Navigating the Auto Loan Landscape: Your Ultimate Guide to Car Loan Institutions

Navigating the Auto Loan Landscape: Your Ultimate Guide to Car Loan Institutions Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle often involves securing financing. For many, this means understanding the intricate world of car loan institutions. Choosing the right lender can significantly impact your financial well-being, influencing everything from your monthly payments to the total cost of your car over its lifetime.

This comprehensive guide will demystify the various types of auto loan lenders, equip you with the knowledge to make informed decisions, and help you navigate the application process with confidence. We’ll dive deep into what makes each institution unique, the critical factors to consider, and how to secure the most favorable terms for your next vehicle purchase.

Navigating the Auto Loan Landscape: Your Ultimate Guide to Car Loan Institutions

Understanding the Pillars of Car Financing: Who Offers Auto Loans?

When you’re ready to finance a car, you’ll find a diverse array of car loan institutions vying for your business. Each type of lender has its own operational model, advantages, and disadvantages. Understanding these differences is crucial for finding a loan that aligns with your financial situation and preferences.

Let’s explore the primary players in the auto financing market.

1. Traditional Banks

Traditional banks are often the first place people consider for any type of loan, including car loans. These established financial institutions, such as Chase, Bank of America, Wells Fargo, and local community banks, offer a wide range of financial products and services. Their long-standing presence and familiar brand names provide a sense of security and trust for many borrowers.

Based on my experience, banks tend to offer competitive interest rates to borrowers with excellent credit histories. They often have robust online platforms for applications and account management, alongside physical branches for in-person support. However, their approval processes can sometimes be more stringent and slower compared to other lenders, especially for individuals with less-than-perfect credit.

Banks typically evaluate your credit score, income, debt-to-income ratio, and employment history very closely. They are looking for reliable borrowers who pose minimal risk. While they might offer a wide array of loan products, their flexibility for those with credit challenges can be limited.

2. Credit Unions

Credit unions are non-profit financial cooperatives owned by their members. Unlike banks, which are driven by shareholder profits, credit unions prioritize offering better rates and lower fees to their members. This fundamental difference often translates into some of the most competitive auto loan interest rates available on the market.

To access a credit union loan, you typically need to become a member, which usually involves meeting specific eligibility criteria such as living in a certain geographic area, working for a particular employer, or belonging to an affiliated organization. The membership process is generally straightforward and worth the effort for the potential savings.

Pro tips from us: Many of our clients find credit unions to be incredibly member-centric. They often provide more personalized service and might be more willing to work with borrowers who have slightly less-than-perfect credit, as long as they have a solid relationship with the institution. Their local focus often means a deeper understanding of community needs.

3. Dealership Financing (Captive and Third-Party)

Dealerships offer a convenient, one-stop shop for both purchasing a vehicle and securing financing. This can be especially appealing for buyers who prefer to streamline the entire process. However, it’s important to understand the two main forms of dealership financing.

Captive financing refers to loans offered directly through the car manufacturer’s own finance company, such as Ford Credit, Toyota Financial Services, or Honda Financial Services. These lenders are primarily focused on selling their brand’s vehicles and often provide promotional rates, cash-back offers, or special lease deals to incentivize purchases. They can be particularly attractive for new car buyers with strong credit.

Third-party financing through a dealership means the dealer acts as an intermediary, connecting you with external banks, credit unions, or other financial institutions from their network. While convenient, this approach might involve the dealer adding a markup to the interest rate they receive from the lender. This is where comparing offers before you step into the dealership becomes critical.

Common mistakes to avoid are solely relying on dealership financing without exploring other options. While convenient, it might not always be the cheapest. Always come prepared with a pre-approved loan offer from another institution to use as leverage in negotiations.

4. Online Lenders

The digital age has brought forth a new breed of car loan institutions: online lenders. Companies like LightStream, Capital One Auto Finance (online division), and Carvana (which also offers financing) operate primarily or exclusively online, often streamlining the application and approval process. Their digital-first approach can lead to quicker decisions and funding.

Online lenders typically leverage technology to assess creditworthiness efficiently, sometimes offering competitive rates to a broader spectrum of borrowers, including those with average credit. Their overhead costs can be lower than traditional banks with extensive branch networks, potentially translating into savings for consumers.

The convenience of applying from anywhere, at any time, is a major draw. However, the lack of in-person support might be a drawback for some. It’s essential to ensure any online lender you consider is reputable and transparent about their terms and conditions.

5. Specialty Lenders

Beyond the main categories, there are also specialty lenders who focus on specific niches, such as bad credit auto loans or loans for specific types of vehicles (e.g., RVs, motorcycles). These lenders often cater to individuals who may not qualify for traditional financing due to poor credit scores, past bankruptcies, or unique financial situations.

While they provide a vital service to borrowers who might otherwise be unable to secure a loan, the trade-off is often higher interest rates and potentially more restrictive terms. It’s crucial to thoroughly vet specialty lenders and understand all the costs involved before committing. They often take on higher risk, which is reflected in their pricing.

The Car Loan Process: From Application to Repayment

Understanding how auto loan lenders operate is just as important as knowing who they are. The process generally follows a similar path, regardless of the institution, but nuances exist.

1. Application and Pre-qualification

The first step is typically filling out a loan application. This involves providing personal and financial information, including your income, employment history, residence details, and social security number. Many lenders now offer a "pre-qualification" option.

Pre-qualification allows you to see potential loan terms and rates without a hard inquiry on your credit report. This is an invaluable tool for shopping around, as it doesn’t negatively impact your credit score. Based on my experience, getting pre-qualified by several lenders is one of the most powerful strategies for comparison shopping.

2. Credit Check and Underwriting

Once you submit a formal application, the lender will perform a hard credit inquiry. This allows them to access your detailed credit report and score, which are crucial for assessing your creditworthiness. They will also verify your income and employment.

The underwriting process involves the lender evaluating all the provided information to determine your eligibility, the maximum loan amount they are willing to offer, and the interest rate. They assess the risk involved in lending to you. A strong credit history and stable income significantly improve your chances of approval and securing favorable terms.

3. Loan Offer and Terms

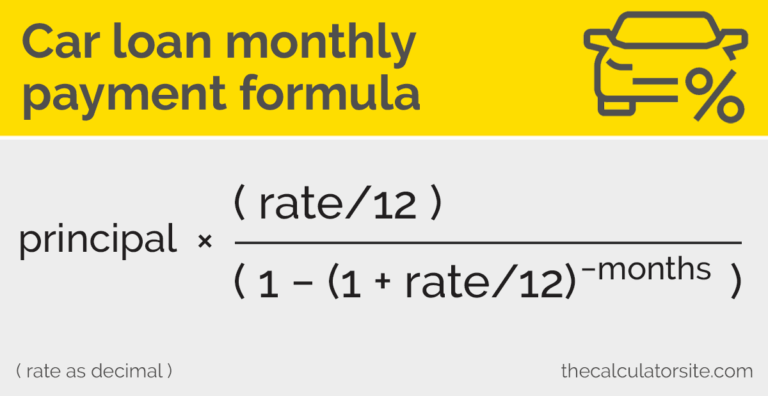

If approved, the lender will present you with a loan offer detailing the principal amount, the annual percentage rate (APR), the loan term (number of months), and your estimated monthly payment. The APR is particularly important as it represents the true cost of borrowing, encompassing the interest rate and any fees.

Pro tips from us: Always focus on the APR, not just the advertised interest rate. It gives you a more complete picture of what you’ll actually pay. Ensure you understand all aspects of the loan offer before moving forward.

4. Vehicle Selection and Finalization

With a pre-approval or loan offer in hand, you are in a stronger negotiating position at the dealership. You can focus on the car price, knowing your financing is already secured. Once you choose your vehicle, the lender will finalize the loan based on the specific car’s details and your agreed-upon terms.

This often involves signing loan documents, which formally obligate you to repay the loan according to the agreed schedule. Be sure to read every single document carefully before signing.

5. Repayment

Your repayment journey begins shortly after the loan is finalized, typically with your first payment due within 30-45 days. Most car loans are repaid in fixed monthly installments over the loan term. It’s crucial to make payments on time to avoid late fees and protect your credit score.

Key Factors to Consider When Choosing an Auto Loan Lender

With so many car loan institutions available, how do you narrow down your options? Several critical factors should guide your decision-making process.

1. Annual Percentage Rate (APR)

The APR is arguably the most significant factor. It’s not just the interest rate; it’s the total cost of borrowing expressed as an annual percentage, including interest and certain fees. A lower APR means lower overall costs for your loan.

Even a small difference in APR can translate to hundreds or thousands of dollars saved over the life of the loan. Always compare APRs across different lenders to find the most cost-effective option.

2. Loan Term

The loan term is the duration over which you will repay the loan, typically ranging from 24 to 84 months. A shorter loan term usually means higher monthly payments but less interest paid overall. Conversely, a longer loan term reduces your monthly payments but increases the total interest expense.

Common mistakes to avoid are extending the loan term simply to achieve a lower monthly payment without considering the increased total cost. While a longer term can make a car seem more affordable monthly, it often means paying significantly more in the long run.

3. Fees and Charges

Some auto loan lenders may charge various fees, such as origination fees, application fees, or prepayment penalties. While not all lenders impose these, it’s essential to ask about them upfront. These fees can add to the total cost of your loan.

A prepayment penalty, for instance, means you could be charged a fee if you pay off your loan early. This is less common with auto loans but still worth checking in the fine print.

4. Customer Service and Reputation

The lender’s reputation and quality of customer service can greatly influence your borrowing experience. Research reviews, check ratings, and consider how easily you can contact them if you have questions or issues. A reliable lender will offer transparent communication and efficient support.

Based on my experience, institutions with strong customer service often make the entire loan process smoother and less stressful. This is particularly true if you ever need to discuss payment adjustments or other loan modifications.

5. Eligibility Requirements

Each lender has specific criteria for loan approval. These typically include a minimum credit score, income requirements, and sometimes even residency restrictions. Before applying, review these requirements to ensure you meet them, saving you time and potential credit report inquiries.

For example, credit unions often have membership requirements, while some online lenders might cater specifically to certain credit tiers. Matching your profile to a lender’s typical borrower can improve your chances of approval.

Preparing for Your Car Loan Application

Being prepared can significantly improve your chances of securing the best possible car financing. Here’s what you need to do:

1. Know Your Credit Score

Your credit score is a numerical representation of your creditworthiness. Lenders use it to assess the risk of lending to you. A higher credit score (generally above 700) typically qualifies you for the lowest interest rates.

Access your credit report from all three major bureaus (Equifax, Experian, TransUnion) annually through AnnualCreditReport.com. Review it for accuracy and dispute any errors. If your score is low, take steps to improve it, such as paying bills on time and reducing existing debt. You can learn more about this in our article: Understanding Your Credit Score: A Comprehensive Guide (Internal Link 1).

2. Save for a Down Payment

A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan. It also shows lenders you’re serious and reduces their risk, potentially leading to better terms.

Aim for at least 10-20% of the vehicle’s purchase price if possible. A significant down payment can also help you avoid being "upside down" on your loan, where you owe more than the car is worth, especially common with new vehicles that depreciate quickly.

3. Establish a Budget

Before you even start looking at cars or loans, determine how much you can comfortably afford to pay each month. Factor in not just the loan payment, but also insurance, fuel, maintenance, and potential repair costs.

Pro tips from us: Use a budget calculator to ensure your total monthly car expenses don’t exceed 10-15% of your take-home pay. This prevents you from being "car poor."

4. Gather Necessary Documents

When applying for a loan, you’ll typically need:

- Proof of identity (driver’s license, passport)

- Proof of residence (utility bill, lease agreement)

- Proof of income (pay stubs, tax returns, bank statements)

- Social Security number

- Vehicle information (if you’ve already chosen a car)

Having these ready can expedite the application process.

Pro Tips for Securing the Best Car Loan

Navigating the world of auto loan lenders can be complex, but these strategies will give you an edge.

- Get Pre-Approved: As mentioned, pre-approval from banks or credit unions gives you concrete loan offers before you step into a dealership. This allows you to negotiate the car price as a cash buyer, separating the car purchase from the financing, which is a powerful position to be in.

- Shop Around Aggressively: Don’t settle for the first offer. Compare at least 3-5 loan offers from different car loan institutions. Your credit score won’t be significantly impacted if all inquiries are made within a short window (typically 14-45 days), as credit bureaus recognize you’re rate shopping.

- Negotiate the Price of the Car First: Always agree on the vehicle’s purchase price before discussing financing. This prevents the dealer from shifting profits from one area to another.

- Read the Fine Print: Thoroughly review all loan documents. Understand the APR, loan term, any fees, and the total amount you will pay over the life of the loan. Don’t hesitate to ask questions if anything is unclear.

- Consider Refinancing: If your credit score improves after taking out a loan, or if interest rates drop, you might be able to refinance your existing car loan for a better rate. This can save you a significant amount over time. We cover this in depth here: Refinancing Your Car Loan: When and Why It Makes Sense (Internal Link 2).

The Future of Car Loan Institutions

The landscape of car financing is constantly evolving. We’re seeing increasing innovation in online lending platforms, artificial intelligence for credit assessment, and greater transparency in loan offers. As technology advances, securing an auto loan may become even more streamlined and personalized.

However, the core principles remain: understanding your financial standing, comparing offers diligently, and choosing a reputable lender. Consumers who are informed and proactive will always be in the best position to secure favorable terms.

Conclusion: Empowering Your Auto Loan Decisions

Securing a car loan is a significant financial commitment. By thoroughly understanding the different car loan institutions, their operational models, and the key factors that influence your loan terms, you empower yourself to make intelligent decisions. Whether you choose a traditional bank, a member-focused credit union, a convenient online lender, or leverage dealership financing, knowledge is your most valuable asset.

Remember to prioritize a low APR, manageable loan terms, and transparent fees. Always prepare by checking your credit, saving for a down payment, and setting a realistic budget. With this comprehensive guide, you are well-equipped to navigate the auto loan landscape and drive away with confidence, knowing you’ve secured the best possible financing for your vehicle. For more detailed information on consumer finance and loans, consider consulting trusted external resources like the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov (External Link).