Navigating the Car Loan Crisis: Your Expert Guide to Understanding, Avoiding, and Overcoming Auto Debt Challenges

Navigating the Car Loan Crisis: Your Expert Guide to Understanding, Avoiding, and Overcoming Auto Debt Challenges Carloan.Guidemechanic.com

The rumble of a new car engine, the gleam of fresh paint – for many, owning a vehicle represents freedom, convenience, and a significant life milestone. However, beneath the polished exterior of the automotive market, a growing concern has been quietly accelerating: the car loan crisis. This isn’t just about individual financial woes; it’s a complex web of economic factors, lending practices, and consumer behavior that could have far-reaching implications.

As an expert blogger and professional SEO content writer, I’ve closely observed the shifts in consumer finance, and the auto loan sector presents a particularly interesting and often precarious landscape. This article will serve as your ultimate guide, delving deep into what the car loan crisis truly entails, its causes, warning signs, and most importantly, how you can navigate these challenging waters to protect your financial future. We’re here to equip you with the knowledge to make informed decisions and avoid becoming another statistic.

Navigating the Car Loan Crisis: Your Expert Guide to Understanding, Avoiding, and Overcoming Auto Debt Challenges

What Exactly is the Car Loan Crisis? Defining the Problem

When we talk about a "car loan crisis," we’re referring to a situation where a significant portion of consumers are struggling to manage their auto loan debt. This manifests in rising delinquency rates – borrowers falling behind on their payments – and an increasing number of repossessions. It’s a systemic issue, not just isolated incidents of bad luck.

Currently, the total outstanding auto loan debt in the United States alone has swelled to staggering levels, often exceeding $1.5 trillion. This sheer volume of debt, combined with specific lending trends, creates a fertile ground for instability. It’s a weight that many households are carrying, and for some, it’s becoming too heavy to bear.

One of the most significant contributors to this burgeoning problem is the proliferation of subprime auto loans. These are loans extended to borrowers with lower credit scores, typically below 620-660, who are deemed to have a higher risk of default. While they offer a path to car ownership for those who might otherwise be excluded, they often come with much higher interest rates and less favorable terms, setting borrowers up for potential financial distress.

Based on my experience observing market trends, the rise in subprime lending isn’t accidental. It’s often a response by lenders to a competitive market and a way to expand their customer base. However, without adequate safeguards and responsible underwriting, this practice can lead to a precarious situation for both the borrower and the broader financial system.

The Roots of the Problem: Why Are We Here?

Understanding the car loan crisis requires looking at the confluence of factors that have brought us to this point. It’s not a single cause, but rather several interconnected elements that have fueled the growth of auto loan debt. Let’s break down these underlying issues.

Easy Credit Availability and Extended Loan Terms

One primary driver has been the relative ease with which consumers can obtain credit for car purchases. For years, low interest rates have made borrowing seem more affordable, encouraging more people to take out loans. This has been coupled with a significant trend towards longer loan terms.

It’s no longer uncommon to see car loans stretching for 72, 84, or even 96 months. While these extended terms reduce the monthly payment, making a car seem more affordable on a superficial level, they dramatically increase the total amount of interest paid over the life of the loan. This also means that borrowers spend a longer time underwater, owing more than the car is worth, a concept known as negative equity.

Rising Vehicle Prices: New and Used Cars

Another undeniable factor is the relentless increase in vehicle prices. Whether you’re eyeing a brand-new sedan or a pre-owned SUV, cars are simply more expensive than they used to be. This surge is due to a variety of reasons, including technological advancements, supply chain issues, and increased demand.

As car prices climb, the amount people need to borrow also increases. This directly translates to larger loan principals and, consequently, higher monthly payments or longer loan terms to keep those payments "affordable." It’s a vicious cycle where the cost of entry into car ownership keeps rising.

The Surge in Subprime Lending Practices

As previously mentioned, subprime auto loans play a critical role in the crisis. Lenders, in their pursuit of market share and profits, have sometimes loosened their lending standards. This means approving loans for individuals with less-than-stellar credit histories, who might have unstable incomes or high debt-to-income ratios.

While providing access to credit, this practice can be predatory if not managed responsibly. These loans often carry exorbitant interest rates, sometimes in the double digits, making them incredibly difficult for borrowers to repay, especially if they encounter any financial setbacks. Common mistakes to avoid are accepting the first loan offer without comparison or signing up for terms you don’t fully understand.

Consumer Behavior and Overstretching Budgets

Consumers themselves also contribute to the problem. The desire for a newer, nicer, or more feature-rich vehicle can sometimes override financial prudence. Many individuals opt for cars that stretch their budgets thin, often without a substantial down payment. This can lead to financial distress down the line.

The allure of low monthly payments, facilitated by long loan terms, can mask the true total cost of the vehicle. People might focus solely on the immediate affordability without considering the long-term financial commitment. Pro tips from us: always scrutinize loan terms beyond the monthly payment; look at the total cost of the loan including all interest and fees.

Broader Economic Pressures

Finally, wider economic conditions significantly impact the ability of consumers to manage their car loans. Inflation, which erodes purchasing power, means that other essential costs like housing, food, and utilities are also increasing. For many, wages haven’t kept pace with these rising expenses.

This squeeze on household budgets leaves less disposable income available for car payments. When an unexpected expense arises – a medical bill, a home repair, or job loss – the car payment is often one of the first obligations to become challenging, potentially leading to delinquency.

Warning Signs: How to Spot Trouble Before It Hits

Recognizing the early indicators of financial strain, both personally and systemically, is crucial for avoiding the full brunt of the car loan crisis. Awareness is your first line of defense. Let’s look at the red flags.

For Individuals: Personal Indicators of Trouble

If you find yourself experiencing any of these situations, it’s time to take a serious look at your car loan situation:

- High Debt-to-Income Ratio: Your monthly debt payments, including your car loan, consume a disproportionately large percentage of your gross income. A good rule of thumb is to keep total debt payments below 36% of your income.

- Struggling with Monthly Payments: You consistently find yourself short on funds when the car payment is due, or you have to choose between your car payment and other essential bills. This is a clear sign of overextension.

- Negative Equity (Being "Upside Down"): You owe more on your car loan than the car is currently worth. This is particularly dangerous because if your car is totaled or stolen, insurance payout might not cover the remaining loan balance, leaving you still owing money for a car you no longer have.

- Constant Refinancing: You’re frequently refinancing your car loan, especially just to lower your monthly payment without reducing the principal significantly. This often extends the loan term further, costing you more in the long run.

- Rolling Negative Equity into a New Loan: A common mistake to avoid is trading in a car with negative equity and having that outstanding balance added to your new car loan. This immediately puts you upside down on the new vehicle and escalates your overall debt burden.

For the Economy: Systemic Indicators

Beyond individual struggles, there are broader economic trends that signal a worsening car loan crisis:

- Rising Delinquency Rates: A consistent upward trend in the percentage of borrowers who are 30, 60, or 90+ days late on their payments. This is a primary indicator of widespread financial stress.

- Surge in Repossessions: An increase in the number of vehicles being repossessed by lenders. This signifies that a growing number of borrowers are unable to meet their financial obligations.

- Declining Used Car Values: If many repossessed cars flood the market, it can drive down the value of used vehicles. For individuals, this worsens negative equity issues and makes it harder to sell a car to escape a bad loan.

The Ripple Effect: Broader Economic and Personal Impacts

The car loan crisis isn’t just about a missed payment; it creates a cascade of negative consequences that can severely impact individuals and potentially reverberate through the wider economy. Understanding these impacts underscores the urgency of addressing the problem.

Personal Impacts: Financial Distress and Damaged Futures

For individuals caught in the grip of car loan trouble, the repercussions can be severe and long-lasting. The most immediate impact is on your credit score. Missed payments and repossessions are major derogatory marks that can significantly lower your score, making it harder to secure other forms of credit like mortgages, personal loans, or even rental agreements in the future.

Beyond credit, the stress of constant financial worry takes a heavy toll on mental and emotional well-being. The threat of repossession can be incredibly frightening, leading to anxiety and instability. If your car is repossessed, you lose your primary mode of transportation, which can impact your ability to get to work, care for family, and maintain daily life, further exacerbating financial difficulties.

In cases of repossession, borrowers might still owe a "deficiency balance" if the sale of the repossessed vehicle doesn’t cover the remaining loan amount and associated fees. This means you could be without a car and still be pursued by the lender for the outstanding debt, a truly devastating scenario.

Economic Impacts: A Broader Financial Instability

While a car loan crisis might not trigger a recession on the scale of a housing crisis, its economic implications are not to be underestimated. A downturn in the auto sector can affect manufacturing, sales, and related industries, leading to job losses. Lenders face losses from defaulted loans, which can tighten credit standards across the board, making it harder for even creditworthy individuals to borrow.

Furthermore, when consumers are spending a disproportionate amount of their income on car payments or dealing with car loan debt, they have less money for other goods and services. This reduction in consumer spending can slow economic growth across various sectors, creating a broader ripple effect throughout the economy. It’s a subtle but persistent drag on overall economic health.

Navigating the Storm: Strategies for Individuals to Avoid or Mitigate the Crisis

The good news is that with awareness and proactive steps, you can either avoid falling into the car loan crisis or mitigate its impact if you’re already struggling. It’s all about informed decision-making and responsible financial planning.

Before Buying: Smart Preparations

The best defense is a good offense. Your preparation before even stepping onto a car lot is paramount.

- Do Your Research: Understand the true market value of the car you’re interested in, both new and used. Don’t rely solely on the dealership’s numbers.

- Create a Realistic Budget: Determine how much you can truly afford for a monthly car payment, including insurance, fuel, maintenance, and registration. A common mistake to avoid is only factoring in the loan payment without these other significant costs. Pro tips from us: your total car expenses (payment, insurance, gas, maintenance) should ideally not exceed 10-15% of your net monthly income.

- Save for a Substantial Down Payment: Aim for at least 10-20% of the car’s price. A larger down payment reduces the amount you need to borrow, lowers your monthly payments, and helps you avoid negative equity from the start.

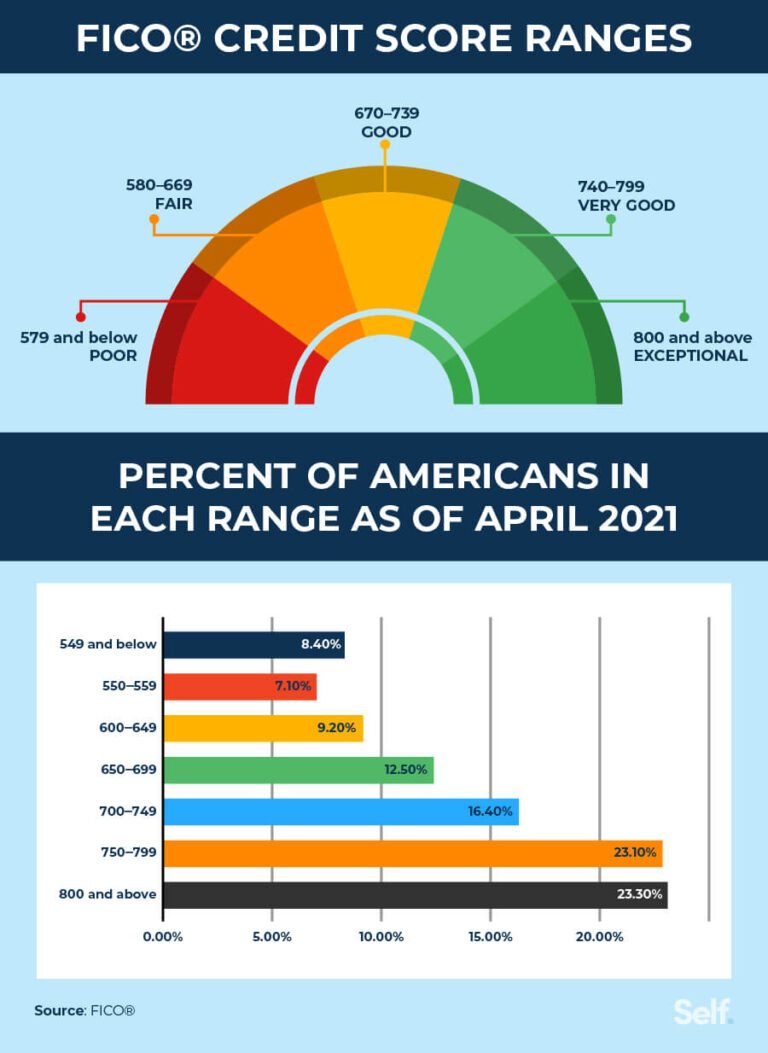

- Understand Your Credit Score: Check your credit report and score before you apply for a loan. This gives you leverage in negotiations and helps you anticipate the interest rates you’ll be offered. could be a helpful resource here.

During Loan Application: Smart Borrowing Practices

Once you’re ready to buy, approach the loan application process strategically.

- Shop Around for Lenders: Don’t just accept the financing offered by the dealership. Get pre-approved by several banks, credit unions, and online lenders. This allows you to compare interest rates and terms, giving you the power to choose the best option.

- Negotiate Terms, Not Just Price: Focus on the total cost of the loan, including the interest rate, loan term, and any fees, not just the monthly payment. A lower monthly payment over a longer term often means paying much more overall.

- Avoid Unnecessary Add-ons: Be wary of extended warranties, GAP insurance (unless necessary and priced fairly), and other dealership extras that significantly inflate the loan amount. Only agree to what you genuinely need.

- Read the Fine Print: Always read the entire loan agreement before signing. Understand all clauses, penalties for late payments, and early payoff options.

After Loan Approval: Responsible Management

Once you have the car and the loan, ongoing management is key.

- Pay On Time, Every Time: This is fundamental for maintaining a good credit score and avoiding late fees. Set up automatic payments to ensure consistency.

- Consider Extra Payments: If you have extra cash, even paying a little more than your minimum monthly payment can significantly reduce the total interest paid and shorten the loan term. Designate extra payments specifically towards the principal.

- Refinancing Options (with Caution): If interest rates have dropped or your credit score has improved, refinancing might be an option to get a lower rate or a more favorable term. However, be cautious not to extend the loan term unnecessarily, which could increase total interest paid.

- Understand Negative Equity: Stay aware of your car’s value relative to your loan balance. provides more details on this.

If You’re Struggling: Taking Action

If you find yourself struggling to make payments, don’t panic or ignore the problem. Proactive communication is vital.

- Communicate with Your Lender: Contact your lender as soon as you anticipate a problem. They may be willing to work with you on a temporary payment deferral, a revised payment plan, or other options.

- Explore Deferment or Forbearance: Some lenders offer programs to temporarily pause or reduce payments, often with interest still accruing. Understand the terms carefully.

- Consider Debt Consolidation (with Caution): If you have multiple high-interest debts, consolidating them into a single loan with a lower interest rate might free up cash. However, ensure the new loan’s terms are truly beneficial and don’t just shift the problem.

- Selling the Car: If all else fails and you have positive equity, selling the car to pay off the loan might be the best option to avoid repossession and further credit damage. If you have negative equity, you might need to cover the difference out of pocket, but it could still be better than a repossession.

The Role of Lenders and Regulators: Towards a More Sustainable Future

While individual responsibility is paramount, the wider financial ecosystem also has a significant role to play in preventing and mitigating the car loan crisis. This involves both the practices of lending institutions and the oversight provided by regulatory bodies.

Responsible Lending: A Foundation for Stability

Lenders bear a crucial responsibility to ensure they are not extending credit to borrowers who are unlikely to repay. This involves robust underwriting processes, where a thorough assessment of a borrower’s income, debt, and credit history is conducted. Based on my observations of market behavior, a focus purely on profit margins without adequate risk assessment can lead to systemic problems.

Transparency is another key aspect of responsible lending. Borrowers should be provided with clear, easy-to-understand information about all loan terms, including the annual percentage rate (APR), total cost of the loan, and any associated fees. Hidden clauses or complex jargon only serve to confuse borrowers and can lead to poor decision-making. Lenders should also avoid pushing unnecessary add-on products that inflate the loan amount.

Regulatory Oversight: Protecting Consumers and the Market

Government agencies and regulatory bodies play a vital role in setting standards and enforcing fair lending practices. The Consumer Financial Protection Bureau (CFPB) in the United States, for instance, aims to protect consumers by ensuring that financial markets are fair, transparent, and competitive. Such bodies can investigate predatory lending practices, set limits on interest rates for certain types of loans, and issue guidelines for responsible underwriting.

Effective regulation helps to prevent a race to the bottom where lenders compromise standards to gain market share. It creates a level playing field and protects vulnerable consumers from exploitative practices. While striking a balance between consumer protection and market innovation is challenging, strong oversight is essential for maintaining the health and stability of the auto loan market. This might include stricter reporting requirements for subprime loans or increased scrutiny of dealerships’ financing departments. External Link: Learn more about the CFPB’s work on auto loans here: Consumer Financial Protection Bureau (CFPB) – Auto Loans

Proactive Steps for a Healthier Financial Future

Beyond immediate solutions, fostering long-term financial health is the ultimate protection against any future car loan crisis or other financial setbacks. These steps empower you to build resilience and make confident financial decisions.

- Build an Emergency Fund: Aim to save at least three to six months’ worth of living expenses in an easily accessible savings account. This fund acts as a buffer against unexpected events like job loss, medical emergencies, or significant car repairs, preventing you from missing loan payments.

- Prioritize Improving Credit Health: Consistently pay all your bills on time, keep credit card balances low, and avoid opening too many new credit accounts. A higher credit score opens doors to better interest rates and more favorable loan terms across all types of borrowing.

- Invest in Financial Literacy Education: Take the time to learn about personal finance, budgeting, investing, and understanding credit. The more knowledgeable you are, the better equipped you’ll be to make sound decisions and recognize potential pitfalls. There are numerous free resources available online and through community programs.

- Consider Alternatives to New Car Purchases: Don’t feel pressured to always buy new. Well-maintained used cars, reliable public transportation, ride-sharing, or even electric bicycles can be excellent, more affordable alternatives depending on your lifestyle and location. Challenge the societal expectation that a brand-new car is a necessity.

- Live Below Your Means: This fundamental principle of financial success involves consciously spending less than you earn. By consistently doing so, you create surplus funds that can be used for savings, investments, or making extra payments on debt, accelerating your journey to financial freedom.

Conclusion: Driving Towards Financial Stability

The car loan crisis is a complex and evolving challenge, but it’s not insurmountable. By understanding its underlying causes, recognizing the warning signs, and implementing proactive strategies, both individuals and the industry can work towards a more stable and sustainable future. This isn’t just about avoiding debt; it’s about empowering yourself with financial literacy and making choices that align with your long-term well-being.

Remember, a car is a tool, not a trophy. Making responsible financial decisions about your auto loan can protect your credit, reduce stress, and free up your resources for other important life goals. Don’t let the allure of a shiny new vehicle drive you into a financial ditch. Instead, take the wheel with confidence, armed with knowledge, and steer yourself towards a path of lasting financial security.

What are your thoughts or experiences with car loans? Share your insights in the comments below – your perspective can help others navigate this critical issue!