Navigating the Auto Loan Maze: How "Car Loan Com BBB" Can Be Your Ultimate Guide to Trustworthy Financing

Navigating the Auto Loan Maze: How "Car Loan Com BBB" Can Be Your Ultimate Guide to Trustworthy Financing Carloan.Guidemechanic.com

The open road beckons, a brand-new vehicle promising adventure and convenience. For many, this dream begins with a car loan – a financial commitment that can shape your budget for years to come. In today’s digital age, finding a reputable lender can feel like navigating a complex maze, with countless "Car Loan Com" options vying for your attention. How do you cut through the noise and identify a truly trustworthy partner?

This is where the Better Business Bureau (BBB) steps in, acting as a crucial beacon of trust and transparency. When you search for "Car Loan Com BBB," you’re not just looking for a company; you’re seeking validation, consumer feedback, and a clear picture of a lender’s ethical practices. This comprehensive guide will equip you with the knowledge to leverage the BBB effectively, understand the nuances of auto financing, and make an informed decision that secures your financial peace of mind.

Navigating the Auto Loan Maze: How "Car Loan Com BBB" Can Be Your Ultimate Guide to Trustworthy Financing

Understanding the Landscape: What is "Car Loan Com" and Why BBB Matters?

The term "Car Loan Com" often refers to the myriad online platforms and financial institutions offering auto loans. These can range from traditional banks and credit unions to specialized online lenders and dealership financing arms. The internet has made applying for a car loan incredibly convenient, but this convenience also brings a flood of options, some more reputable than others.

In this crowded digital space, consumer trust is paramount. You’re entrusting a company with significant personal financial information and committing to a long-term agreement. Therefore, thorough due diligence is not just recommended; it’s essential.

The Better Business Bureau (BBB) serves as an invaluable, non-profit organization dedicated to fostering trust between consumers and businesses. It provides a platform for consumers to research companies, file complaints, and see how businesses respond to issues. For a critical financial decision like a car loan, checking a lender’s BBB profile offers a vital layer of protection and insight into their operational integrity.

The Role of the Better Business Bureau in Car Loan Decisions

The BBB’s mission is straightforward: to be the leader in advancing marketplace trust. They achieve this by setting standards for ethical business behavior and then evaluating companies against these benchmarks. When you look up a "Car Loan Com" on the BBB website, you’re tapping into a rich repository of information.

This information includes a company’s BBB rating, details on their accreditation status, and a detailed history of consumer complaints and their resolutions. It’s a transparent window into how a business interacts with its customers, particularly when things don’t go as planned. Based on my experience, neglecting this step is one of the biggest mistakes consumers make.

The BBB acts as a neutral third party, offering an objective assessment that can be incredibly difficult to find elsewhere. It’s not just about finding a company; it’s about finding a company you can trust with one of your most significant purchases.

Deciphering BBB Ratings for Car Loan Companies: More Than Just a Letter

A company’s BBB rating is often the first thing consumers notice, ranging from A+ (highest) to F (lowest). While a quick glance at the letter grade is helpful, a truly informed decision requires a deeper understanding of what these ratings signify. It’s not just an arbitrary letter; it’s a comprehensive assessment.

An A+ rating typically indicates a business operates in a trustworthy manner, makes a good faith effort to resolve customer concerns, and has a strong track record. Conversely, an F rating signals significant unresolved issues, a pattern of poor customer service, or a failure to address complaints.

Several key factors influence a BBB rating. These include the volume and type of complaints filed against the business, how quickly and effectively the business resolves those complaints, and whether any government actions have been taken against them. The BBB also considers a company’s transparency in its business practices and how long it has been operating.

It’s crucial to understand the difference between a BBB rating and BBB accreditation. Accreditation is a voluntary process where a business pays a fee and agrees to adhere to the BBB’s standards of trust. While accreditation can be a positive sign, a high rating for a non-accredited business can still indicate reliability. Pro tips from us: Always prioritize the rating and the complaint history over just the accreditation badge. A company can be accredited but still have a less-than-stellar complaint record if they don’t resolve issues effectively.

Navigating BBB Complaints: A Deep Dive into Consumer Experiences

The real treasure trove of information on the BBB website lies within the complaint section. This is where you gain insight into real consumer experiences and how a "Car Loan Com" responds to challenges. To access this, simply search for the specific lender on the BBB website and navigate to their profile page. You’ll typically find a tab or section dedicated to customer complaints.

When reviewing complaints, you’ll encounter a variety of issues common to the car loan industry. These often include disputes over misleading terms or interest rates, unexpected or hidden fees that weren’t clearly disclosed, and aggressive collection practices. Some consumers report difficulties with loan modifications or deferrals, especially during times of financial hardship.

Customer service issues, such as unreturned calls or unhelpful representatives, are also frequently cited. In more severe cases, complaints may involve issues related to vehicle repossession, where consumers feel their rights were violated or proper procedures weren’t followed. Based on my experience, paying close attention to these patterns can reveal systemic issues within a company, rather than isolated incidents.

Beyond just reading the complaints, it’s vital to analyze the complaint resolution. Did the company respond promptly? Was the complaint resolved to the customer’s satisfaction? A company that consistently resolves complaints, even if they have many, often demonstrates a commitment to customer service. Conversely, a pattern of unresolved complaints, or responses that dismiss customer concerns, should raise a significant red flag. This detailed review helps you understand the true operational ethos of a potential lender.

Beyond the BBB: Holistic Due Diligence for Your Car Loan

While the BBB is an indispensable tool, it’s part of a larger ecosystem of due diligence you should perform before committing to a car loan. A truly informed decision requires looking at multiple angles.

Firstly, always compare multiple lenders. Don’t just settle for the first offer you receive, especially if it’s from a dealership. Shop around with banks, credit unions, and online lenders to ensure you’re getting the most competitive rates and terms. This simple step can save you thousands over the life of the loan.

Secondly, and perhaps most critically, read the fine print of any loan agreement. Seriously, read every single word. Pay close attention to the Annual Percentage Rate (APR), which includes both the interest rate and any additional fees. Look for prepayment penalties, which can cost you extra if you decide to pay off your loan early. Understand late fees, default clauses, and any clauses regarding vehicle repossession.

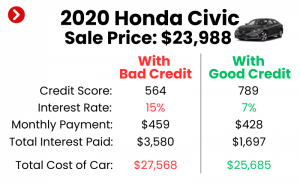

Understanding your credit score is also paramount, as it directly impacts the interest rates you’ll be offered. A higher score typically translates to lower rates, saving you money. You can get a free copy of your credit report from each of the three major bureaus annually. This allows you to check for errors and understand your financial standing.

Familiarize yourself with the difference between prequalification and pre-approval. Prequalification provides an estimate of what you might qualify for without a hard credit inquiry. Pre-approval, on the other hand, involves a hard credit pull but gives you a firm offer for a specific loan amount and rate. Having a pre-approval in hand empowers you to negotiate with confidence at the dealership.

Finally, consider other online review platforms like Yelp, Google Reviews, and Trustpilot. While these platforms can offer broader public sentiment, remember that BBB complaints often carry more weight due to their structured resolution process. For more severe consumer protection issues, you can also consult the Consumer Financial Protection Bureau (CFPB) website, which serves as a federal agency dedicated to protecting consumers in the financial marketplace. This is an excellent external resource for official government oversight.

Common Mistakes to Avoid When Seeking a Car Loan

Based on my experience, many consumers fall into similar traps when financing a vehicle. Avoiding these common mistakes can save you significant stress and money.

One of the most frequent errors is not checking your credit score before applying for a loan. Knowing your score empowers you to understand the rates you qualify for and spot any potential errors that could unfairly impact your application. Another common pitfall is only applying with one lender, especially if that lender is the dealership’s in-house financing arm. This limits your options and often results in higher interest rates.

Many consumers focus solely on the monthly payment, neglecting the total cost of the loan. A low monthly payment might seem attractive, but if it’s stretched over a very long term with a high interest rate, you’ll end up paying far more overall. Always consider the total amount you will repay.

Ignoring the fine print, as mentioned before, is another critical error. Hidden fees, unexpected penalties, or unfavorable terms can turn a seemingly good deal into a financial burden. Be wary of "guaranteed approval" scams, which often target individuals with poor credit. These typically come with exorbitant interest rates and predatory terms.

Lastly, not understanding the difference between simple interest and precomputed interest can be costly. Most modern car loans use simple interest, where interest is calculated on the remaining principal balance. Precomputed interest, less common now, calculates interest upfront, meaning you might not save as much by paying off the loan early. Pro tips from us: always confirm your loan uses simple interest to ensure maximum flexibility and savings.

Pro Tips for Improving Your Car Loan Chances & Terms

Securing the best possible car loan involves strategic planning. Here are some pro tips to put you in the driver’s seat.

Firstly, proactively boost your credit score well before you apply. Paying bills on time, reducing outstanding debt, and avoiding new credit applications can significantly improve your creditworthiness. A higher score directly translates to lower interest rates and better terms.

Secondly, save for a larger down payment. A substantial down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan. It also shows lenders you’re a lower risk.

Consider a shorter loan term if it’s affordable for your budget. While longer terms mean lower monthly payments, they also mean more interest paid overall. A shorter term saves you money in the long run and gets you out of debt faster.

Don’t forget that refinancing is always an option later on. If your credit score improves or interest rates drop after you’ve secured your initial loan, you might be able to refinance for a better rate and save money. Keep this in mind as a future strategy.

Have all your documents ready before you apply. This includes proof of income, identification, and residence. Being organized streamlines the application process and shows lenders you are a serious and prepared borrower. For more guidance on financial preparation, consider reading our article on "Understanding Your Credit Score: A Comprehensive Guide" for a deeper dive into credit management.

Finally, and perhaps most importantly, negotiate, negotiate, negotiate! Whether it’s the car price or the loan terms, everything is usually negotiable. Don’t be afraid to walk away if the deal doesn’t feel right. Your leverage increases when you have pre-approval from another lender.

When to File a Complaint (and How)

Despite your best efforts, sometimes issues still arise with a car loan company. If direct communication with your lender has failed to resolve a significant problem, filing a complaint with the BBB can be an effective next step.

You should consider filing a complaint when you experience issues like misleading information, unexpected fees, failure to honor agreed-upon terms, or persistent aggressive collection tactics. It’s also appropriate if customer service consistently fails to address your concerns or provides unhelpful responses.

To file a BBB complaint, visit their website and navigate to the "File a Complaint" section. You’ll need to provide details about the business, a clear and concise description of your issue, and what resolution you are seeking. Include all relevant documentation, such as loan agreements, correspondence, and payment records.

Once filed, the BBB will forward your complaint to the business and request a response. They act as a mediator, facilitating communication and working towards a resolution. The company typically has a set period to respond, and you will be notified of their proposed resolution. This process ensures a documented record of the issue and the company’s response, which can be invaluable. For broader consumer protection, you might also consider filing a complaint with the CFPB if the issue falls within their purview.

Conclusion: Your Smart Path to Car Loan Success

Securing a car loan is a significant financial decision, but it doesn’t have to be daunting. By leveraging resources like "Car Loan Com BBB," you empower yourself with the knowledge and insights needed to choose a reputable lender and secure favorable terms. Understanding BBB ratings, analyzing complaint histories, and performing comprehensive due diligence are not just steps; they are essential safeguards for your financial well-being.

An informed consumer is a powerful consumer. By asking the right questions, scrutinizing the fine print, and utilizing trusted resources, you can avoid common pitfalls and ensure your car loan journey is smooth and transparent. Your dream car awaits, but smart financing ensures the journey is smooth and your financial future remains secure. Prioritize trust, transparency, and thorough research, and you’ll be well on your way to owning your next vehicle with confidence.