for pre-owned vehicles. They usually carry slightly higher interest rates compared to new car loans because used cars have a shorter remaining lifespan and are perceived as having a higher risk of mechanical issues. The value also depreciates faster initially.

Loan terms for used cars are often shorter, typically ranging from 36 to 60 months. This is partly due to the car’s age and mileage, which limit its useful life as collateral. Ensure the loan term doesn’t outlast the vehicle’s reliable service.

3. Car Loan Refinancing

Refinancing involves taking out a new car loan to pay off your existing one. This strategy is primarily used to secure a lower interest rate, reduce your monthly payments, or change the loan term. It can be a game-changer if your credit score has improved since your original purchase.

Many people consider refinancing if they initially received a high-interest rate due to poor credit, or if market rates have dropped significantly. It’s essentially renegotiating your existing auto loan to better suit your current financial situation.

4. Lease vs. Buy: A Quick Distinction

While not strictly a "loan," leasing is an alternative form of car financing. When you lease, you’re essentially renting the car for a set period, typically 2-4 years, with mileage restrictions. You don’t own the vehicle and return it at the end of the term, or you can opt to buy it out.

Leasing often results in lower monthly payments than buying, but you don’t build equity. This article focuses on car loans (buying), where you take ownership and build equity over time. Understanding the difference is crucial for making the right choice for your lifestyle.

The Application Process: Your Step-by-Step Guide to Auto Financing

Securing a car loan might seem daunting, but breaking it down into manageable steps makes it much clearer. A well-prepared applicant is a confident applicant, and confidence often translates to better terms. This process is about demonstrating your reliability to lenders.

Step 1: Get Pre-Approved for Your Car Loan

This is arguably the most crucial first step in the entire car financing journey. Pre-approval means a lender has provisionally agreed to lend you a certain amount of money at a specific interest rate, based on a preliminary review of your credit and financial situation. It’s not a final offer but a strong indicator.

Based on my experience, having a pre-approval in hand transforms you into a cash buyer at the dealership. You know your budget before you even start shopping, which helps you negotiate on the car price, not just the monthly payment. It also provides a benchmark against any financing offers the dealership might present.

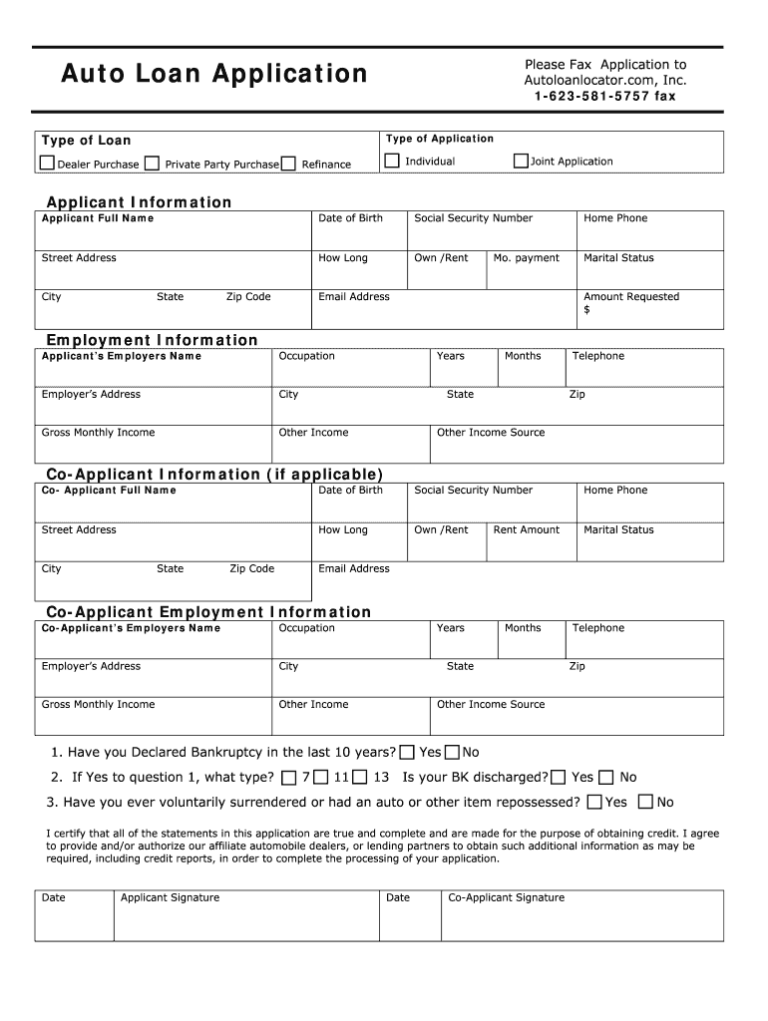

Step 2: Gather Your Required Documents

Lenders need to verify your identity, income, and financial stability. Having these documents ready speeds up the application process significantly.

- Proof of Identity: Driver’s license, passport, or state ID.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2 forms, tax returns (especially for self-employed individuals).

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: Essential for credit checks.

- Trade-in Information (if applicable): Title or registration for your current vehicle.

Step 3: Understand the Role of Your Credit Score

Your credit score is the single most important factor determining the interest rate you’ll be offered on a car loan. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt.

- FICO and VantageScore: These are the two primary credit scoring models. Scores typically range from 300-850.

- Good Credit (700+): Generally qualifies you for the lowest interest rates.

- Fair Credit (600-699): You’ll likely get approved, but with slightly higher rates.

- Poor Credit (below 600): Approval might be harder, and interest rates will be significantly higher to offset the lender’s perceived risk.

Common mistakes to avoid are not checking your credit score before applying. This simple check can help you identify errors and understand where you stand. You can get free credit reports annually from each of the three major bureaus (Equifax, Experian, TransUnion) at AnnualCreditReport.com.

Step 4: Your Debt-to-Income Ratio (DTI)

Lenders also assess your Debt-to-Income (DTI) ratio. This is the percentage of your gross monthly income that goes towards debt payments (including your potential new car payment). A lower DTI indicates you have more disposable income to handle new debt.

A DTI of 43% or less is generally preferred by lenders, though some might go higher depending on other factors. This metric helps lenders gauge your ability to comfortably afford the monthly auto loan payments.

Step 5: The Power of a Down Payment

A down payment is the initial amount of money you pay upfront towards the purchase of the vehicle. It directly reduces the amount you need to borrow, thereby lowering your monthly payments and the total interest paid over the loan’s life.

Based on my experience, a substantial down payment (typically 10-20% for new cars, 10% for used cars) can also improve your chances of approval and secure a better interest rate, especially if your credit isn’t perfect. It shows the lender your commitment and reduces their risk.

Key Factors That Dictate Your Car Loan Terms

Beyond your personal financial profile, several intrinsic elements of the car loan itself will shape your monthly payments and overall cost. Understanding these elements is fundamental to being an informed borrower. Don’t just look at the monthly payment; delve into the details.

1. The Interest Rate (APR)

The interest rate is the cost of borrowing money, expressed as a percentage of the principal. The Annual Percentage Rate (APR) includes not only the interest rate but also any additional fees charged by the lender, giving you a more complete picture of the annual cost.

- Fixed vs. Variable: Most car loans have a fixed interest rate, meaning it stays the same throughout the loan term. Variable rates, while less common for car loans, can fluctuate with market conditions.

- Impact: A lower APR directly translates to lower monthly payments and less total interest paid over the life of the loan. Even a small difference in APR can save you hundreds, if not thousands, of dollars.

2. The Loan Term

The loan term is the duration over which you agree to repay the auto loan, typically expressed in months (e.g., 36, 48, 60, 72, 84 months). This factor has a significant impact on both your monthly payment and the total cost.

- Shorter Terms: Higher monthly payments, but you pay less total interest and own the car outright sooner. This is often the more financially sound option if you can afford it.

- Longer Terms: Lower monthly payments, making the car more "affordable" on a month-to-month basis. However, you’ll pay significantly more in total interest, and you might find yourself "upside down" on the loan (owing more than the car is worth) for a longer period.

3. The Principal Amount

This is the actual amount of money you are borrowing after your down payment and any trade-in value have been applied. The larger the principal, the higher your monthly payments and total interest will be, assuming the same interest rate and term.

4. Fees and Charges

While not all car loans have extensive fees, it’s crucial to be aware of any potential additional costs.

- Origination Fees: A fee charged by some lenders for processing your loan application.

- Prepayment Penalties: Some loans might charge a fee if you pay off your loan early. This is less common with auto loans but worth checking.

- Late Payment Fees: Standard fees if you miss a payment deadline.

From my perspective, understanding these factors empowers you to not only compare offers effectively but also to negotiate better terms. Don’t hesitate to ask lenders for a full breakdown of all costs associated with the loan.

5. Collateral: The Car Itself

As mentioned earlier, the car you purchase serves as collateral for the auto loan. This means the lender has a legal right to repossess the vehicle if you default on your payments. The car’s value is critical to the lender’s risk assessment.

The lender will typically place a lien on the vehicle’s title, which is removed once the loan is fully paid off. This security is why car loans often have lower interest rates compared to unsecured personal loans.

Smart Strategies for Securing the Best Car Loan

Now that you understand the mechanics of car financing, let’s talk strategy. Getting a car loan isn’t just about applying; it’s about positioning yourself for the most favorable terms. These expert tips will help you save money and gain peace of mind.

1. Improve Your Credit Score

Before you even start shopping for a car, take steps to boost your credit score. Even a few points can make a difference in your interest rate.

- Pay Bills On Time: Payment history is the most significant factor in your credit score.

- Reduce Existing Debt: Especially credit card balances, as high utilization can hurt your score.

- Check for Errors: Review your credit report for any inaccuracies and dispute them immediately.

2. Save for a Substantial Down Payment

We’ve discussed the benefits, but it bears repeating: a larger down payment is your friend. It reduces the amount you need to borrow, cuts down your total interest, and minimizes the risk of being upside down on your loan. Aim for at least 10-20% of the car’s purchase price.

3. Shop Around for Your Car Loan

Never settle for the first car loan offer you receive, especially not solely from the dealership. Get pre-approvals from multiple lenders: banks, credit unions, and online lenders.

- Compare APRs: This is the most important number to compare, as it reflects the true annual cost of borrowing.

- Look at Loan Terms: Ensure the monthly payment and total interest align with your budget and financial goals.

- Consider All Fees: Factor in any origination fees or other charges.

Multiple loan applications within a short period (typically 14-45 days) are usually treated as a single "hard inquiry" on your credit report, minimizing the impact on your score. So, shop around confidently!

4. Negotiate Loan Terms

Don’t be afraid to negotiate, even with pre-approved offers. If you have multiple offers, you can leverage them to get an even better deal. Ask if the lender can match or beat a competitor’s APR. This is where your pre-approval becomes a powerful negotiation tool at the dealership.

5. Read the Fine Print of Your Car Loan Contract

Before signing anything, meticulously read the entire auto loan contract. Understand every clause, especially those related to:

- Interest Rate and APR: Confirm it matches what was agreed upon.

- Loan Term: Ensure it’s the correct number of months.

- Total Loan Amount: Verify it’s what you expect.

- Fees: Check for any hidden or unexpected charges.

- Prepayment Penalties: Confirm if any exist.

If anything is unclear, ask for clarification. A reputable lender will be happy to explain every detail. For up-to-date economic data and consumer insights, reputable financial news outlets or government financial agencies like the Consumer Financial Protection Bureau (CFPB) can be invaluable resources for understanding your rights and responsibilities as a borrower. (e.g., https://www.consumerfinance.gov/)

Post-Loan Management and Common Pitfalls to Avoid

Securing your car loan is a major achievement, but the journey doesn’t end there. Responsible post-loan management is crucial for protecting your credit and ensuring a smooth ownership experience. Being proactive can save you from potential financial headaches.

Making Payments On Time

This seems obvious, but consistent on-time payments are paramount. Every payment you make on time strengthens your credit history and contributes positively to your credit score. Conversely, even a single late payment can significantly damage your credit and incur late fees. Set up automatic payments to avoid missing due dates.

Refinancing Opportunities

Keep an eye on interest rates and your credit score throughout your loan term. If rates drop or your credit improves, refinancing your auto loan could save you a substantial amount of money. It’s often worth exploring if you’re halfway through a high-interest loan.

Early Payoff: Pros and Cons

Paying off your car loan early can save you a lot in interest, especially if you have a high APR. It also frees up monthly cash flow and removes a debt burden. However, consider if those extra funds could be better used elsewhere, such as paying off higher-interest debt or building an emergency fund. Always check for prepayment penalties before making extra payments.

Avoiding Repossession

If you face financial difficulties and anticipate missing car loan payments, do not wait. Contact your lender immediately. They may be willing to work with you by offering deferment options, modified payment plans, or other solutions to prevent repossession. Ignoring the problem will only make it worse.

The Future of Car Loans: Innovation on the Horizon

The car loan industry is constantly evolving, driven by technological advancements and shifting consumer expectations. Staying aware of these trends can help you prepare for future auto financing opportunities.

- Digitalization and AI: Expect even more streamlined, fully online application processes. Artificial intelligence and machine learning are increasingly used for faster, more accurate credit assessments, potentially offering personalized loan products.

- Sustainable Financing: With the rise of electric vehicles (EVs), specialized car loans for eco-friendly vehicles are becoming more prevalent. These might offer lower interest rates or unique incentives to encourage EV adoption.

- Personalized Products: Lenders are moving towards highly personalized auto loan offers based on individual driving habits, usage patterns, and even real-time financial data (with user consent).

- Blockchain Technology: While still in early stages, blockchain could eventually revolutionize loan security and transparency, though this is further down the road.

These innovations aim to make car financing more accessible, efficient, and tailored to the modern consumer.

Conclusion: Empowering Your Car Loan Journey

Navigating the car loan industry might seem complex, but with the right knowledge, it becomes an empowering journey. From understanding the various types of auto loans and mastering the application process to strategically shopping for the best terms, every step you take to educate yourself pays dividends. Remember, a car loan is a significant financial commitment, and making an informed decision is paramount to your financial well-being.

By applying the insights shared in this expert guide, you’re not just getting a loan; you’re making a smart investment in your transportation needs and your financial future. Be proactive, compare your options diligently, and always read the fine print. Armed with this comprehensive understanding, you are now well-equipped to secure a car loan that perfectly fits your budget and drives you towards your dreams. Start your journey to smart car financing today, and hit the road with confidence!