Navigating the Bay State’s Roads: Your Ultimate Guide to the Car Loan Calculator Massachusetts

Navigating the Bay State’s Roads: Your Ultimate Guide to the Car Loan Calculator Massachusetts Carloan.Guidemechanic.com

Dreaming of cruising along the scenic Massachusetts coastline or navigating the bustling streets of Boston in a new set of wheels? For many, the journey to car ownership begins not on the showroom floor, but with a critical financial tool: the car loan calculator. In the Bay State, where unique regulations and a dynamic market shape auto financing, understanding your potential car loan is more than just smart—it’s essential.

This comprehensive guide will demystify the Car Loan Calculator Massachusetts, transforming you from a hesitant browser into a confident car buyer. We’ll delve deep into how these calculators work, what factors truly matter, and how you can leverage them to secure the best possible deal. Our goal is to equip you with the knowledge to make informed decisions, ensuring your Massachusetts car purchase is smooth, affordable, and perfectly aligned with your financial goals.

Navigating the Bay State’s Roads: Your Ultimate Guide to the Car Loan Calculator Massachusetts

I. Understanding the Massachusetts Car Market & Loan Landscape

Massachusetts boasts a vibrant and diverse automotive market, from compact city cars to robust SUVs designed for New England winters. While the thrill of finding the perfect vehicle is undeniable, the financial aspects often feel daunting. This is where a strategic approach to financing becomes paramount.

The financial landscape for car loans in Massachusetts has its own nuances. Consumer protection laws are robust, aiming to safeguard buyers from predatory practices. Understanding these regulations, alongside the standard financial variables, is crucial for any prospective car owner in the state. A general car loan calculator might give you a ballpark figure, but one tailored or understood within the context of Massachusetts provides far greater accuracy and peace of mind.

II. What Exactly is a Car Loan Calculator and How Does It Work?

At its core, a car loan calculator is a powerful online tool designed to estimate your potential monthly car payments. It takes several key pieces of information and, using a standard amortization formula, quickly provides you with a clear financial picture. Think of it as your personal financial forecaster for your next vehicle.

The primary purpose of this calculator is to empower you. It allows you to experiment with different loan scenarios before you even set foot in a dealership. This pre-planning helps you understand what you can truly afford, preventing the stress of unexpected monthly payments or an unsustainable financial burden.

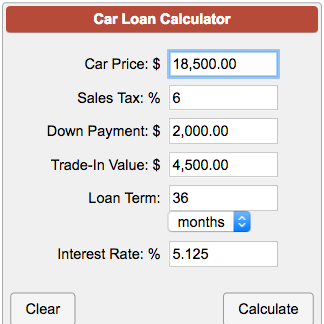

To generate an estimate, you typically input four main components: the total loan amount, the interest rate (APR), the loan term (duration), and any down payment you plan to make. The calculator then processes these inputs to reveal your estimated monthly payment and, often, the total interest you’ll pay over the life of the loan. It’s a straightforward process that yields invaluable insights.

III. The Core Components of Your Massachusetts Car Loan Calculation

Understanding the variables that feed into a Car Loan Calculator Massachusetts is key to manipulating it effectively. Each component plays a significant role in determining your final monthly payment and the total cost of your vehicle.

A. The Loan Amount: Your Starting Point

The loan amount isn’t simply the sticker price of the car. It’s the total sum you need to borrow after accounting for several other factors. This includes the vehicle’s purchase price, minus any down payment you make, and also factoring in your trade-in value, if applicable. Remember, the higher the loan amount, the higher your monthly payments will generally be. Carefully assess the actual price of the car you are considering.

B. Interest Rate (APR): The Cost of Borrowing

The Annual Percentage Rate (APR) is arguably the most critical factor. It represents the annual cost of borrowing money, expressed as a percentage of the loan amount. A lower APR means less money paid in interest over the life of the loan, leading to lower monthly payments and significant overall savings.

Several elements influence your APR, including your credit score, the loan term, the lender you choose, and prevailing market interest rates. In Massachusetts, as elsewhere, lenders assess your creditworthiness to determine the risk of lending to you. A strong credit history signals reliability, often unlocking more favorable rates. Based on my experience, even a small difference in APR can translate into hundreds or thousands of dollars saved over a typical 5-year car loan.

C. Loan Term: How Long Will You Pay?

The loan term is the duration, in months, over which you agree to repay the loan. Common terms range from 36 to 72 months, sometimes even longer. This choice presents a trade-off:

- Shorter Terms (e.g., 36-48 months): These typically come with higher monthly payments but result in less total interest paid over time. You pay off the loan faster, freeing up your budget sooner.

- Longer Terms (e.g., 60-72+ months): These offer lower monthly payments, making the car more "affordable" on a month-to-month basis. However, you’ll pay significantly more in total interest over the life of the loan, and your car’s depreciation might outpace your equity build-up.

Pro tips from us: While lower monthly payments can be tempting, always calculate the total cost over the entire loan term. A longer term might seem appealing upfront but can be a hidden financial drain.

D. Down Payment: Your Upfront Investment

A down payment is the initial amount of money you pay towards the purchase of the vehicle. This reduces the total amount you need to borrow. The power of a good down payment cannot be overstated.

- Reduces Loan Principal: Less money borrowed means less interest accrues.

- Lower Monthly Payments: A smaller loan amount directly translates to more manageable monthly payments.

- Improved Loan Terms: Lenders often view borrowers with substantial down payments as lower risk, potentially offering better interest rates.

- Avoid "Upside Down": A larger down payment helps prevent you from owing more on the car than it’s worth (being "upside down" or "underwater"), especially during the initial years of ownership when depreciation is highest.

Aiming for at least 10-20% of the vehicle’s purchase price as a down payment is a smart financial strategy.

E. Sales Tax & Fees in Massachusetts: Don’t Forget the Extras

When calculating your car loan, it’s crucial to factor in additional costs specific to Massachusetts. These aren’t typically included in the advertised price but significantly impact your total financed amount.

- Massachusetts Sales Tax: The current sales tax rate on vehicle purchases in MA is 6.25%. This is applied to the purchase price of the vehicle, after any trade-in credit.

- Registration Fees: You’ll need to pay fees to register your vehicle with the Massachusetts Registry of Motor Vehicles (RMV).

- Title Fees: A fee for processing the vehicle’s title.

- Documentation Fees ("Doc Fees"): Dealerships often charge a documentation fee for handling paperwork. While these are regulated to some extent, they can vary.

These additional costs can quickly add thousands to your total, so always include them in your financial planning. Many advanced car loan calculators allow you to input sales tax and other fees to get a more accurate picture of your total financed amount.

F. Trade-In Value: Reducing Your Loan Principal

If you’re trading in your current vehicle, its value can significantly reduce the amount you need to finance for your new car. The trade-in value is essentially treated like an additional down payment. Be sure to research your car’s trade-in value using reputable sources like Kelley Blue Book or Edmunds before heading to the dealership. This empowers you to negotiate effectively and ensures you get a fair price for your old vehicle.

IV. Step-by-Step: Using Your Car Loan Calculator Massachusetts Effectively

Maximizing the utility of a car loan calculator is straightforward. Follow these steps to get the most accurate and insightful results for your Massachusetts car purchase.

- Choose a Reliable Calculator: Opt for calculators from reputable financial institutions, automotive websites, or dedicated financial planning tools. Ensure it allows for the input of all key variables discussed above, including sales tax.

- Gather Your Financial Data: Before you start, have a clear idea of your budget, potential down payment, and an estimate of your credit score. If you have a trade-in, know its approximate value.

- Input the Variables:

- Vehicle Price: The agreed-upon selling price of the car.

- Down Payment: The amount you plan to pay upfront.

- Trade-In Value: If applicable, the value of your old car.

- Interest Rate (APR): Use an estimated rate based on your credit score. If unsure, use a slightly higher estimate to be conservative.

- Loan Term: Experiment with different terms (e.g., 36, 48, 60, 72 months).

- Massachusetts Sales Tax (6.25%): Most good calculators will have a field for this or you can add it to the loan amount.

- Other Fees: Add estimated registration, title, and documentation fees to your total loan amount or use a calculator that has fields for them.

- Interpret the Results: The calculator will instantly display your estimated monthly payment and often the total interest paid over the life of the loan. Pay attention to both figures. A low monthly payment might seem great, but if the total interest is exorbitant, it might not be the best deal.

- Run "What-If" Scenarios: This is where the calculator truly shines.

- What if you increase your down payment by $1,000?

- What if you choose a 48-month term instead of 60 months?

- What if you can secure an interest rate 0.5% lower?

By adjusting each variable, you can see its direct impact on your monthly payment and overall cost, helping you find your financial sweet spot.

Pro tips from us: Don’t just settle for the first calculation. Play around with different scenarios. For instance, see how much you save in total interest by slightly increasing your monthly payment. This iterative process is crucial for informed decision-making.

V. Beyond the Calculator: Securing the Best Car Loan in Massachusetts

While a Car Loan Calculator Massachusetts is an indispensable tool, it’s just one piece of the puzzle. To truly secure the best financing, you need a proactive strategy.

A. Improve Your Credit Score

Your credit score is the single most significant factor in determining the interest rate you’ll be offered. A higher score signifies lower risk to lenders, translating into better rates. Before applying for a loan, take steps to improve your credit:

- Pay all bills on time.

- Reduce outstanding debt.

- Avoid opening new credit accounts right before applying for a car loan.

- Check your credit report for errors and dispute them.

– Placeholder for an internal link to a credit score improvement article.

B. Shop Around for Lenders

Never take the first loan offer you receive. Different lenders—banks, credit unions, online lenders, and even dealership finance departments—will offer varying rates and terms based on their own risk assessments and business models.

- Credit Unions: Often known for competitive rates and personalized service, especially for members.

- Banks: Traditional lenders with a wide range of options.

- Online Lenders: Can offer quick approvals and competitive rates due to lower overheads.

- Dealership Financing: Convenient, but sometimes marked up. Use their offer as a negotiation point if you’ve already secured pre-approval elsewhere.

Compare at least three to five offers. This comparison shopping can save you thousands over the life of the loan.

C. Get Pre-Approved

Obtaining pre-approval for a car loan from an external lender (like your bank or credit union) before you visit the dealership is a powerful strategy.

- Know Your Buying Power: You’ll know exactly how much you can afford and at what interest rate.

- Negotiate with Confidence: You walk into the dealership as a cash buyer, which gives you leverage. You can negotiate the car’s price based on the best financing you’ve already secured.

- Avoid Pressure: You won’t feel pressured to accept the dealership’s financing simply because it’s convenient.

D. Negotiate Like a Pro

When it comes to negotiation, always focus on the total price of the car, not just the monthly payment. Dealers sometimes use low monthly payments to distract from a higher overall vehicle price or unfavorable loan terms. Be firm, do your research, and be prepared to walk away if the deal isn’t right.

E. Understand the Fine Print

Before signing any loan agreement, meticulously read every clause. Look out for:

- Prepayment Penalties: Fees for paying off your loan early.

- Hidden Fees: Any charges not clearly explained.

- Balloon Payments: A large lump sum payment due at the end of the loan term (rare for standard auto loans, but be aware).

Ensure you understand all the terms and conditions. If something is unclear, ask for clarification until you’re completely satisfied.

Common mistakes to avoid are: Focusing solely on the monthly payment, neglecting the total cost of the loan, not comparing offers from multiple lenders, and failing to read the entire loan agreement before signing. These oversights can cost you a significant amount of money over time.

VI. Massachusetts-Specific Considerations for Car Loans

While the general principles of car loans apply nationwide, Massachusetts has certain regulations and aspects that buyers should be aware of.

- Consumer Protection Laws: Massachusetts has strong consumer protection laws designed to protect buyers from unfair and deceptive practices. The Office of Consumer Affairs and Business Regulation is a valuable resource for understanding your rights as a car buyer in the state. – Placeholder for an external link.

- Insurance Requirements: Massachusetts law mandates minimum insurance coverage for all registered vehicles. Before you drive off the lot, you’ll need proof of insurance. Factor the cost of insurance into your overall monthly budget, as it’s a significant ongoing expense. – Placeholder for an internal link to a car insurance article.

- Sales Tax Exemption (Limited): While you pay 6.25% sales tax on the vehicle’s purchase price, if you trade in a vehicle, the value of your trade-in is deducted before the sales tax is calculated. This can provide a small but welcome saving.

- Lemon Law: Massachusetts has a "Lemon Law" that provides protection for buyers of new and, to a lesser extent, used cars that turn out to have significant, unfixable defects. While not directly related to the loan itself, it’s a critical protection for car owners in the state.

Being aware of these Massachusetts-specific details ensures you’re fully prepared for your car buying journey.

VII. The Long-Term Financial Impact of Your Car Loan

A car loan is a significant financial commitment that extends well beyond the initial purchase. Understanding its long-term impact is crucial for your overall financial health.

- Budgeting for Car Ownership: Your monthly car payment is just one piece of the puzzle. Remember to budget for fuel, insurance (which can be higher in urban Massachusetts areas), routine maintenance, and unexpected repairs. A holistic budget prevents financial strain.

- Building Equity: Over time, as you pay down your loan, you build equity in your vehicle. This means the car’s value exceeds the remaining loan balance. Having equity can be beneficial if you decide to sell or trade in the car in the future.

- Refinancing Options: If your credit score significantly improves after you’ve taken out your initial loan, or if market interest rates drop, you might be able to refinance your car loan for a lower interest rate or a more favorable term. This can lead to substantial savings over the remaining life of the loan.

Based on my experience: The smartest car buyers view their vehicle purchase as part of a larger financial plan. Don’t just think about today’s payment; consider the entire cost of ownership and how it fits into your future financial goals.

VIII. Frequently Asked Questions (FAQs) about Car Loans in MA

Q1: What’s a good interest rate for a car loan in Massachusetts?

A: Good interest rates vary based on your credit score, market conditions, and the loan term. Generally, excellent credit (720+) can qualify for rates below 5-6% for new cars, while lower scores will see higher rates. Always compare personalized offers.

Q2: Can I get a car loan with bad credit in Massachusetts?

A: Yes, it’s possible, but you’ll likely face higher interest rates. Lenders specializing in subprime loans might be an option, but be prepared for less favorable terms. A larger down payment can help improve your chances and reduce the overall cost.

Q3: Is it better to get a loan from a dealership or a bank/credit union in MA?

A: While dealership financing is convenient, it’s often best to get pre-approved by a bank or credit union first. This gives you a competitive offer to compare against any financing the dealership might offer, ensuring you get the best possible rate.

Q4: How does a trade-in affect my car loan in Massachusetts?

A: Your trade-in value acts like a down payment, reducing the amount you need to borrow. In Massachusetts, the trade-in value is also deducted from the purchase price before sales tax is calculated, saving you a bit more.

Conclusion

The journey to purchasing a car in Massachusetts, or anywhere for that matter, is an exciting one. However, the financial decisions involved can be complex. By mastering the Car Loan Calculator Massachusetts and understanding the factors that influence your financing, you empower yourself to make intelligent, informed choices.

This tool isn’t just about crunching numbers; it’s about gaining clarity, building confidence, and ultimately, securing a car loan that perfectly fits your budget and lifestyle. So, before you hit the road in your new ride, take the time to calculate, compare, and strategize. Your wallet will thank you. Start planning your Massachusetts car purchase today and drive away with confidence!